Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

CSA Notice and Request for Comment: Proposed Amendments to NI 41-101 General Prospectus Requirements and Proposed Consequential Amendments

CSA Notice and Request for Comment: Proposed Amendments to NI 41-101 General Prospectus Requirements and Proposed Consequential Amendments

PROPOSED AMENDMENTS TO

NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS

NATIONAL INSTRUMENT 44-101 SHORT FORM PROSPECTUS DISTRIBUTIONS

NATIONAL INSTRUMENT 44-102 SHELF DISTRIBUTIONS AND

NATIONAL INSTRUMENT 81-101 MUTUAL FUND PROSPECTUS DISCLOSURE

AND RELATED COMPANION POLICIES

AND

PROPOSED CONSEQUENTIAL AMENDMENTS

CSA Notice and Request for Comment

Appendices

Appendix A

Schedule A-1 -- Proposed Amendments to National Instrument 41-101 General Prospectus Requirements

Schedule A-2 -- Proposed Amendments to Companion Policy 41-101CP to National Instrument 41-101 General Prospectus Requirements

Appendix B

Schedule B-1 -- Blackline Showing Proposed Changes to National Instrument 41-101 General Prospectus Requirements

Schedule B-2 -- Blackline Showing Proposed Changes to Form 41-101F1 Information Required in a Prospectus

Schedule B-3 -- Blackline Showing Proposed Changes to Form 41-101F2 Information Required in an Investment Fund Prospectus

Schedule B-4 -- Blackline Showing Proposed Changes to Companion Policy 41-101CP to National Instrument 41-101 General Prospectus Requirements

Appendix C

Schedule C-1 -- Proposed Amendments to National Instrument 44-101 Short Form Prospectus Distributions

Schedule C-2 -- Proposed Amendments to Companion Policy 44-101CP to National Instrument 44-101 Short Form Prospectus Distributions

Appendix D

Schedule D-1 -- Blackline Showing Proposed Changes to National Instrument 44-101 Short Form Prospectus Distributions

Schedule D-2 -- Blackline Showing Proposed Changes to Form 44-101F1 Short Form Prospectus

Schedule D-3 -- Blackline Showing Proposed Changes to Companion Policy 44-101CP to National Instrument 44-101 Short Form Prospectus Distributions

Appendix E

Schedule E-1 -- Proposed Amendments to National Instrument 44-102 Shelf Distributions

Schedule E-2 -- Proposed Amendments to Companion Policy 44-102CP to National Instrument 44-102 Shelf Distributions

Appendix F

Proposed Amendments to National Instrument 81-101 Mutual Fund Prospectus Disclosure

Appendix G

Schedule G-1 -- Blackline Showing Proposed Changes to National Instrument 81-101 Mutual Fund Prospectus Disclosure

Schedule G-2 -- Blackline Showing Proposed Changes to Form 81-101F2 Contents of Annual Information Form

Appendix H

Schedule H-1 -- Proposed Amendments to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

Schedule H-2 -- Proposed Amendments to Companion Policy 52-107CP to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

Appendix I

Schedule I-1 -- Blackline Showing Proposed Changes to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

Schedule I-2 -- Blackline Showing Proposed Changes to Companion Policy 52-107CP to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

Appendix J

Proposed Amendments to National Instrument 51-102 Continuous Disclosure Obligations

Appendix K

Proposed Amendments to National Instrument 13-101 System for Electronic Document and Analysis Retrieval

Appendix L

Information required by local securities legislation

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

CSA Notice and Request for Comment

NOTICE AND REQUEST FOR COMMENT

PROPOSED AMENDMENTS TO

NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS AND COMPANION

POLICY 41-101CP TO NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS

REQUIREMENTS

AND

PROPOSED AMENDMENTS TO

NATIONAL INSTRUMENT 44-101 SHORT FORM PROSPECTUS DISTRIBUTIONS AND

COMPANION POLICY 44-101CP TO NATIONAL INSTRUMENT 44-101 SHORT FORM

PROSPECTUS DISTRIBUTIONS

AND

PROPOSED AMENDMENTS TO

NATIONAL INSTRUMENT 44-102 SHELF DISTRIBUTIONS AND

COMPANION POLICY 44-102CP TO NATIONAL INSTRUMENT 44-102

SHELF DISTRIBUTIONS

AND

PROPOSED AMENDMENTS TO

NATIONAL INSTRUMENT 81-101 MUTUAL FUND PROSPECTUS DISCLOSURE

AND

RELATED COMPANION POLICIES

AND

PROPOSED CONSEQUENTIAL AMENDMENTS

July 15, 2011

Introduction

We, the Canadian Securities Administrators (CSA), are publishing for a 90-day comment period proposed amendments to:

• National Instrument 41-101 General Prospectus Requirements (NI 41-101);

• Companion Policy 41-101CP Companion Policy to National Instrument 41-101 General Prospectus Requirements (41-101CP);

• National Instrument 44-101 Short Form Prospectus Distributions (NI 44-101);

• Companion Policy 44-101CP to National Instrument 44-101 Short Form Prospectus Distributions (44-101CP);

• National Instrument 44-102 Shelf Distributions (NI 44-102);

• Companion Policy 44-102CP to National Instrument 44-102 Shelf Distributions (44-102CP); and

• National Instrument 81-101 Mutual Fund Prospectus Disclosure (NI 81-101).

We are also publishing proposed consequential amendments to:

• National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards (NI 52-107);

• Companion Policy 52-107CP to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards (52-107 CP);

• National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102); and

• National Instrument 13-101 System for Electronic Document and Analysis Retrieval (NI 13-101).

The references above to a national instrument include its form(s).

The proposed amendments to NI 41-101, 41-101CP, NI 44-101, 44-101CP, NI 44-102, 44-102CP and NI 81-101 are collectively referred to in this notice as the "Proposed Amendments".

Proposed Text

The text of the Proposed Amendments is contained in the following Appendices A to K.

|

Appendix A

|

Proposed Amendments to NI 41-101 and 41-101CP

|

|

|

|

|

Appendix B

|

Blackline Showing Proposed Changes to NI 41-101 and 41-101CP

|

|

|

|

|

Appendix C

|

Proposed Amendments to NI 44-101 and 44-101CP

|

|

|

|

|

Appendix D

|

Blackline Showing Proposed Changes to NI 44-101 and 44-101CP

|

|

|

|

|

Appendix E

|

Proposed Amendments to NI 44-102 and 44-102CP

|

|

|

|

|

Appendix F

|

Proposed Amendments to NI 81-101

|

|

|

|

|

Appendix G

|

Blackline Showing Proposed Changes to NI 81-101

|

|

|

|

|

Appendix H

|

Proposed Consequential Amendments to NI 52-107 and 52-107CP

|

|

|

|

|

Appendix I

|

Blackline Showing Proposed Changes to NI 52-107 and 52-107CP

|

|

|

|

|

Appendix J

|

Proposed Consequential Amendments to NI 51-102

|

|

|

|

|

Appendix K

|

Proposed Consequential Amendments to NI 13-101

|

We invite comment on the Proposed Amendments.

Background

NI 41-101 provides a comprehensive set of prospectus requirements for issuers. NI 44-101 sets out requirements for an issuer intending to file a prospectus in the form of a short form prospectus. NI 44-102 sets out requirements for a distribution under a short form prospectus using shelf procedures. NI 81-101 sets out requirements for an issuer that is a mutual fund to file a simplified prospectus, annual information form and fund facts document. NI 41-101, NI 44-101, NI 44-102 and NI 81-101 are collectively referred to in this notice as the "Prospectus Rules".

Purpose of the Proposed Amendments

The primary purpose of the Proposed Amendments is to amend the Prospectus Rules and their related companion policies to address user experience and the CSA's experience with the Prospectus Rules since the implementation of the general prospectus rule, NI 41-101, on March 17, 2008. As part of a post-adoption process following implementation of NI 41-101, the CSA has tracked issues that have arisen in connection with NI 41-101 and other Prospectus Rules and has developed amendments to address those issues where warranted.

The Proposed Amendments to the Prospectus Rules are intended to:

• clarify certain provisions of the Prospectus Rules;

• address significant identified gaps in the Prospectus Rules;

• modify certain requirements in the Prospectus Rules to enhance their effectiveness;

• remove or streamline certain requirements in the Prospectus Rules that are burdensome for issuers and of limited utility for investors or securityholders; and

• codify prospectus relief that has been granted in the past.

Summary of Key Proposed Amendments

This section describes the key Proposed Amendments. It is not a complete list of all the Proposed Amendments.

