Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

CSA Staff Notice 51-346 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2016

CSA Staff Notice 51-346 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2016

CSA Staff Notice 51-346 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2016

July 18, 2016

Introduction

This notice contains the results of the reviews conducted by the Canadian Securities Administrators (CSA) within the scope of their Continuous Disclosure Review Program (CD Review Program). The goal of the program is to improve the completeness, quality and timeliness of continuous disclosure provided by reporting issuers{1} (issuers) in Canada. This program was established to assess the compliance of continuous disclosure (CD) documents and to help issuers understand and comply with their obligations under the CD rules so that investors receive high quality disclosure.

In this notice, we summarize the results of the CD Review Program for the fiscal year ended March 31, 2016 (fiscal 2016). Appendix A -- Financial Statement, MD&A and Other Regulatory Deficiencies (Appendix A) includes information about areas where common deficiencies were noted, with examples in certain instances, to help issuers address these deficiencies and to illustrate best practices.

For further details on the CD Review Program, see CSA Staff Notice 51-312 (revised) Harmonized Continuous Disclosure Review Program.

Results for Fiscal 2016

Issuers selected for a CD review (full or issue oriented review (IOR)) are identified using a risk-based and outcomes-focused approach using both qualitative and quantitative criteria. IORs may be based on a specific accounting, legal or regulatory issue, an emerging issue, implementation of recent rules or on matters where we believe there may be a heightened risk of investor harm. A review may also stem from monitoring of our issuers through news releases, media articles, complaints and other sources.

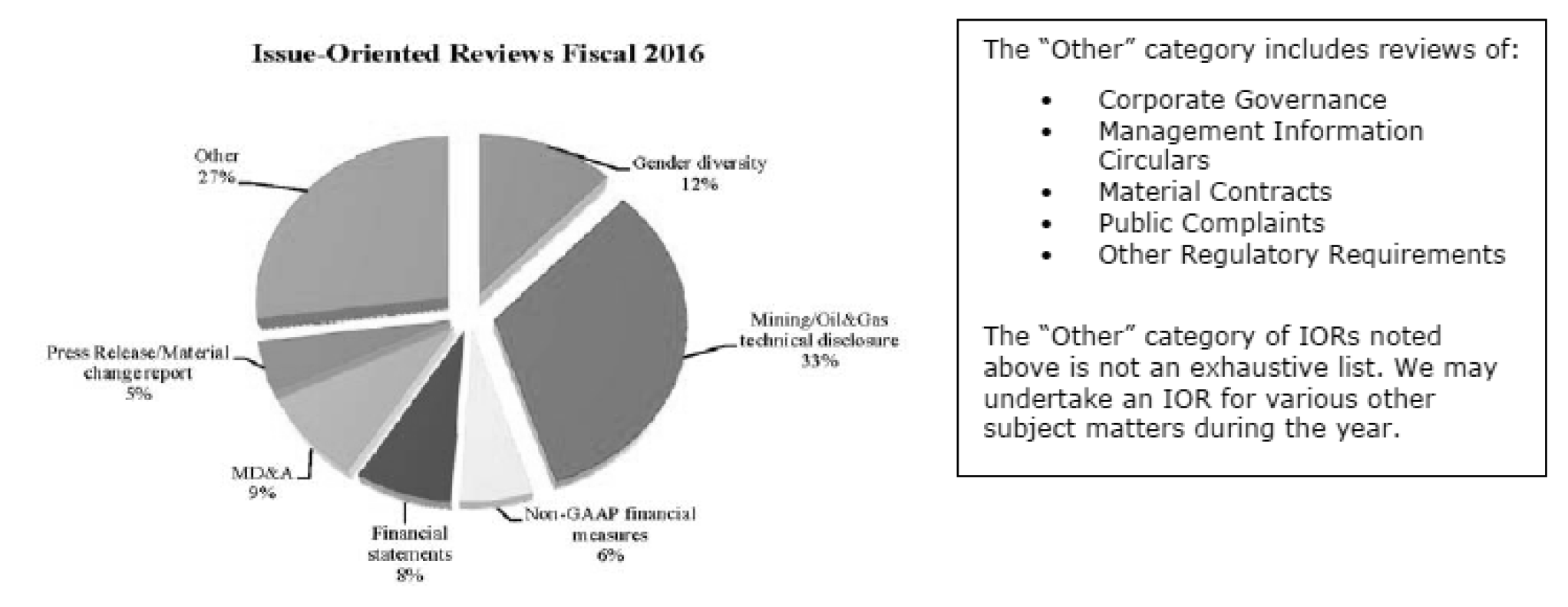

During fiscal 2016, a total of 902 CD reviews (fiscal 2015 -- 1,058 CD reviews) were conducted with IORs consisting of 69% of the total (fiscal 2015 -- 74%). The nature of an IOR will impact the time spent and outcome obtained from the review. The following are some of the IORs conducted by one or more jurisdictions:

