Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

OSC Staff Notice: 81-723 - Summary Report for Investment Fund Issuers 2013

OSC Staff Notice: 81-723 - Summary Report for Investment Fund Issuers 2013

OSC Staff Notice 81-723

Summary Report for Investment Fund Issuers 2013

Introduction

This, our fourth annual Summary Report for Investment Fund Issuers, provides an overview of the key activities and initiatives of the Ontario Securities Commission for 2013 that impact investment fund issuers and the fund industry, including:

• key policy initiatives,

• emerging issues and trends,

• continuous disclosure and compliance reviews, and

• recent developments in staff practices.

The following pages provide information about the status of some of the initiatives the OSC is undertaking to promote clear and concise disclosure in order to assist investors to make more informed investment decisions. The report also provides information about our work to address the sufficiency of regulatory coverage across all investment fund products. It highlights recent product and market developments, as well as our regulatory response to these developments, in order to assist the investment fund industry in understanding and complying with current regulatory requirements.

The OSC is responsible for overseeing over 3,500 publicly-offered investment funds. Ontario based publicly-offered investment funds hold approximately 80% of the just over $1 trillion in publicly-offered investment fund assets in Canada.

We administer the regulatory framework for investment funds, including:

• reviewing and assessing product disclosure for all types of investment funds, including prospectuses and continuous disclosure filings,

• considering applications for discretionary relief from securities legislation and rules, and

• taking a leadership role in developing new rules and policies to adapt to the changing environment in the investment fund industry.

We also monitor and participate in investment fund regulatory developments globally, primarily through our work with the International Organization of Securities Commissions (IOSCO). OSC staff participation on the IOSCO C5 Investment Management and IOSCO C8 Retail Investors committees informs our operational and policy work. We discuss our participation with IOSCO further on our website at www.osc.gov.on.ca. In this report, we highlight some of the recent work by IOSCO C5 and IOSCO C8 that we think will be of interest to investment fund issuers.

The investment fund products we oversee include both conventional mutual funds and non-conventional investment funds. Non-conventional funds include non-redeemable investment funds such as closed-end funds, mutual funds listed and posted for trading on a stock exchange (ETFs), commodity pools, scholarship plans, labour-sponsored or venture capital funds and flow-through limited partnerships. We discuss the different types of funds further on our website at https://www.osc.ca/en/industry/investment-funds-and-structured-products/operating-investment-fund-ontario.

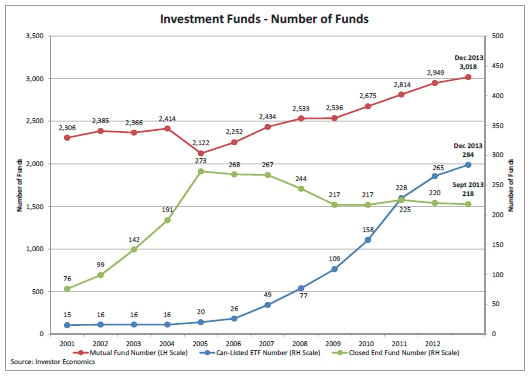

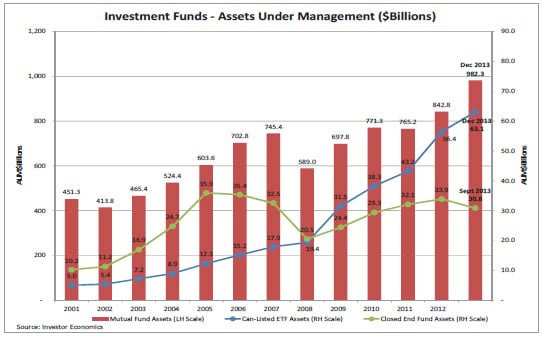

The ETF market continued to grow steadily during the course of the year. As at December 2013, there were 284 ETFs with assets of approximately $63.1 billion. In comparison, as at December 2012, there were 265 ETFs with assets of approximately $56.4 billion, representing an increase in assets of almost 12%. Over the same period, conventional fund assets increased by approximately 17%. As at September 2013, closed-end fund assets had declined by approximately $3 billion from the previous December to approximately $30.8 billion.

Investment Funds - Number of Funds

As these and other investment products increase in number, and as the use of ETFs by retail investors continues to grow, the OSC will continue to assess and respond to product developments and innovations with a view to promoting investor protection and assessing the sufficiency and consistency of the regulatory treatment of different investment fund products.