Certain key Proposed Amendments apply to all issuers other than investment funds. These are described below in Part I under sections (a) through (k). Other key Proposed Amendments apply specifically to investment funds. These are described below in Part II under sections (l) through (s).

Part I -- Key Proposed Amendments Generally Applicable to Issuers

(a) No Minimum Offering Amount

In the course of conducting prospectus reviews, the CSA identified concerns with certain best effort offerings that were not subject to a minimum offering amount by issuers that:

• faced significant short-term non-discretionary expenditures or significant short-term capital or contractual commitments, and

• did not appear to have other readily accessible resources to satisfy those expenditures or commitments.

While an issuer may not propose to provide a minimum offering amount, the CSA has determined that additional disclosure is warranted in such cases. The CSA therefore proposes enhanced requirements in connection with the issuer's use of proceeds, as set out in proposed new subsections 6.3(3) and (4) of Form 41-101F1 Information Required in a Prospectus (Form 41-101F1) and equivalent new subsections 4.2(3) and (4) of Form 44-101F1 Short Form Prospectus (Form 44-101F1). However, regulators may still expect an issuer to provide a minimum offering amount in certain circumstances depending on the severity of the issuer's financial situation, results of the regulator's review and the application of receipt refusal provisions under securities law. This is clarified in a Proposed Amendment to section 2.2.1 of 41-101CP.

(b) Personal Information Form Reforms

In order to help regulators determine the suitability of directors and executive officers of an issuer filing a prospectus, the CSA introduced a detailed personal information form (PIF) for directors and executive officers in 2008. Since that time, we have identified a number of issues with the PIF filing requirement. For instance, under the current rules, an issuer is not required to submit a new PIF for an individual even if a number of years has passed since the filing of the previous PIF, nor is an issuer required to confirm that the previously filed PIF is still correct. Additionally, the rules do not permit us to accept the PIF that a different issuer may have filed for the same individual.

The CSA therefore proposes the following changes to the PIF:

1. We propose to define a "personal information form" in NI 41-101 to formally include a TSX or TSX Venture Exchange PIF, provided that an NI 41-101 certificate and consent is appended to it and the information contained in the PIF continues to be correct at the time that the NI 41-101 certificate and consent is executed.

2. We propose to require that an issuer file a PIF with the regulator for an individual (i.e. director, executive officer, etc. as prescribed under subparagraph 9.1(b)(ii) of NI 41-101) at the time of each prospectus filing.

3. We propose to exempt the issuer from the requirement described in paragraph 2 above if, at the time of the prospectus filing:

(a) an issuer filed a PIF of that individual with the regulator within the past 3 years;

(b) the responses of that individual to certain key questions in his or her PIF (questions 4(b) and (c) and questions 6 through 9 of the current PIF and questions 6 through 10 of the proposed amended PIF) have not changed; and

(c) a certificate is filed by the issuer identifying the previous PIF filing (by either appending the previously filed PIF to the certificate or providing certain information) and giving the confirmation in paragraph (b) above.

4. We propose to make minor amendments to the PIF to remove certain personal questions that are of limited utility and to align with the TSX and TSX Venture Exchange PIFs.

(c) Contractual Rights of Rescission

The CSA has identified an investor protection concern that arises where the distribution of a convertible, exchangeable or exercisable security is qualified under a prospectus and the subsequent conversion, exchange or exercise is made on a prospectus-exempt basis within a short period of time following the purchase of the original security under the prospectus. Under provincial securities legislation in effect in most provinces, the purchaser does not have a right of rescission in respect of the underlying security.

For this reason, we propose to modify the guidance in section 2.9 of 41-101CP to clarify that in certain circumstances, the issuer should provide the purchaser with a contractual right of rescission in respect of the issuance of the underlying security where the conversion, exchange or exercise of the security could occur within a short period of time (generally within 180 days) of the purchase of the security under the prospectus.

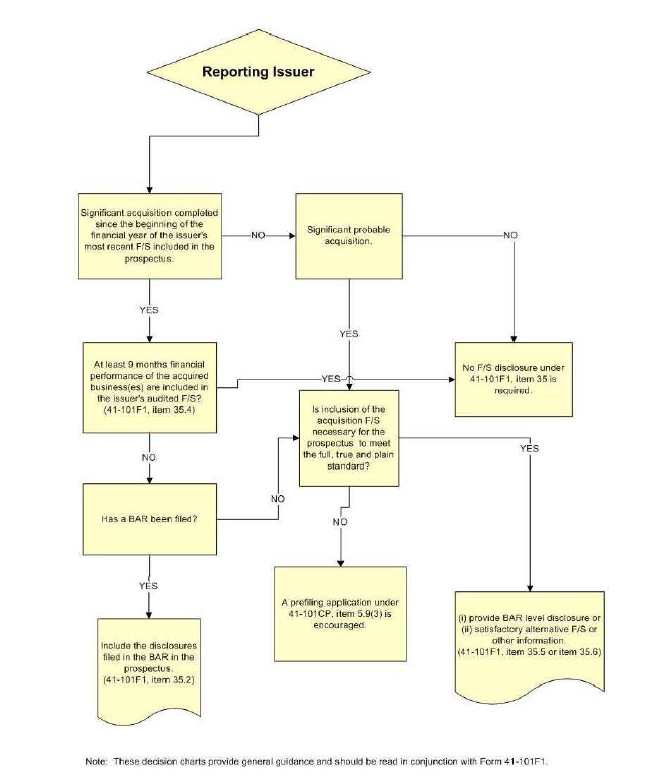

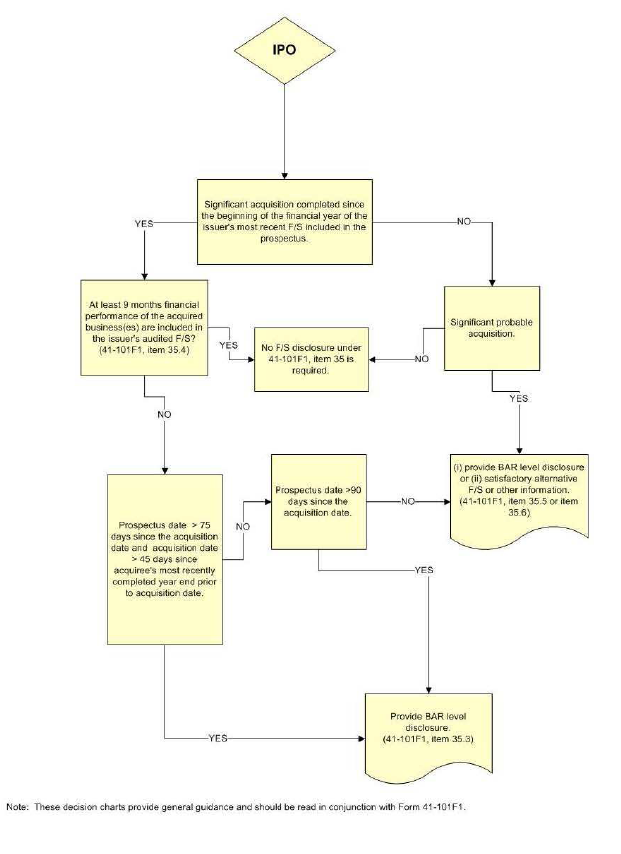

(d) Interaction of Items 32 and 35 in Form 41-101F1: Significant Acquisitions that Are Also Acquisitions of a Primary Business or Predecessor Entity

A proposed or completed significant acquisition by an issuer filing a prospectus in the form of Form 41-101F1 may also constitute an acquisition of a primary business for the issuer or a predecessor entity of the issuer. For example, this is generally the case where the significance of the acquisition to the issuer exceeds 100%. In these circumstances, the issuer must include financial statements pursuant to Item 32 of Form 41-101F1 (by operation of section 32.1 of Form 41-101F1), rather than Item 35 of Form 41-101F1.

However, the interaction of Items 32 and 35 of Form 41-101F1 -- both of which could apply to a significant acquisition by an issuer have been confusing to some users, particularly in the case of reporting issuers.

We have therefore clarified in both Items 32 and 35 of Form 41-101F1 that a non-reporting issuer or a shell reporting issuer that has carried out a significant acquisition that constitutes the acquisition of a primary business or predecessor entity of the issuer is required to disclose the financial statements under Item 32 and not under Item 35. The imposition of this clarifying provision regarding subsequent prospectus filings by shell reporting issuers does not represent a substantive new requirement because these issuers would generally have already had to report the significant acquisition in a previously filed information circular containing Item 32 prospectus-level disclosure for the significant acquisition.