CD Outcomes for Fiscal 2016

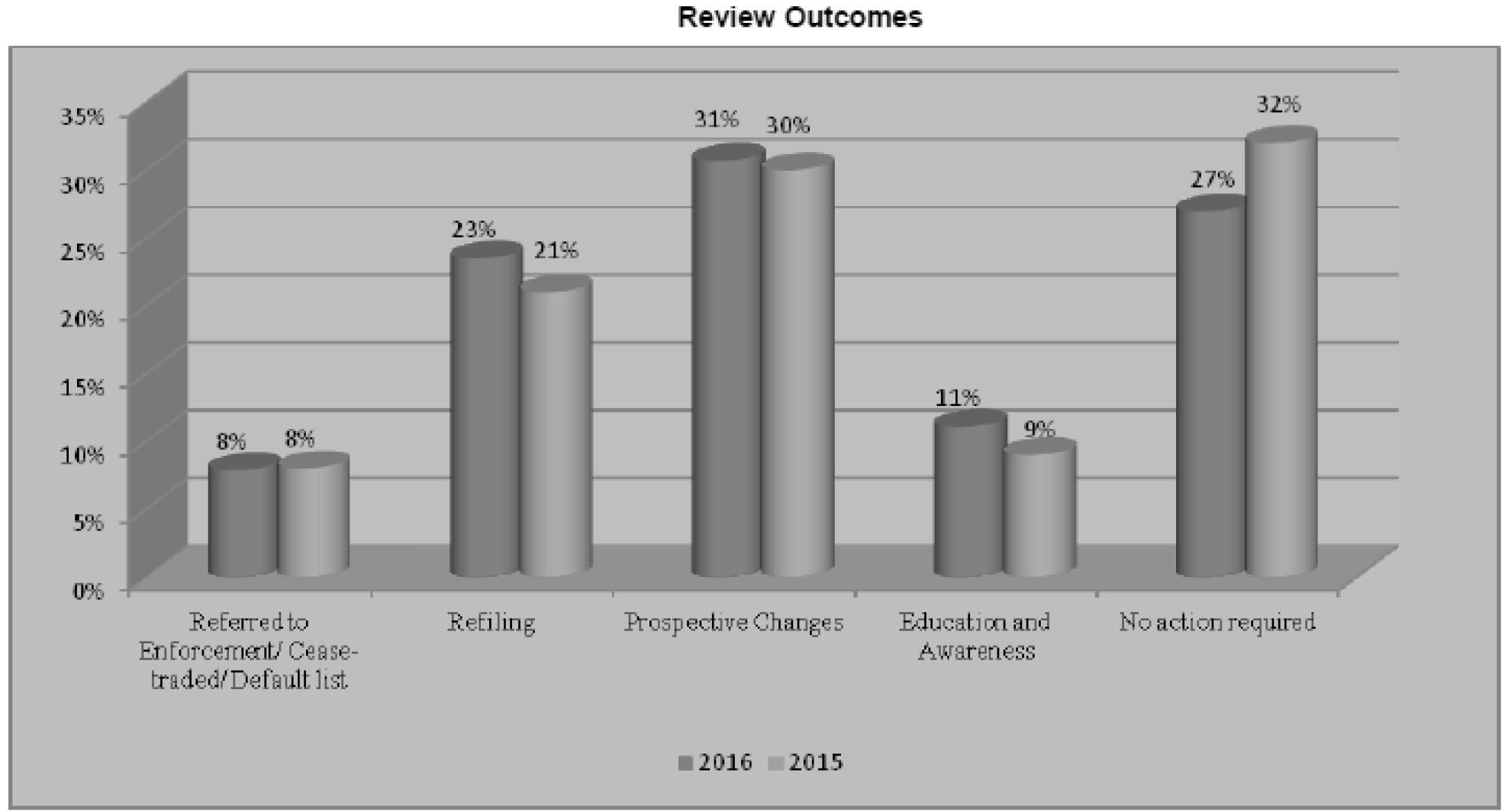

In fiscal 2016, 62% (fiscal 2015 -- 59%) of our review outcomes required issuers to take action to improve and/or amend their disclosure or resulted in the issuer being referred to enforcement, cease traded or placed on the default list.

We classify the outcomes of the full reviews and IORs into five categories as described in Appendix B -- Categories of Outcomes. Some CD reviews may generate more than one category of outcome. For example, an issuer may have been required to refile certain documents and also make certain changes on a prospective basis.

Where possible, we have attempted to identify trends we observed when comparing fiscal 2016 to prior years. However, given our risk-based approach noted above, the outcomes on a year to year basis may vary and cannot be interpreted as an emerging trend. The issues as well as the issuers reviewed each year might be different. In fiscal 2016 we continued to see substantive outcomes being obtained as a result of our reviews as noted in the categories of refilings and referred to enforcement/default list/cease traded.

Refilings are significant events that should be clearly and broadly disclosed to the market in a timely manner in accordance with Item 11.5 of NI 51-102.

The refilings of issuers' CD records included some of the following areas:

• Financial Statements: compliance with recognition, measurement and disclosure requirements in International Financial Reporting Standards (IFRS), which included, but was not limited to, impairment, accounting for acquisitions, revenue, going concern disclosures, and significant judgements.

• Management's Discussion and Analysis (MD&A): compliance with Form 51-102F1 of NI 51-102 (Form 51-102F1), which included, but was not limited to, non-GAAP financial measures, discussion of operations, liquidity, related party transactions and forward looking information.

• Other Regulatory Requirements: compliance with other regulatory matters, which included, but were not limited to, mining technical reports, investor presentations, gender diversity disclosure, business acquisition reports (BARs), executive compensation disclosure, and filing of previously unfiled documents, such as material contracts, clarifying news releases or material change reports to address concerns around unbalanced or insufficient disclosure.

Results by Jurisdiction

All CSA jurisdictions participate in the CD review program and some local jurisdictions may publish staff notices and reports communicating results and findings of the CD reviews conducted in their jurisdictions. Refer to the individual regulator's website for copies of these notices and reports:

• www.bcsc.bc.ca

• www.albertasecurities.com

• www.osc.gov.on.ca

• www.lautorite.qc.ca

{1} In this notice "issuers" means those reporting issuers contemplated in National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102).

