Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

OSC Staff Notice: 33-745 - 2014 Annual Summary Report for Dealers, Advisers and Investment Fund Managers

OSC Staff Notice: 33-745 - 2014 Annual Summary Report for Dealers, Advisers and Investment Fund Managers

OSC Staff Notice 33-745 -- Compliance and Registrant Regulation -- Annual Summary Report for Dealers, Advisers and Investment Fund Managers is reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the Staff Notice.

Annual Summary Report for Dealers, Advisers and Investment Fund Managers

Compliance and Registrant Regulation

OSC Staff Notice 33-745

September 25, 2014

DIRECTOR'S MESSAGE

The Ontario Securities Commission (OSC) expects strong compliance by registrants and articulates its expectations through its oversight, guidance and outreach. Registrants have an obligation to deal fairly, honestly and in good faith with their clients so they can invest with confidence, which is essential to the integrity of the capital markets of Ontario.

To assist registrants with meeting their regulatory obligations, the OSC's Compliance and Registrant Regulation Branch (CRR) has focused its efforts on enhancing communication with registrants and providing tools to assist them with maintaining effective compliance systems. We launched a new Registrant Outreach Program in September, 2013 with the objective of opening the lines of communication between registrants and CRR and creating a central repository of tools and information that will assist registrants in maintaining effective compliance systems. Since the launch of the program, more than 2,000 people have attended educational seminars either in-person or via webinar and the feedback has been overwhelmingly positive. As we continue to add more resources to the Registrant Outreach Program, we encourage registrants to check the program's webpage frequently for updates.

In addition to this report, CRR staff has published topic-specific guidance to assist registrants with meeting their regulatory obligations. For example, we published guidance to help registrants meet their Know Your Client (KYC), Know Your Product (KYP) and suitability obligations as well as guidance to help investment fund managers avoid common issues when managing their investment funds. KYC, KYP and suitability obligations are among the most fundamental obligations owed by registrants to their clients, and we continue to see issues with the way registrants fulfill these obligations, so this will remain a focus for CRR.

We also use the traditional tools of on-site compliance reviews and sweeps to identify compliance deficiencies, where appropriate, at each firm we review. The remediation of these deficiencies through dialogue with CRR staff provides an opportunity to enhance compliance systems. Also, the data collected from the 2014 Risk Assessment Questionnaire will help us to focus our resources on higher-risk issues and registrants. CRR staff will commence on-site reviews based on this new data by the end of the year.

To better serve the registrant community, we created a new registration team within CRR and added the position of Manager, Registration. By pooling our registration resources under this one team, we will gain efficiencies and enhance internal practices. Also, registration is an important gatekeeper function and the team is enhancing the registration process by developing a new initiative that will move the initial registration for firms closer to a "first compliance review." This initiative is under development, but firms that seek registration for the first time can expect that we will request additional information and potentially an in-person meeting as part of the registration process. This will allow us to focus on the firm's fitness for registration, enhancing the firm's understanding of regulatory obligations prior to registration and establishing positive communications with the registrant. Registrants and CRR staff will benefit from open communications about current regulatory obligations and practices.

Increasing our engagement with registrants was one of CRR's goals which aligned with the expansion of the OSC's direct outreach to market participants in 2013-14. Open communication with registrants gives CRR staff valuable insights into how registrants are adapting to the changes in the market environment and investor expectations. We are delighted with the participation and feedback we have received regarding our efforts to engage with our registrant community. It has been a constructive dialogue about strengthening the culture of compliance with Ontario securities law in the shared interest of protecting investors and fostering fair and efficient capital markets. We look forward to continuing the dialogue with our registrant community.

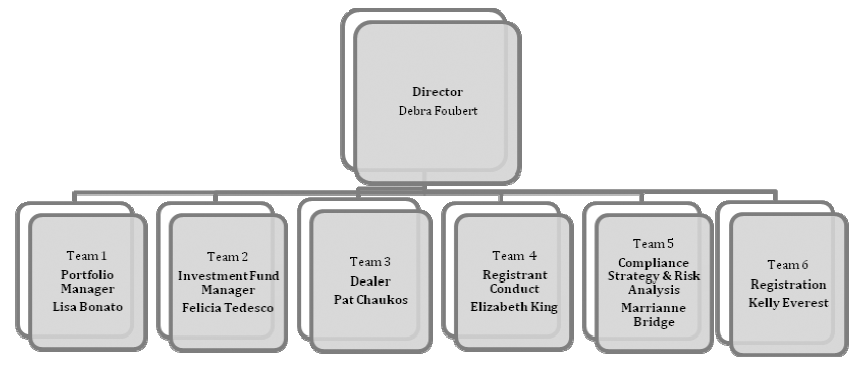

Debra Foubert

Director, Compliance and Registrant Regulation Branch

Introduction

The regulatory framework for Ontario's capital markets is designed to provide protection to investors while fostering fair and efficient capital markets.

Ontario Securities Commission Notice 11-769 -- Statement of Priorities

This annual summary report prepared by the CRR Branch (the annual report) provides information for registered firms and individuals (collectively, registrants) that are directly regulated by the OSC. These registrants primarily include:

• exempt market dealers (EMDs)

• scholarship plan dealers (SPDs)

• advisers (portfolio managers or PMs) and

• investment fund managers (IFMs).

The OSC's CRR Branch registers and oversees firms and individuals in Ontario that trade or advise in securities or act as IFMs.

|

Individuals |

Firms |

|

|

|

|

|

||||

|

66,210 |

1,056{1} |

|

|

|

|

|

||||

|

|

PMs |

EMDs |

SPDs |

IFMs |

|

|

||||

|

|

310{2} |

261{2} |

3{2} |

482{3} |

(i) Registrants overseen by the OSC

Although the OSC registers firms and individuals in the category of mutual fund dealer and firms in the category of investment dealer, these firms and individuals are directly overseen by their self-regulatory organizations (SROs), the Mutual Fund Dealers Association of Canada (MFDA) and the Investment Industry Regulatory Organization of Canada (IIROC), respectively. This report focusses primarily on registered firms and individuals directly overseen by the OSC.

In this report, we summarize new and proposed rules and initiatives impacting registrants, current trends in deficiencies from compliance reviews of registrants (including acceptable practices to address them and unacceptable practices to prevent them), and current trends in registration. We provide an update on our Registrant Outreach program that helps strengthen our communication with registrants on compliance practices. We also provide a summary of some key registrant misconduct cases, explain where registrants can get more information about their obligations, and provide CRR contact information.

This report is a key component of our outreach to registrants. We strongly encourage registrants to thoroughly read and use this report to enhance their understanding of:

• initial and ongoing registration and compliance requirements,

• OSC staff expectations of registrants and our interpretation of regulatory requirements, and

• new and proposed rules and other regulatory initiatives.

As a means of promoting pro-active compliance, we recommend registrants use this report as a self-assessment tool to strengthen their compliance with Ontario securities law, and as appropriate, to make changes to enhance their systems of compliance, internal controls and supervision.{4}

1 Key policy initiatives impacting registrants

1.1 Ongoing amendments to registration requirements, exemptions and ongoing registrant obligations

"There is a sea of change occurring in today's financial markets.....This requires regulation that promotes confidence in our capital markets, is responsive to changes in the economic and business environment, and reflects the reality of today's global, competitive capital markets.

March 27, 2014 Speech by Howard Wetston, Chair, OSC to the Toronto Region Board of Tradem

Since the implementation of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103) in September 2009, and the amendments which came into force in July 2011, we have monitored this relatively new regulatory regime for registrants and engaged in discussions with stakeholders about their practical experiences working with the regime. With the Canadian Securities Administrators (CSA), we developed additional technical and substantive amendments to NI 31-103 and NI 33-109 Registration Information (NI 33-109) arising from this ongoing consultation.

On December 5, 2013, the CSA published for comment Proposed Amendments to NI 31-103, NI 33-109, NI 52-107, OSC Rule 33-506 and OSC Rule 35-502 and Related Forms (NI 31-103 Proposed Amendments). The purpose of the NI 31-103 Proposed Amendments are to:

• codify current exemption orders,

• refine certain exemptions,

• provide guidance and clarification that will enhance investor protection and improve the day-to-day operation of the registration regime for industry participants and regulators,

• implement consequential amendments to other national instruments and rules as a result of the NI 31-103 Proposed Amendments (consequential amendments to NI 33-109, NI 52-107, OSC Rule 33-406 and OSC Rule 35-502), and

• further clarify the legislative intent of NI 31-103.

The NI 31-103 Proposed Amendments comment period is closed. The CSA has reviewed comments submitted by various stakeholders and is considering these comments in relation to the future NI 31-103 amendments.

For your ease of reference, the majority of the NI 31-103 Proposed Amendments are summarized in relevant sections throughout this report. For more information, see the published NI 31-103 Proposed Amendments on the OSC website.

1.2 Exempt market review

|

EXEMPT MARKET REVIEW{5} |

||

|

|

||

|

$104 BILLION |

90% |

74% |

|

|

||

|

Ontario capital exemption distributions |

Capital raised through accredited investor exemption |

Capital raised through debt-related securities |

As part of our continued work to enhance and expand the exempt market, we published proposals for both the CSA policy review of the existing minimum amount and accredited investor prospectus exemptions (accredited investor exemption) and the OSC's expanded review of potential new prospectus exemptions. These initiatives, discussed briefly below, will impact investors, issuers, EMDs and other registrants distributing exempt market products.

On February 27, 2014, the CSA published proposed amendments relating to the accredited investor exemption and the minimum amount investment prospectus exemption (MA exemption) in National Instrument 45-106 Prospectus and Registration Exemptions (NI 45-106).

The amendments include:

• a new risk acknowledgement form for individual accredited investors that describes, in plain language, the individual accredited investor categories and the protections an investor will not receive by purchasing under the accredited investor exemption,

• restricting the MA exemption to distributions involving non-individual investors, and

• amending the definition of accredited investor in Ontario to allow fully managed accounts to purchase investment fund securities using the managed account category of the accredited investor exemption, as is permitted in other Canadian jurisdictions.

For more information, see Proposed Amendments to Accredited Investor and Minimum Amount Investment Prospectus Exemptions.

On March 20, 2014, the OSC published a proposal setting out four new prospectus exemptions. The publication of these proposals follows a comprehensive review of the exempt market. As part of that review, we considered the written comments received on earlier proposals. We also conducted extensive consultations with a broad range of stakeholders through a series of one-on-one meetings and town hall meetings, and an online survey designed to gauge the views of retail investors on investing in start-ups and small and medium-sized enterprises.

The OSC also published for comment two new reports of exempt distribution: a report for investment funds and a report for all other issuers. For additional information on these reports and the proposed exemptions, see Introduction of Proposed Prospectus Exemptions and Proposed Report of Exempt Distribution in Ontario.

1.3 Best interest standard

We are re-evaluating the advisor-client relationship by considering whether an explicit statutory fiduciary (or "best interest") standard should apply to dealers and advisers and on what terms. A fiduciary duty is essentially a duty to act in a client's best interest.

In Ontario, section 116 of the Securities Act (Ontario) (Act) applies a best interest standard to IFMs in their dealings with the investment funds they manage. There is no equivalent provision under the Act that explicitly applies a best interest standard to dealers and advisers in their dealings with their clients, although section 2.1 of OSC Rule 31-505 Conditions of Registration requires dealers and advisers to deal fairly, honestly and in good faith with their clients. While there is no statutory best interest duty for dealers and advisers in Ontario, Canadian courts can find that a given dealer or adviser owes a best interest duty to his or her client depending on the nature of their relationship.

CSA Consultation Paper 33-403 The Standard of Conduct for Advisers and Dealers: Exploring the Appropriateness of Introducing a Statutory Best Interest Duty When Advice is Provided to Retail Clients was published on October 25, 2012. We received numerous comment letters on the consultation paper and conducted three roundtables in June and July 2013 (all comment letters and the transcripts from the roundtables are available on the OSC website). On December 17, 2013, we published CSA Staff Notice 33-316 -- Status Report on Consultation under CSA Consultation Paper 33-403: The Standard of Conduct for Advisers and Dealers: Exploring the Appropriateness of Introducing a Statutory Best Interest Duty When Advice is Provided to Retail Clients, which summarized the consultation work conducted to date in respect of the best interest consultation initiative, and identified the key themes that emerged from the best interest consultation process.

We continue to work with our CSA colleagues on this project. The continued work required will depend in part on the outcome of the research we conduct this year. Once this research and analysis has been completed, we will publish the results and our decision on how we plan to move forward with the best interest duty initiative, including timing.

1.4 Cost disclosure, performance reporting and client statements

On July 15, 2013, the Client Relationship Model -- Phase 2 (CRM2) amendments to NI 31-103 came into effect. They are being phased-in over a three-year period. The amendments introduce new requirements for reporting to clients about the costs and performance of their investments, and the content of the investments in their accounts. The requirements apply to dealers and PMs in all categories of registration, with some application to IFMs as well. For more information about these amendments, see CSA Notice of Amendments to NI 31-103 and to Companion Policy 31-103CP (Cost Disclosure, Performance Reporting and Client Statements).

As of July 15, 2013, minor clarifications to NI 31-103 took effect, such as enhancements to relationship disclosure information. Beginning July 15, 2014, dealers and PMs were required to:

• provide pre-trade disclosure of charges, and

• report on compensation from debt securities transactions.

IIROC and MFDA member rules are harmonized with the CSA's CRM2 requirements and will be implemented on the same schedule. SRO members who comply with equivalent member rules will be exempted from the CRM2 requirements in NI 31-103.

To help industry implement the changes, on March 7, 2014 we sent an email blast on CRM2 planning tips directly to the chief compliance officers (CCOs) of all registered dealers and PMs. We have also initiated a CRM2 discussion forum with industry associations and regulators, including IIROC and the MFDA.

Beginning July 15, 2015, expanded account statement requirements will be implemented. These include requirements to provide position cost information and to determine market values using a prescribed methodology for most securities owned by clients, including those held in client name.

For additional information on future requirements, see section 1.1 of OSC Staff Notice 33-742 -- 2013 OSC Annual Summary Report for Dealers, Advisers and Investment Fund Managers (OSC Staff Notice 33-742) and the frequently asked questions and additional guidance in CSA Staff Notice 31-337 Cost Disclosure, Performance Reporting and Client Statements -- Frequently Asked Questions and Additional Guidance as of February 27, 2014.

1.5 Independent dispute resolution services for registrants

On May 1, 2014, NI 31-103 was amended to make the Ombudsman for Banking Services and Investments (OBSI) the common dispute-resolution service for the securities industry in Canada except in Québec.

The transition period for existing registrants expired on August 1, 2014. All dealers and PMs registered in Ontario were required as of August 2, 2014 to be OBSI "Participating Firms" requiring registrants to take reasonable steps to make OBSI's services available to clients who have "eligible complaints" (as defined in section 13.16). There are also new related client disclosure requirements. For more information about these amendments, see CSA Notice of Amendments to NI 31-103 and to 31-103CP (Dispute Resolution Services).

We remind all dealers and PMs of their existing requirements in section 13.15 of NI 31-103 to have internal complaint handling policies in place to ensure that all client complaints are addressed appropriately.

On May 1, 2014, the CSA published CSA Staff Notice 31-338 Guidance on Dispute Resolution Services Client Disclosure for Registered Dealers and Advisers that are not members of a Self-Regulatory Organization. This Notice provides guidance regarding the disclosure firms must provide to their clients about the availability of OBSI's services and internal complaint handling procedures that meet the requirements of the rule. The notice also provides a sample client disclosure document.

The participating CSA jurisdictions have entered into a Memorandum of Understanding (MOU) with OBSI concerning its oversight of this initiative. For additional information please refer to the MOU.

1.6 PM -- IIROC dealer service arrangements

Working together, CSA and IIROC staff are reviewing service arrangements between CSA-regulated PMs and investment dealers that are members of IIROC to assess if rules and/or guidance is needed.

Typically under these arrangements, an IIROC dealer provides trading and custody services to a PM and its clients, but may also provide recordkeeping, client account statements, and margin services. These arrangements are similar to introducing broker-carrying broker arrangements between IIROC dealers that are governed under IIROC Dealer Member Rule 35, but are not subject to any specific rules or guidance.

We identified a number of issues with PM-IIROC dealer service arrangements, including:

• agreement between the PM and the dealer,

• disclosure to the PM's clients, and

• in some cases, the PM relying on the dealer's books and records, and account statement delivery to the PM's clients, to meet its own obligations without being responsible and accountable for the services, and without adequate supervision.

The CSA is working with IIROC to address these issues. The working group is also considering whether PM clients need to continue to receive dual account statements separately from their respective PM and custodian, and if instead the delivery of one account statement (such as a joint account statement from the PM and custodian) is a viable option, keeping in mind investor protection and other regulatory concerns.

Until this work is complete, PMs are to comply with their existing account statement delivery obligations in section 14.14 of NI 31-103, and prepare for the new additional statement requirements in section 14.14.1 of NI 31-103 which come into force on July 15, 2015.

See section 4.3.3 of OSC Staff Notice 33-742 for more information on OSC staff's current expectations and interim guidance on PM client account statement delivery practices.

1.7 Derivatives regulation

In December 2010, the Act was amended to establish a framework for derivatives regulation in Ontario. However, certain amendments relating to derivatives regulation have not yet been proclaimed into force as the necessary supporting rules are not yet in place.

We are consulting with the OSC Derivatives Branch in developing a number of rules relating to the regulation of derivatives, including a rule for determining whether products should be regulated as securities, derivatives, or exempt from regulation (the Product Determination Rule), and a rule that will set out the principal registration requirements and exemptions for derivatives' market participants, including derivatives dealers, derivatives advisers and large derivatives' market participants (the Derivatives Registration Rule).

In April 2013, the CSA Derivatives Committee published for comment CSA Consultation Paper 91-407 -- Derivatives: Registration. We are reviewing the comments received on the consultation paper and developing the proposed Derivatives Registration Rule.

On January 3, 2014, the OSC published a Notice of Ministerial Approval in connection with the Product Determination Rule, OSC Rule 91-506 Derivatives: Product Determination, and OSC Rule 91-507 Trade Repositories and Derivatives Data Reporting (the Trade Repositories Rule). The rules were effective December 31, 2013.

Although the Product Determination Rule only currently applies to the related Trade Repositories Rule, it is anticipated that, once the remaining rules relating to the new derivatives regulatory framework are in place, the Product Determination rule will be extended to apply generally.

As a result of amendments to the Trade Repositories Rule made in April 2014, the trade reporting requirements will take effect on October 31, 2014. We encourage registrants to review their policies and procedures in relation to the reporting of over the counter derivatives transactions. We are working with the OSC Derivatives Branch in developing an oversight program for testing registrant compliance with these new requirements.

2 Outreach to registrants

"We want to provide registrants with tools to build proactive compliance systems."

April 9, 2013 speech by Debra Foubert, Director, Compliance and Registrant Regulation at the Strategy Institute: Annual Registrant Regulation, Conduct & Compliance Summit

We continued to interact with our stakeholders through our outreach program to registrants which was launched in 2013. The objectives of our Registrant Outreach program are to strengthen our communication with Ontario registrants that we directly regulate and other industry participants (such as lawyers and compliance consultants), promote stronger compliance practices and, enhance investor protection.

2.1 Registrant Outreach program

|

REGISTRANT OUTREACH STATISTICS |

|||||

|

|

|||||

|

16 |

2000 |

Key features |

|||

|

|

|||||

|

• |

In-person & webinar seminars provided to June 30, 2014 |

• |

Individuals attended outreach sessions to June 30, 2014 |

• |

dedicated web page |

|

|

|

|

|

• |

educational seminars |

|

|

|

|

|

• |

registrant outreach community |

|

|

|

|

|

• |

registrant resources |

The Registrant Outreach program continues to provide Ontario registrants with practical knowledge on compliance-related matters and gives them the opportunity to hear first-hand from OSC Staff about the latest issues impacting them. Since the launch of the program in July 2013, approximately 2,000 individuals have attended registrant outreach sessions, either in-person or via webinar. The feedback from these participants has been very positive.

The outreach program is interactive and has the following features to enhance the dialogue with registrants:

a) Registrant outreach web page

We set up a Registrant Outreach page on the OSC's website at www.osc.gov.on.ca, which was designed to enhance awareness of topical compliance issues and policy initiatives. Registrants are encouraged to check the web page on a regular basis for updates on regulatory issues impacting them.

b) Educational seminars

Anyone interested in attending an event can go to the Calendar of Events section of the Registrant Outreach page of the OSC website, for seminar descriptions and registration.

c) Registrant outreach community

Registrants are also encouraged to join our Registrant Outreach Community to receive regular e-mail updates on OSC policies and initiatives impacting registrants, as well as the latest publications and guidance on our expectations regarding compliance.

d) Registrant resources

The registrant resources section of the web page provides registrants and other industry participants with easy, centralized access to recent compliance materials. If you have questions related directly to the Registrant Outreach program or have suggestions for seminar topics, please send an email to [email protected].

2.2 Registrant Advisory Committee

The OSC's Registration Advisory Committee (RAC) was established in January 2013. The RAC, which is currently comprised of 11 external members, advises OSC staff on issues and challenges faced by registrants in interpreting and complying with Ontario securities law, including registration and compliance related matters. The RAC also acts as a source of feedback to OSC staff on the development and implementation of policy and rule making initiatives that promote investor protection and fair and efficient capital markets. The RAC meets quarterly and members serve a two year term. The initial two year term will expire in December 2014 and a call for new members will be made in the fall of 2014. You can find a list of current RAC members on the OSC website.

Topics of discussion with the RAC this year have included the proposed mutual fund risk classification methodology for use in the Fund Facts, the proposed exemptions included as part of the exempt market review process (discussed briefly above), current topics related to PMs and IFMs, the electronic delivery of documents to the OSC, the new proposed OSC derivatives rules (discussed briefly above), and proposed changes to the OSC Rule 13-502 Fees (the Fees Rule).

2.3 Communication tools for registrants

We use a number of tools to communicate initiatives that we work on and the findings of those initiatives to our registrants, including OSC Compliance annual reports, Staff Notices (OSC and CSA) and e-mail blasts. The information provided to registrants via e-mail blasts is discussed in various sections of this report. The table below provides a listing of recent e-mail blasts sent to registrants.

|

Date of email blast |

E-mail blast topic and additional information |

|

|

|

|

June 19, 2014 |

OSC Staff Notice 33-743 -- Guidance on sales practices, expense allocation and other relevant areas developed from the results of the targeted review of large investment fund managers (OSC Staff Notice 33-743) |

|

|

See section 4.4 b) of this report. |

|

|

|

|

June 10, 2014 |

Risk Assessment Questionnaire (RAQ) |

|

|

See section 4.1 a) (ii) of this report. |

|

|

|

|

May 1, 2014 |

Requirement to make OBSI available to clients |

|

|

See section 1.5 of this report. |

|

|

|

|

March 12, 2014 |

Requirement to make OBSI available to clients |

|

|

See section 1.5 of this report. |

|

|

|

|

March 7, 2014 |

CRM2 FAQ published; planning tips |

|

|

See section 1.4 of this report. |

|

|

|

|

February 11, 2014 |

Requirement to deliver documents electronically to the Ontario Securities Commission (Effective February 19, 2014) |

|

|

See section 4.1 d) (ii) of this report. |

|

|

|

|

January 9, 2014 |

CSA Staff Notice 31-336 -- Guidance for Portfolio Managers, Exempt Market Dealers and Other Registrants on the Know-Your-Client, Know-Your-Product and Suitability Obligations |

|

|

See section 4.1 c) (i) of this report. |

|

|

|

|

November 20, 2013 |

Guidance for changes in calculating capital markets participation fees by registrant firms, unregistered exempt international firms and unregistered IFMs effective April 1, 2013 |

|

|

See section 4.1 e) of this report. |

|

|

|

|

September 9, 2013 |

Calculation of excess working capital and the use of subordination agreements |

|

|

See section 4.1 c) (iv) 3) of this report. |

For more information, see OSC E-mail blasts.

2.4 Impact of "Heartbleed" vulnerability on registrants

On April 17, 2014, we sent a survey to registrants with head offices in Ontario in response to the "Heartbleed" bug. The "Heartbleed" bug presented a vulnerability to Internet services that allowed an attacker/hacker to read encrypted information which could expose sensitive data such as passwords and bank account information. The purpose of the survey was to gauge the degree to which the "Heartbleed" bug impacted our registrants.

The survey results indicated that 66% of registrants transacted with or for their clients or others through web sites, social media, file transfers or remote connections. This indicates that a large number of survey respondents not only use the Internet, but do so in such a way that sensitive information is likely exchanged over the web either with clients or service providers.

Strong and tailored cyber security measures are an important element of a registrant's controls in promoting reliability of their operations and the protection of confidential information. To manage the risks of a cyber threat, registrants and regulated entities should be aware of the challenges of cybercrime and should take the appropriate protective measures necessary to safeguard themselves and their clients and stakeholders.

For additional information on guidance to strengthen cyber security, refer to CSA Staff Notice 11-326 Cyber Security published on September 26, 2013.

3 Registration of firms and individuals

"Participation as a registrant in Ontario's capital markets is a privilege that comes with significant responsibilities to investors and the public at large"

June 13, 2012 speech by Mary Condon, Vice-Chair, Compliance & Risk Management Strategies Summit for Portfolio Managers and Fund Managers

The registration requirements under securities law help to protect investors from unfair, improper or fraudulent practices by market participants. The information required to support a registration application allows us to assess a firm's and an individual's fitness for registration. When assessing a firm's fitness for registration we consider whether it is able to carry out its obligations under securities law. We use three fundamental criteria to assess an individual's fitness: proficiency, integrity and solvency. These fitness requirements are the cornerstones of the registration regime.

In this section, we discuss current trends in registration, discuss novel business activities potentially requiring registration, provide an update on supervisory terms and conditions (T&Cs), outline a new pre-registration process recently implemented and provide a snapshot of the NI 31-103 Proposed Amendments that will impact registration requirements.

3.1 New rules and initiatives for registrants

a) Pre-registration reviews

We commenced pre-registration reviews by incorporating compliance review procedures as part of the registration process. We are referring to this process as "Registration as the first Compliance Review". The procedures include reviewing a firm's financial condition, business plan and at a high level the policies and procedures manual. Additional procedures may also be conducted with a focus on proposed operations, compliance systems, and proficiency of the firms' individuals. Information is gathered by OSC staff through written inquires, requests for documentation and/or interviews of a firm's key representatives.

The purpose of the pre-registration review is to assess compliance with Ontario securities law at the time of registration. Noted deficiencies are raised with firms and corrective action of all issues is required prior to firm registration. The pre-registration review will enhance firms' awareness of their obligations to establish an adequate compliance system.

- - - - - - - - - - - - - - - - - - - -

Suggested practices to prepare for an OSC pre-registration review:

Firms must:

• Establish an effective compliance system prior to commencing registerable activities.

• Ensure that written policies and procedures adequately address all aspects of business operations.

• Be prepared to answer detailed questions (in writing or in person) regarding the firm's business plan and compliance systems including:

• products and services that will be offered,

• business growth plans,

• details on referral arrangements, if any,

• supervisory structure within the context of the firm's growth objectives,

• marketing plans,

• material business contracts, and

• oversight for outsourced business arrangements.

• Be prepared to provide

• the firm's application or membership in OBSI, if applicable,

• details regarding planned custodial arrangements,

• copies of business plans and policies and procedures manual, and

• copies of other information such as offering documents, referral agreements, KYC documents, and disclosure documents.

Firms are encouraged to:

• Compile records requested on a timely basis.

• Perform an initial self-assessment to determine compliance with Ontario securities law, or engage a compliance consultant to perform the assessment prior to registration, and rectify all deficient areas prior to applying for registration.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Unacceptable practices

Firms are encouraged to avoid the following practices:

• Conduct the following after submission of a registration application:

• draft the written policies and procedures manual, and

• search for possible service providers.

• Provide documents related to the registration process in stages; complete documentation relating to the registration application should be provided at the time of registration including audited financial statements.

- - - - - - - - - - - - - - - - - - - -

b) NI 31-103 Proposed Amendments to registration requirements

The following chart provides a high level overview of the NI 31-103 Proposed Amendments to registration requirements that will impact registrants.

|

Proposed amendment{6} |

Topic |

Purpose |

|

|

||

|

Section 3.3 of NI 31-103 |

Proficiency: review of time-limits used to stale date exams |

Technical amendment to codify blanket/omnibus relief dated February 26, 2010 currently being relied on related to examinations and programs for dealing representatives of EMDs and SPDs. |

|

|

||

|

Section 4.1 of NI 31-103 |

Prohibition in s. 4.1(1)(b) regarding dually registered individuals |

To clarify that the dual registration prohibition applies to a firm registered in any jurisdiction of Canada. |

|

|

||

|

Section 13.4 of the Companion Policy to National Instrument 31-103 (31-103CP) |

Identifying and responding to conflicts of interest |

To add guidance relating to conflicts of interest in relation to registered representatives that serve on the boards of reporting issuers or have outside business activities (OBAs). |

|

|

||

|

NI 33-109 |

Amendments to NI 33-109 forms |

To update and enhance certain NRD forms. |

For additional information see sections 1.1 and 3.3 of this report.

c) Registration service commitment

In May 2014, we issued the OSC service commitment in which our service standards are set out in detail. The following standards, conditions and timelines pertain to registrants and registration-related filings where the OSC is the principal regulator.

|

Service Commitment Summary |

|||

|

|

|||

|

Item |

Service commitment |

||

|

|

|||

|

New business submissions |

• |

A registration officer will: |

|

|

|

|

• |

contact your representative and provide instructions on fee payment and provide notification that the system is ready to accept applications from the "mind and management" of your business within 5 working days upon receipt of your application |

|

|

|

• |

best efforts target: 95% of the filings. |

|

|

• |

Aim to provide a decision to your application within 90 working days where the following conditions are met: |

|

|

|

|

• |

you are a non-SRO applicant, |

|

|

|

• |

all questions are answered with sufficient detail, |

|

|

|

• |

all regulatory obligations are met, |

|

|

|

• |

there are no concerns with your fitness for registration, and |

|

|

|

• |

you respond to our request for information in a timely manner |

|

|

|

• |

best efforts target: 80% or more of these filings. |

|

|

|||

|

Dealing representatives -- new applications and reactivations |

• |

Aim to review, analyze, and provide a decision to your application with 5 working days where the following conditions are met: |

|

|

|

|

• |

your application is complete, |

|

|

|

• |

your application is not associated with a new business application, and |

|

|

|

• |

there are no concerns with your fitness for registration |

|

|

|

• |

best efforts target: 80% or more of these filings. |

|

|

|||

|

Advising representatives (ARs), associate advising representatives (AARs) and CCOs -- new applications and reactivations |

• |

Aim to apply a decision to your application within 20 working days where the following conditions are met: |

|

|

|

|

• |

your application is complete, |

|

|

|

• |

your application is not associated with a new business application, and |

|

|

|

• |

there are no concerns with your fitness for registration |

|

|

|

• |

best efforts target: 80% or more of these filings. |

|

|

|||

|

Notices of termination (where individuals leave former firm in good standing) |

• |

Aim to complete a notice of termination within 5 working days. |

|

|

|

|

• |

best efforts target: 95% or more of these filings |

In relation to the service commitments summarized above, if we do not receive a response within three weeks of making a request relating to a registration filing, we will generally consider the file to be dormant and will take steps to close it. Prior to closing the file, we will send the filer another notification asking for a status update and informing them of the imminent files closure within two weeks unless we receive a response to our notification. In cases where a re-activitation of the file is requested, an additional fee may be required.

3.2 Trends in registration

a) Registration of not for profit issuers

We became aware of a number of not for profit issuers that are distributing their own securities. NI 45-106 provides an exemption from the prospectus requirement in section 2.38 for certain not for profit issuers distributing their own securities provided they comply with certain conditions. However, as of March 27, 2010, the registration exemption previously available under section 3.38 of NI 45-106 is no longer available. A not for profit issuer is required to consider whether it is engaged in the business of trading in securities (please refer to the 31-103CP section 1.3 Factors in determining business purpose). If an issuer is in the business of trading its securities, then registration as a dealer is required.

b) Tax shelter products

We remind registrants that tax shelter products, including ones that involve leveraged donations of property (for instance, artwork and medical supplies) to charities and ones that are marketed to investors on the basis of tax credits or deductions that are claimed to be available, are typically considered "securities" and require registration. See section 4.2 b) of this report for further information.

c) Desk review of supervisory T&Cs

We conducted a desk review of non-SRO registrant firms whose sponsored individuals have been or are currently subject to supervisory T&Cs. The types of T&Cs reviewed included strict supervision, close supervision, OBAs, and requirement to deliver disclosure documents to clients. The objective of the review was to ensure adequate supervision by the firm over these T&Cs. We also compared the T&Cs to the original activities that led to their imposition and concluded that the T&Cs were fitting for the types of activities reported. The review concluded that most firms were adhering to the T&Cs imposed on their individual registrants and were conducting adequate supervision. One firm was identified as not fulfilling their supervisory obligations. We are following up with this firm.

d) Registration of online portals

We have seen a number of firms applying to register as EMDs that plan to operate accredited investor only internet portals. EMDs can operate portals to facilitate distributions of securities in reliance on prospectus exemptions (e.g. the accredited investor exemption) provided they comply with all normal requirements applicable to the EMD category, including KYC and suitability.

In contrast, Multilateral Instrument 45-108 Crowdfunding, the proposed crowdfunding rule, contemplates that funding portals will register in the restricted dealer category. The crowdfunding prospectus exemption is aimed at allowing retail investors to participate in the capital raising of businesses in Canada. The crowdfunding portal is subject to important conditions (e.g. it can only distribute securities in reliance on the new crowdfunding prospectus exemption, which includes investment limits of $2,500 per investment/$10,000 per annum) and will not be able to distribute securities in reliance on other exemptions, e.g. the accredited investor exemption.

e) Registration of online advisory businesses

We have seen increasing interest in advisers providing advice through online platforms. We have recently registered a small number of PM firms that will operate online and expect to see others enter the market. The online advice model that we have considered to be acceptable involves an interactive website used to collect KYC information, which will be reviewed by a registered AR. The AR will communicate with the client by telephone, video link, email or internet chats. The AR must ensure that sufficient KYC information has been gathered to support the PM firm's obligation to make suitability determinations for the client.

Each of the firms that we have registered to provide online advice operates on a discretionary managed account basis, using portfolios of unleveraged exchange traded funds (ETFs) or low cost mutual funds. In most cases, these are model portfolios which are selected for a client based on a profile generated by the KYC collection process. An AR will review and approve the suitability of the portfolio for the client. The client's account is periodically rebalanced to the parameters set for their portfolio.

This is not the so-called "robo-advice" model seen in the United States, where online advice has seen rapid growth in the last few years. The online advisers operating in Ontario are offering hybrid services that utilize an online platform for the efficiencies it offers, while ARs remain actively involved in decision making.

We do not think that an entirely automated decision making process would be acceptable at this stage. The KYC and suitability obligations of PMs that provide their services through online platforms remain the same as for any other PM. A PMs obligations under securities law does not change as a result of the delivery method of providing the services to a client. We expect firms that are interested in implementing an online advice operating model in Ontario to submit their proposed online KYC questionnaire and related processes for a due diligence review by CRR staff. This review in no way diminishes the firm's ongoing responsibilities under applicable securities law.

f) Fees for late document filings

We continue to see late regulatory filings related to registration documents including, but not limited to:

• financial and civil disclosures,

• other business activities,

• ownership of securities and derivatives firms, and

• acquisition notices under sections 11.9 and 11.10 of NI 31-103 (see section 4.1 b) in this report for additional information).

Most registration updates must be filed within 10 days of a change to a registered firm's information in Form 33-109F6 -- Firm Registration Form or Form 33-109F4 -- Individual Registration Form.

When required documents are filed late, late fees will apply and be charged. The applicable fee is $100 per business day, subject to a maximum aggregate fee of $5,000 for all documents required to be filed within a calendar year. Please see the full list found in Appendix D -- Additional Fees for Late Document Filings in the Fees Rule.

We remind firms that they are expected to have an effective compliance system in place to minimize late filings.

g) Registration related conflicts of interest

The CSA provided clarification and guidance regarding OBAs in the NI 31-103 Proposed Amendments dated December 5, 2013. Disclosure is and will continue to be required for all officer or director positions and any other equivalent positions held as well as positions of influence per Item 10 -- Current employment, other business activities, officer positions held and directorships in Form 33-109F4 (the F4). Guidance has also been added in the 31-103CP which clarifies that disclosure is required for certain paid or unpaid roles with charitable, social or religious organizations and for owners of a holding company.

We continue to place restricted client T&Cs on individuals with a position of influence (particularly over potentially vulnerable clients). These T&Cs restrict the individual from trading or advising clients met through the OBA (and close family members of those clients). For example, this year restricted client T&Cs were placed on:

• teachers (elementary, secondary and college),

• registered nurses (hospital and nursing home),

• early childhood educators (daycare and school),

• a volunteer minister, and

• support workers (work with clients with mental health issues, abused women or the elderly).

- - - - - - - - - - - - - - - - - - - -

Suggested practices to adequately address OBA

Registrants Must:

• Assess OBAs to identify conflicts of interest, determine the level of risk, and respond appropriately (for example, approve each new OBA before it begins).

• Promote compliance with OBA requirements through an annual attestation and questionnaire, ongoing monitoring, and education.

• When onboarding a new registered or permitted individual:

• review and discuss all pre-existing OBAs,

• review and vet responses to all conflict of interest questions in Schedule G (Item 10 of the F4),

• ensure OBA disclosure on NRD is complete and correct, and

• remind the individuals that any change to this disclosure must be reported to the firm and filed on NRD within 10 days of the change.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Unacceptable practices

Registrants must not:

• Permit an OBA if it cannot properly control the potential conflict of interest.

• State in the F4 disclosure- Item 10 that there is no actual or potential conflicts of interest and client confusion when that is not true (e.g., individual holds an elected office or provides free investment management services to a social organization).

• Sponsor an individual with an OBA until the firm is ready to discuss what additional supervisory/oversight policies and procedures they are willing to perform to ensure compliance with the restricted client T&Cs.

- - - - - - - - - - - - - - - - - - - -

3.3 Proposed amendments to NI 31-103{7}

a) Proficiency of registrants

Experience for CCOs of Dealers

In the course of compliance reviews, we identified a number of dealer firms that have CCOs who are not adequately performing their responsibilities. This deficiency is often associated with a finding that the CCO does not have relevant experience. As a result, we proposed amendments to add a requirement that CCOs of mutual fund dealers, SPDs and EMDs have 12 months of relevant securities industry experience in the 36-month period prior to applying for registration. These new requirements will apply to new firm applications only.

Proficiency Principle - CCOs of dealers, advisers and IFMs

The experience requirement being proposed for dealer CCOs is consistent with the proficiency principle in section 3.4 of NI 31-103 which states that a CCO must not perform an activity that requires registration unless the individual has the education, training and experience that a reasonable person would consider necessary to perform the activity competently. We have further elaborated on this principle in 31-103CP to clarify that this must include a good understanding of the regulatory requirements applicable to the firm (and individuals acting on its behalf) as well as the knowledge and ability to design and implement an effective compliance system.

Experience for ARs and AARs

We provided further guidance in 31-103CP clarifying what we may consider relevant investment management experience for AR and AARs. This guidance incorporates content from CSA Staff Notice 31-332 Relevant Investment Management Experience for Advising Representatives and Associate Advising Representatives of Portfolio Managers (CSA Staff Notice 31-332) published on January 17, 2013. Firms should continue to refer to the CSA Staff Notice 31-332 for specific examples. We expect firms and individuals to consider CSA Staff Notice 31-332 and 31-103CP as guidance at appropriate times, such as during the job application, hiring process and submission of applications for registration.

3.4 Trends in applications for PM registration

We are receiving a number of registration applications for small and one person PM firms (which may also include the categories of IFM and EMD) where none of the applicants have been previously registered as an AR, employed at a registered PM firm or been employed in a compliance capacity.

In order for these individuals (and firms) to be registered, they must provide evidence that they have the required courses and relevant investment management experience to qualify as an AR or CCO, as is the case for all new CCO and AR applicants. The individuals must also demonstrate how they meet the requirements of the proficiency principle in section 3.4 of NI 31-103 to competently perform the activities requiring registration.

- - - - - - - - - - - - - - - - - - - -

Suggested practices to adequately prepare individual registration applications

Applicants must:

• Send evidence of course completion.

• Provide information on experience that is clear, accurate and relevant. For example, the information should:

• provide details of relevant past duties and responsibilities, including the dates and employers where the experience was obtained,

• provide an estimate of the percentage of time spent on the more relevant activities,

• focus on the experience of the individual; where it is helpful or necessary to include information about the individual's team or firm to put the information in context, ensure that the duties and responsibilities of the particular individual are clear, and

• ensure that past experience is distinguished from proposed activities that the individual will conduct upon registration.

• Be prepared to provide evidence of the experience being described upon request (for example, a letter from a former supervisor confirming and describing the experience).

• Be prepared to answer questions about their understanding of the regulatory requirements for the category of registration applied for.

• For CCO applicants, provide information on how their past experience has provided them with the knowledge and ability to design and implement an effective compliance system.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Unacceptable practices

Applicants must not:

• Provide information that has not been reviewed for accuracy. By filing the application, the individual is certifying that the information is true and complete. It is also the firm's obligation under Part 5 of NI 33-109 to make reasonable efforts to ensure the truth and completeness of the information submitted.

• Expect that the discretionary management of the individual's own investment portfolio will qualify as relevant investment management experience or be sufficient to demonstrate the experience or competencies required for registration as a CCO.

• Rely solely on third parties such as legal counsel and compliance consultants to meet proficiency and other regulatory requirements. While we encourage registrants to make use of external supports, such as legal counsel and compliance consultants, the obligations set out in Part 5.2 of NI 31-103 are those of the registrant.

- - - - - - - - - - - - - - - - - - - -

4 Information for dealers, advisers and investment fund managers

"Our job as a regulator is to create the framework and set the rules of the game to make Ontario's capital markets fairer and more efficient, and provide an appropriate level of investor protection."

May 2, 2013 speech by Howard Wetston, Chair, OSC to the 2013 EMDA Exempt Market

The information in this section includes the key findings and outcomes from our ongoing compliance reviews of the registrants we directly regulate. We highlight current trends in deficiencies from our reviews and provide suggested practices to address the deficiencies. We also discuss new or proposed rules and initiatives impacting registrants.

This part of the report is divided into four main sections. The first section contains general information that is relevant for all registrants. The other sections contain information specific to dealers (EMDs and SPDs), advisers (PMs) and IFMs, respectively. This report is organized to allow a registrant to focus on reading the section for all registrants and the sections that apply to their registration categories. However, we recommend that registrants review all sections in this part, as some of the information presented for one type of registrant may be relevant to other registrants.

4.1 All registrants

This section discusses our compliance review process, current trends in deficiencies and suggested practices to address them, and new and proposed rules and initiatives impacting all registrants.

a) Compliance review process

We conduct compliance reviews of registered firms on a continuous basis. The purpose of compliance reviews is primarily to assess compliance with Ontario securities law; but they also help registrants to improve their understanding of regulatory requirements and our expectations, and help us to learn about a specific industry topic or practice we may have concerns with. We frequently conduct compliance reviews on-site at a registrant's premises, but also perform desk reviews from our offices. For information on "What to expect from, and how to prepare for an OSC compliance review" see the slides from the Registrant Outreach session provided on October 22, 2013 on "Start to finish: Getting through an OSC compliance review".

(i) Risk-based approach

Firms are generally selected for review using a risk-based approach. This approach is intended to identify firms that are most likely to have material compliance issues (including risk of harm to investors) or significant impact to the capital markets if there are compliance breaches. To determine which firms should be reviewed, we consider a number of factors, including firms' responses to the most recent RAQ, their compliance history, complaints or tips from external parties, and referrals from another OSC branch, an SRO or another regulator.

(ii) Risk Assessment Questionnaire

"This process is essential for gathering data from the firms we regulate, which in turn, informs our approach to compliance...We use this data to make evidence-based decisions about which firms require further attention and oversight."

June 10, 2014 press release re Ontario Securities Commission Issues 2014 Risk Assessment Questionnaire

We issue a comprehensive RAQ periodically to collect information about our registrants' business operations. The 2014 RAQ was sent on June 10, 2014 to firms that were registered with the OSC in the categories of PM, restricted PM, IFM, EMD, and/or restricted dealer. Firms had approximately 40 days to complete and submit the RAQ online.

The RAQ supports our risk based approach to select firms for on-site compliance reviews or targeted reviews. Based on the responses to this year's RAQ, we will select higher risk firms for on-site compliance reviews.

(iii) Sweep reviews

In addition to reviewing firms based on risk selection, we also conduct sweeps which are compliance reviews on a specific topic on firms in an industry sector. Sweeps allow us to respond on a timely basis to industry-wide concerns or issues. We regularly perform sweeps of newly registered firms to assess if they are off to a good start and to help them to understand their requirements and our expectations. We also regularly review large or "impact" firms as discussed in (i) above.

Some of the sweep reviews we performed this year are highlighted below:

• We completed the reviews of a sample of "impact" PMs, IFMs and EMDs. The results of this sweep produced staff guidance in relation to IFMs only. See section 4.4 b) on Sweep of large "impact" IFMs for a summary of this sweep's findings and the guidance issued.

• We started on-site reviews of a sample of newly registered IFMs. We included IFMs in the sample that were registered during a specified time period and that had not previously been reviewed. See section 4.4 c) on Sweep of newly registered IFMs for additional information.

• We performed a desk review of the 2013 capital markets participation fees provided to the OSC for 123 registrants. See section 4.1 e) on Ongoing review of capital markets participation fees for additional information.

• We performed a desk review of supervisory T&Cs. See section 3.2 c) on Desk review of supervisory T&Cs for this sweep's findings.

(iv) Outcomes of compliance reviews

In most cases, the deficiencies found in a compliance review are set out in a written report to the firm so that they can take appropriate corrective action. After a firm addresses its deficiencies, the expected outcome is that they have enhanced their compliance. If a firm had many significant deficiencies, once it addresses these, the expected outcome is that they have significantly enhanced their compliance.

In addition to issuing compliance deficiency reports, we take additional regulatory action when warranted (including when we identify potential registrant misconduct or fraud).

The outcomes of our compliance reviews in fiscal 2014, with comparables for 2013, are presented in the following table and are listed in their increasing order of seriousness. Firms are shown under the most serious outcome obtained for a particular review. The percentages in the table are based on the registered firms we reviewed during the year and not the population of all registered firms.

|

Outcomes of compliance reviews (all registration categories) |

Fiscal 2014 |

Fiscal 2013 |

|

|

||

|

Enhanced compliance |

53% |

38% |

|

|

||

|

Significantly enhanced compliance |

28% |

52% |

|

|

||

|

Terms and conditions on registration |

10% |

3% |

|

|

||

|

Surrender of registration |

3% |

1% |

|

|

||

|

Referral to the Enforcement Branch |

5% |

2% |

|

|

||

|

Suspension of registration{8} |

9% |

4% |

For an explanation of each outcome, see Appendix A in OSC Staff Notice 33-738 -- 2012 OSC Annual Summary Report for Dealers, Advisers and Investment Fund Managers (OSC Staff Notice 33-738).

(v) Contacting investors as part of compliance reviews

We continue to contact investors as part of our ongoing, normal course reviews of dealers and advisers. For additional information, see the section titled "Contacting investors as part of compliance reviews" in OSC Staff Notice 33-742.

b) Failure to provide notice of ownership changes or asset acquisitions

We continue to have significant concerns with some registrants not providing us with the required notice under sections 11.9 or 11.10 of NI 31-103 of proposed ownership changes in, or asset acquisitions of, registered firms. For example, we continue to find a number of cases where:

• Registrants (including the Ultimate Designated Person (UDP), CCO, AR, or dealing representative of the firm) acquired 10% or more of the securities of another registered firm, or their sponsoring firm, without first providing us with the required notice.

• Registered firms have not provided us with the required notice as soon as the registered firm knew, or had reason to believe, that 10% or more of its voting securities were going to be acquired by a non-registrant, including an officer, director, permitted individual or employee of the firm (barring exceptional circumstances, we expect to receive notice of these transactions at least 30 days prior to the transaction taking place).

• Registrants acquired all or a substantial part of the assets of another registered firm without first providing us with the required notice. Examples of scenarios where we would expect to receive (and have, in fact, received) a section 11.9 or 11.10 notice in this context include:

• the acquisition (whether structured as a "purchase" for compensation or not) of another registered firm's book of business, including where the other registered firm is a one-person firm

• the acquisition of a business line or division of another, large registered firm, and

• the acquisition of all of the investment fund management contracts of another registered firm that is an IFM.

We also found that some IIROC or MFDA member firms did not file the required notices under sections 11.9 or 11.10 based on the view that their SRO notice process was sufficient. This is not the case. The notice obligations apply to all registrants, including member firms of IIROC and the MFDA, and arise from the OSC's responsibility to register, among others, dealer firms.

In the cases where registrants did not provide us with the required notice for their completed acquisitions, we required them to file the notice materials for review and pay the applicable filing fees. Although in all of these cases to date we issued a letter to each firm warning them of the seriousness of their failure to provide notice, we may in appropriate circumstances also take other regulatory action. As we mentioned in last year's report, registrants that do not give us the required notice (or provide the notice after the specified deadline) will most likely also be charged late fees for the late notice, as well as applicable late fees for each related securities regulatory filing that is also filed late. For a further discussion regarding late fees generally, see section 3.2(f) of this report.

In addition to filing notices under sections 11.9 or 11.10 of NI 31-103, a change in share ownership of a registered firm, or an acquisition of its assets, typically triggers additional securities regulatory filings. In addition to any SRO filings (discussed above), these additional filings could include:

• filings under NI 33-109 (including, in particular, filings of Form 33-109F5 Change of Registration Information), and

• change of manager approval requests under section 5.5 of National Instrument 81-102 Mutual Funds.

Registrants must take care to ensure that all applicable securities regulatory filings are filed in accordance with their specified timelines in the event of a change in share ownership of a registered firm, or an acquisition of its assets.

Finally, NI 31-103 Proposed Amendments include proposed amendments that will streamline and clarify the filing requirements for notices under sections 11.9 and 11.10 of NI 31-103. For further information about these amendments, see sections 1.1 and 4.1 d) (i) of this report.

c) Current trends in deficiencies and acceptable practices

In this section, we summarize key trends in deficiencies from recent compliance reviews of EMDs, PMs, and IFMs. For each deficiency, we summarize the applicable requirements under Ontario securities law which must be followed. In addition, where applicable, we provide acceptable and unacceptable practices relating to the deficiency discussed. The acceptable and unacceptable practices throughout this report are intended to give guidance to help registrants address the deficiencies, and provide our expectations of registrants. While the best practices set out in this report are intended to present acceptable methods registrants can use to prevent or rectify a deficiency, they are not the only acceptable methods. Registrants may use alternative methods, provided those methods adequately demonstrate that registrants have met their responsibility under the spirit and letter of securities law.

We strongly recommend registrants review the deficiencies and suggested practices in this report that apply to their registration categories and operations to assess and, as needed, implement enhancements to their compliance systems and internal controls.

(i) Non-compliance with KYC, KYP and suitability requirements and accredited investor requirements

We continue to have concerns that some dealers and advisers are not adequately meeting their KYC, KYP and suitability obligations. We also remain concerned that some EMDs are selling securities to investors that do not qualify under a prospectus exemption (such as the accredited investor exemption).

On January 9, 2014, we published CSA Staff Notice 31-336 -- Guidance for Portfolio Managers, Exempt Market Dealers and Other Registrants on the Know-Your-Client, Know-Your-Product and Suitability Obligations (CSA Staff Notice 31-336).

The notice provides additional guidance to registrants in the areas of KYC, KYP and suitability obligations and sets out our expectations of registrants on how to comply with these important regulatory requirements. In particular, we expect registrants to take extra care in complying with their KYC, KYP and suitability obligations when dealing with clients who are seniors or those who may be in a position of vulnerability. Some of the suggested practices and unacceptable practices are highlighted below:

- - - - - - - - - - - - - - - - - - - -

Suggested practices to adequately address KYC, KYP, suitability and accredited investor requirements

Registrants must:

• Engage in a meaningful discussion with clients to obtain a solid understanding of the client's personal and financial circumstances.

• Update KYC information at least annually or more often if there is a significant change to the client's life circumstances or a significant change in market conditions.

• Conduct product due diligence and be able to explain clearly to clients a security's risks, key features, any conflicts of interest and initial and ongoing costs and fees.

• Maintain adequate documentation to support the suitability analysis of each trade and be able to explain to clients how the proposed investment strategy is suitable for the client and how it aligns with their investment needs and objectives.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Unacceptable practices

Registrants must not:

• Delegate KYC and the suitability obligation to an unregistered individual.

• Solely ask the clients to "tick a box" that best describes their investment objectives or risk tolerance without engaging in a discussion with the clients about their personal and financial circumstances.

• Fail to fully understand the structure and features of products before recommending them to clients.

- - - - - - - - - - - - - - - - - - - -

We strongly encourage our registrants to use CSA Staff Notice 31-336 as a self-assessment tool to strengthen their compliance and to improve their systems of internal control and supervision.

(ii) Written policies and procedures are not tailored to a registrant's operations

During our reviews of newly registered IFM firms (see section 4.4 c)) for additional information), we noted instances where some firms did not have a written policies and procedures manual that was tailored to their operations and did not adequately cover the processes and procedures that a firm should have in place to establish an adequate compliance system.

To meet the requirements of section 11.1 of NI 31-103, we expect firms to establish, maintain and apply policies and procedures that are tailored to their respective business operations in order to establish a system of controls and supervision to ensure compliance with securities law and to manage the risks associated with their business in accordance with prudent business practices.

Part 11 of 31-103CP provides guidance on the content and maintenance of written policies and procedures. We also expect firms to have a process in place to ensure that written policies and procedures are regularly updated for changes in the firm's business operations, industry practice and securities law.

- - - - - - - - - - - - - - - - - - - -

Suggested practices to adequately tailor written policies and procedures to a registrant's operations

Registrants must:

• Develop and enforce policies and procedures that are applicable to their firm's business operations.

• Develop policies and procedures that are sufficiently detailed and cover areas relevant to a firm's business operations.

• Provide adequate training to all employees to ensure that employees understand the established policies and procedures and understand how to incorporate them in their daily business activities.

• Review the written policies and procedures on a frequent basis to confirm that the policies and procedures are current and adequately reflect the firm's business operations, industry practice and securities law.

• Remove sections from a policies and procedures manual that are not applicable to the firm's operations.

• Add sections to a policies and procedures manual that are specific to the firm's operations.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Unacceptable practices

Registrants must not:

• Use a template of written policies and procedures provided by another firm or a consultant without reviewing and tailoring the template to the firm's operations and security law obligations.

- - - - - - - - - - - - - - - - - - - -

Section 11.1 of NI 31-103 requires you to establish, maintain and apply policies and procedures that establish a system of controls and supervision to ensure compliance with securities law and manage the risks associated with your business in accordance with prudent business practices. You must also have processes in place to ensure that your written policies and procedures are regularly updated, such as for changes in your business practice, industry practice or securities law.

Please refer to Part 11 of 31-103CP, under the heading "Detailed policies and procedures", for guidance on the content, accessibility and maintenance of written policies and procedures.

(iii) Inadequate insurance coverage

Some IFMs that were part of the newly registered IFM reviews (discussed in section 4.4 b) of this report) did not maintain an adequate financial institution bond (FIB). In these cases, the FIB provided insurance coverage for the benefit plan of the firm's employees under the same insurance rider maintained by the firm to meet its obligations under section 12.6 of NI 31-103. Although this coverage is not offside securities law, the FIB did not include specific provisions to ensure that the claims made by and paid in relation to the employee benefit plan would not affect the limits or coverage applicable to the firm under the FIB.

We also noted that the firms that had this type of insurance coverage in place were not aware of the affect that the coverage could have on the limits available to the firm under the FIB.

Section 12.6 of NI 31-103 prohibits a firm from maintaining bonding or insurance that benefits, or names as an insured, another person or company unless certain conditions are met. One of these conditions is that the individual or aggregate limits under the FIB may only be affected by claims made by or on behalf of the firm or the firm's subsidiary whose financial results are consolidated with the firm's. Additional guidance related to this issue is also found in section 12.6 of 31-103CP.

There is a risk of harm to investors when a firm is not adequately meeting its insurance requirements. The requirement to maintain insurance exists to protect investors in the case of adverse circumstances.

- - - - - - - - - - - - - - - - - - - -

Suggested practices to maintain adequate insurance coverage

Registrants must:

• Carefully read all sections of the insurance policy and understand the firm's insurance coverage.

• Fully understand the implications of insuring additional entities under the FIB on the limits available to the firm.

• Verify by reviewing the insurance policy that the limits available to the firm will not be affected by also insuring other entities and confirm this with the insurance provider.

• Confirm that the insurance coverage in place meets securities law requirements at all times.

• Have written policies and procedures in place to make sure that the insurance policy is regularly reviewed and approved for all of the above and for compliance with securities law.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Unacceptable practices

Registrants must not:

• Solely rely on their insurance provider to use a template insurance policy and FIB to meet the insurance requirements under Division 2 of NI 31-103.

• Sign off on an insurance policy without carefully reading the policy and understanding all of the implications to the firm's coverage by providing coverage to other entities.

- - - - - - - - - - - - - - - - - - - -

(iv) Repeat common deficiencies

The following includes the deficiencies that we continue to find in reviews of our registrants that have been reported on in previous annual reports and prior guidance. We encourage you to review the information sources provided as the previously published guidance is still applicable to these issues.

|

Repeat common deficiency |

Information source |

|

|

|

||

|

1) Inadequate compliance system and UDP and CCO not meeting their responsibilities |

• |

Section 4.1.2 in OSC Staff Notice 33-742 under the heading Inadequate compliance systems and UDPs and CCOs not meeting their requirements |

|

|

• |

Section 11.1 of 31-103CP |

|

|

• |

May 2012 OSC e-mail blast to CCOs and UDPs on Inadequate Compliance Systems |

|

|

||

|

2) Inadequate or no annual compliance report |

• |

Section 4.1.2 in OSC Staff Notice 33-742 under the heading Inadequate or no annual compliance report |

|

|

• |