The Proposed Amendments also clarify the circumstances when an issuer must provide pro forma financial statements if it has made an acquisition that constitutes the acquisition of a primary business or predecessor entity of the issuer.

Pursuant to new proposed section 32.7 of Form 41-101F1, we will only require the pro forma financial statement disclosure to reflect the effect of a proposed or completed acquisition of a primary business or predecessor entity by an issuer if such pro forma statements are necessary for full, true and plain disclosure of all material facts relating to the securities being distributed.

(e) Exemption from Incorporation by Reference of Reports/Opinions Produced in Information Circular

The CSA proposes to codify relief we have granted to issuers allowing them to exclude from their prospectuses reports or opinions of experts that are incorporated by reference into the prospectus indirectly through the incorporation by reference of a special meeting information circular. These circulars generally relate to a restructuring transaction or other special business of the issuer where the issuer or its board of directors engaged an expert to provide advice that is specific to the business transacted at the special meeting.

For example, a board may retain a firm to provide a fairness opinion to assist the board in determining whether to recommend that a proposed transaction be approved by the issuer's shareholders. Similarly, an issuer may include a tax opinion that is specific to the proposed transaction. Given the limited purpose and nature of the expert's engagement, the CSA has determined that in some cases it is not necessary to incorporate by reference those types of reports or opinions that are specific in nature and scope. This proposed exemption is set out in proposed new subsection 11.1(3) of Form 44-101F1.

(f) Prior Sales and Trading Price and Volume Disclosure

The CSA proposes to modify the prospectus disclosure relating to prior sales information and trading price and volume information contained in Item 13 of Form 41-101F1 and Item 7A of Form 44-101F1 as follows:

• clarify that if an issuer is distributing a series of debt under the prospectus, it must provide prior sales and trading price and volume disclosure in respect of that series of debt; and

• streamline the prior sales and trading price and volume disclosure so that it only applies to the class or series of securities that is being distributed under the prospectus, as that information is the most relevant to the investor purchasing that security.

(g) Non-Issuer's Submission to the Jurisdiction and Appointment of Agent for Service

We propose to amend the requirement to file a non-issuer's submission to the jurisdiction and appointment of an agent for service contained in subparagraph 9.2(a)(vii) of NI 41-101, Appendix C of NI 41-101 and subparagraph 4.2(a)(vi) of NI 44-101. Under the current requirement in subparagraph 9.2(a)(vii) of NI 41-101, a person or company residing outside Canada that is required to sign or provide a certificate must submit to our jurisdiction and appoint an agent in Canada.

We propose to expand the existing requirement to all foreign directors of the issuer, as all directors are liable in our statutory liability regime for misrepresentations contained in the prospectus. The proposed amendments will be made to subparagraph 9.2(a)(vii) of NI 41-101 and subparagraph 4.2(a)(vi) of NI 44-101.

We also propose amendments to clarify the related disclosure on enforceability of judgments against foreign persons and companies in sections 1.12 of Form 41-101F1 and 1.11 of Form 44-101F1 accordingly.

Potential further extension of filing requirement to foreign experts

CSA staff are also considering, as part of the Proposed Amendments, to further extend the requirement to file a non-issuer's submission to the jurisdiction and appointment of an agent for service form to all foreign experts (such as, for example, "qualified persons" or auditors) who have consented to the disclosure in a prospectus of information from a report, opinion or statement made by them. These persons are liable under our statutory liability regime for misrepresentations in the prospectus that are derived from report, opinion or statement.

In order to effect this potential amendment subparagraph 9.2(a)(vii) of NI 41-101 would be amended to include "each person required to file a consent under section 10.1" and section 1.12 of Form 41-101F1 would be amended to encompass "a person who is required to file a consent under section 10.1 of the Instrument". Corresponding changes would also be made to NI 44-101 and Form 44-101F1.

We are interested in your comments on this potential change. Please refer to the "Comments" section of this Notice for our specific questions on the potential extension of the non-issuer's submission to the jurisdiction and appointment of an agent for service form filing requirement to all foreign experts. Upon consideration of public comments, CSA staff may determine to implement this change as part of the Proposed Amendments.

(h) Successor Issuer

Based on our prospectus reviews, we have reconsidered the successor issuer criteria for purposes of short-form eligibility. In the Proposed Amendments we have modified the successor issuer definition to address areas where further clarification was required, including:

• in circumstances where the successor issuer acquired a business from a predecessor that represented less than all of the predecessor's business, we have clarified that substantially all of the business must have been divested by the predecessor to the successor in order for the issuer to be considered a successor issuer. This amendment is intended to ensure that an issuer will only be considered a successor issuer (and thereby become short-form eligible despite its fairly recent status as a reporting issuer) if the historical financial statements of its predecessor are a relevant, accurate proxy for the successor issuer's financial statements; and

• we have clarified that a successor issuer can include a reverse takeover (RTO) acquiree, i.e. an issuer can be a successor to itself.

We have also expanded the application of section 2.7 of NI 44-101 to permit a capital pool company listed on the TSX Venture Exchange to be considered short-form eligible under this provision if it is a successor issuer and has filed a filing statement in connection with an RTO or a qualifying transaction.

(i) Primary Business Oil & Gas Exemption to Provide Operating Statements

We propose to extend the exemption available to oil and gas issuers carrying out acquisitions that would be considered acquisitions of a primary business or predecessor entity to rely on operating statements (in lieu of financial statements) when providing financial statement disclosure about the acquisition. This proposed exemption is found in new proposed section 32.9 of Form 41-101F1.

Also, based on prior requests for relief which we have granted, we have developed a provision to exempt an oil and gas issuer from having to provide an audited operating statement the third year back if a recent independent reserves evaluation (in the forms of Form 51-101F1 Statement of Reserves Data and Other Oil and Gas Information, Form 51-101F2 Report on Reserves Data by Independent Qualified Reserves Evaluator or Auditor and Form 51-101F3 Report of Management and Directors on Oil and Gas Disclosure) has been prepared (and included in the prospectus) with an effective date within 6 months of the preliminary prospectus receipt date.

(j) Notice of Intention Exemption

Presently an issuer that is new to the short form prospectus regime must file a notice declaring its intention to be qualified to file a short form prospectus at least 10 business days prior to the filing of the preliminary short form prospectus. We propose to exempt a successor issuer from having to wait the 10 business day period to file its preliminary prospectus if its predecessor issuer previously filed the notice of intention. The successor issuer would still need to file the notice of intention either prior to or concurrently with the filing of the preliminary prospectus. We also propose a similar exemption for a credit support issuer which relies upon the continuous disclosure record of its credit supporter.

(k) Time to File Final Prospectus

Presently, pursuant to subsection 2.3(1) of NI 41-101, an issuer must file its final prospectus no later than 90 days after the date of the receipt of its preliminary prospectus. We propose to clarify that if an issuer files an amendment to a preliminary prospectus, the 90-day time period will recommence from the date of the receipt of the amendment to the preliminary prospectus. However, irrespective of the filing of one or more amendments to the preliminary prospectus, an issuer shall not be permitted to file the final prospectus more than 180 days after the date of the receipt for the preliminary prospectus.

Part II -- Key Proposed Amendments Applicable to Investment Funds

(l) Non-Canadian Investment Funds

We propose to extend the existing disclosure requirement for foreign investment fund managers to foreign investment funds and any other non-Canadian entity required to provide a certificate under Part 5 of NI 41-101 or other securities legislation.

(m) Leverage Disclosure for Investment Funds

We propose to enhance the disclosure requirements relating to the use of leverage as an investment strategy in the prospectus summary and body of a prospectus in the form of Form 41-101F2 Information Required in an Investment Fund Prospectus (Form 41-101F2). The enhanced disclosure requirements are intended to provide investors with a better understanding of how the investment fund intends to utilize leverage and the nature of the leverage that may be used by the investment fund.

We propose to modify the prospectus disclosure in paragraph 3.3(1)(e) of Form 41-101F2 and paragraph 6.1(1)(b) of Form 41-101F2 as follows:

• for leverage created through borrowing or the issuance of preferred securities, the investment fund must disclose the maximum amount of leverage it may use as a ratio of its maximum total assets divided by its net asset value; and

• if leverage is created through the use of specified derivatives or similar instruments, the investment fund must disclose the maximum amount of leverage the investment fund may use as a multiple of net assets and explain how the investment fund uses the term "leverage" and the significance of the maximum and minimum amounts of leverage to the investment fund.