APPENDIX A

FINANCIAL STATEMENT, MD&A AND OTHER REGULATORY DEFICIENCIES

Our CD reviews identified several financial statement, MD&A and other regulatory deficiencies that resulted in issuers enhancing their disclosure and/or refiling their CD documents. To help issuers better understand and comply with their CD obligations, we present the key observations from our reviews in both a hot buttons chart as well as detailed discussions. The hot buttons section includes observations along with considerations for issuers including the relevant authoritative guidance. The discussion that follows each chart includes examples of deficient disclosure contrasted against more robust entity-specific disclosure or a more in-depth explanation of the matters we observed.

Issuers must ensure that their CD record complies with all relevant securities legislation. The volume of disclosure filed does not necessarily equate to full compliance.

The following observations are provided for illustrative purposes only. This is not an exhaustive list and does not represent all the requirements that could apply to a particular issuer's situation.

FINANCIAL STATEMENT DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

FINANCIAL STATEMENTS |

||||

|

|

||||

|

Market Risk -- Sensitivity Analysis |

• |

Some issuers present sensitivity analysis that is not reflective of the reasonably possible changes in the relevant risk at the date of the financial statements and/or is not meaningful in light of the current economic environment. |

• |

Issuers must disclose sensitivity analysis for each type of market risk (currency risk, interest rate risk, and other price risk) to which the entity is exposed at the end of the reporting period, showing how profit or loss and equity would have been affected by changes in the relevant risk variable that were reasonably possible at that date. |

|

|

|

|

• |

An appropriate percentage change in the relevant risk should be used. For example, presenting a 1% change instead of a more reasonably higher percentage would not provide investors with meaningful information. |

|

|

|

|

• |

Issuers should consider disclosing whether the impact of the sensitivity analysis yields a proportional or non-proportional result. This information will provide investors with an understanding of the impact of the risk on the issuer should there be a significant downturn. |

|

|

||||

|

|

|

|

Reference: Paragraph 40 of IFRS 7 -- Financial Instruments: Disclosure |

|

|

|

||||

|

Contingent Consideration in Business Combinations |

• |

Some issuers fail to identify and account for contingent consideration and inappropriately account for settlements as a measurement period adjustment. |

• |

Issuers must recognize contingent consideration at fair value as of the acquisition date. Accounting for a change in fair value subsequent to the acquisition date depends on whether the change is a measurement period adjustment. |

|

|

||||

|

|

|

|

• |

Initial accounting for contingent consideration has an impact on the financial statements for the current period and for the subsequent periods. |

|

|

||||

|

|

|

|

Reference: Paragraphs 39, 40, 45-49, 58 of IFRS 3 Business Combinations (IFRS 3) |

|

|

|

||||

|

Goodwill and Intangible Assets Recognized in Business Combinations |

• |

We continue to see issuers that allocate the entire purchase price to one intangible asset. However, the disclosure indicates the presence of other identifiable intangible assets or goodwill. |

• |

Issuers must separately recognize the identifiable intangible assets acquired in a business combination. |

|

|

||||

|

|

• |

Some issuers do not explain how they determined the useful lives for finite-lived intangible assets, or why an intangible asset has an indefinite useful life. Some issuers inappropriately determine an indefinite useful life for an intangible asset that has a finite useful life. |

• |

Distinguishing the indefinite-lived intangible assets from those with a finite life, as well as determining the useful lives for finite-lived intangible assets has an impact on the financial statements for the current period and for the subsequent periods. |

|

|

||||

|

|

|

|

Reference: Paragraph 10, B31-B34, 18 to 37 of IFRS 3 and paragraphs 118 to 123 of IAS 38 Intangible Assets |

|

|

|

||||

|

Functional Currency |

• |

Some issuers change their functional currency when the timing of that change did not correspond to the timing of the change in the underlying circumstances. |

• |

Once an issuer determines its functional currency, the functional currency should not change unless there is a change in the relevant underlying transactions, events and conditions. |

|

|

|

|

• |

We may ask issuers to explain what changes occurred and to explain timing of the change. |

|

|

|

|

• |

When there is a change in functional currency, the translation procedures applicable to the new functional currency is applied prospectively from the date of the change. |

|

|

|

|

• |

Issuers must also disclose that a change has occurred and the reason for the change. |

|

|

||||

|

|

|

|

Reference: Paragraphs 13, 35 and 54 of IAS 21 The Effects of Changes in Foreign Exchange Rates |

|

|

|

||||

|

Operating Segments |

• |

Issuers often aggregate several operating segments into a single operating segment for reporting purposes. This is particularly prevalent in certain industries such as the retail industry, for example, where retailers have several different distinct operations that offer a broad range of products (for example, home furnishings, personal care, and clothing) that are all considered to be part of one operating segment for reporting purposes. |

• |

Issuers that aggregate operating segments into a single operating segment for reporting purposes must ensure that the aggregation criteria have been met. Issuers are required to disclose the judgments made by management in applying the aggregation criteria. |

|

|

||||

|

|

|

|

• |

Issuers are required to report separately specific information about an operating segment that meets certain quantitative thresholds. |

|

|

||||

|

|

|

|

• |

Further, operating segments that do not meet any of the quantitative thresholds may be considered reportable, and separately disclosed, if management believes that information about the segment would be useful to investors of the financial statements. |

|

|

||||

|

|

|

|

Reference: Paragraph 8, 11 and 12 of IFRS 8 Operating Segments and Item 1.2 of Form 51-102F1. |

|

DISCLOSURE EXAMPLE

1. CREDIT RISK

The objective of IFRS 7 Financial Instruments: Disclosures (IFRS 7) is to ensure an entity provides disclosure to enable users to evaluate the significance of financial instruments and the nature and extent of risks arising from those financial instruments and how the entity manages those risks.

Credit risk is the risk that one party to a financial instrument will cause a loss for the other party by failing to discharge its obligations. Given continued economic challenges, many issuers have experienced an increase in their aged account receivables, however we have noted that the disclosure provided by some issuers in respect of their accounts receivable, and related allowances, are not sufficient for readers to understand the underlying credit risk.