Investment Funds - Assets Under Management ($Billions)

1. Key Policy Initiatives

The OSC continues to play a leading role in several significant policy initiatives with other securities regulators in Canada through the Canadian Securities Administrators (the CSA). This section reports on the status of significant policy initiatives including:

• transition to IFRS

• mutual fund fees

• point of sale and risk classification methodology for Fund Facts

• modernization of investment fund product regulation

• exempt market

• electronic delivery of documents

• scholarship plans

1.1 Transition to IFRS

The CSA completed the final step in the transition to International Financial Reporting Standards (IFRS) for investment funds with the publication of final amendments to National Instrument 81-106 Investment Fund Continuous Disclosure (NI 81-106), its Companion Policy and related amendments on October 3, 2013. Initially proposed in 2009, the IFRS-related amendments to NI 81-106 were deferred when the International Accounting Standards Board (IASB) agreed to make revisions to resolve a potentially significant accounting issue for investment funds. The final amendments reflect comments received on the 2009 proposal, additional stakeholder consultations and further IASB developments related to investment funds. The changes impact investment fund requirements relating to the presentation of financial statements and terminology to reflect the transition to IFRS.

In Ontario, the amendments to NI 81-106 and related amendments received ministerial approval on November 21, 2013. Investment funds must apply the changes for financial years beginning on or after January 1, 2014.

1.2 Mutual Fund Fees

On December 13, 2012 the CSA published for comment CSA Discussion Paper and Request for Comment 81-407 Mutual Fund Fees (the Discussion Paper). The Discussion Paper examined a number of investor protection issues that we think arise from the current mutual fund fee structure in Canada, including the potential conflicts of interests that embedded advisor compensation, or trailing commissions, may give rise to. It solicited comments on several potential regulatory options to address the issues identified including, among others, introducing a statutory best interest duty for advisors and capping or banning trailing commissions.

We received 99 comment letters on the Discussion Paper from various industry stakeholders as well as various investor advocates and individual investors.

The OSC and CSA also held various in-person consultations{1} throughout the Summer and Fall of 2013, to probe deeper into some of the themes emerging from the comment letters received in response to the Discussion Paper.

On December 12, 2013 the CSA published CSA Staff Notice 81-323 Status Report on Consultation under CSA Discussion Paper and Request for Comment 81-407 Mutual Fund Fees, which provides a summary of the key comments received on the Discussion Paper through the comment process and the subsequent in-person consultations.

1.3 Point of Sale and Risk Classification Methodology for Fund Facts

The Point of Sale (POS) Project is a continuation of the CSA's participation in the project by the Joint Forum of Financial Market Regulators to develop a more effective disclosure regime for conventional mutual funds and segregated funds. The Fund Facts is central to the POS project and is designed to make it easier for investors to find and use key information.

On June 18, 2010, the CSA announced its approach to proceed with a staged implementation of the POS Project in CSA Staff Notice 81-319 Status Report on the Implementation of Point of Sale Disclosure for Mutual Funds.

Stage 1, which came into force January 1, 2011, required that mutual funds produce and file the Fund Facts, and for the Fund Facts to be available on the mutual fund's or mutual fund manager's website. The Fund Facts must also be delivered or sent to investors free of charge on request.

Stage 2, allowing the delivery of the Fund Facts to satisfy the current prospectus delivery requirements to deliver a prospectus within two days of buying a mutual fund, was completed with the publication of final amendments on June 13, 2013. The amendments are phased-in, with the amendments to Form 81-101F3 Contents of Fund Facts Document, including enhancements to the presentation of the risk and performance sections of the Fund Facts, effective as of January 13, 2014. The amendments that require delivery of the Fund Facts and allow for the Fund Facts to satisfy the current prospectus delivery requirement under securities legislation to deliver a prospectus within two days of buying a mutual fund take effect on June 13, 2014.

On September 5, 2013, we published OSC Staff Notice 81-721 -- Frequently Asked Questions on the Implementation of Stage 2 of Point of Sale Disclosure for Mutual Funds -- Delivery of Fund Facts (FAQs). The FAQs were published to respond to implementation questions related to the Stage 2 final amendments.

In Stage 3, the CSA is proceeding with three concurrent work streams: (i) the development of a CSA mutual fund risk classification methodology, (ii) proposed amendments aimed at implementing pre-sale delivery of the Fund Facts, and (iii) the development of a summary disclosure document for exchange-traded mutual funds (ETFs), similar to the Fund Facts, and a requirement to deliver the summary disclosure document within two days of an investor buying an ETF.

On December 12, 2013, the CSA published CSA Notice 81-324 and Request for Comments Proposed CSA Mutual Fund Risk Classification Methodology for Use in Fund Facts (the Proposed Methodology), which sets out a proposed risk classification methodology for use by mutual fund managers in the Fund Facts. The CSA developed the Proposed Methodology in response to stakeholder feedback that the CSA has received throughout the POS Project, notably that a standardized risk classification methodology proposed by the CSA would be more useful to investors as it would provide a consistent and comparable basis for measuring the risk of different mutual funds.

Prior to the publication of the Proposed Methodology, the CSA held consultations with industry representatives, academics and investor advocates to seek their feedback. The comment period for the Proposed Methodology is open until March 12, 2014. We are also seeking feedback on whether the CSA should mandate the Proposed Methodology or, alternatively, adopt it as guidance for investment fund managers.

In relation to the second work stream of Stage 3, the CSA expect to publish for comment in Spring, 2014 proposed amendments aimed at implementing pre-sale delivery of the Fund Facts. The original proposals relating to the pre-sale delivery of Fund Facts were published for comment in June 2009. The CSA are revisiting the original 2009 proposals, informed by the regulatory regimes of other jurisdictions that have implemented pre-sale delivery requirements, by IOSCO principles, and by the comments received from stakeholders.

Finally, as part of the third work stream related to Stage 3, the CSA granted exemptive relief orders introducing an alternative delivery regime for ETFs which requires delivery of a summary disclosure document with the trade confirmations for all ETF purchases as of September 2013. The CSA exemptive relief orders cover all ETF manufacturers and bank-owned dealers, which account for approximately 80% of ETF trades. The codification of these orders encompassing a Fund Facts-type document for ETFs and an accompanying alternative delivery model is expected to be published for comment in Fall, 2014.

1.4 Modernization of Investment Fund Product Regulation

The mandate for this initiative is to review the regulation of publicly offered investment funds with a view to developing rules that recognize product developments and trends in the investment fund industry. The initiative is being carried out in two phases.

Phase 1 of this initiative, which amended National Instrument 81-102 Mutual Funds (NI 81-102) to update certain regulatory requirements for mutual funds, came into force in 2012.

Phase 2 of this initiative, now underway, consists of three parts:

• amendments to NI 81-102 to introduce core investment restrictions and operational requirements for publicly offered non-redeemable investment funds (the NI 81-102 Amendments);

• amendments to National Instrument 81-104 Commodity Pools to create a more comprehensive alternative investment fund framework that will operate in conjunction with the proposed amendments to NI 81-102 (the Alternative Fund Proposals); and

• the introduction of new requirements intended to enhance the disclosure provided by all investment funds related to securities lending, repurchase and reverse repurchase transactions and to keep pace with global regulatory developments (the Securities Lending Disclosure Requirements).

The Phase 2 proposals were published for comment on March 27, 2013 for a 90 day comment period. In June, 2013, the CSA received a request from 42 market participants asking for an extension of the comment period on the basis that the Phase 2 proposals represented fundamental changes to the regulatory framework for non-redeemable investment funds, and that market participants required additional time to formulate a constructive response. In light of this request, the CSA published CSA Staff Notice 11-324 Extension of Comment Period (Staff Notice 11-324), which announced that the comment period for the Phase 2 proposals was being extended until August 23, 2013. Staff Notice 11-324 also provided an update prioritizing the proposed amendments that the CSA intended to finalize, and indicated that implementation of the Alternative Fund Proposals would be considered in conjunction with certain investment restriction proposals for NI 81-102, which will be finalized and come into force at a later date.

By the closing of the comment period on August 23, 2013, the CSA had received 49 comment letters from a wide range of market participants, including investment fund managers, investment dealers, law firms and an investor advocate. The CSA have reviewed all the comments that were received and are currently working on responding to those comments with a view to finalizing the NI 81-102 Amendments and the Securities Lending Disclosure Requirements by Summer, 2014.

1.5 Exempt Market

As part of the OSC's exempt market initiative, we are pursuing the following efforts for investment funds as articulated in OSC Notice 45-712 Progress Report on Review of Prospectus Exemptions to Facilitate Capital Raising:

• Amending the accredited investor exemption to permit fully managed accounts, where the adviser has a fiduciary relationship with the investor, to purchase any securities on an exempt basis, including investment fund securities. Currently, in Ontario only, investment funds are carved out of the managed account category of the accredited investor exemption. Removing the carve-out would harmonize the managed account category of the accredited investor exemption in Canada. We are currently aiming to publish this amendment for comment as part of the CSA's review of the accredited investor and minimum amount exemptions.

• Improving data collection related to exempt market activities. We are currently developing for publication for comment enhanced reporting requirements and a revised form of Report of Exempt Distributions for investment fund issuers in Ontario.

1.6 Electronic Delivery of Documents

This is a reminder to all investment fund issuers that, effective February 19, 2014, OSC Rule 11-501 Electronic Delivery of Documents to the Ontario Securities Commission (OSC Rule 11-501), will make it mandatory for all market participants to electronically file a number of documents that are currently filed in paper format with the OSC.

OSC Rule 11-501 requires a number of documents to be electronically filed or delivered to the OSC, including:

• Form 45-106F1 and Form 45-501F1 Report of Exempt Distributions

• Applications for exemptive relief and notice filings

• Pre-files or waiver applications (for prospectuses or applications)

• Forms, notices and other materials required under Ontario's securities rules that are not filed through the System for Electronic Document Analysis and Retrieval (SEDAR), the System for Electronic Disclosure by Insiders (SEDI), or the National Registration Database (NRD).

Filers must electronically transmit the required documents through the electronic filing portal located on the OSC's website starting February 19, 2014, although market participants may elect to electronically file on a voluntary basis in the interim.

1.7 Scholarship Plans

On May 31, 2013, amendments to National Instrument 41-101 General Prospectus Requirements (NI 41-101), including new Form 41-101F3 Information Required in a Scholarship Plan Prospectus came into force (the New Form).

The New Form aims to improve the prospectus disclosure provided by scholarship plans by introducing a prospectus form tailored to reflect the unique features of this product. The New Form requires scholarship plans to provide investors with key information in a simple, accessible and comparable format to assist them in making a more informed investment decision.

Central to the New Form is the Plan Summary document. Similar to the Fund Facts for mutual funds, it is written in plain language, is to be no more than four pages, and highlights the potential risks and the costs of investing in a scholarship plan. It forms part of the prospectus, but is bound separately.

The timing of the coming into force of the New Form was designed to ensure that it was adopted by each scholarship plan provider during their 2013 prospectus renewal cycle. The CSA expect that adoption of the New Form will lead to more understandable and effective disclosure for investors, enabling them to better appreciate the possible outcomes and risks associated with investing in scholarship plans.

2. Emerging Issues and Trends

2.1 Investments in Mortgages

Over the course of the last year, we saw an incremental increase in the number of prospectus offerings by issuers, purporting to be investment funds, that proposed to invest substantially all of their assets in a pool of mortgages (a mortgage investment entity or MIE). Generally, the mortgages purchased by these MIEs are originated and serviced by one or more mortgage originators, who may or may not act as the MIE's manager. In most instances, the originator uses the MIE as a source of funding for the originator's mortgage lending business. In staff's view, this type of MIE is not an investment fund.

Staff provided guidance in OSC Staff Notice 81-722 Mortgage Investment Entities and Investment Funds, which was published on September 12, 2013, setting out the factors that staff would consider in determining whether an MIE is an investment fund. The notice detailed the reasons for staff's view, and reminded issuers that, since these MIEs are not considered investment funds, any initial prospectus filed by such issuers should be prepared and filed in the form of a completed Form 41-101F1 Information Required in a Prospectus, and any continuous disclosure should be filed in accordance with the continuous disclosure regime applicable to reporting issuers that are not investment funds (National Instrument 51-102 Continuous Disclosure Obligations).

2.2 Update on Linked Note Offerings

We continue to review novel linked note supplements filed for pre-clearance under National Instrument 44-102 Shelf Distributions: and CSA Staff Notice 44-304 Linked Notes Distributed under Shelf Prospectus System. We also continue to monitor the development of the industry generally and regulatory developments internationally.

We are becoming increasingly aware of the convergence of some notes with other investment products, particularly where the return on the notes is derived from the return on an investment fund. We are also reviewing the approach followed in other jurisdictions, such as the U.S., regarding disclosure of the fair value of the note on the cover page of the supplement. We are considering publishing guidance regarding the foregoing and as an update to CSA Staff Notice 44-304 in the upcoming fiscal year. We anticipate revising the pre-clearance criteria for notes linked to investment funds such that each offering of notes that is linked to one or more conventional mutual funds may be considered novel and subject to pre-clearance, whether a template was previously pre-cleared or not.

2.3 Increased Use of Derivatives

We have observed an increase in the use of derivatives by investment funds to offer more efficient investment exposure to areas that are harder to reach through direct investments, as well as to modify investment exposure in response to macro changes in the capital markets.

For example, certain investment funds are using currency derivatives to create fixed income exposure to emerging markets while holding domestic securities, and shorter term fixed income funds are creating exposure through interest rate derivatives while holding longer term debt. Funds are increasingly hedging and modifying their investment exposures in response to the changes in capital market expectations, including expectations relating to the direction of interest rates.

In response to this trend, our focus has been to ensure that there is a sufficient and appropriate level of disclosure so that investors can understand how the investment exposure is modified and created, and the additional risk that accompanies certain derivative transactions. We also focus on whether these exposure adjustments are within the fund's stated investment objectives and strategies.

2.4 Senior Secured and Floating Rate Loans

Over the course of the year, we observed an increase in offerings of non-investment grade fixed income products. As fixed income offerings move away from investment grade, our focus has been on ensuring that the disclosure by investment funds investing in fixed income securities provides sufficient information about the type, features and risks of the non-investment grade debt that is included in the investment fund portfolio. We note that, generally, the names and description of these investment funds (which include, for example, "senior" or "secured") may preclude investors from being alerted to the higher risks associated with the non-investment grade debt.

2.5 Character Conversion Transactions

On March 21, 2013, the Minister of Finance presented the federal government's 2013 budget. The budget contained amendments to the Tax Act (the Budget Amendments), which impacted investment funds that used specified derivatives (generally forward agreements) to provide investors with an economic return based on the performance of a reference fund.

Through the use of forward agreements, these funds were able to characterize the economic return of a reference fund, which would otherwise be treated as ordinary income in the hands of its securityholders, as capital gains. Investment funds that employed this structure generally have investment objectives of providing "tax advantaged" returns to securityholders. The Budget Amendments effectively prohibited the character conversion described above, meaning that from the effective date of the Budget Amendments, the economic returns provided to investors would be taxable as ordinary income.

Subsequent to the budget announcement, we issued OSC Staff Notice 81-719 Effect of Proposed Income Tax Act Amendments on Investment Funds -- Character Conversion Transactions (the Conversion Notice). The Conversion Notice stated that investment fund managers should consider the effects of the Budget Amendments on their investment funds, particularly if income conversion was an essential aspect of the fund, as evidenced by the fund's investment objective, name or the manner in which the fund was marketed. The Conversion Notice further advised investment fund managers that they should consider whether affected investment funds should be capped to new and additional investments.

Investment Funds staff took part in several discussions with senior staff from the Ministry of Finance (Canada) and Canada Revenue Agency concerning the Budget Amendments. In these discussions, we provided background information on the use of character conversion transactions by investment funds and the impact of the Budget Amendments.

As a result of the Budget Amendments, we reviewed a number of prospectus amendments for investment funds, as well as applications that were filed in connection with fundamental changes being made by investment funds to alter their investment structures.

3. Disclosure and Compliance Reviews

On an ongoing basis, OSC staff review the prospectus and continuous disclosure filings of Ontario-based investment funds. Risk-based criteria are used to select investment funds for reviews of their disclosure documents. We may also choose to conduct targeted reviews of a particular industry segment or on a particular topic. In addition to our prospectus and continuous disclosure reviews, the Investment Funds Branch works closely with staff in the Compliance and Registrant Regulation (CRR) Branch on issues related to fund manager compliance and identifying possible emerging issues. This sometimes leads to us conducting joint reviews.

3.1 Continuous Disclosure Reviews

This section discusses some of our reviews and findings in connection with:

• bullion funds

• risk ratings in Fund Facts

• sales communications/advertising

• fixed income ETFs

• operating expenses

3.1.1 Bullion Funds

In response to a significant drop in gold bullion prices in April 2013, staff conducted a targeted review of investment funds that hold substantially all of their assets in precious metals bullion. In order to understand how the funds and their managers responded to the market events, we asked about the asset flows in these funds and in bullion markets, as well as the impact of the market events on the premium and discount spread of bullion exchange-traded funds. We also looked into how the fund manager assessed each fund's ability to liquidate bullion to meet redemptions in times of stress. We were informed that physical markets for bullion remained liquid during this period of declining prices. In terms of fulfilling redemption requests, gold bullion funds generally benefit from: (i) the size of the gold bullion markets relative to the funds' holdings, and (ii) the short settlement period for gold bullion transactions relative to redemption transactions which affords the ability to know, with certainty, the required liquidity to support redemption activity.

3.1.2 Risk Ratings in Fund Facts

During the year, staff completed targeted continuous disclosure reviews of risk ratings of mutual funds disclosed in their Fund Facts. Staff have conducted similar reviews in the past and continue to monitor the risk ratings of mutual funds. As part of the review, staff focused on mutual funds in the same fund family that had both a currency hedged fund and an unhedged fund that provided exposure to the same underlying fund or portfolio. These reviews were initiated since staff noted that fund managers tend to rate both the currency hedged fund and the unhedged fund with the same risk ratings, even though volatility of past returns varied between the two funds. It is staff's view that the risk ratings for currency hedged funds should be determined separate and apart from their unhedged counterparts.

Staff communicated their views to a number of fund managers as part of these continuous disclosure reviews and also reiterated their views on this issue in the most recent Investment Funds Practitioner published in November 2013.

3.1.3 Sales Communications/Advertising

In July 2013, staff of the Investment Funds Branch issued OSC Staff Notice 81-720 Report on Staff's Continuous Disclosure Review of Sales Communications by Investment Funds (the Sales Communication Notice). The Sales Communication Notice sets out guidance based on our findings from a targeted continuous disclosure review of the advertising and marketing materials of publicly offered investment funds (the Sales Communication Review).

The Sales Communication Review began in May 2012. During the review, we selected 4 or 5 investment fund managers each quarter and asked for their sales communications for the previous three months. These included all published and non-print advertising in newspapers, presentations, brochures, internet ads, social media, fund manager websites, television and radio ads, email blasts, green sheets and any other marketing materials.

The fund managers included in our sample offered a range of fund types, including conventional mutual funds, closed-end funds, exchange-traded funds, commodity pools and labour sponsored investment funds. As the advertising of conventional mutual funds is primarily targeted to retail investors, we chose to focus a higher proportion of our CD reviews on this type of investment fund.

Included in our review were 8 medium to large mutual fund groups. Together, these fund groups have assets under management of more than $270 billion, or about 30% of the industry total, and offer more than 800 mutual funds to the public. We also selected 4 smaller fund groups, as well as some specialty funds. The ETF providers included in our sample represent approximately 20% of the ETF industry assets under management.

The Sales Communication Review found general compliance with disclosure requirements related to sales communications. However, some sales communications did not contain all the information mandated for a sales communication, but rather referred to another source, such as the fund's website or prospectus, for more information.

Key outcomes from the Sales Communication Review included:

• marketing, legal and/or compliance departments of fund managers initiated reviews of their current policies and procedures relating to marketing, and conducted training sessions with their staff on sales communications;

• potentially misleading performance charts in sales communications were removed or replaced with more balanced charts; and

• potentially misleading headlines and statements were removed from advertisements and marketing materials.

The Sales Communication Notice provided guidance to investment funds based on our observations from the Sales Communication Review. Topics on which we provided guidance included:

• the applicability of the disclosure requirements related to sales communications to materials created for branding purposes or for distribution to dealers;

• examples of features or statements that may cause a sales communication to be potentially misleading by creating an unrealistic expectation or an unjustified sense of safety, particularly from the perspective of the retail investor;

• the use of performance data in sales communications; and

• sales communications transmitted through alternative media.

3.1.4 Fixed Income ETFs

In response to the increased volatility seen in the fixed income markets, we undertook a review of fixed income ETFs, focusing on the liquidity of underlying assets and the effectiveness of the market making function by designated brokers. We examined how fund managers assessed the liquidity of the underlying assets of the ETFs. We also enquired with the ETF managers regarding the controls in place to ensure effective operation of the designated brokers' market making function, including details and scope of any legal agreements, number and size of market makers, monitoring programs and contingency plans. We wrote to four ETF managers, with head-offices in Ontario, covering more than 90% of ETF assets under management.

We noted that ETF managers generally conduct thorough due diligence when selecting and monitoring the designated brokers for their funds. ETF managers generally also appear to have good controls in place to monitor market quality statistics for their ETFs such as premiums/discounts to NAV or liquidity of underlying holdings. Where required, we have communicated further with individual ETF managers regarding industry best practices. Investment Funds staff will continue to monitor market quality statistics of the Canadian ETF market on an ongoing basis to identify any instances where regulatory action may be required.

3.1.5 Operating Expenses

During the year, staff highlighted the disclosure of fees and expenses as an area of particular focus for prospectus and continuous disclosure reviews. Subsequently, staff started a targeted review of the allocation of overhead expenses between fund managers and their funds, in particular, how fund managers address conflicts of interest and whether sufficient disclosure is provided to investors in prospectuses, financial statements and the management reports of fund performance relating to these related party transactions.

This targeted review focuses on all types of publicly offered investment funds, including conventional mutual funds, ETFs and closed-end funds, and included fund managers ranging from the largest to the smallest in terms of assets under management, as well as bank-affiliated fund managers. The review is currently ongoing and we intend to publish a staff notice in 2014 with the findings of the review.

3.2 Compliance and Registrant Regulation Branch and Investment Fund Manager Compliance Reviews

In November 2013, staff of the CRR Branch published OSC Staff Notice 33-742 OSC Annual Summary Report for Dealers, Advisers and Investment Fund Managers. The Staff Notice summarizes new and proposed rules and initiatives impacting registrants, current trends in deficiencies from compliance reviews of registrants (and suggested practices to address them), and current trends in registration issues.