An instruction in Form 41-101F2 states that for the purposes of the above disclosure requirements, the term "specified derivative" has the same meaning as in National Instrument 81-102 Mutual Funds.

(n) Investment Fund Trading Expense Ratio Disclosure

In addition to the current requirement to disclose an investment fund's annual returns and management expense ratio for the past five years in subsection 3.6(4) of Form 41-101F2 and Item 11 of Form 41-101F2, we propose a requirement that the investment fund's trading expense ratio for the past five years be disclosed. An investment fund's trading expense ratio represents the total trading commissions and costs of the investment fund as a percentage of its net assets. This disclosure requirement will better enable investors to determine the full costs of owning an investment fund or compare the historical costs of different investment funds.

(o) Organization and Management Details of the Investment Fund

We propose to amend the current disclosure required by Item 19 of Form 41-101F2 relating to the organizational and management details of an investment fund to require the disclosure of the following additional information:

• an expanded requirement to disclose current or past bankruptcies of and cease trade orders against any issuer, as opposed to the current disclosure requirement that only applies to investment fund issuers, where the directors or executive officers of the investment fund or its investment fund manager were directors of or held specified executive positions with the issuer,

• enhanced disclosure of ownership interests in the investment fund and its investment fund manager for directors and executive officers of the investment fund and investment fund manager and members of the investment fund's independent review committee; and

• a new disclosure requirement relating to principal distributors of investment funds and a requirement that principal distributors of investment funds sign a prospectus certificate in the same form as the investment fund.

(p) Principal Securityholders

We propose to amend the disclosure of principal securityholders of the investment fund as required by subsection 28.1(1) of Form 41-101F2, to limit disclosure to circumstances where this information is known or ought to be known by the investment fund or its investment fund manager. This amendment will predominantly affect exchange traded funds in continuous distribution (ETFs), who may not be able to readily determine their beneficial owners. Disclosure of this information has less utility for ETFs because it would only reflect ownership at a moment in time and beneficial securityholders of ETFs may change very quickly. The amendment is also consistent with exemptive relief from certain takeover bid requirements that many ETFs have received.

(q) Mutual Fund Personal Information Form Reforms

We have drafted reforms to the PIF delivery requirements in NI 81-101 that correspond with the proposed NI 41-101 reforms relating to the PIF. These amendments are intended to address the issues described above and conform the PIF delivery requirements for conventional mutual funds with those for other issuers.

(r) Documents Incorporated by Reference in a Mutual Fund Prospectus

We propose to amend section 3.1 of NI 81-101 to require the incorporation by reference, where a mutual fund has not yet filed interim or annual financial statements, of the audited balance sheet filed with the mutual fund's simplified prospectus. We also propose to require the incorporation by reference of a mutual fund's interim financial statements and interim management report of fund performance (MRFP), where the mutual fund has not yet filed its annual comparative financial statements and annual MRFP.

(s) Principal Distributor Certificate for Mutual Funds

We propose to amend the principal distributor certificate required by Form 81-101F2 Contents of Annual Information Form to require a principal distributor of a mutual fund to provide the same certificate as the mutual fund and the manager of the mutual fund.

Consequential Amendments

(a) Consequential Amendments to NI 52-107

We propose amendments to NI 52-107 to ensure that the operating statements which a prospectus filer is permitted to provide under new proposed section 32.9 of Form 41-101F1 (described under section (i) in Part I of the Summary of Key Proposed Amendments above) can benefit from the financial reporting framework available in NI 52-107 for oil and gas operating statements.

We also propose to repeal the financial reporting framework for carve-out financial statements presently found in subsection 3.11(6) of NI 52-107. As corroborated by external feedback, we do not feel it is necessary for the CSA to prescribe a separate financial reporting framework for carve-out financial statements. It is our view that auditors will generally be able to confirm that the carve-out financial statements have been prepared in accordance with International Financial Reporting Standards, and that instances in which this is not the case will be relatively rare.

(b) Consequential Amendments to NI 51-102

Presently an issuer is permitted to utilize operating statements, in lieu of financial statements, if it complies with the requirements of section 8.10 of NI 51-102. One requirement is that the acquisition must be an asset acquisition. We propose to expand this provision's application to a share acquisition in certain restricted circumstances. Specifically, the vendor must have transferred the applicable oil and gas assets to a corporation that will be considered the transferor of the transaction and was created for the sole purpose of facilitating the acquisition, and this transferor had no assets or operations other than those attributable to the transferred oil and gas assets. A parallel proposed amendment is provided in section 32.9 of Form 41-101F1 for an acquisition that constitutes the acquisition of a primary business of the issuer.

(c) Consequential Amendments to NI 13-101

We propose amendments to NI 13-101 to update the terminology used for various types of prospectus forms referenced in Appendix A of NI 13-101. Certain of these references are out-of-date.

Anticipated Costs and Benefits

We are proposing the Proposed Amendments to the Prospectus Rules because of issues identified in prospectus reviews, applications for exemptive relief from prospectus requirements and recurring inquiries from prospectus filers or CSA staff concerning certain prospectus requirements.

The Proposed Amendments are designed to enhance the effectiveness of the prospectus disclosure standards, clarify the requirements, address significant identified gaps, and modify or streamline requirements where warranted. The CSA anticipates that these modifications will ease the process and burden of prospectus disclosure for issuers while at the same time delivering effective, relevant and meaningful disclosure to investors.

Alternatives Considered

We considered maintaining the status quo. However, as discussed above, many of the Proposed Amendments are intended to clarify the Prospectus Rules or to modify or streamline Prospectus Rule requirements where warranted.

Therefore, to provide the appropriate degree of certainty, clarity and consistency among affected issuers, we considered it preferable to amend, replace and add provisions to the Prospectus Rules and associated guidance.

Unpublished Materials

In developing the Proposed Amendments to the Prospectus Rules, we have not relied on any significant unpublished study, report, or other written materials.

Local Notices

Certain jurisdictions will publish other information required by local securities legislation in Appendix L to this notice.

Comments

We request your comments on the Proposed Amendments to the Prospectus Rules. In addition to any general comments you have, we also invite comments on the following specific topic:

Questions relating to Non-Issuer's Submission to the Jurisdiction and Appointment of Agent for Service

As described in paragraph (g) of the "Summary of Key Proposed Amendments" section of this Notice, we are considering further extending the requirement to file a non-issuer's submission to the jurisdiction and appointment of an agent for service form to all foreign experts who have consented to the disclosure in a prospectus of information from a report, opinion or statement made by them.

We are interested in your general comments on this potential change. In particular, we welcome your comments on the following questions:

(a) Do you believe that it is appropriate to extend the requirement to file a non-issuer's submission to the jurisdiction and appointment of an agent for service form to foreign experts who have consented to the disclosure in a prospectus of information from a report, opinion or statement made by them given that these persons are liable under our statutory liability regime for misrepresentations in the prospectus that are derived from that report, opinion or statement? Why or why not?

(b) If foreign experts are required to file a non-issuers' submission to the jurisdiction and appointment of an agent for service form, do you anticipate that this obligation will impose any significant practical or financial burden on these experts or issuers? If so, please explain why. Would your response change if the form requirement for foreign experts only concerned either submission to the jurisdiction or an appointment of an agent for service?

Please provide your comments in writing by October 14, 2011. Regardless of whether you are sending your comments by email, you should also send or attach your submissions in an electronic file in Microsoft Word, Windows format.

Address your submissions to the following Canadian securities regulatory authorities:

British Columbia Securities Commission

Alberta Securities Commission

Saskatchewan Financial Services Commission

Manitoba Securities Commission

Ontario Securities Commission

Autorité des marchés financiers

Superintendent of Securities, Prince Edward Island

Nova Scotia Securities Commission

New Brunswick Securities Commission

Securities Commission of Newfoundland and Labrador

Superintendent of Securities, Yukon Territory

Superintendent of Securities, Northwest Territories

Superintendent of Securities, Nunavut

Deliver your comments only to the address that follows. Your comments will be distributed to the other participating CSA member jurisdictions.

Alex Poole

Senior Legal Counsel, Corporate Finance

Alberta Securities Commission

Suite 600, 250-5th Street SW

Calgary, Alberta T2P 0R4

Fax: (403) 297-4482

Email: [email protected]

Anne-Marie Beaudoin

Corporate Secretary

Autorité des marchés financiers

800, square Victoria, 22e étage

C.P. 246, tour de la Bourse

Montréal, Québec H4Z 1G3

Fax: 514-864-6381

Email: [email protected]

Please note that comments received will be made publicly available and posted at www.albertasecurities.com and the websites of certain other securities regulatory authorities. We cannot keep submissions confidential because securities legislation in certain provinces requires that a summary of the written comments received during the comment period be published.