The following is an example of the type of deficient disclosure that we have seen for accounts receivable (and related allowances).

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure -- Credit Risk

The issuer's annual financial statements credit risk note disclosed the following:

(000's)

December 31, 2015

December 31, 2014

Accounts Receivable

$61,550

$54,500

Allowance for doubtful accounts

( 2,550)

( 2,500)

Net Accounts Receivable

59,000

52,000

At December 31, 2015, the Company had $29 million (2014-- $24 million) of receivables that were considered past due. Collection usually occurs in the 30 day range.

- - - - - - - - - - - - - - - - - - - -

Specific disclosure missing from this example with respect to credit risk included:

• information about the credit quality of financial assets that are neither past due nor impaired (IFRS 7, paragraph 36(c));

• an analysis of the age of the accounts receivable that are past due, but not impaired (IFRS 7, paragraph 37(a));

• an analysis of accounts receivable that are individually determined to be impaired as at the reporting date, including the factors the issuer considered in determining that they are impaired (IFRS 7, paragraph 37(b));

• a reconciliation of changes to the allowance account for credit losses (IFRS 7, paragraph 16).

A better example of disclosure might be as follows:

- - - - - - - - - - - - - - - - - - - -

Example of Entity-Specific Disclosure -- Credit Risk

Credit risk is the risk that we will experience financial loss if a customer does not fulfill its contractual obligations to us. Our credit risk exposure is mainly limited to accounts receivable from our customers. The allowance for doubtful accounts and past due receivables are reviewed by management on a monthly basis. Accounts receivable are considered for impairment on a case-by-case basis when they are past due to determine if there is any objective evidence of impairment that a customer will default. Accounts receivable that are past due but not impaired are receivables where customers have failed to make payments when contractually due, but we expect the full amount to be collected.

Management assesses impairment after taking into consideration the customer's payment history, their credit worthiness and the current economic environment in which the customer operates to assess impairment. Historical bad debt expenses have not been significant and have typically been limited to specific customer circumstances. Given the cyclical nature of the oil and gas industry along with the current economic operating environment, a customer's ability to fulfill its payment obligations can change suddenly and without notice.

Based on the nature of its operations, ABC Ltd. will always have a concentration of credit risk in one industry-as a substantial portion of the Company's accounts receivable are with customers in the oil and gas industry. As at December 31, 2015, one customer comprised 43% of trade accounts receivable (2014 -- 15%).

Management expects full collection on accounts receivable that are neither past due nor impaired.

The following table presents accounts receivables as at December 31, 2015:

Past due but not impaired

(000's)

Neither past due nor impaired

<30 days

31-90 days

90-180 days

>180 days

Total

Accounts receivable

$30,000

$12,000

$9,000

$7,000

$1,000

$59,000

The following table presents accounts receivable as at December 31, 2014:

Past due but not impaired

(000's)

Neither past due nor impaired

<30 days

31-90 days

90-180 days

>180 days

Total

Accounts receivable

$28,000

$10,000

$6,500

$5,000

$2,500

$52,000

For the years ended December 31, 2015 and 2014, the change in the allowance for doubtful account is as follows:

(000's)

<<2015>>

<<2014>>

Balance, beginning of the year

$2,500

$2,450

Allowance

400

300

Write-offs

(350)

(250)

Balance, end of year

2,550

2,500

One customer that had a receivable balance of $350 outstanding for a period of greater than 180 days as at December 31, 2015 has indicated that it would not be able to pay due to financial difficulties experienced by the company. As a result, we included an allowance of $200 during fiscal 2015 (fiscal 2014 -- $150) and subsequently wrote off the full amount of $350 as at December 31, 2015.

- - - - - - - - - - - - - - - - - - - -

MD&A DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

MD&A |

||||

|

|

||||

|

Liquidity and Capital Resources |

• |

Many issuers continue to face going concern and liquidity risks. We continue to see issuers provide a boilerplate discussion of liquidity and capital resources, or merely reproduce amounts from their statements of cash flows without providing any analysis. |

• |

This section of the MD&A should discuss an issuer's ability to generate sufficient financial resources in the short term and the long term, to maintain its capacity, to meet its planned growth or to fund development activities. |

|

|

||||

|

|

• |

Some issuers have refinanced or entered into new debt facilities which generally resulted in more restrictive covenants and a decreased borrowing capacity but failed to discuss the actual and expected changes in the source of funds required to meet any shortfall resulting from the decreased borrowing capacity. |

• |

If an issuer has, or expects to have, a working capital deficiency, the MD&A should discuss the issuer's ability to meet obligations as they become due and how the issuer expects to remedy the deficiency. |

|

|

||||

|

|

• |

Issuers that have debt covenants that they have breached or may breach in the near term do not discuss how they intend to cure the default or address the significant risk of default. |

• |

Issuers should discuss any defaults or arrears or any significant risk of defaults or arrears on debt covenants. If an issuer is close to breaching its covenants, waiting to disclose this risk until after a covenant has been breached is not acceptable or useful and may have a material impact on investors. |

|

|

||||

|

|

|

|

• |

We encourage issuers with debt covenants to include the terms and conditions of the debt covenants, especially when a breach of the covenant could trigger a material additional funding requirement or early repayment. |

|

|

||||

|

|

|

|

• |

These disclosures are important to enable investors to assess how an issuer will meet its obligations and short and long-term objectives, particularly if an issuer's financial condition has deteriorated. |

|

|

||||

|

|

|

|

Reference: Item 1.6 and 1.7 of Form 51-102F1 |

|

|

|

||||

|

Forward Looking Information (FLI) |

• |

We continue to see issuers that fail to provide required disclosure relating to FLI. In particular, we note that while many issuers disclose FLI in their MD&A, news releases and other CD documents to the public, they do not always update this information as required. |