Section 4.4 of OSC Staff Notice 33-742 contains information specifically for investment fund managers derived from the reviews carried out by the CRR Branch. Topics included:

• inappropriate expenses charged to funds,

• inadequate disclosure in offering memoranda,

• inadequate oversight of outsourced functions and service providers, and

• non-delivery of net asset value adjustments.

4. Outreach, Consultation and Education

We continue our efforts to be transparent regarding practices and procedures that impact investment fund issuers in as timely a manner as possible. Our intent in doing so is to better enable fund managers and their advisors to avoid potential regulatory issues when they are at the planning stage for a new fund or transaction. As indicated at various points earlier in this report, we publish guidance and updates for the investment fund industry periodically.

During the year, we updated stakeholders on the status of the IFRS-related amendments, before and after the publication of those amendments, at three events organized by national accounting firms. After publishing the amendments, we also presented to, and discussed the amendments with, the Investment Funds Standing Committee at CPA Canada. We have also participated in the discussion of on-going implementation issues at the IFRS Discussion Group at CPA Canada.

In our bid to provide responsive regulation, we engage in periodic discussions with, and seek feedback on our various policy initiatives from, other regulators such as the Mutual Fund Dealers Association of Canada and the Investment Industry Regulatory Organization of Canada. We also seek input from the OSC's Investor Advisory Panel, whose mandate is to solicit and represent the views of investors on the Commission's policy and rule-making initiatives.

As in past years, we met with staff from the Investment Management and Derivatives divisions of the Securities and Exchange Commission to discuss investment fund trends, novel products and emerging issues that are common to our respective jurisdictions. These meetings help ensure that our regulatory approaches to product development are consistent and that opportunities for regulatory arbitrage between our markets are minimized.

Finally, in an effort to ensure effective national oversight of the investment fund industry, the CSA's Investment Funds Committee holds monthly conference calls. The Committee provides a forum for discussing novel applications, policy interpretation and initiatives, and operational matters in a timely fashion. It ensures that regulatory requirements are nationally applied consistently, fairly, and effectively, pursuant to the Passport system. In January 2014, Rhonda Goldberg, Director of the Investment Funds Branch, was appointed Chair of the Committee.

4.1 Investment Funds Product Advisory Committee (IFPAC)

The OSC's IFPAC was established in August, 2011. The IFPAC, which is currently comprised of 12 external members, advises OSC staff specifically on emerging product developments and innovations occurring in the investment fund industry, and discusses the impact of these developments and emerging issues. The IFPAC also acts as one source of feedback to OSC staff on the development of policy and rule-making initiatives to promote investor protection, fairness and market efficiency across all types of investment fund products. The IFPAC meets quarterly and members serve a two year term. The initial two year term expired in Spring, 2013, with 6 members returning and 6 new members joining. You can find a list of current IFPAC members on the OSC website.

Topics of discussion with IFPAC this year have included the cost of ownership of investment fund products, the proposed risk classification methodology for use in the Fund Facts, linked notes, the exempt market review and the changes proposed to the Report of Exempt Distribution for investment fund issuers.

4.2 The Investment Funds Practitioner

The Investment Funds Practitioner is an overview of recent and topical issues arising from applications for discretionary relief, prospectuses and continuous disclosure documents that investment fund issuers file with the OSC and that are reviewed by the Investment Funds Branch. It is intended to assist investment fund managers and their advisors who regularly prepare public disclosure documents and applications for discretionary relief on behalf of investment funds. The Practitioner is also intended to make fund managers more broadly aware of some of the issues we have raised in connection with our reviews and how we have resolved them. The Practitioner can be found on our website www.osc.gov.on.ca at Information for Investment Funds.

We have published 2 editions of the Investment Funds Practitioner since last year's summary report: May 2013 and November 2013. We welcome suggestions for future topics.

4.3 IOSCO Committee 5 -- Investment Management

Investment Funds staff continued their participation in IOSCO C5 during 2013. This committee is focussed on investment management issues and is comprised of representatives from almost 30 regulators. The international developments discussed at C5 inform our policy and operational work, which is also guided by the principles and best practices published by IOSCO. During 2013, these included principles related to valuation, liquidity risk management and the regulation of ETFs. On January 8, 2014, IOSCO and the FSB jointly published a consultation document entitled "Assessment Methodologies for Identifying Non-Bank Non-Insurance Global Systemically Important Financial Institutions" for public comment. C5 participated in the development of the methodology for investment funds, including hedge funds, and fund managers. Current C5 initiatives include reviewing reliance on credit ratings and an examination of safe keeping and custody practices.

4.4 IOSCO Committee 8 -- Retail Investors

During the year, Howard Wetston, Chair and CEO of the OSC, was appointed Vice Chair of the Board of IOSCO. In June 2013 he was also appointed Chair of the newly formed IOSCO Committee 8. The Investment Funds Branch, with support from the Office of the Investor, Communications, the Investor Education Fund, and Office of Domestic and International Affairs branches of the OSC, assist the Chair of C8 in carrying out his duties.

The primary mandate for C8, which was approved by the IOSCO Board in June, 2013, is to conduct IOSCO's policy work on retail investor education and financial literacy. A secondary mandate is to advise the IOSCO Board on emerging retail investor protection matters.

C8 is intended to:

- reflect IOSCO's commitment to investor protection through the promotion of investor education and financial literacy and demonstrate a leadership role in developing guidance and policy for IOSCO members on behalf of retail investors

- be a forum to share experiences and develop approaches on investor education and financial literacy; and

- help the IOSCO Board take retail investor perspectives into account in prioritizing, coordinating and driving IOSCO's work.

During the year, OSC staff led C8's effort in the development of a strategic framework document. The purpose of this project is to identify and describe work streams that will establish the strategic direction of IOSCO's investor education and financial literacy efforts. This document sets out IOSCO's niche in investor education and financial literacy, current thinking and research, a strategy for program development, proposed work streams and best practices. It is anticipated that the best practices will be published for consultation by March, 2014.

5. Feedback and Contact Information

If you have any questions regarding, or feedback on, our third annual summary report, please send them to [email protected].

You can find additional information regarding investment funds and the Investment Funds Branch on our website.

We have also attached a list of Investment Funds Branch staff at the end of this report.

INVESTMENT FUNDS BRANCH

|

NAME |

|

|

|

|

|

Goldberg, Rhonda -- Director |

|

|

|

|

|

Chan, Raymond -- Manager |

|

|

|

|

|

McKall, Darren -- Manager |

|

|

|

|

|

Nunes, Vera -- Manager |

|

|

|

|

|

Alamsjah, Rosni -- Administrative Assistant |

|

|

|

|

|

Asadi, Mostafa -- Legal Counsel |

|

|

|

|

|

Au, Matthew -- Senior Accountant |

|

|

|

|

|

Bahuguna, Shaill -- Administrative Support Clerk |

|

|

|

|

|

Barker, Stacey -- Senior Accountant |

|

|

|

|

|

Bent, Christopher -- Legal Counsel |

|

|

|

|

|

Buenaflor, Eric -- Financial Examiner |

|

|

|

|

|

De Leon, Joan -- Review Officer |

|

|

|

|

|

Gerra, Frederick -- Legal Counsel |

|

|

|

|

|

Huang, Pei-Ching -- Senior Legal Counsel |

|

|

|

|

|

Jaisaree, Parbatee -- Administrative Assistant |

|

|

|

|

|

Joshi, Meenu -- Accountant |

|

|

|

|

|

Kalra, Ritu -- Senior Accountant |

|

|

|

|

|

Kearsey, Ian -- Senior Legal Counsel |

|

|

|

|

|

Kwan, Carina -- Legal Counsel |

|

|

|

|

|

Lee, Bryana -- Legal Counsel |

|

|

|

|

|

Lee, Irene -- Senior Legal Counsel |

|

|

|

|

|

Leonardo, Tracey -- Administrative Assistant |

|

|

|

|

|

Mainville, Chantal -- Senior Legal Counsel |

|

|

|

|

|

Marcovici, Harald -- Legal Counsel |

|

|

|

|

|

Nania, Viraf -- Senior Accountant |

|

|

|

|

|

Paglia, Stephen -- Senior Legal Counsel |

|

|

|

|

|

Persaud, Violet -- Review Officer |

|

|

|

|

|

Russo, Nicole -- Review Officer |

|

|

|

|

|

Schofield, Melissa -- Senior Legal Counsel |

|

|

|

|

|

Thomas, Susan -- Senior Legal Counsel |

|

|

|

|

|

Tong, Louisa -- Administrative Assistant |

|

|

|

|

|

Welsh, Doug -- Senior Legal Counsel |

|

|

|

|

|

Yu, Sovener -- Accountant |

|

|

|

|

|

Zaman, Abid -- Accountant |

|

{1} The consultations on the Discussion Paper included a public roundtable held at the OSC on June 7, 2013, followed by non-public consultations carried out by the British Columbia Securities Commission on June 24 and 25 and by the AMF on September 5, September 17 and October 3, 2013.