Questions

A. Questions relating to Investment Funds

Certain Proposed Amendments apply only to investment funds. These amendments are found in Form 41-101F2 Information Required in an Investment Fund Prospectus and NI 81-101 including Form 81-101F2 Contents of Annual Information Form. Also, the key Proposed Amendments applicable to investment funds are described above under Part II of the Summary of Key Proposed Amendments. If your questions relate to these Proposed Amendments, please refer your questions to any of:

Christopher Birchall

Senior Securities Analyst, Corporate Finance

British Columbia Securities Commission

604-899-6722

Ian Kerr

Senior Legal Counsel, Corporate Finance

Alberta Securities Commission

403-297-2659

Bob Bouchard

Director

Manitoba Securities Commission

204-945-2555

Ian Kearsey

Legal Counsel, Investment Funds Branch

Ontario Securities Commission

416-593-2169

Chantal Leclerc

Senior Policy Advisor

Autorité des marchés financiers

514-395-0337 ext. 4463

Anick Ouellette

Analyst, Investment Funds Branch

Autorité des marchés financiers

514-395-0337 ext. 4472

B. All Other Questions relating to the Proposed Amendments

Certain Proposed Amendments apply to issuers other than investment funds. These amendments are found in NI 41-101 including Form 41-101F1 Information Required in a Prospectus, NI 44-101 including Form 44-101F1 Short Form Prospectus, NI 44-102 and the Consequential Amendments to NI 52-107, NI 51-102 and NI 13-101. Also, the key Proposed Amendments applicable to such issuers are described above under Part I of the Summary of Key Proposed Amendments. If your questions relate to these Proposed Amendments, please refer your questions to any of:

Larissa Streu

Senior Legal Counsel, Corporate Finance

British Columbia Securities Commission

604-899-6888

Allan Lim

Manager, Corporate Finance

British Columbia Securities Commission

604-899-6780

Alex Poole

Senior Legal Counsel, Corporate Finance

Alberta Securities Commission

403-297-4482

Blaine Young

Associate Director, Corporate Finance

Alberta Securities Commission

403-297-4220

Cheryl McGillivray

Manager, Corporate Finance

Alberta Securities Commission

403-297-3307

Ian McIntosh

Deputy Director, Corporate Finance

Saskatchewan Financial Services Commission - Securities Division

306-787-5867

Bob Bouchard

Director

Manitoba Securities Commission

204-945-2555

Matthew Au

Senior Accountant, Corporate Finance

Ontario Securities Commission

416-593-8132

Jason Koskela

Legal Counsel, Corporate Finance

Ontario Securities Commission

416-595-8922

Rosetta Gagliardi

Senior Policy Advisor

Autorité des marchés financiers

514-395-0337 ext. 4462

Chantal Leclerc

Senior Policy Advisor

Autorité des marchés financiers

514-395-0337 ext. 4463

Natalie Brown

Analyste expert, financement des sociétés

Senior Securities Analyst, Corporate finance

Autorité des marchés financiers

514-395-0337 ext. 4388

Kevin Redden

Director, Corporate Finance

Nova Scotia Securities Commission

902-424-5343

Pierre Thibodeau

Senior Securities Analyst

New Brunswick Securities Commission

506-643-7751

List of Appendices

|

Appendix A

|

Proposed Amendments to National Instrument 41-101 General Prospectus Requirements and Companion Policy 41-101CP to National Instrument 41-101 General Prospectus Requirements

|

|

|

|

||

|

|

Schedule A-1

|

Proposed Amendments to National Instrument 41-101 General Prospectus Requirements

|

|

|

Schedule A-2

|

Proposed Amendments to Companion Policy 41-101CP to National Instrument 41-101 General Prospectus Requirements

|

|

|

||

|

Appendix B

|

Blackline Showing Proposed Changes to National Instrument 41-101 General Prospectus Requirements and Companion Policy 41-101CP to National Instrument 41-101 General Prospectus Requirements

|

|

|

|

||

|

|

Schedule B-1

|

National Instrument 41-101 General Prospectus Requirements

|

|

|

Schedule B-2

|

Form 41-101F1 Information Required in a Prospectus

|

|

|

Schedule B-3

|

Form 41-101F2 Information Required in an Investment Fund Prospectus

|

|

|

Schedule B-4

|

Companion Policy 41-101CP to National Instrument 41-101 General Prospectus Requirements

|

|

|

||

|

Appendix C

|

Proposed Amendments to National Instrument 44-101 Short Form Prospectus Distributions and Companion Policy 44-101CP to National Instrument 44-101 Short Form Prospectus Distributions

|

|

|

|

||

|

|

Schedule C-1

|

Proposed Amendments to National Instrument 44-101 Short Form Prospectus Distributions

|

|

|

Schedule C-2

|

Proposed Amendments to Companion Policy 44-101CP to National Instrument 44-101 Short Form Prospectus Distributions

|

|

|

||

|

Appendix D

|

Blackline Showing Proposed Changes to National Instrument 44-101 Short Form Prospectus Distributions and Companion Policy 44-101CP to National Instrument 44-101 Short Form Prospectus Distributions

|

|

|

|

||

|

|

Schedule D-1

|

National Instrument 44-101 Short Form Prospectus Distributions

|

|

|

Schedule D-2

|

Form 44-101F1 Short Form Prospectus

|

|

|

Schedule D-3

|

Companion Policy 44-101CP to National Instrument 44-101 Short Form Prospectus Distributions

|

|

|

||

|

Appendix E

|

Proposed Amendments to National Instrument 44-102 Shelf Distributions and Companion Policy 44-102CP to National Instrument 44-102 Shelf Distributions

|

|

|

|

||

|

|

Schedule E-1

|

Proposed Amendments to National Instrument 44-102 Shelf Distributions

|

|

|

Schedule E-2

|

Proposed Amendments to Companion Policy 44-102CP to National Instrument 44-102 Shelf Distributions

|

|

|

||

|

Appendix F

|

Proposed Amendments to National Instrument 81-101 Mutual Fund Prospectus Disclosure

|

|

|

|

||

|

Appendix G

|

Blackline Showing Proposed Changes to National Instrument 81-101 Mutual Fund Prospectus Disclosure

|

|

|

|

||

|

|

Schedule G-1

|

National Instrument 81-101 Mutual Fund Prospectus Disclosure

|

|

|

Schedule G-2

|

Form 81-101F2 Contents of Annual Information Form

|

|

|

||

|

Appendix H

|

Proposed Amendments to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards and Companion Policy 52-107CP to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standard

|

|

|

|

||

|

|

Schedule H-1

|

Proposed Amendments to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

|

|

|

Schedule H-2

|

Companion Policy 52-107P to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

|

|

|

||

|

Appendix I

|

Blackline Showing Proposed Changes to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards and Companion Policy 52-107CP to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

|

|

|

|

||

|

|

Schedule I-1

|

National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

|

|

|

Schedule I-2

|

Companion Policy 52-107CP Companion Policy to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

|

|

|

||

|

Appendix J

|

Proposed Amendments to National Instrument 51-102 Continuous Disclosure Obligations

|

|

|

|

||

|

Appendix K

|

Proposed Amendments to National Instrument 13-101 System for Electronic Document and Analysis Retrieval

|

|

|

|

||

|

Appendix L

|

Information required by local securities legislation

|

|

Schedule A-1 -- Proposed Amendments to National Instrument 41-101 General Prospectus Requirements

APPENDIX A

SCHEDULE A-1

AMENDMENTS TO

NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS

1. National Instrument 41-101 General Prospectus Requirements is amended by this Instrument.

2. Section 1.1 is amended by

(a) in the definition of "executive officer",

(i) adding "or an investment fund manager," after "means, for an issuer",

(ii) inserting "(a.1) a chief executive officer or chief financial officer" after "(a) a chair, vice-chair or president,", and

(iii) in paragraph (c), adding "or investment fund manager" after "issuer".

(b) after the definition of "over-allotment option", adding the following definition:

""personal information form" means in respect of an individual,

(a) a completed Schedule 1 of Appendix A, or

(b) A TSX/TSXV personal information form submitted by an individual to the Toronto Stock Exchange or to the TSX Venture Exchange to which is attached a completed certificate and consent in the form set out in Schedule 1 -- Part B of Appendix A, if the personal information in the form continues to be correct at the time that the certificate and consent is executed by the individual;", and

(c) after the definition of "transition year", adding the following definition:

""TSX/TSXV personal information form" means a completed personal information form of an individual in compliance with the requirements of Form 4 for the Toronto Stock Exchange or Form 2A for the TSX Venture Exchange, as applicable, each as amended from time to time;".

3. Subsection 2.3(1) is amended by

(a) replacing "a final prospectus" with "an amendment to a preliminary prospectus", and

(b) deleting "that relates to the final prospectus".

4. Section 2.3 is amended by adding the following subsections after subsection 2.3(1):

"(1.1) An issuer must not file a final prospectus more than 90 days after the date of the receipt for the preliminary prospectus or an amendment to the preliminary prospectus which relate to the final prospectus.

(1.2) If an issuer files an amendment pursuant to subsection (1), the total period of time permitted to file the final prospectus under subsection (1.1) must not exceed 180 days from the date of the receipt of the preliminary prospectus.".

5. Part 5 is amended by adding the following section after section 5.10:

"Certificate of principal distributor

5.10.1(1) If the issuer is an investment fund that has a principal distributor, a prospectus must contain a certificate, in the applicable issuer certificate form, signed by the principal distributor.

(2) If the principal distributor is a company, the certificate must be signed by any officer or director of the principal distributor duly authorized to sign."

6. Section 9.1 is amended by renumbering it as subsection 9.1(1).

7. Subparagraph 9.1(1)(b)(ii) is amended by

(a) replacing "Appendix A" with "personal information form", and

(b) replacing "for;" with "for".

8. Clause 9.1(1)(b)(ii)(D) is amended by replacing "for whom the issuer has not previously filed or delivered," with "; and".

9. Clause 9.1(1)(b)(ii)(E) is deleted.

10. Clause 9.1(1)(b)(ii)(F) is deleted.

11. Clause 9.1(1)(b)(ii)(G) is deleted.

12. Section 9.1 is amended by adding the following subsection after subsection (1):

"(2) Despite subparagraph 9.1(1)(b)(ii), an issuer is not required to file a personal information form for an individual if all of the following are satisfied:

(a) a personal information form of the individual has been executed by the individual within three years preceding the date of the filing of the preliminary or pro forma long form prospectus;

(b) the personal information form was delivered to the regulator or, in Québec, the securities regulatory authority

(i) by an issuer on behalf of the individual on or after [insert effective date of amendments]; or

(ii) by the issuer on behalf of the individual after March 16, 2008 but before [insert effective date of amendments] in the form set out in Appendix A to NI 41-101 in effect during this period;

(c) the information concerning the individual contained in the responses to

(i) questions 6 through 10 of the personal information form referenced in subparagraph (b)(i) remains correct as at the date of the certificate referred to in paragraph (d); or

(ii) questions 4(B) or (C) and questions 6 through 9 of the personal information form referenced in subparagraph (b)(ii) remains correct as at the date of the certificate referred to in paragraph (d);

(d) the issuer delivers to the regulator or, in Québec, the securities regulatory authority, concurrently with the filing of the preliminary or pro forma long form prospectus, a certificate of the issuer in the form set out in Schedule 4 of Appendix A stating that the individual has provided the issuer with confirmation in respect of the requirement contained in paragraph (c);

(e) the certificate referenced in paragraph (d) is dated no earlier than 30 days before the filing of the preliminary or pro forma long form prospectus.".

13. Subparagraph 9.2(a)(vii) is amended by

(a) deleting "and" in clause (A),

(b) adding the following clause after clause (A)

"(A.1) each director of the issuer, and", and

(c) replacing "each person or company required to sign a certificate under Part 5" in clause (B) with "any other person or company that provides or signs a certificate under Part 5".

14. Subparagraph 9.2(a)(xii) is amended by

(a) after "Undertaking to File",replacing "Documents and Material Contracts" with "Agreements, Contracts and Material Contracts",

(b) replacing "a document referred to in subparagraph (ii), (iii) or (iv)" with "an agreement, contract or declaration of trust under subparagraph (ii) or (iv) or a material contract under subparagraph (iii)",

(c) deleting "or become effective" wherever it appears,

(d) replacing "to file the document" with "to file the agreement, contract, declaration of trust or material contract", and

(e) replacing "within seven days after the completion of the distribution; and" with "no later than seven days after execution of the agreement, contract, declaration of trust or material contract;".

15. Paragraph 9.2(a) is amended by adding the following subparagraph after subparagraph 9.2(a)(xii):

"(xii.1) Undertaking to File Unexecuted Documents - if a document referred to in subparagraph (ii) will not be executed in order to become effective and has not become effective before the filing of the final long form prospectus, but will become effective on or before the completion of the distribution, the issuer must file with the securities regulatory authority, no later than the time of filing of the final long form prospectus, an undertaking of the issuer to the securities regulatory authority to file the document promptly and in any event no later than seven days after the document becomes effective; and"

16. Subsection 10.1(1) is amended by

(a) replacing "An issuer" with "Subject to subsection (1.1), an issuer".

(b) adding a period at the end of paragraph (c), and

(c) deleting the following:

"if that person or company is named in a prospectus or an amendment to a prospectus, directly or, if applicable, in a document incorporated by reference,

(d) as having prepared or certified any part of the prospectus or the amendment,

(e) as having opined on financial statements from which selected information included in the prospectus has been derived and which audit opinion is referred to in the prospectus directly or in a document incorporated by reference, or

(f) as having prepared or certified a report, valuation, statement or opinion referred to in the prospectus or the amendment, directly or in a document incorporated by reference."

17. Section 10.1 is amended by adding the following subsection after subsection (1):

"(1.1) Subsection (1) only applies if the person or company is named in a prospectus or an amendment to a prospectus, directly or, if applicable, in a document incorporated by reference,

(a) as having prepared or certified any part of the prospectus or the amendment,

(b) as having opined on financial statements from which selected information included in the prospectus has been derived and which audit opinion is referred to in the prospectus directly or in a document incorporated by reference, or

(c) as having prepared or certified a report, valuation, statement or opinion referred to in the prospectus or the amendment, directly or in a document incorporated by reference.".

18. Section 11.2 is amended by replacing "No" with "Except as required under section 11.3, no".

19. Paragraph 11.2(b) is amended by adding "on an as-if converted basis" after "offering".

20. Section 13.3 is amended by

(a) in paragraph (d), adding "fundamental" before "investment objective(s)", and

(b) adding the following paragraph after paragraph (h):

"(i) whether the security is or will be a qualified investment for a registered retirement savings plan, registered retirement income fund, registered education savings plan or tax free savings account or qualifies or will qualify the holder for special tax treatment.".

21. Section 14.5 is amended by

(a) in subsection 14.5(1), replacing "agreements between the investment fund and the custodian or the custodian and the sub-custodian" with "custodian agreements and sub-custodian agreements",

(b) in subparagraph 14.5(1)(g), striking out "," after "sub-custodian", and

(c) in subsection 14.5(3), replacing "An agreement between an investment fund and a custodian or a custodian and a sub-custodian respecting the portfolio assets" with "A custodian agreement or sub-custodian agreement concerning the portfolio assets of an investment fund".

22. Paragraph 19.3(2)(a) is amended by adding "pro forma or" after "the filing of the" wherever it occurs.

23. Appendix A is amended by repealing the following:

"PERSONAL INFORMATION FORM AND AUTHORIZATION OF

INDIRECT COLLECTION, USE AND DISCLOSURE OF

PERSONAL INFORMATION

In connection with an issuer's (the "Issuer") filing of a prospectus, the attached Schedule 1 contains information (the "Information") concerning every individual for whom the Issuer is required to provide the Information under Part 9 of this Instrument or Part 4 of NI 44-101. The Issuer is required by provincial and territorial securities legislation to deliver the Information to the regulators listed in Schedule 3.

The Issuer confirms that each individual who has completed a Schedule 1:

(a) has been notified by the Issuer

(i) of the Issuer's delivery to the regulator of the Information in Schedule 1 pertaining to that individual,

(ii) that the Information is being collected indirectly by the regulator under the authority granted to it by provincial and territorial securities legislation or provincial legislation relating to documents held by public bodies and the protection of personal information,

(iii) that the Information collected from each director and executive officer of the investment fund manager may be used in connection with the prospectus filing of the Issuer and the prospectus filing of any other issuer managed by the investment fund manager,

(iv) that the Information is being collected and used for the purpose of enabling the regulator to administer and enforce provincial and territorial securities legislation, including those obligations that require or permit the regulator to refuse to issue a receipt for a prospectus if it appears to the regulator that the past conduct of management, an investment fund manager or promoter of the Issuer affords reasonable grounds for belief that the business of the Issuer will not be conducted with integrity and in the best interests of its securityholders, and

(v) of the contact, business address and business telephone number of the regulator in the local jurisdiction as set out in the attached Schedule 3, who can answer questions about the regulator's indirect collection of the Information;

(b) has read and understands the Personal Information Collection Policy attached hereto as Schedule 2; and

(c) has, by signing the certificate and consent in Schedule 1, authorized the indirect collection, use and disclosure of the Information by the regulator as described in Schedule 2.

Date: ________________________________________Name of IssuerPer: ________________________________________Name____________________Official Capacity(Please print the name of the person signing on behalf of the issuer)".

24. Schedule 1 of Appendix A is amended by renumbering it as Schedule 1, Part A.

25. Part A of Schedule 1 of Appendix A is amended by

(a) deleting the following from the end of Part A:

- - - - - - - - - - - - - - - - - - - -

"CERTIFICATE AND CONSENT

- - - - - - - - - - - - - - - - - - - -

I, ____________________ (Please Print -- Name of Individual) hereby certify that:

(a) I have read and understood the questions, cautions, acknowledgement and consent in this Form, and the answers I have given to the questions in this Form and in any attachments to it are true and correct, except where stated to be to the best of my knowledge, in which case I believe the answers to be true;

(b) I have read and understand the Personal Information Collection Policy attached hereto as Schedule 2 (the "Personal Information Collection Policy");

(c) I consent to the collection, use and disclosure of the information in this Form and to the collection, use and disclosure of further personal information in accordance with the Personal Information Collection Policy; and

(d) I understand that I am providing this Form to a regulator listed in Schedule 3 attached hereto and I am under the jurisdiction of the regulator to which I submit this Form, and it is a breach of securities legislation to provide false or misleading information to the regulator.

____________________Date [within 30 days of the date of the preliminary prospectus]____________________Signature of Person Completing this Form", and(b) by replacing in the paragraph preceding the General Instructions of Part A of Schedule 1 of Appendix A

". Where an individual has submitted a personal information form (an "Exchange Form") to the Toronto Stock Exchange or the TSX Venture Exchange and the information has not changed, the Exchange Form may be delivered in lieu of this Form; provided that the certificate and consent of this Form is completed and attached to the Exchange Form."

with "or Part 2 of National Instrument 81-101 Mutual Fund Prospectus Disclosure.".

26. Part A of Schedule 1 of Appendix A, General Instructions, is amended by

(a) in "All Questions"

(i) adding "will not be accepted" after ""Not Applicable"", and

(ii) replacing "2B(iii) and 5 will not be accepted" with the following:

"2(iii) and (v) and 5.

For the purposes of answering the questions in this Form, the term "issuer" includes an investment fund manager.",

(b) in the title Questions 6 to 9, replacing "9" with "10", and

(c) in Questions 6 to 10,

(i) replacing "check" with "place a checkmark", and

(ii) replacing "questions 6 to 9" with "questions 6 to 10".

27. Part A of Schedule 1 of Appendix A, Definitions, is amended by

(a) in paragraph (b) of the definition of "Offence",adding "Canadian or foreign" before "jurisdiction",

(b) in paragraph (d)of the definition of "Offence", adding "other" before "foreign",

(c) in the NOTE to the definition of "Offence",

(i) replacing "and it has not been revoked" with "for an Offence that relates to fraud (including any type of fraudulent activity), misappropriation of money or other property, theft, forgery, falsification of books or documents or similar Offences,", and

(ii) replacing "offence" with "Offence",

(d) in paragraph (a) of the definition of "Proceedings",adding "which is currently" after "inquiry",

(e) in paragraph (d) of the definition of "Proceedings"

(i) replacing "self-regulatory organization" wherever it occurs with "self-regulatory entity",

(ii) replacing "and their representatives" with "(including where applicable, issuers listed on a stock exchange) and individuals associated with those members and issuers",

(iii) replacing "by-laws or rules" with "by-laws, rules or policies", and

(iv) replacing "for a hearing" with "to be heard",

(f) in the definition of "securities regulatory authority or (SRA)"

(i) deleting the brackets surrounding "(SRA)",

(ii) replacing "in any jurisdiction or in any foreign jurisdiction" with "in any Canadian or foreign jurisdiction", and

(iii) replacing "or professional organization" with "entity",

(g) in the definition of "securities regulatory or professional organization",replacing "or professional organization" with ""entity" or "SRE"",

(h) in paragraph (a) of the definition of "securities regulatory entity or "SRE"",adding "derivatives," after "stock,",

(i) in paragraph (e) of the definition of "securities regulatory entity or "SRE",

(i) replacing "self-regulatory entity" with "self-regulatory organization",

(ii) adding "policies," after "rules,", and

(iii) replacing "a self-regulatory or professional organization" with "an SRE".

28. Section 1.A. of Part A of Schedule 1 of Appendix A is amended by replacing "MIDDLE NAME(S) (If none, please state)" with "FULL MIDDLE NAME(S) (No initials. If none, please state)".

29. Section 1.E. of Part A of Schedule 1of Appendix A is amended by

(a) adding an asterisk immediately after "E-MAIL", and

(b) adding "*Please provide an email address that the regulator may use to contact you regarding this PIF. This email address may be used to exchange personal information relating to you." below the last information field.

30. Section 1.F. of Part A of Schedule 1 of Appendix A is amended by replacing "correctly identify" with "recall".

31. Section 2.A. of Part A of Schedule 1 of Appendix A is amended by

(a) deleting the title "A. CANADIAN CITIZENSHIP",

(b) in subparagraph(i), replacing "Citizen" with "citizen", and

(c) after subparagraph (iii), adding the following:

"(iv) Do you hold citizenship in any country other than Canada?

(v) If "Yes" to Question 2(iv), the name of the country(ies):".

32. Section 2.B. of Part A of Schedule 1 of Appendix A is repealed.

33. The introduction of section 3 of Part A of Schedule 1 of Appendix A is amended by

(a) adding "complete" before "employment history",

(b) replacing "10" with "5", and

(c) after the last sentence, adding "If you were unemployed during this period of time, please state this and identify the period of unemployment.".

34. Section 4 of Part A of Schedule 1 of Appendix A is amended by replacing

"4. POSITIONS WITH OTHER ISSUERS

YES

NO

A.

While you were a director, officer or insider of an issuer, did any exchange or self-regulatory organization ever refuse approval for listing or quotation of that issuer (including a listing resulting from a qualifying transaction, reverse takeover, backdoor listing or change of business)? If yes, attach full particulars.

_____

_____

B.

Has your employment in a sales, investment or advisory capacity with any firm or company engaged in the sale of real estate, insurance or mutual funds ever been terminated for cause?

_____

_____

C.

Has a firm or company registered under the securities laws of any jurisdiction or of any foreign jurisdiction as a securities dealer, broker, investment advisor or underwriter, suspended or terminated your employment for cause?

_____

_____

D.

Are you or have you during the last 10 years ever been a director, officer, promoter, insider or control person for any reporting issuer?

_____

_____

with the following:

"4. INVOLVEMENT WITH ISSUERS

YES

NO

A.

Are you or have you during the last 10 years ever been a director, officer, promoter, insider or control person for any reporting issuer?

_____

_____

35. Section 5.A. of Part A of Schedule 1 of Appendix A is amended by replacing

"A.

PROFESSIONAL DESIGNATION(S) -- Provide any professional designation held and professional associations to which you belong. For example, Barrister & Solicitor, C.A., C.M.A., C.G.A., P.Eng., P.Geol., and CFA, etc. and indicate which organization and the date the designations were granted.

PROFESSIONAL DESIGNATION And MEMBERSHIP NUMBER

GRANTOR OF DESIGNATION And JURISDICTION OR FOREIGN JURISDICTION

DATE GRANTED

ACTIVE?

MM

DD

YY

YES

NO"

_______________

_______________

___

___

___

___

___

_______________

_______________

___

___

___

___

___

_______________

_______________

___

___

___

___

___

with the following:

"A.

PROFESSIONAL DESIGNATION(S) -- Identify any professional designation held and professional associations to which you belong, for example, Barrister & Solicitor, C.A., C.M.A., C.G.A., P.Eng., P.Geol., CFA, etc. and indicate which organization and the date the designations were granted.

PROFESSIONAL DESIGNATION And MEMBERSHIP NUMBER

GRANTOR OF DESIGNATION And CANADIAN OR FOREIGN JURISDICTION

DATE GRANTED

MM

YY

____________________

____________________

___

_____

____________________

____________________

___

_____

____________________

____________________

___

_____

Describe the current status of any designation and/or association (e.g. active, retired, non-practicing, suspended)".

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

36. Section 6 of Part A of Schedule 1 of Appendix A is amended by replacing

"6. OFFENCES - If you answer "YES" to any item in Question 6, you must provide complete details in an attachment.

YES

NO

A.

Have you ever pleaded guilty to or been found guilty of an offence?

___

___

B.

Are you the subject of any current charge, indictment or proceeding for an offence?

___

___

C.

To the best of your knowledge, are you or have you ever been a director, officer, promoter, insider, or control person of an issuer, in any jurisdiction or in any foreign jurisdiction, at the time of events, where the issuer:

___

___

(i)

has ever pleaded guilty to or been found guilty of an offence?

___

___

(ii)

is the subject of any current charge, indictment or proceeding for an offence?"

___

___

with the following:

"6. OFFENCES - If you answer "YES" to any item in Question 6, you must provide complete details in an attachment. If you have received a pardon under the Criminal Records Act (Canada) for an Offence that relates to fraud (including any type of fraudulent activity), misappropriation of money or other property, theft, forgery, falsification of books or documents or similar Offences, you must disclose the pardoned Offence in this Form.

YES

NO

A.

Have you ever, in any Canadian or foreign jurisdiction, pled guilty to or been found guilty of an Offence?

___

___

B.

Are you the subject of any current charge, indictment or proceeding for an Offence, in any Canadian or foreign jurisdiction?

___

___

C.

To the best of your knowledge, are you currently or have you ever been a director, officer, promoter, insider or control person of an issuer, in any Canadian or foreign jurisdiction, at the time of events, where the issuer:

___

___

(i)

pled guilty to or was found guilty of an Offence?

___

___

(ii)

is now the subject of any charge, indictment or proceeding for an Offence?".

___

___

37. The introduction of section 7 of Part A of Schedule 1 of Appendix A is amended by adding "You must answer "YES" or "NO" for EACH of (A), (B) and (C) below." after the last sentence.

38. Section 7.A. of Part A of Schedule 1 of Appendix A is amended by replacing "jurisdiction or in any foreign jurisdiction" with "Canadian or foreign jurisdiction".

39. Section 7.C. of Part A of Schedule 1 of Appendix A is amended by

(a) adding "currently" after "are you", and

(b) replacing "jurisdiction or in any foreign jurisdiction" with "Canadian or foreign jurisdiction".

40. Section 8.A. of Part A of Schedule 1 of Appendix A is amended by replacing

YES

NO

"A.

CURRENT PROCEEDINGS BY SECURITIES REGULATORY AUTHORITY OR SELF REGULATORY OR PROFESSIONAL ORGANIZATION. Are you now, in any jurisdiction or in any foreign jurisdiction, the subject of:

___

___

(i)

a notice of hearing or similar notice issued by a SRA?

___

___

(ii)

a proceeding or to your knowledge, under investigation, by an exchange or other self regulatory or professional organization?

___

___

(iii)

settlement discussions or negotiations for settlement of any nature or kind whatsoever with a SRA or any self regulatory or professional organization?"

___

___

with the following:

YES

NO

"A.

CURRENT PROCEEDINGS BY SECURITIES REGULATORY AUTHORITY OR SELF REGULATORY ENTITY. Are you now, in any Canadian or foreign jurisdiction, the subject of:

___

___

(i)

a notice of hearing or similar notice issued by an SRA or SRE?

___

___

(ii)

a proceeding or to your knowledge, under investigation, by an SRA or SRE?

___

___

(iii)

settlement discussions or negotiations for settlement of any nature or kind whatsoever with an SRA or SRE?".

___

___

41. Section 8.B. of Part A of Schedule 1 of Appendix A is amended by replacing

YES

NO

"B.

PRIOR PROCEEDINGS BY SECURITIES REGULATORY AUTHORITY OR SELF REGULATORY OR PROFESSIONAL ORGANIZATION. Have you ever:

___

___

(i)

been reprimanded, suspended, fined, been the subject of an administrative penalty, or otherwise been the subject of any disciplinary proceedings of any kind whatsoever, in any jurisdiction or in any foreign jurisdiction, by a SRA or self regulatory or professional organization?

___

___

(ii)

had a registration or licence for the trading of securities, exchange or commodity futures contracts, real estate, insurance or mutual fund products cancelled, refused, restricted or suspended?

___

___

(iii)

been prohibited or disqualified under securities, corporate or any other legislation from acting as a director or officer of a reporting issuer?

___

___

(iv)

had a cease trading or similar order issued against you or an order issued against you that denied you the right to use any statutory prospectus or registration exemption?

___

___

(v)

had any other proceeding of any nature or kind taken against you?"

___

___

with the following:

YES

NO

"B.

PRIOR PROCEEDINGS BY SECURITIES REGULATORY AUTHORITY OR SELF REGULATORY ENTITY. Have you ever:

___

___

(i)

been reprimanded, suspended, fined, been the subject of an administrative penalty, or been the subject of any proceedings of any kind whatsoever, in any Canadian or foreign jurisdiction, by an SRA or SRE?

___

___

(ii)

had a registration or licence for the trading of securities, exchange or commodity futures contracts, real estate, insurance or mutual fund products cancelled, refused, restricted or suspended, by an SRA or SRE?

___

___

(iii)

been prohibited or disqualified by an SRA or SRE under securities, corporate or any other legislation from acting as a director or officer of a reporting issuer or been prohibited or restricted by an SRA or SRE from acting as a director, officer or employee of, or an agent or consultant to, a reporting issuer?

___

___

(iv)

had a cease trading or similar order issued against you or an order issued against you by an SRA or SRE that denied you the right to use any statutory prospectus or registration exemption?

___

___

(v)

had any other proceeding of any nature or kind taken against you by an SRA or SRE?".

___

___

42. Section 8.C. of Part A of Schedule 1 of Appendix A is amended by

(a) replacing "a" with "an" before "SRA",

(b) replacing "self regulatory or professional organization" with "SRE" wherever it appears,

(c) replacing "any jurisdiction or in any foreign jurisdiction" with "any Canadian or foreign jurisdiction",

(d) replacing "a jurisdiction or in a foreign jurisdiction" with "a Canadian or foreign jurisdiction", and

(e) adding ", by-laws or policies" after "rules".

43. Section 8.D. of Part A of Schedule 1 of Appendix A is amended by

(a) replacing "any jurisdiction or in any foreign jurisdiction" with "any Canadian or foreign jurisdiction", and

(b) replacing "self regulatory or professional organization" with "self regulatory entity".

44. Subparagraph 8.D.(v) of Part A of Schedule 1 of Appendix A is amended by replacing

"(v) taken any other proceeding of any nature or kind against the issuer, including a trading halt, suspension or delisting of the issuer (other than in the normal course for proper dissemination of information, pursuant to a reverse takeover, backdoor listing or similar transaction)?"

with the following:

"(v) commenced any other proceeding of any nature or kind against the issuer, including a trading halt, suspension or delisting of the issuer, in connection with an alleged or actual contravention of an SRA's or SRE's rules, regulations, policies or other requirements, but excluding halts imposed (i) in the normal course for proper dissemination of information, or (ii) pursuant to a business combination, reverse take-over or similar transaction involving the issuer that is regulated by an SRE or SRA, including a Qualifying Transaction, Reverse Takeover or Change of Business involving the issuer (as those terms are defined in the TSX Venture Corporate Finance Manual as amended)?".

45. Subparagraph 8.D.(vi) of Part A of Schedule 1 of Appendix A is amended by

(a) deleting "involved in", and

(b) replacing "in a jurisdiction or in a foreign jurisdiction or a self regulatory or professional organization's rules" with "or the rules, by-laws or policies of an SRE".

46. Section 9.A. of Part A of Schedule 1 of Appendix A is amended by replacing "any jurisdiction or in any foreign jurisdiction" with "any Canadian or foreign jurisdiction".

47. Subparagraph 9.A.(i) of Part A of Schedule 1 of Appendix A is amended by adding a comma after "changes".

48. Subparagraph 9.A.(ii) of Part A of Schedule 1 of Appendix A is amended by

(a) replacing "for" with "of" after "an issuer",

(b) deleting the comma after "control person", and