• |

Issuers must discuss, in their MD&A, the events and circumstances that occurred during the period that are reasonably likely to cause actual results to differ materially from material FLI that has been previously disclosed to the public and the expected differences. |

|

|

||||

|

|

|

|

• |

Updates to previously disclosed FLI help investors understand the issuer's progress toward achieving previously disclosed targets and objectives and any material changes that may likely impact its business. |

|

|

||||

|

|

• |

We have also observed issuers who withdrew previously disclosed material FLI without providing the required disclosure. In particular, we note issuers that cease to report FLI when actual results vary negatively from the previously disclosed FLI. |

• |

If issuers decide to withdraw previously disclosed material FLI, they must disclose this decision in their MD&A and discuss the events and circumstances that led it to that decision, including a discussion of the assumption underlying the FLI that are no longer valid. |

|

|

||||

|

|

|

|

Reference: Part 4A and 4B and section 5.8(5) of NI 51-102 |

|

|

|

||||

|

Overall Performance (Discussion of Operating Segments) |

• |

We continue to see issuers identify segments in their MD&A that are inconsistent with those identified in their financial statements. |

• |

At a minimum, the discussion of operating segments should be based on the operating segments as disclosed in the issuer's financial statements. |

|

|

||||

|

|

• |

With respect to financial performance, some issuers fail to provide an analysis of operating segments using the segment performance measures presented in the financial statements (i.e. segment revenue or segment profit and loss). |

• |

This section of the MD&A should provide an analysis of the issuer's financial condition, financial performance and cash flows, and should specifically address operating segments. Issuers may supplement the discussion with the use of non-GAAP financial measures. Such supplemental disclosure should not be more prominent than the GAAP measure. |

|

|

||||

|

|

|

|

• |

This disclosure enables investors to assess the performance of each operating segment that is reported in the issuer's financial statements. |

|

|

||||

|

|

|

|

Reference: Item 1.2(a), Item 1.4(a) of Form 51-102F1 |

|

|

|

||||

|

Investment Entities |

• |

Some issuers relying on the investment entity definition in IFRS 10 Consolidated Financial Statements do not provide sufficient information, both qualitative and quantitative, for their material investments and related investment and operating activities. |

• |

Except in limited circumstances, an investment entity must measure its investments at fair value through profit and loss, including its investments in subsidiaries. |

|

|

||||

|

|

|

|

In order to meet the requirements in Item 1.2 and 1.4 of Form 51-102F1 and in order to provide investors with sufficient information, issuers should provide the following: |

|

|

|

||||

|

|

|

|

• |

Sufficient MD&A disclosure about material investments and portfolio changes to understand fair market value fluctuations, how fair market value is determined and changes in investment portfolio composition. |

|

|

||||

|

|

|

|

• |

The MD&A should also discuss the investment entity's investment strategy and parameters and investment specific risks and uncertainties that may materially impact the issuer's performance and financial condition. This information should also be included in the issuer's Annual Information Form (AIF) (Item 5 of Form 51-102F2 Annual Information Form). |

|

|

||||

|

|

|

|

• |

Sufficient disclosure for related party agreements, executive compensation and highly concentrated investments are also important considerations for investment entities in discussing their financial performance and operations. |

|

|

||||

|

|

|

|

• |

We may also consider if additional financial or operational information should be provided to investors. |

|

|

||||

|

|

|

|

• |

Mining and oil and gas issuers should also consider the applicability of technical disclosure requirements. |

|

|

||||

|

|

|

|

Reference: IFRS 10 and Item 1.2 and 1.4 of Form 51-102F1 |

|

DISCLOSURE EXAMPLES

1. NON-GAAP FINANCIAL MEASURES

A non-GAAP financial measure (NGM) is a numerical measure of an issuer's historical or future financial performance, financial position or cash flow that is not specified, defined or determined under the issuer's GAAP and is not presented in an issuer's financial statements. A NGM excludes amounts that are included in, or includes amounts that are excluded from, the most directly comparable measure specified, defined or determined under the issuer's GAAP.

CSA Staff Notice 52-306 (Revised) Non-GAAP Financial Measures (SN 52-306) provides guidance to issuers that disclose NGMs. The guidance is intended to help ensure that the information disclosed does not mislead investors. SN 52-306 states that in order to ensure that a NGM does not mislead investors, an issuer should present with equal or greater prominence to that of the NGM, the most directly comparable measure specified, defined or determined under the issuer's GAAP and presented in its financial statements.{2}

We continue to see issuers that fail to disclose and discuss the most directly comparable GAAP measure as presented in the financial statements when they present and discuss NGMs in their MD&As or news releases. We often see issuers that highlight the NGM, sometimes in bold print and mention the most directly comparable GAAP measure in a less prominent location in the disclosure, most often when the GAAP measure is less favourable than the positive NGM. Determining whether inappropriate prominence is given to a NGM measure is a matter of judgement, taking into account the manner in which the NGM is presented (for example, ordering and font style) as compared to the related GAAP measure, as well as the emphasis of the related commentary. It would be inappropriate for an issuer to discuss results and trends of its NGMs, without at least providing equally prominent discussion of the most directly comparable GAAP measure.

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure -- Non-GAAP Measures in MD&A

The Company achieved record financial results and met its financial targets. Adjusted EBITDA{1} which excludes the impact of interest, taxes, depreciation, amortization and restructuring charges totaled $65 million in 2015, an increase of 12% from $58 million in 2014. The year-over-year increase in adjusted EBITDA is attributable to lower cash operating expenses, primarily from synergies achieved in the Company's cost structure.

- - - - - - - - - - - - - - - - - - - -

In the above example, the issuer failed to present and discuss the most comparable GAAP measure set out in the financial statements. In this case, the most comparable GAAP measure to "Adjusted EBITDA" would have been "Net Income".

A better example of disclosure might be as follows:

- - - - - - - - - - - - - - - - - - - -

Example of Entity-Specific Disclosure -- Non-GAAP Measures in MD&A

The Company's net income for the year decreased by 32% to $44 million (2014 -- $65 million). The year-over-year decrease in net income is primarily attributable to an increase in amortization and depreciation of $6.5 million due to a reduction in the estimated useful life of certain IT systems, and a restructuring charge of $15 million related to Company-wide efforts to improve efficiencies and centralize certain processes. Adjusted EBITDA{1}, which excludes the impact of interest, taxes, depreciation, amortization and restructuring charges totaled $65 million in 2015, an increase of 12% (2014 -- $58 million).

- - - - - - - - - - - - - - - - - - - -

In the above example, the issuer presents and discusses the directly most comparable GAAP measure with equal or greater prominence to that of the NGM. The disclosure also highlights the decreased "Net Income" despite the increased "Adjusted EBITDA" (the related NGM). Failing to highlight the decreased "Net Income" is misleading.

2. DISCUSSION OF OPERATIONS

Venture Issuers without Significant Revenue

Many venture issuers incur significant costs, either capitalized or expensed, on projects that have not generated significant revenue, but fail to provide adequate disclosure in accordance with Item 1.4, Item 1.7(a)(iii), and Item 1.15(b)(i) of Form 51-102F1.

To meet these requirements, issuers should discuss the following for each significant project:

• details of the project, including the issuer's plan for the project and the current status relative to plan;

• costs incurred to date and costs incurred for each of the periods presented;

• nature, timing and estimated costs to complete the project;

• risks and uncertainties that the issuer reasonably believes may materially affect future performance (for example, for a research and development company, this may include obtaining necessary regulatory approval); and

• other capital resources required to maintain capacity, meet planned growth or to fund development activities.

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure -- Venture Issuers without Significant Revenue (development stage biotech company)

We are primarily focused on the research, development and commercialization of Technology X and completing clinical trials and obtaining regulatory acceptance from Health Canada. Our Phase III clinical trials commenced in July 2015. For the year ended December 31, 2015, we generated revenues of $nil and recorded a loss of $3 million. For the year ended December 31, 2015, we had negative operating cash outflows of $3.1 million.

- - - - - - - - - - - - - - - - - - - -

The above example does not provide sufficient information about the company's business objectives, progress towards its business objectives, resources required to achieve its business objectives, or costs incurred to date. A better example of disclosure might be as follows:

- - - - - - - - - - - - - - - - - - - -

Example of Entity-Specific Disclosure -- Venture Issuers without Significant Revenue (development stage biotech company)

(Note: The requirement to describe the project is not fully reflected in this illustrative example.)

During 20XX, the company initiated activities to develop Technology X. Based on the positive results of these activities, the company is currently focused on developing Prototype A using Technology X. During the year ended December 31, 2015, we advanced Prototype A by completing Phase II clinical trials and commenced Phase III clinical trials.

Our primary business objectives over the next 12 months are:

-- Complete Phase III clinical trials and conduct a study for additional patients that may be required by Health Canada, complete data readout and analysis, submit the application to Health Canada; and

-- Hire additional staff that would be required to conduct Phase III trials and monitor progress and results.

In order to obtain approval from Health Canada, we must successfully complete Phase III clinical trials. In addition, Health Canada may require us to conduct studies for additional patients to gather further evidence for effectiveness of the prototype. Upon obtaining the final approval from Health Canada, we can establish a manufacturing contract with a supplier with appropriate regulatory approval certification and commence production. In anticipation of completing the pivotal Phase III clinical trials, we are in the process of negotiating with certain suppliers, however there can be no assurance that the company will be able to secure manufacturing capacity of a third-party manufacturer on suitable terms.

Our Phase III clinical trials for Prototype A commenced in July 2015, have 300 patients enrolled, and are conducted by third party contractors such as ABC Company at several sites in Ontario, Alberta, British Columbia, and Saskatchewan. Phase III clinical trials are expected to cost $1.5 million and be completed by July 2016. We anticipate submitting the application to Health Canada in December 2016 after we have evaluated and analyzed the data. The application to Health Canada must meet specific requirements and the review by Health Canada normally takes a period of 8 to 12 months. There is no assurance that Health Canada will accept the application or, if accepted, any approval will be granted on a timely basis. A failure to obtain approval or a delayed approval would adversely affect our business.

The research and development (R&D) of Prototype A will require an estimated total investment of $8.5 to $11 million. As of December 31, 2015, we have incurred cumulative expenditures of approximately $8.5 million (December 31, 2014-- $6.5 million) on Prototype A. For the year ended December 31, 2015, we incurred a total of $2 million (2014 -- $3.5 million) on R&D expenses. The material components of the expenses for prototypes A are disclosed below in the MD&A (Note: chart not included in this illustrative example). The decrease in R&D expenses compared to 2014 is due to the fact that the expenditures for Phase II trials for Prototype A were substantially incurred in prior years while expenditures in 2015 are mainly related to data analysis for Phase II trials and the preparation of Phase III trials.

As of December 31, 2015, we have working capital of $0.7 million. We plan to raise $2 million in the next year through private placements to meet the capital requirements. We have not entered into any financing agreements and there is no assurance that we will obtain funding for our operations.

- - - - - - - - - - - - - - - - - - - -

OTHER REGULATORY DISCLOSURE DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

REGULATORY |

||||

|

|

||||

|

Material Contracts |

• |

We continue to see issuers that make prohibited redactions in a material agreement. For example, we have seen redactions of debt covenants and ratios in financing or credit agreements or key terms necessary for an understanding of the impact of the contract on the business. |

• |

Redactions of provisions in a material agreement are permitted if the issuer reasonably believes that disclosure of that provision would be seriously prejudicial to the interests of the issuer or would violate confidentiality provisions. |

|

|

||||

|

|

• |

We also see issuers that fail to provide a description of the type of information redacted. |

• |

We may ask the issuer to explain the basis for considering the disclosure of the provision seriously prejudicial. |

|

|

||||

|

|

• |

We also see inconsistencies between the material contracts filed on SEDAR and those listed as material contracts in the AIF, with some of the latter (for example) not filed on SEDAR. |

• |

Certain redactions are not permitted, including debt covenants and ratios in financing or credit agreements; events of default or other terms relating to the termination of the material contract; or other terms necessary for understanding the impact of the material contract on the business of the issuer. |

|

|

||||

|

|

|

|

• |

Issuers should consider their disclosure obligations when negotiating material contracts with third parties. |

|

|

||||

|

|

|

|

• |

The AIF must discuss the particulars of any material contracts. |

|

|

||||

|

|

|

|

• |

We note that if an issuer's business is substantially dependent on a contract, then the issuer does not meet the ordinary course exemption and must file the material contract on SEDAR. |

|

|

||||

|

|

|

|

Reference: Sections 12.2 and 12.3 of NI 51-102 and Item 15 of Form 51-102F2. |

|

|

|

||||

|

Audit Committee Composition -- Venture Issuers |

• |

Some venture issuers have not met the audit committee composition requirements. |

• |

Effective for financial years beginning on or after January 1, 2016, the audit committee of a venture issuer must be composed of a minimum of three members, each of whom is a director and a majority of whom must not be executive officers, employees, control persons of the venture issuer or of an affiliate of the venture issuer. |

|

|

||||

|

|

|

|

• |

Exceptions are provided in certain circumstances until the later of the next annual meeting and the date that is six months after the date on which the circumstances arose. |

|

|

||||

|

|

|

|

Reference: Part 6 -- Venture Issuers of NI 52-110 Audit Committees |

|

|

|

||||

|

Management Information Circular |

• |

Some management information circulars prepared in situations of restructuring under which securities are to be changed, exchanged, issued or distributed do not provide prospectus level disclosure. |

• |

In preparing a management information circular, the issuer must provide disclosure described in the form of prospectus (i.e. NI 41-101F1 Information Required in a Prospectus, NI 44-101F1 Short Form Prospectus). |

|

|

||||

|

|

• |

Some issuers who, for example, spin out a new entity or complete a reverse takeover transaction, fail to provide a full description of the proposed business of the company and related financial information. |

• |

This includes, among other things, financial statements, executive compensation disclosure, risk factors and a fulsome description of the business as required by the prospectus form. |

|

|

||||

|

|

• |

Some issuers do not incorporate by reference the management information circular related to a restructuring transaction into their material change report or the material change report does not include the disclosure as required by Item 5.2 of Form 51-102F3. |

• |

In the case where a management information circular, non-offering prospectus or filing statement is not filed, the issuer must include the information required by Item 14.2 of Form 51-102F5 (Item 14.2) in the material change report. |

|

|

||||

|

|

|

|

• |

In determining whether the business being acquired is a significant acquisition for purposes of Item 14.2, venture issuers can apply the threshold that came into effect with the venture issuer amendments on June 30, 2015, which set the significance threshold at 100% for asset and investment tests. |

|

|

||||

|

|

|

|

Reference: Item 14.2 of Form 51-102F5-- Information Circular and Item 5.2 of Form 51-102F3-Material Change Report |

|

|

|

||||

|

Annual Information Form |

• |

Issuers often do not provide sufficient description of their business and the applicable risk factors in their AIF. |

• |

The AIF should include a description of the issuer's business and its operating segments that are reportable segments (as described in the issuer's GAAP). |

|

|

||||

|

|

|

|

• |

The disclosure should also provide information on various aspects of the business, including but not limited to, production and services, specialized skills and knowledge, competitive conditions, new products, any economic dependence and changes to contracts. |

|

|

||||

|

|

|

|

• |

It is also important to discuss, in sufficient detail, the relevant risk factors that affect the issuer. If a particular risk, for example, cash flow and liquidity, has become particularly prevalent in the current year, issuers should update their disclosure to address this change. |

|

|

||||

|

|

|

|

Reference: Item 5 of Form 51-102F2 |

|

DISCUSSION OF OTHER REGULATORY DEFICIENCIES

1. INSIDER REPORTING

Insider reporting requirements are found in National Instrument 55-104 Insider Reporting Requirements and Exemptions (NI 55-104). Through our reviews, we continue to find deficiencies in insider reports filed by reporting insiders of issuers of all sizes.

Reporting insiders are generally required to file an initial insider report within 10 calendar days of becoming a reporting insider and any subsequent insider reports reflecting changes in their holdings within 5 calendar days of such change. Also reporting insiders should update their insider profile on SEDI when they cease to be an insider of a reporting issuer within 10 calendar days of the change.

Some of the most common insider reporting deficiencies and/or errors we have seen in the past year include:

• missing SEDI profiles for reporting insiders who are required to file reports pursuant to NI 55-104;

• failure to file insider reports on SEDI for acquisitions made pursuant to a normal course issuer bid;

• failure to report the expiration of certain issuer derivative securities such as options or warrants within the required 5 day period; and

• failure to file amended issuer profile supplements on SEDI to reflect changes, such as adding a new security designation to reflect the adoption of a stock option plan.

Further, we continue to see balance discrepancies between the information contained in a reporting insider's SEDI filings and the related information disclosed in the issuer's CD records. In order to avoid variances in the public records filed by the issuer, we recommend that issuers implement a process to annually verify the securities holdings communicated to them by their reporting insiders. Also, reporting insiders should be proactive and regularly review the information circulars and other CD records of the issuer to ensure their security holdings are properly reflected. We encourage issuers to engage with their reporting insiders more frequently to ensure the accurate and complete reporting of all insider information.

We see many insider reports being filed on SEDI with:

• inaccurate transaction codes;

• inaccurate transaction dates;

• inaccurate reporting with respect to type of ownership (direct, indirect or control or direction);

• failing to report the name of the registered holder; and

• incorrect security designations created by issuers, precluding their reporting insiders from correctly reporting their transactions.

We understand that many reporting insiders rely on third parties to complete their SEDI filings which may result in late and/or inaccurate filings. We remind reporting insiders that the responsibility to file insider reports remains with the reporting insider regardless of whether they use a third party agent. In order to reduce deficiencies and inaccuracies, all reporting insiders should periodically review their SEDI profile and filings to make sure their reports are being filed correctly.

2. OIL AND GAS REPORTING

National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (NI 51-101) prescribes the disclosure standards and annual disclosure requirements for reporting issuers engaged in oil and gas activities, as defined in section 1.1 of NI 51-101.

Section 2.1 of NI 51-101 requires the annual filing of:

• Form 51-101F1 Statement of Reserves Data and Other Oil and Gas Information (Form NI 51-101F1);

• Form 51-101F2 Report on [Reserves Data][,] [Contingent Resources Data][,] [and] [Prospective Resources Data] by Independent Qualified Reserves Evaluator or Auditor; and

• Form 51-101F3 Report of Management and Directors on Oil and Gas Disclosure.

Observed disclosure deficiencies often involve errors; omissions and potentially misleading information of abandonment and reclamation costs; resources other than reserves and type wells; drilling locations and required associated information.

Resources other than reserves -- deficiencies include disclosure of estimates that have not been risked for chance of commerciality and the absence of meaningful disclosure concerning both risks and level of uncertainty and significant positive and negative factors:

• Part 7 of the Form 51-101F1 requires disclosed estimates of contingent resources (Item 7.1) and prospective resources (Item 7.2) be risked for chance of commerciality;

• Subsection 5.9(1)(d) of NI 51-101 requires disclosure of risks and level of uncertainty associated with recovery of resources other than reserves; subsection 5.7(2) of the Companion Policy 51-101CP Standards of Disclosure for Oil and Gas Activities (51-101CP) states that a reporting issuer should ensure that in satisfying these requirements, their disclosure includes the risks and uncertainties appropriate and meaningful for their activities and it must not be in the form of a general disclaimer (emphasis added); and

• Subsection 5.9(2)(d)(iii) requires estimates be accompanied by the significant positive and negative factors relevant to the estimate.

Type of wells, drilling locations and associated information -- deficiencies include compliance with the requirements of Part 5 of NI 51-101:

• Estimates must be prepared or audited by a qualified reserves evaluator or auditor, per subsections 5.2(1)(a)(ii), 5.9(2)(a) and 5.10(1)(c);

• Estimates must be prepared in accordance with the Canadian Oil and Gas Evaluation Handbook (COGE Handbook), per subsections 5.2(1)(a)(iii), 5.3, 5.9(2)(b) and 5.10(1)(c); and

• Disclosure of analogous information must comply with section 5.10 (see section 5.8 of the 51-101CP).

Abandonment and reclamation costs -- deficiencies include absence of disclosure concerning significant abandonment and reclamation costs:

• Item 5.2 of Form 51-101F1 requires identification and discussion of significant economic factors or uncertainties that affect particular components of reserves data (emphasis added), with abandonment and reclamation costs specified in Instruction (1); and

• Item 6.2.1 of Form 51-101F1 requires identification and discussion of significant economic factors or uncertainties that have affected or are reasonably expected to affect the anticipated development or production activities on properties with no attributed reserves (emphasis added), with abandonment and reclamation costs specified in Instruction (1).

Issuers are reminded that publicly disclosed estimates of future net revenue must be net of abandonment and reclamation costs. For further information, please see CSA Staff Notice 51-345 Disclosure of Abandonment and Reclamation Costs in National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities and Related Forms.

{2} Issuers should ensure that they refer to all the guidance set forth in SN 52-306 in preparing their disclosure documents in respect of NGMs.

{1} Refer to the "Non-GAAP financial measures" section on page X for more information about this measure and for a reconciliation of the NGM to the most directly comparable GAAP measure.

{1} Refer to the "Non-GAAP financial measures" section on page X. for more information about this measure and for a reconciliation of the NGM to the most directly comparable GAAP measure.

APPENDIX B

CATEGORIES OF OUTCOMES

Referred to Enforcement/Cease-Traded/Default List

If the issuer has substantive CD deficiencies, we may add the issuer to our default list, issue a cease trade order and/or refer the issuer to enforcement.

Refiling

The issuer must amend and refile certain CD documents or must file a previously unfiled document.

Prospective Changes

The issuer is informed that certain changes or enhancements are required in its next filing as a result of deficiencies identified.

Education and Awareness

The issuer receives a proactive letter alerting it to certain disclosure enhancements that should be considered in its next filing or when staff of local jurisdictions publish staff notices and reports on a variety of continuous disclosure subject matters reflecting best practices and expectations.

No Action Required

The issuer does not need to make any changes or additional filings. The issuer could have been selected in order to monitor overall quality disclosure of a specific topic, observe trends and conduct research.

Questions -- Please refer your questions to any of the following: