Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

CSA Notice of Publication of Multilateral Instrument 45-108 Crowdfunding

CSA Notice of Publication of Multilateral Instrument 45-108 Crowdfunding

CSA NOTICE OF PUBLICATION OF

MULTILATERAL INSTRUMENT 45-108

CROWDFUNDING

CSA Notice of Publication of Multilateral Instrument 45-108 Crowdfunding

Annex A -- Crowdfunding Regime

Annex A1 Multilateral Instrument 45-108 Crowdfunding

Annex A2 Form 45-108F1 Crowdfunding Offering Document

Annex A3 Form 45-108F2 Risk Acknowledgement

Annex A4 Form 45-108F3 Confirmation of Investment Limits

Annex B -- Amending Instrument for National Instrument 45-102 Resale of Securities

Annex C -- Summary of Notable Changes to the March 2014 45-108 Materials

Annex D2 Amending Instruments for Local Rules and Local Policy Changes

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

CSA Notice of Publication of Multilateral Instrument 45-108 Crowdfunding

CSA Notice of Publication of Multilateral Instrument 45-108 Crowdfunding

November 5, 2015

Introduction

The securities regulatory authorities in Manitoba, Ontario, Québec, New Brunswick and Nova Scotia (collectively, the participating jurisdictions or we) are publishing in final form Multilateral Instrument 45-108 Crowdfunding (MI 45-108 or the Rule), which includes a crowdfunding prospectus exemption (the crowdfunding exemption) and a registration framework for funding portals (funding portals) (collectively, the 45-108 crowdfunding regime). We are also making consequential amendments to other rules (the consequential amendments).

The Financial and Consumer Affairs Authority (FCAA) of Saskatchewan, which worked with the participating jurisdictions on the Rule, will be republishing MI 45-108 for a 60 day comment period.

The participating jurisdictions have coordinated their efforts in finalizing the 45-108 crowdfunding regime. In some jurisdictions, Ministerial approvals are required for the implementation of the 45-108 crowdfunding regime. Where applicable, Annex D provides information about each participating jurisdiction's approval process.

Provided all necessary Ministerial approvals are obtained, MI 45-108 will come into force in the participating jurisdictions on January 25, 2016.

Substance and purpose of the 45-108 crowdfunding regime

As securities regulators, we have the responsibility to examine whether securities law contributes to the efficient functioning of our capital markets, while maintaining adequate investor protection. This includes assessing whether the securities regulatory framework remains responsive and relevant in a dynamic environment that is being shaped by advances in technology and a broad array of demographic, cultural and economic forces.The internet and social media have enabled start-ups and technology companies that foster innovation to reach out to a large number of investors, including retail investors (the crowd), to raise capital.

Selling securities over the internet to a large number of investors, sometimes referred to as "crowdfunding", has emerged as a new way for some businesses, particularly start-ups and small and medium-sized enterprises (SMEs), to access capital that would not have otherwise been accessible. "Crowdfunding" is an umbrella term used to capture many forms of capital and fund raising, that in this context, we mean raising capital from members of the public through the distribution/sale of securities. Crowdfunding may enable issuers to raise capital more effectively and at a lower cost while also providing investors with greater access to investment opportunities. The 45-108 crowdfunding regime is intended to leverage the use of the internet and social media to facilitate capital formation primarily for start-ups and SMEs that foster innovation and to provide new investment opportunities for investors. At the same time, we believe the 45-108 crowdfunding regime maintains an appropriate level of investor protection and regulatory oversight to be responsive both to global market developments in this area and to our mandate to provide protection to investors.

The 45-108 crowdfunding regime will enable start-ups and SMEs in their early-stages of development to raise capital online from a large number of investors through a single registered funding portal. A limit on the total amount that can be raised will be imposed on issuers and investors will be subject to investment limits as a means of limiting their exposure to a highly risky investment. The registration of the funding portal is a key investor protection measure as registration addresses, among other things, potential integrity concerns that may apply to funding portals and the persons operating them, as well as potential concerns relating to conflicts of interest and self-dealing.

We believe the introduction of the 45-108 crowdfunding regime is a significant step in enhancing capital raising alternatives in Canada, particularly for start-ups and SMEs. The introduction of the 45-108 crowdfunding regime in the participating jurisdictions will allow start-ups and SMEs to benefit from greater access to capital from investors that was previously limited.

The 45-108 crowdfunding regime encompasses measures which are intended to provide effective protection for investors, including:

Type of security

•

issuers can only offer non-complex securities

Investment limits

•

investors are subject to the following investment limits:

•

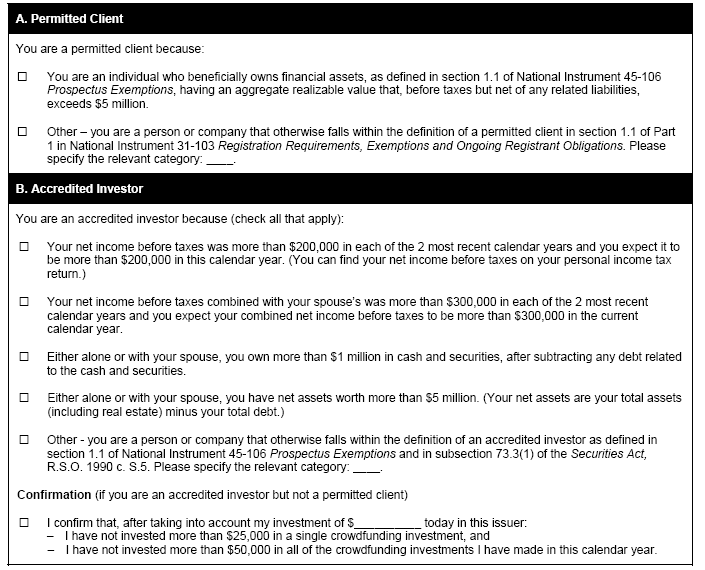

an investor that does not qualify as an accredited investor:

•

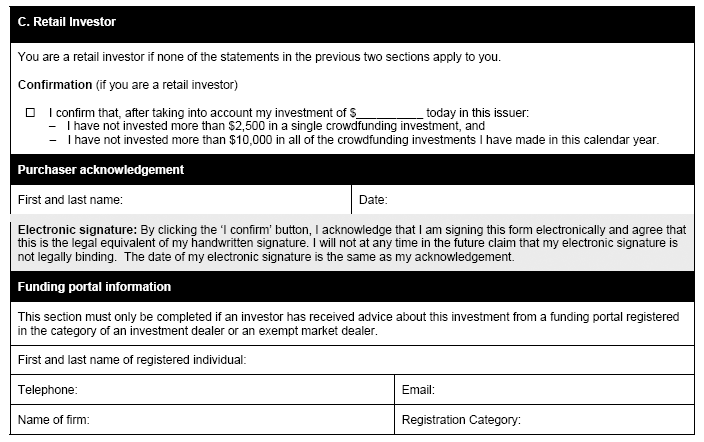

$2,500 per investment, and

•

in Ontario, $10,000 in total in a calendar year,

•

an accredited investor other than a permitted client:

•

$25,000 per investment, and

•

in Ontario, $50,000 in total in a calendar year,

•

in Ontario, no investment limits for a permitted client

Offering document

•

issuers are required to prepare an offering document that contains all of the information about the issuer and its business that an investor should know before purchasing the issuer's securities

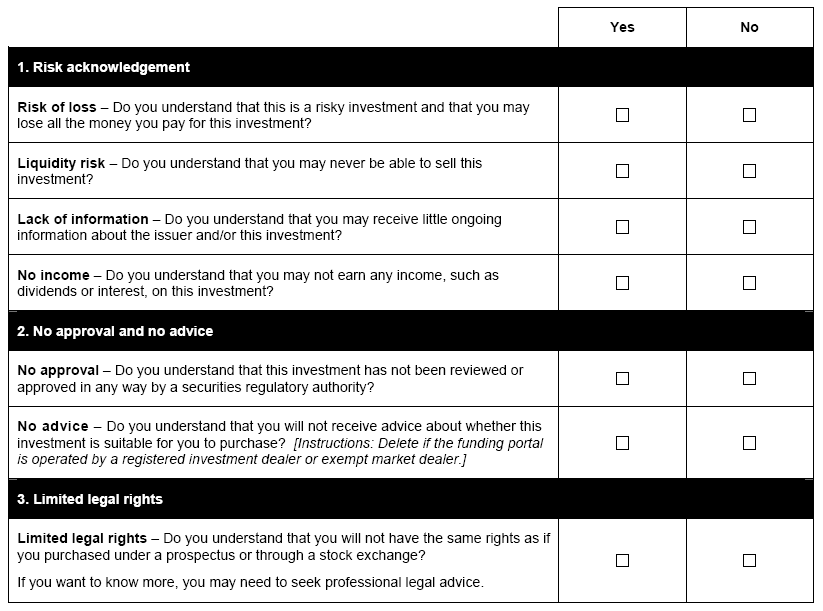

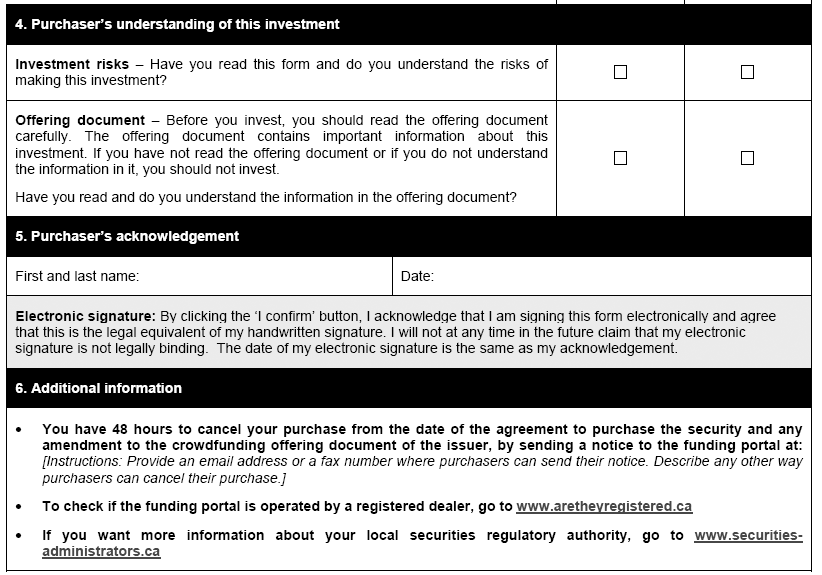

Risk acknowledgement form (RAF)

•

investors must complete a RAF requiring them to positively confirm having read and understood the risk warnings and information in the crowdfunding offering document before they can enter into an agreement to purchase securities

Liability for materials

•

issuers are accountable for and are subject to a standard of liability on the crowdfunding offering document and other permitted materials, and investors are provided with a related right of action

Advertising and solicitation

•

a prohibition on advertising and general solicitation

Ongoing disclosure

•

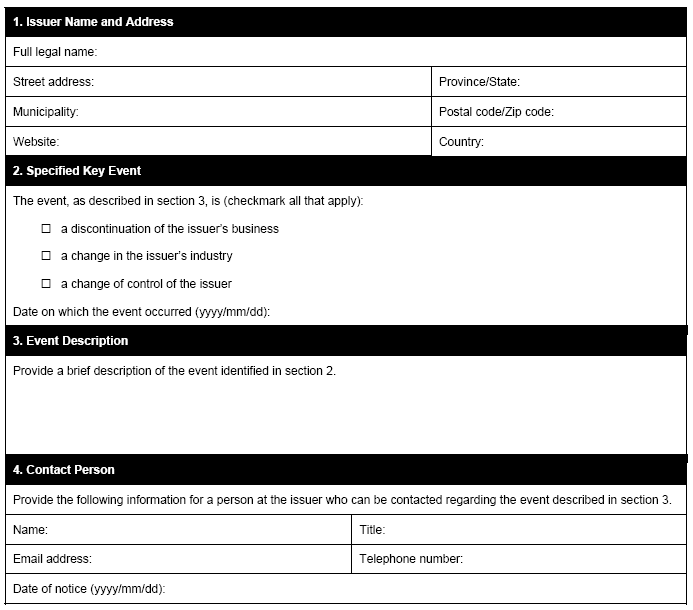

non-reporting issuers must make available to investors (i) annual financial statements, (ii) a notice of use of proceeds, and (iii) in New Brunswick, Nova Scotia and Ontario, a notice of a discontinuation of the issuer's business, a change in the issuer's industry or a change of control of the issuer

•

reporting issuers must continue to comply with all of their disclosure requirements

Registered funding portal

•

issuers can only distribute securities through a single funding portal that is registered as an investment dealer, exempt market dealer or restricted dealer as outlined in the Rule, and must post the offering document and other permitted materials solely on that funding portal's online platform

Funding portal requirements

•

funding portals are prohibited from offering securities of a related issuer

•

a funding portal must fulfill certain gatekeeper responsibilities prior to allowing an issuer access to its online platform, including reviewing the issuer's disclosure in the crowdfunding offering document and other permitted materials for completeness, accuracy and any misleading statements

•

a funding portal must review information and obtain background checks on the issuer and its directors, executive officers and promoters, and deny an issuer access to the funding portal in certain circumstances

We note that the use of the internet for raising capital is not restricted to crowdfunding as defined in the 45-108 crowdfunding regime. Many online platforms today are used to raise capital under other prospectus exemptions such as the accredited investor exemption.

Background

On March 20, 2014, the securities regulatory authorities of Saskatchewan, Manitoba, Québec, New Brunswick and Nova Scotia published a Notice of Publication and Request for Comment on two different crowdfunding prospectus exemption regimes:

• the start-up crowdfunding registration and prospectus exemptions (the start-up crowdfunding exemptions); and

• the proposed 45-108 crowdfunding regime.

The proposed 45-108 crowdfunding regime was also published on March 20, 2014 (the March 2014 45-108 materials) in a Notice and Request for Comment by the Ontario Securities Commission (OSC), as part of a broad review of the exempt market that would, among other things, introduce four new prospectus exemptions for issuers other than investment funds.

The securities regulatory authorities of British Columbia, Saskatchewan, Manitoba, Québec, New Brunswick and Nova Scotia have implemented the start-up crowdfunding exemptions by way of local blanket orders on May 14, 2015. The 45-108 crowdfunding regime and the start-up crowdfunding exemptions are viewed by those jurisdictions (except for British Columbia, which is not a jurisdiction participating in the 45-108 crowdfunding regime) as complementary regimes, as the 45-108 crowdfunding regime is available to both reporting and non-reporting issuers and provides both higher investment limits for investors and higher limits on the amount issuers can raise.

Summary of written comments received by the participating jurisdictions

The comment period for the March 2014 45-108 materials ended on June 18, 2014. The participating jurisdictions collectively received 70 written submissions. We have considered the comments received and thank all of the commenters for their input.

Comment letters received by the following jurisdictions can be viewed on their websites as noted:

• OSC -- www.osc.gov.on.ca

• AMF -- www.lautorite.qc.ca/en

A summary of the comments submitted to the OSC, together with the responses of OSC staff, is contained in Annex F.

A summary of the general themes raised in the comment letters that were received across the participating jurisdictions is set out under the heading "Key themes from the comment letters" below.

Key themes from the comment letters

There were several key themes expressed throughout the comment letters submitted to us. Below is a summary of these key themes.

Investor protection

A significant number of commenters raised concerns related to investor protection. Many of the commenters noted the high probability that investors would lose their entire investment in a start-up or a SME because these businesses typically have low survival rates and there are often issues related to corporate governance, insider trading and integrity concerns.

Some of the commenters further noted that unsophisticated investors are particularly vulnerable in a crowdfunding investment environment. Particular concerns expressed included:

• investors lack the requisite expertise, skills and experience to invest in a crowdfunded offering,

• investors are unfamiliar with start-up investing principles and the risks particular to start-ups and SMEs,

• investors lack sufficient information to make appropriate investment decisions due to the low level of disclosure required of non-reporting issuers under the crowdfunding exemption,

• there will be limited access to ongoing information about a start-up or SME that is a non-reporting issuer,

• investors do not understand and appreciate the restrictions on their ability to resell the shares they purchase, and

• the risk of fraud in a crowdfunding environment, particularly given the increased access of unsophisticated investors to private markets that the exemption would provide and the broad reach afforded by the internet.

As we expand accessibility to the exempt market through crowdfunding, we recognize that investor protection measures are an important component of the framework and we will remain vigilant in monitoring the adequacy of the protection it affords investors. We believe the 45-108 crowdfunding regime we are introducing will provide greater access to capital for start-ups and SMEs and that the framework we are adopting, including the measures noted above, will provide effective protection for investors.

Investment limits

The March 2014 45-108 materials included proposed investment limits for all investors: a $2,500 limit per investment and a $10,000 limit for all investments made by an investor under the crowdfunding exemption in a calendar year. A large number of commenters expressed a range of opinions about the proposed investment limits.

One group of commenters thought the proposed investment limits would frustrate the 45-108 crowdfunding regime's objectives of facilitating capital raising for start-ups and SMEs, would interfere with investors' ability to pursue their investment objectives, and would not provide meaningful investor protection.

Another group of commenters recommended that the dollar amount of the investment limits be reduced for investors. The commenters pointed to the concept of crowdfunding being based on small investments made by a broad pool of investors and the limited amount of funds Canadians have available to invest annually as evidenced by published economic data. The commenters argued that lower investment limits would discourage over-concentration by unsophisticated investors in a risky class of investments.

Several commenters supported removing or increasing investment limits for accredited investors. The arguments in support of this position generally pertained to the relatively high level of sophistication such investors possess and their ability to retain advice and withstand loss.

We continue to believe that investment limits are a necessary and appropriate investor protection tool that can help to reduce the risk associated with an investment in securities under the crowdfunding exemption, while still facilitating capital-raising by start-ups and SMEs. However, in light of the feedback received, we considered different approaches to investment limits under the crowdfunding exemption and have made changes to the investment limits that were proposed in the March 2014 45-108 materials.

Financial statement assurance requirements for non-reporting issuers and other financial disclosure

Several commenters provided feedback regarding the proposed assurance requirements for the financial statements of a non-reporting issuer that distributes securities in reliance on the crowdfunding exemption. The commenters' recommendations on non-reporting issuers' financial statements included a mandatory audit, a review being sufficient and a tiered approach to assurance requirements.

We continue to support a tiered approach to financial statement assurance requirements. After considering the comments, we have simplified and raised the thresholds based on the amount an issuer has raised under one or more prospectus exemptions since its formation. As such, a non-reporting issuer's financial statements will be required to be:

• audited or reviewed by a public accounting firm if the cumulative amount an issuer has raised under prospectus exemptions since its formation is $250,000 or more but is less than $750,000, or

• audited if the cumulative amount an issuer has raised under prospectus exemptions since its formation is $750,000 or more.

We think these thresholds strike an appropriate balance between providing investors with reliable financial information and not imposing a disproportionate financial burden on start-ups and SMEs that have limited financial resources to pursue their business.

Offering limit

Several commenters expressed views about the proposed $1.5 million limit on the aggregate amount that could be raised by an issuer group under the crowdfunding exemption. Although several commenters supported the proposed limit, an equal number of commenters thought the limit should be higher.

We maintain that a limit of $1.5 million is appropriate. The focus of the crowdfunding exemption is to facilitate capital raising by start-ups and SMEs, and the proposed limit is commensurate with the capital needs of issuers at this stage of development. There are other prospectus exemptions available to address the needs of issuers at more advanced stages of development.

Funding portal registration in other registration categories and use of the crowdfunding exemption

Many commenters disagreed with the prohibition on a funding portal against being registered in another registration category and suggested other registrants should be allowed to use the crowdfunding exemption. These commenters noted that registrants in other categories would have the experience and expertise to perform the work and comply with requirements in the Rule. They also noted that this restriction would increase complexity and costs for an issuer raising funds under multiple prospectus exemptions, and limiting funding portals to one prospectus exemption would prevent funding portals from being economically viable.

We considered the comments received and amended the March 2014 45-108 materials to permit registered dealers, such as investment dealers and exempt market dealers, to use the crowdfunding exemption. However, these registered dealers will need to comply with all of the requirements applicable to their registration category, including performing specific know-your-client and know-your product due diligence on the issuers, in addition to the requirements applicable to a funding portal as set out in the Rule.

However, a funding portal registered as a restricted dealer is a specialized type of restricted dealer that can only rely on the crowdfunding exemption to facilitate distributions of simple securities and their review of issuers will be limited in comparison to the know-your-product obligations of investment dealers and exempt market dealers relying on the crowdfunding exemption. In light of the limited activities of the restricted dealer funding portal, they will not be required to conduct a suitability assessment for the investor and will not assess the merits or expected returns of an investment. Rather, the restricted dealer funding portal will provide a gatekeeper role focused on compliance by issuers with the requirements of the Rule. Considering the limited activities of the restricted dealer funding portal, we continue to believe a funding portal that is registered as a restricted dealer in accordance with the Rule should not be registered in any other registration category, and, in Ontario, should not be affiliated with another registered firm.

Custodial requirements -- holding, handling or having access to purchaser funds or assets

Many commenters expressed an opinion on the restriction on holding, handling, or having access to client funds or securities by funding portals.

We acknowledge these comments and agree that client funds and assets would be better protected if they were held by the funding portal that is subject to capital and insurance requirements. We have amended the March 2014 45-108 materials so that a funding portal registered in the category of restricted dealer will be permitted to hold, handle, control or have access to purchaser funds provided the restricted dealer funding portal maintains the minimum capital requirement and fidelity bond insurance requirements equivalent to an exempt market dealer. Funding portals that are registered as exempt market dealers and investment dealers will be required to comply with the capital and insurance requirements applicable to their registration category and where applicable, as required by the Investment Industry Regulatory Organization of Canada.

Advertising and solicitation

The March 2014 45-108 materials proposed that all relevant information about a crowdfunding offering would be required to be made available only on the funding portal's online platform through which the distribution was to be made and not on any other website. An issuer could inform potential investors that the issuer was proposing to offer its securities under the crowdfunding exemption and refer the potential investors to the online platform of the funding portal for more information.

Commenters generally supported, or did not believe it was inappropriate to have, reasonable restrictions on advertising and solicitation by funding portals and issuers relying on the crowdfunding exemption. However, some commenters disagreed with the restrictions on advertising and solicitation by funding portals and issuers. They felt that limiting avenues or channels through which investors receive information or advertisements about an investment opportunity would be a detriment to an issuer seeking capital and to investors seeking as much information as possible about a potential investment. These commenters suggested that other means of communication, such as e-mail, text, or verbal communications, should also be permitted.

We note that an issuer is permitted to inform potential investors of its offering on the funding portal's online platform and may use any form of communication (e.g., text, email or posters) it chooses to direct potential investors to the funding portal's online platform. We continue to believe that all materials pertaining to a crowdfunding offering (including terms sheets and videos) should only be made available to potential investors on the funding portal's online platform for ease of investor reference and to facilitate the exchange of information and views that is conducive to eliciting the "wisdom of the crowd". This will also allow the funding portal to ensure that all materials of the issuer are consistent with the crowdfunding offering document and comply with the requirements on advertising and solicitation.

The funding portal is able to advertise its business. For example, it can advertise the fact that crowdfunding offerings could be made through the funding portal and the fact that information about such offerings would be posted on its online platform.

Changes to the March 2014 45-108 materials

After considering the comments received and consultations with stakeholders, we have made some changes to the proposal that was published for comment. We do not consider the changes made since the publication for comment to be material and therefore are not republishing the 45-108 crowdfunding regime for a further comment period.

Annex C contains a summary of notable changes between the March 2014 45-108 materials published for comment and the final publication.

Consequential amendments

National amendments

We are making consequential amendments to the following instrument:

• National Instrument 45-102 Resale of Securities so that securities distributed under the crowdfunding exemption are subject to a "restricted period" on resale.

In Québec, the consequential amendments to National Instrument 45-102 Resale of Securities are published for comment for a 30-day comment period. The consequential amendment is intended to come into force in Québec at the same time MI 45-108 comes into force on January 25, 2016.

Local amendments

Any changes to local rules or policies will be identified in a local notice, where applicable.

Local notices

Annex D is being published in any local jurisdiction that is making related changes to local securities laws and sets out any additional information that is relevant to that jurisdiction only.

Questions

Please refer your questions to any of:

Annexes to Notice

|

Annex A -- |

Crowdfunding Regime |

|

|

A1 Multilateral Instrument 45-108 Crowdfunding |

|

|

A2 Form 45-108F1 Crowdfunding Offering Document |

|

|

A3 Form 45-108F2 Risk Acknowledgement |

|

|

A4 Form 45-108F3 Confirmation of Investment Limits |

|

|

A5 Form 45-108F4 Notice of Specified Key Events |

|

|

A6 Form 45-108F5 Personal Information Form and Authorization to Collect, Use and Disclose Personal Information |

|

|

A7 Companion Policy 45-108CP Crowdfunding |

|

Annex B -- |

Amending Instrument for National Instrument 45-102 Resale of Securities |

|

Annex C -- |

Summary of Notable Changes to the March 2014 45-108 Materials |

|

Annex D -- |

Local Matters |

|

Annex E -- |

OSC List of Commenters |

|

Annex F -- |

OSC Summary of Comments and Responses |

Annex A -- Crowdfunding Regime

Annex A1 Multilateral Instrument 45-108 Crowdfunding

ANNEX A1

MULTILATERAL INSTRUMENT 45-108 CROWDFUNDING

Multilateral Instrument 45-108 Crowdfunding

Table of Contents

|

Part 1 |

Definitions and interpretation |

|

|

|

1. |

Definitions |

|

|

2. |

Terms defined or interpreted in other instruments |

|

|

3. |

Purchaser |

|

|

4. |

Specifications -- Québec |

|

|

||

|

Part 2 |

Crowdfunding prospectus exemption |

|

|

Division 1: Distribution requirements |

||

|

|

5. |

Crowdfunding prospectus exemption |

|

|

6. |

Conditions for closing of the distribution |

|

|

7. |

Certificates |

|

|

8. |

Right of withdrawal |

|

|

9. |

Liability for misrepresentation -- reporting issuers |

|

|

10. |

Liability for untrue statement -- non-reporting issuers |

|

|

11. |

Advertising and general solicitation |

|

|

12. |

Additional distribution materials |

|

|

13. |

Commissions or fees |

|

|

14. |

Restriction on lending |

|

|

15. |

Filing or delivery of distribution materials |

|

|

||

|

Division 2: Ongoing disclosure requirements for non-reporting issuers |

||

|

|

16. |

Annual financial statements |

|

|

17. |

Annual disclosure of use of proceeds |

|

|

18. |

Notice of specified key events |

|

|

19. |

Period of time for providing ongoing disclosure |

|

|

20. |

Books and records |

|

|

||

|

Part 3 |

Requirements for funding portals |

|

|

Division 1: Registration requirements, general |

||

|

|

21. |

Restricted dealer funding portal |

|

|

22. |

Registered dealer funding portal |

|

|

||

|

Division 2: Registration requirements, funding portals |

||

|

|

23. |

Restricted dealing activities |

|

|

24. |

Advertising and general solicitation |

|

|

25. |

Access to funding portal |

|

|

26. |

Issuer access agreement |

|

|

27. |

Obligation to review materials of eligible crowdfunding issuer |

|

|

28. |

Denial of issuer access and termination |

|

|

29. |

Return of funds |

|

|

30. |

Notifications |

|

|

31. |

Removal of distribution materials |

|

|

32. |

Monitoring purchaser communications |

|

|

33. |

Online platform acknowledgement |

|

|

34. |

Purchaser requirements prior to purchase |

|

|

35. |

Required online platform disclosure |

|

|

36. |

Delivery to the issuer |

|

|

37. |

Release of funds |

|

|

38. |

Reporting requirements |

|

|

||

|

Division 3: Additional requirements, restricted dealer funding portal |

||

|

|

39. |

Prohibition on providing recommendations or advice |

|

|

40. |

Restriction on referral arrangements |

|

|

41. |

Permitted dealing activities |

|

|

42. |

Chief compliance officer |

|

|

43. |

Proficiency |

|

|

||

|

Part 4 |

Exemption |

|

|

|

44. |

Exemption |

|

|

||

|

Part 5 |

Coming into force |

|

|

|

45. |

Effective date |

|

|

||

|

Appendix A -- Signing Requirements for Certificate of a Crowdfunding Offering Document (Section 7) |

||

|

|

||

|

Form 45-108F1 Crowdfunding Offering Document |

||

|

|

||

|

Form 45-108F2 Risk Acknowledgement |

||

|

|

||

|

Form 45-108F3 Confirmation of Investment Limits |

||

|

|

||

|

Form 45-108F4 Notice of Specified Key Events |

||

|

|

||

|

Form 45-108F5 Personal Information Form and Authorization to Collect, Use and Disclose Personal Information |

||

Multilateral Instrument 45-108 Crowdfunding

PART 1 DEFINITIONS AND INTERPRETATION

Definitions

1. In this Instrument

"accredited investor" means

(a) except in Ontario, an accredited investor as defined in National Instrument 45-106 Prospectus Exemptions, and

(b) in Ontario, an accredited investor as defined in subsection 73.3(1) of the the Securities Act, R.S.O. 1990 c. S.5 and in National Instrument 45-106 Prospectus Exemptions;

"aggregate minimum proceeds" means the amount disclosed in item 5.2 of the crowdfunding offering document that is sufficient to accomplish the business objectives of the issuer;

"Canadian Financial Statement Review Standards" means standards for the review of financial statements by a public accountant determined with reference to the Handbook;

"confirmation of investment limits form" means a completed Form 45-108F3 Confirmation of Investment Limits;

"crowdfunding offering document" means a completed Form 45-108F1 Crowdfunding Offering Document together with any amendment to that document and any document incorporated by reference therein;

"crowdfunding prospectus exemption" means the exemption from the prospectus requirement in section 5 [Crowdfunding prospectus exemption];

"distribution period" means the period referred to in the crowdfunding offering document during which an eligible crowdfunding issuer offers its securities to purchasers in reliance on the crowdfunding prospectus exemption;

"eligible crowdfunding issuer" means an issuer if all of the following apply:

(a) the issuer and, if applicable, its parent are incorporated or organized under the laws of Canada or any jurisdiction of Canada;

(b) the head office of the issuer is located in Canada;

(c) a majority of the directors of the issuer are resident in Canada;

(d) the principal operating subsidiary of the issuer, if any, is incorporated or organized under

(i) the laws of Canada or any jurisdiction of Canada, or

(ii) the laws of the United States of America or any state or territory of the United States of America or the District of Columbia;

(e) the issuer is not an investment fund;

"eligible securities" means securities of an eligible crowdfunding issuer having the same price, terms and conditions that are distributed under the crowdfunding prospectus exemption during the distribution period and are any one or more of the following:

(a) a common share;

(b) a non-convertible preference share;

(c) a security convertible into securities referred to in paragraph (a) or (b);

(d) a non-convertible debt security linked to a fixed or floating interest rate;

(e) a unit of a limited partnership;

(f) a flow-through share under the ITA;

"executive officer" means an individual who is

(a) a chair, vice-chair or president,

(b) a chief executive officer or chief financial officer,

(c) a vice-president in charge of a principal business unit, division or function including sales, finance or production, or

(d) performing a policy-making function in respect of the issuer;

"funding portal" means

(a) a registered dealer funding portal, or

(b) a restricted dealer funding portal;

"issuer access agreement" means a written agreement entered into between an eligible crowdfunding issuer and a funding portal in compliance with section 26 [Issuer access agreement];

"issuer group" means

(a) an eligible crowdfunding issuer,

(b) an affiliate of the eligible crowdfunding issuer, and

(c) any other issuer

(i) that is engaged in a common enterprise with the eligible crowdfunding issuer or with an affiliate of the eligible crowdfunding issuer, or

(ii) that is controlled, directly or indirectly, by the same person or company or persons or companies that control, directly or indirectly, the eligible crowdfunding issuer;

"permitted client" means a permitted client as defined in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

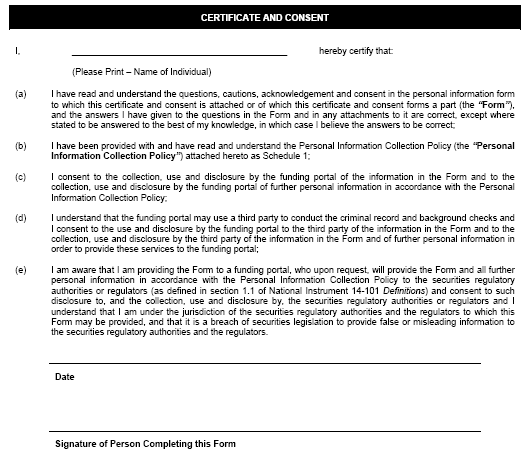

"personal information form" means a completed Form 45-108F5 Personal Information Form and Authorization to Collect, Use and Disclose Personal Information;

"registered dealer funding portal" means a person or company that

(a) is registered in the category of investment dealer or exempt market dealer under National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations, and

(b) acts or proposes to act as an intermediary in a distribution of eligible securities through an online platform in reliance on the crowdfunding prospectus exemption;

"restricted dealer funding portal" means a person or company that

(a) is registered in the category of restricted dealer under National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations,

(b) is authorized under the terms and conditions of its restricted dealer registration to distribute securities under this Instrument,

(c) acts or proposes to act as an intermediary in a distribution of eligible securities through an online platform in reliance on the crowdfunding prospectus exemption,

(d) is not registered in any other registration category, and

(e) in Ontario, is not an affiliate of another registered dealer, registered adviser, or registered investment fund manager;

"right of withdrawal" means the right referred to in section 8 [Right of withdrawal] or a comparable right described in securities legislation of the jurisdiction in which the purchaser resides;

"risk acknowledgement form" means a completed Form 45-108F2 Risk Acknowledgement;

"SEC issuer" means an SEC issuer as defined in National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards;

"U.S. AICPA Financial Statement Review Standards" means the standards of the American Institute of Certified Public Accountants for a review of financial statements by a public accountant, as amended from time to time.

Terms defined or interpreted in other instruments

2.

(1) Unless otherwise defined herein, in Part 2 [Crowdfunding prospectus exemption], each term has the meaning ascribed, or interpretation given, to it in National Instrument 45-106 Prospectus Exemptions.

(2) Unless otherwise defined herein, in Part 3 [Requirements for funding portals], each term has the meaning ascribed, or interpretation given, to it in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations.

Purchaser

3. References to a "client" in a provision of any instrument with which a funding portal is required to comply under Part 3 [Requirements for funding portals], must be read as if the references are to a "purchaser".

Specifications -- Québec

4.

(1) In Québec, "trade" in this Instrument refers to any of the following activities:

(a) the activities described in the definition of "dealer" in section 5 of the Securities Act (chapter V-1.1), including the following activities:

(i) the sale or disposition of a security by onerous title, whether the terms of payment be on margin, installment or otherwise, but does not include a transfer or the giving in guarantee of securities in connection with a debt or the purchase of a security, except as provided in paragraph (b);

(ii) participation as a trader in any transaction in a security through the facilities of an exchange or a quotation and trade reporting system;

(iii) the receipt by a registrant of an order to buy or sell a security;

(b) a transfer or the giving in guarantee of securities of an issuer from the holdings of a control person in connection with a debt.

(2) In Québec, the crowdfunding offering document and materials that are made available to purchasers by a reporting issuer in accordance with this Instrument are documents authorized by the Autorité des marchés financiers for use in lieu of a prospectus.

(3) In Québec, the crowdfunding offering document and materials that are made available to purchasers in accordance with this Instrument must be drawn up in French only or in French and English.

PART 2 CROWDFUNDING PROSPECTUS EXEMPTION

Division 1: Distribution requirements

Crowdfunding prospectus exemption

5.

(1) The prospectus requirement does not apply to a distribution by an eligible crowdfunding issuer of an eligible security of its own issue to a person or company that purchases the security as principal if all of the following apply:

(a) the issuer offers the securities during the distribution period and the distribution period ends no later than 90 days after the date the issuer first offers its securities to purchasers;

(b) the total proceeds raised by the issuer group in reliance on the crowdfunding prospectus exemption does not exceed $1,500,000 within the 12-month period ending on the last day of the distribution period;

(c) in Ontario, the acquisition cost of the securities acquired by the purchaser

(i) in the case of a purchaser that is not an accredited investor, does not exceed

(A) $2,500 for the distribution, and

(B) $10,000 for all distributions in reliance on the crowdfunding prospectus exemption in the same calendar year,

(ii) in the case of a purchaser that is an accredited investor that is not a permitted client, does not exceed

(A) $25,000 for the distribution, and

(B) $50,000 for all distributions in reliance on the crowdfunding prospectus exemption in the same calendar year, and

(iii) in the case of a purchaser that is a permitted client, is not limited;

(d) except in Ontario, the acquisition cost of the securities acquired by the purchaser

(i) in the case of a purchaser that is not an accredited investor, does not exceed $2,500 for the distribution, and

(ii) in the case of a purchaser that is an accredited investor, does not exceed $25,000 for the distribution;

(e) the issuer distributes the securities through a single funding portal;

(f) before the purchaser enters into an agreement to purchase the securities, the issuer makes available to the purchaser, through the funding portal, a crowdfunding offering document that is in compliance with

(i) section 7 [Certificates] and section 8 [Right of withdrawal], and

(ii) section 9 [Liability for misrepresentation -- reporting issuers] or section 10 [Liability for untrue statement -- non-reporting issuers], as applicable.

(2) The crowdfunding prospectus exemption is not available if any of the following apply:

(a) the proceeds of the distribution are used by the issuer to invest in, merge with or acquire an unspecified business;

(b) the issuer is not a reporting issuer, and the issuer previously distributed securities in reliance on the crowdfunding prospectus exemption and is not in compliance with any of the following:

(i) section 15 [Filing or delivery of distribution materials];

(ii) section 16 [Annual financial statements];

(iii) section 17 [Annual disclosure of use of proceeds];

(iv) section 19 [Period of time for providing ongoing disclosure];

(v) section 20 [Books and records];

(vi) in New Brunswick, Nova Scotia and Ontario, section 18 [Notice of specified key events];

(c) the issuer is a reporting issuer and is not in compliance with its reporting obligations under securities legislation, including under this Instrument;

(d) the issuer has previously commenced a distribution under this section and that distribution has not closed, been withdrawn or otherwise terminated.

Conditions for closing of the distribution

6. A distribution in reliance on the crowdfunding prospectus exemption must not close unless

(a) the right of withdrawal has expired,

(b) the aggregate minimum proceeds have been raised through one or both of the following:

(i) the distribution;

(ii) any concurrent distributions by any member of the issuer group, provided that the proceeds from those distributions are unconditionally available to the eligible crowdfunding issuer at the time of closing of the distribution,

(c) the issuer has provided to the funding portal written confirmation of the proceeds of the concurrent distributions referred to in subparagraph (b)(ii), if any,

(d) the issuer has received

(i) the purchase agreement entered into between the issuer and the purchaser,

(ii) a risk acknowledgement form for the purchaser where the purchaser positively confirms having read and understood the risk warnings and the information in the crowdfunding offering document,

(iii) except in Ontario, confirmation and validation that the purchaser is an accredited investor if the acquisition cost is greater than $2,500, and

(iv) in Ontario, a confirmation of investment limits form for the purchaser, and

(e) the closing occurs within 30 days of the end of the distribution period.

Certificates

7.

(1) A crowdfunding offering document made available under paragraph 5(1)(f) [Crowdfunding prospectus exemption] must contain a certificate executed by the issuer in accordance with the applicable provisions of Appendix A, which

(a) if the issuer is a reporting issuer, states that "This crowdfunding offering document does not contain a misrepresentation. Purchasers of securities have a right of action in the case of a misrepresentation.", or

(b) if the issuer is not a reporting issuer, states that "This crowdfunding offering document does not contain an untrue statement of a material fact. Purchasers of securities have a right of action in the case of an untrue statement of a material fact."

(2) A certificate under subsection (1) must be true as at the date the certificate is signed, the date the crowdfunding offering document is made available to purchasers and the time of the closing of the distribution.

(3) If a certificate under subsection (1) ceases to be true after a crowdfunding offering document is made available to a purchaser, the issuer must

(a) amend the crowdfunding offering document and provide a newly dated certificate executed by the issuer in accordance with the applicable provisions of Appendix A, and

(b) provide the amended crowdfunding offering document to the funding portal for the purpose of making it available to purchasers.

Right of withdrawal

8. If the securities legislation of the jurisdiction in which a purchaser resides does not provide a comparable right, the crowdfunding offering document made available to the purchaser under paragraph 5(1)(f) [Crowdfunding prospectus exemption] must provide the purchaser with a contractual right to withdraw from any agreement to purchase the security by delivering a notice to the funding portal within 48 hours after the date of the agreement to purchase and any subsequent amendment to the crowdfunding offering document.

Liability for misrepresentation -- reporting issuers

9. If the securities legislation of the jurisdiction in which a purchaser resides does not provide a comparable right, the crowdfunding offering document of a reporting issuer, made available to the purchaser under paragraph 5(1)(f) [Crowdfunding prospectus exemption], must provide a contractual right of action against the issuer for rescission and damages that

(a) is available to the purchaser if the crowdfunding offering document or other materials made available to the purchaser contain a misrepresentation, without regard to whether the purchaser relied on the misrepresentation,

(b) is enforceable by the purchaser delivering a notice to the issuer

(i) in the case of an action for rescission, within 180 days after the date of purchase by the purchaser, or

(ii) in the case of an action for damages, before the earlier of

(A) 180 days after the purchaser first has knowledge of the facts giving rise to the cause of action, or

(B) 3 years after the date of purchase,

(c) is subject to the defence that the purchaser had knowledge of the misrepresentation,

(d) in the case of an action for damages, provides that the amount recoverable

(i) does not exceed the price at which the security was distributed, and

(ii) does not include all or any part of the damages that the issuer proves do not represent the depreciation in value of the security resulting from the misrepresentation, and

(e) is in addition to, and does not detract from, any other right of the purchaser.

Liability for untrue statement -- non-reporting issuers

10. The crowdfunding offering document of an issuer that is not a reporting issuer, made available to a purchaser under paragraph 5(1)(f) [Crowdfunding prospectus exemption], must provide a contractual right of action against the issuer for rescission and damages that

(a) is available to the purchaser if the crowdfunding offering document or other materials made available to the purchaser contain an untrue statement of a material fact, without regard to whether the purchaser relied on the statement,

(b) is enforceable by the purchaser delivering a notice to the issuer

(i) in the case of an action for rescission, within 180 days after the date of purchase by the purchaser, or

(ii) in the case of an action for damages, before the earlier of

(A) 180 days after the purchaser first has knowledge of the facts giving rise to the cause of action, or

(B) 3 years after the date of purchase,

(c) is subject to the defence that the purchaser had knowledge of the untrue statement of a material fact,

(d) in the case of an action for damages, provides that the amount recoverable

(i) does not exceed the price at which the security was distributed, and

(ii) does not include all or any part of the damages that the issuer proves do not represent the depreciation in value of the security resulting from the untrue statement of a material fact, and

(e) is in addition to, and does not detract from, any other right of the purchaser.

Advertising and general solicitation

11.

(1) An issuer must not, directly or indirectly, advertise a distribution, or solicit purchasers, under the crowdfunding prospectus exemption.

(2) Despite subsection (1), the issuer may inform purchasers that it proposes to distribute securities under the crowdfunding prospectus exemption and may refer purchasers to the funding portal facilitating the distribution.

Additional distribution materials

12.

(1) In addition to the crowdfunding offering document required to be made available to a purchaser under paragraph 5(1)(f) [Crowdfunding prospectus exemption], an issuer may make available to a purchaser only through the funding portal the following materials:

(a) a term sheet;

(b) a video;

(c) other materials summarizing the information in the crowdfunding offering document.

(2) The materials referred to in subsection (1) must be consistent with the information in the crowdfunding offering document.

(3) If an amended crowdfunding offering document is made available to purchasers, all materials made available to purchasers under this section must be amended, if necessary, and made available to purchasers through the funding portal.

Commissions or fees

13. No person or company in the issuer group or director or executive officer of an issuer in the issuer group may, directly or indirectly, pay a commission, finder's fee, referral fee or similar payment to any person or company in connection with a distribution in reliance on the crowdfunding prospectus exemption, other than to a funding portal.

Restriction on lending

14. No person or company in the issuer group or director or executive officer of an issuer in the issuer group may, directly or indirectly, lend or finance, or arrange lending or financing, for a purchaser to purchase securities of the issuer under the crowdfunding prospectus exemption.

Filing or delivery of distribution materials

15.

(1) An issuer must, no later than 10 days after the closing of the distribution, file with the securities regulatory authority or regulator Form 45-106F1 Report of Exempt Distribution.

(2) At the same time that the issuer files the form referred to in subsection (1), the issuer must file a copy of the crowdfunding offering document and the materials referred to in paragraphs 12(1)(a) and (c) [Additional distribution materials].

(3) Upon request, the issuer must deliver to the securities regulatory authority or regulator any video referred to in paragraph 12(1)(b) [Additional distribution materials].

Division 2: Ongoing disclosure requirements for non-reporting issuers

Annual financial statements

16.

(1) An issuer that is not a reporting issuer that has distributed securities under the crowdfunding prospectus exemption must deliver to the securities regulatory authority or regulator and make reasonably available to each purchaser, within 120 days after the end of its most recently completed financial year, the financial statements listed in paragraphs 4.1(1)(a), (b), (c) and (e) [Comparative annual financial statements and audit] of National Instrument 51-102 Continuous Disclosure Obligations.

(2) The financial statements referred to in subsection (1) must

(a) be approved by management of the issuer and be accompanied by

(i) a review report or auditor's report if the amount raised by the issuer under one or more prospectus exemptions from the date of the formation of the issuer until the end of its most recently completed financial year, is $250,000 or more but is less than $750,000, or

(ii) an auditor's report if the amount raised by the issuer under one or more prospectus exemptions from the date of the formation of the issuer until the end of its most recently completed financial year, is $750,000 or more,

(b) comply with paragraph 3.2(1)(a) [Acceptable accounting principles -- general requirements], subparagraph 3.2(1)(b)(i) [Acceptable accounting principles -- general requirements], and subsection 3.2(5) [Acceptable accounting principles -- general requirements] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards, and

(c) comply with section 3.5 [Presentation and functional currencies] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards.

(3) If the financial statements referred to in subsection (1) are accompanied by a review report, the financial statements must be reviewed in accordance with Canadian Financial Statement Review Standards and the review report must

(a) not include a reservation or modification,

(b) identify the financial periods that were subject to review,

(c) be in the form specified by Canadian Financial Statement Review Standards, and

(d) refer to IFRS as the applicable financial reporting framework.

(4) If the financial statements referred to in subsection (1) are accompanied by an auditor's report, the auditor's report must be

(a) prepared in accordance with section 3.3 [Acceptable auditing standards -- general requirements] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards, and

(b) signed by an auditor that complies with section 3.4 [Acceptable auditors] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards.

(5) If the financial statements referred to in subsection (1) are those of an SEC issuer,

(a) the financial statements may be prepared in accordance with section 3.7 [Acceptable accounting principles for SEC issuers] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards,

(b) the financial statements may be reviewed in accordance with U.S. AICPA Financial Statement Review Standards and accompanied by a review report prepared in accordance with U.S. AICPA Financial Statement Review Standards that

(i) does not include a modification or exception,

(ii) identifies the financial periods that were subject to review,

(iii) identifies the review standards used to conduct the review and the accounting principles used to prepare the financial statements, and

(iv) refers to IFRS as the applicable financial reporting framework if the financial statements comply with paragraph 3.2(1)(a) [Acceptable accounting principles -- general requirements] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards, and

(c) the financial statements may be audited in accordance with section 3.8 [Acceptable auditing standards for SEC issuers] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards.

(6) If the financial statements referred to in subsection (5) are accompanied by a review report and the statements have been reviewed in accordance with Canadian Financial Statement Review Standards, the review report must be in compliance with paragraphs (3)(a) to (c) and must

(a) refer to IFRS as the applicable financial reporting framework if the financial statements comply with paragraph 3.2(1)(a) [Acceptable accounting principles -- general requirements] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards, or

(b) refer to U.S. GAAP as the applicable financial reporting framework if the financial statements comply with section 3.7 [Acceptable accounting principles for SEC issuers] of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards.

(7) For the purpose of subsection (3) and paragraph (5)(b), the review report must be prepared and signed by a person or company authorized to sign a review report under the laws of a jurisdiction of Canada or a foreign jurisdiction, and that meets the professional standards of that jurisdiction.

(8) If any of the financial statements referred to in subsection (1) are not accompanied by an auditor's report or a review report prepared by a public accountant, the statements must include the following statement; "These financial statements were not audited or subject to a review by a public accountant, as permitted by securities legislation where an issuer has not raised more than a pre-defined amount under prospectus exemptions."

Annual disclosure of use of proceeds

17.

(1) The financial statements of an issuer referred to in section 16 [Annual financial statements] and the financial statements required under section 4.1 [Comparative annual financial statements and audit] of National Instrument 51-102 Continuous Disclosure Obligations must be accompanied by a notice that details, as at the date of the issuer's most recently completed financial year, the use of the gross proceeds received by the issuer from a distribution made under the crowdfunding prospectus exemption.

(2) An issuer is not required to provide the notice referred to in subsection (1) if

(a) the issuer has disclosed in one or more prior notices the use of the entire gross proceeds from the distribution, or

(b) the issuer is no longer required to deliver, and make available to purchasers, annual financial statements.

Notice of specified key events

18. In New Brunswick, Nova Scotia and Ontario, an issuer that is not a reporting issuer that distributes securities in reliance on the crowdfunding prospectus exemption must make reasonably available to each holder of a security acquired under the crowdfunding prospectus exemption, a notice in Form 45-108F4 Notice of Specified Key Events of each of the following events within 10 days of their occurrence:

(a) a discontinuation of the issuer's business;

(b) a change in the issuer's industry;

(c) a change of control of the issuer.

Period of time for providing ongoing disclosure

19. The obligations of an issuer that is not a reporting issuer under section 16 [Annual financial statements] and, in New Brunswick, Nova Scotia and Ontario, under section 18 [Notice of specified key events] apply until the earliest of the following events:

(a) the issuer becomes a reporting issuer;

(b) the issuer has completed a winding up or dissolution;

(c) the securities of the issuer are beneficially owned, directly or indirectly, by fewer than 51 security holders worldwide.

Books and records

20. An issuer that is not a reporting issuer that distributes securities under the crowdfunding prospectus exemption must maintain the following books and records relating to the distribution for 8 years following the closing of the distribution:

(a) the crowdfunding offering document and the materials referred to in subsection 12(1) [Additional distribution materials];

(b) the risk acknowledgement forms;

(c) except in Ontario, confirmation and validation that the purchaser is an accredited investor if the acquisition cost is greater than $2,500;

(d) in Ontario, the confirmation of investment limits forms;

(e) the ongoing disclosure documents described in Division 2 [Ongoing disclosure requirements for non-reporting issuers];

(f) the aggregate number of securities issued under the crowdfunding prospectus exemption, and the date of issuance and the price for each security;

(g) the names of all security holders of the issuer and the number and the type of securities held by each security holder;

(h) such other books and records as are necessary to record the business activities of the issuer and to comply with this Instrument.

PART 3 REQUIREMENTS FOR FUNDING PORTALS

Division 1: Registration requirements, general

Restricted dealer funding portal

21. A restricted dealer funding portal and a registered individual of the restricted dealer funding portal that distributes securities in reliance on the crowdfunding prospectus exemption must comply with all of the following:

(a) the requirements in this section and in Division 2 [Registration requirements, funding portals] and Division 3 [Additional requirements, restricted dealer funding portal] of this Part;

(b) the terms, conditions, restrictions and requirements applicable to a registered dealer and to a registered individual, respectively, including

(i) National Instrument 31-102 National Registration Database,

(ii) National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations, except for the following:

(A) Division 2 of Part 3 [Education and experience requirements], except for subsection 3.4(2) [Proficiency -- initial and ongoing] and section 3.9 [Exempt market dealer -- dealing representative];

(B) section 6.2 [If IIROC approval is revoked or suspended];

(C) section 6.3 [If MFDA approval is revoked or suspended];

(D) Part 8 [Exemptions from the requirement to register];

(E) Part 9 [Membership in a self-regulatory organization];

(F) paragraphs 11.5(2)(i), and (j) [General requirements for records];

(G) paragraphs 13.2(2)(c) and (d) and subsection 13.2(6) [Know your client];

(H) section 13.3 [Suitability];

(I) Division 3 of Part 13 [Referral arrangements], if the restricted dealer funding portal does not enter into a referral arrangement permitted under subsection 40(2) [Restriction on referral arrangements] of this Instrument;

(J) section 13.13 [Disclosure when recommending the use of borrowed money];

(K) section 13.16 [Dispute resolution service];

(L) paragraphs 14.2(2)(i), (j), (k), (m), and (n) [Relationship disclosure information];

(M) Division 5 of Part 14 [Reporting to clients], except for section 14.12 [Content and delivery of trade confirmation],

(iii) National Instrument 33-105 Underwriting Conflicts,

(iv) National Instrument 33-109 Registration Information, and

(v) the requirement to pay fees under securities legislation;

(c) the requirement to deal fairly, honestly and in good faith with purchasers;

(d) any other terms, conditions, restrictions or requirements imposed by a securities regulatory authority or regulator on the restricted dealer funding portal or on a registered individual of the restricted dealer funding portal.

Note: In Ontario, a number of requirements in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations do not apply because similar requirements are contained in provisions of the Securities Act (Ontario). To the extent that (a) one or more requirements of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations made applicable under section 21 [Restricted dealer funding portal] do not apply in Ontario, and (b) there is a similar requirement in the Securities Act (Ontario) that is referenced in a note in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations, a restricted dealer funding portal or a registered individual of the restricted dealer funding portal operating in Ontario is subject to the similar requirement referenced in the Securities Act (Ontario).

Registered dealer funding portal

22. A registered dealer funding portal and a registered individual of the registered dealer funding portal that distributes securities in reliance on the crowdfunding prospectus exemption must comply with all of the following:

(a) the requirements in this section and Division 2 [Registration requirements, funding portals] of this Part;

(b) the terms, conditions, restrictions or requirements applicable to its registration category and to a registered individual, respectively, under securities legislation.

Note: In Ontario, a number of requirements in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations do not apply because similar requirements are contained in provisions of the Securities Act (Ontario). To the extent that (a) one or more requirements of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations made applicable under section 22 [Registered dealer funding portal] do not apply in Ontario, and (b) there is a similar requirement in the Securities Act (Ontario) that is referenced in a note in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations, a registered dealer funding portal or a registered individual of the registered dealer funding portal operating in Ontario is subject to the similar requirement referenced in the Securities Act (Ontario).

Division 2: Registration requirements, funding portals

Restricted dealing activities

23.

(1) A funding portal and a registered individual of the funding portal must not act as intermediaries in connection with a distribution of or trade in securities of an eligible crowdfunding issuer that is a related issuer of the funding portal.

(2) For the purposes of subsection (1), an issuer is not a related issuer where a funding portal, an affiliate of the funding portal, or any officer, director, significant shareholder, promoter or control person of the funding portal or of any affiliate of the funding portal, has beneficial ownership of, or control or direction over, issued and outstanding voting securities of the issuer, or securities convertible into voting securities of the issuer that alone or together constitute 10 percent or less of the outstanding voting securities of the issuer.

Advertising and general solicitation

24.

(1) A funding portal must not, directly or indirectly, advertise a distribution or solicit purchasers under the crowdfunding prospectus exemption.

(2) A funding portal may only make available to purchasers the crowdfunding offering document and the materials under section 12 [Additional distribution materials].

(3) A funding portal must ensure that the information about an eligible crowdfunding issuer and a distribution of eligible securities of the issuer is presented or displayed on its online platform in a fair, balanced and reasonable manner.

Access to funding portal

25.

(1) Prior to allowing an eligible crowdfunding issuer to access the funding portal for the purposes of posting a distribution, a funding portal must

(a) enter into an issuer access agreement with the issuer,

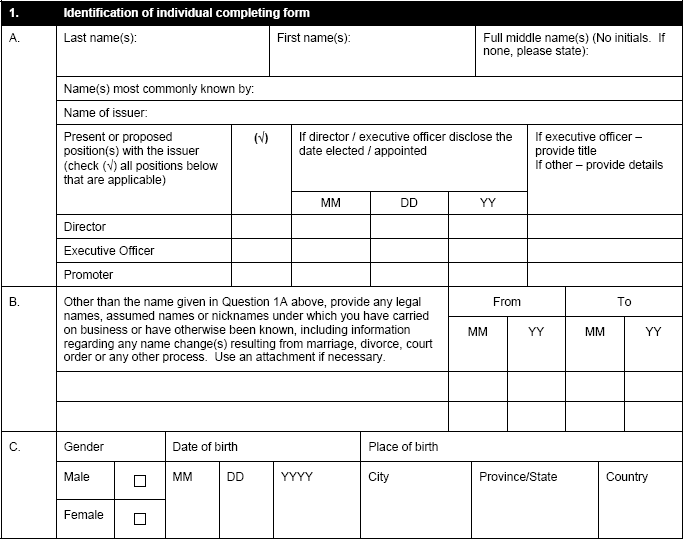

(b) obtain a personal information form from each director, executive officer and promoter of the issuer, and

(c) conduct or arrange for the following:

(i) backgrounds checks on the issuer;

(ii) criminal record and background checks on each individual referred to in paragraph (b).

(2) In respect of each individual who becomes a director, executive officer or promoter of the issuer during the distribution period, the funding portal must

(a) obtain a personal information form, and

(b) conduct or arrange for criminal record and background checks to be conducted.

Issuer access agreement

26. The issuer access agreement referred to in paragraph 25(1)(a) [Access to funding portal] must include all of the following:

(a) confirmation that the issuer will comply with the funding portal's policies and procedures concerning information posted by issuers on the funding portal's online platform;

(b) confirmation that the information that the issuer provides to the funding portal or posts on the funding portal's online platform will only contain permitted materials that are reasonably supported, and will not contain a promotional statement, a misrepresentation or an untrue statement of a material fact or otherwise be misleading;

(c) confirmation from each of the issuer and the funding portal that each is responsible for compliance with applicable securities legislation, including compliance with this Instrument;

(d) a requirement that the funding portal must terminate any distribution and report immediately to the securities regulatory authority or regulator if, at any time during the distribution period, it appears to the funding portal that the business of the issuer is not being, or may not be, conducted with integrity;

(e) in Ontario, confirmation that the funding portal is the agent of the issuer for the purposes of a distribution under the crowdfunding prospectus exemption.

Obligation to review materials of eligible crowdfunding issuer

27.

(1) A funding portal is required to review the crowdfunding offering document, the materials referred to in subsection 12(1) [Additional distribution materials], the personal information forms, the results of the criminal record and background checks, and any other information about an issuer or a distribution made available to the funding portal or of which the funding portal is aware.

(2) If it appears to the funding portal that, based upon its review of the information and materials in subsection (1), the disclosure in the crowdfunding offering document and other materials referred to in subsection 12(1) [Additional distribution materials] is incorrect, incomplete or misleading, the funding portal must require that the issuer correct, complete or clarify the incorrect, incomplete or misleading disclosure prior to its posting on the funding portal's online platform.

Denial of issuer access and termination

28.

(1) The funding portal must not allow an issuer access to its online platform for the purposes of a distribution under the crowdfunding prospectus exemption if

(a) after reviewing the information about the issuer or the distribution made available to the funding portal or of which the funding portal is aware, the funding portal makes a good faith determination that

(i) the business of the issuer may not be conducted with integrity because of the past conduct of

(A) the issuer, or

(B) any of the issuer's directors, executive officers, or promoters,

(ii) the issuer is not complying with one or more of its obligations under this Instrument, or

(iii) the crowdfunding offering document or the materials referred to in subsection 12(1) [Additional distribution materials] contain a statement or information that constitutes a misrepresentation or an untrue statement of a material fact and the issuer has not corrected the statement or information as requested by the funding portal under section 27 [Obligation to review materials of eligible crowdfunding issuer], or

(b) the issuer or any of its directors, executive officers or promoters has pled guilty to or has been found guilty of an offence related to or has entered into a settlement agreement in a matter that involved fraud, or securities violations.

(2) A funding portal must terminate a distribution if, at any time during the distribution period, it appears to the funding portal that the business of the issuer is not being, or may not be, conducted with integrity.

Return of funds

29. A funding portal must promptly return to the purchaser all funds or assets received from a purchaser in connection with a distribution under the crowdfunding prospectus exemption if any of the following apply:

(a) the purchaser exercises its right of withdrawal;

(b) the requirements set out in section 6 [Conditions for closing of the distribution] are not met;

(c) the issuer withdraws the distribution;

(d) the distribution is otherwise terminated.

Notifications

30. If an amended crowdfunding offering document has been made available to purchasers under paragraph 7(3)(b) [Certificates], the funding portal must notify each purchaser that entered into an agreement to purchase securities prior to the amended crowdfunding offering document being made available that an amended crowdfunding offering document and, if applicable, other materials referred to in subsection 12(1) [Additional distribution materials] have been made available on the funding portal's online platform.

Removal of distribution materials

31. A funding portal must remove a crowdfunding offering document and the materials referred to in subsection 12(1) [Additional distribution materials] on the earliest of the following:

(a) the end of the distribution period;

(b) the withdrawal of the distribution;

(c) the date on which the funding portal becomes aware that the crowdfunding offering document or the materials may contain a statement or information that is false, deceptive, misleading or that may constitute a misrepresentation or untrue statement of a material fact.

Monitoring purchaser communications

32. If a funding portal establishes an online communication channel through which purchasers may communicate with one another and with the eligible crowdfunding issuer about a distribution, the funding portal must monitor postings and remove any statement by, or information from, the issuer that is inconsistent with the crowdfunding offering document or is not in compliance with this Instrument.

Online platform acknowledgement

33. Prior to allowing a person or company entry to its online platform, a funding portal must require the person or company to acknowledge all of the following:

(a) that a distribution posted on the funding portal's online platform

(i) has not been reviewed or approved in any way by a securities regulatory authority or regulator, and

(ii) is risky and may result in the loss of all or most of an investment;

(b) that the person or company may receive limited ongoing information about an issuer or an investment made through the funding portal;

(c) that the person or company is entering an online platform operated by a funding portal that

(i) is registered in the category of restricted dealer subject to the terms and conditions of this Instrument, and will not provide advice about the suitability of the purchase of the security, or

(ii) is registered in the category of investment dealer or exempt market dealer, and is required to provide advice about the suitability of the purchase of the security.

Purchaser requirements prior to purchase

34. Prior to a purchaser entering into an agreement to purchase securities under the crowdfunding prospectus exemption, a funding portal must

(a) obtain from the purchaser a risk acknowledgement form where the purchaser positively confirms having read and understood the risk warnings and the information in the crowdfunding offering document,

(b) except in Ontario, confirm and validate that the purchaser is an accredited investor if the acquisition cost is greater than $2,500, and

(c) in Ontario, obtain from the purchaser, and validate, a confirmation of investment limits form.

Required online platform disclosure

35. A funding portal must include on its online platform prominent disclosure of all compensation, including fees, costs and other expenses that the funding portal may charge to, or impose on, an eligible crowdfunding issuer or a purchaser, and any such other disclosure that may be required under securities legislation.

Delivery to the issuer

36. On or before the closing of a distribution, the funding portal must deliver to the issuer the following:

(a) the purchase agreement entered into between the issuer and the purchaser;

(b) a risk acknowledgement form from the purchaser where the purchaser positively confirms having read and understood the risk warnings and the information in the crowdfunding offering document;

(c) except in Ontario, confirmation and validation that the purchaser is an accredited investor, if the acquisition cost is greater than $2,500;

(d) in Ontario, a confirmation of investment limits form for the purchaser.

Release of funds

37. A funding portal must not release the funds raised under the distribution to the eligible crowdfunding issuer unless the requirements set out in section 6 [Conditions for closing of the distribution] have been met.

Reporting requirements

38.

(1) A funding portal must immediately notify the securities regulatory authority or regulator in writing if, at any time during the distribution period, the funding portal terminates a distribution pursuant to subsection 28(2) [Denial of issuer access and termination].

(2) A funding portal must deliver to the securities regulatory authority or regulator, in a format acceptable to the securities regulatory authority or regulator, within 30 days of the end of the second and fourth quarters of its financial year, a report containing the following information for the immediately preceding two quarters:

(a) each distribution through the funding portal, including the name of the issuer, the type of security, the amount of the distribution, the industry of the issuer and the number of purchasers participating in the distribution;

(b) the name and industry of each issuer denied access to the funding portal and the reason for the denial;

(c) the name and industry of each issuer

(i) that was granted access to the funding portal but the distribution did not close and the reason the distribution did not close, or

(ii) that was granted access to the funding portal but was subsequently removed from the funding portal and the reason for removal;

(d) such other information as a securities regulatory authority or regulator may reasonably request.

Division 3: Additional requirements, restricted dealer funding portal

Prohibition on providing recommendations or advice

39. A restricted dealer funding portal and a registered individual of the restricted dealer funding portal must not, directly or indirectly, provide a recommendation or advice to a purchaser

(a) to purchase securities under the crowdfunding prospectus exemption or in connection with any other trade in a security, or

(b) to use borrowed money to finance any part of a purchase of securities under the crowdfunding prospectus exemption or in connection with any other trade in a security.

Restriction on referral arrangements

40.

(1) A restricted dealer funding portal must not participate in a referral arrangement.

(2) Despite subsection (1), a funding portal may compensate a third party for referring an issuer to the funding portal.

Permitted dealing activities

41. A restricted dealer funding portal and a registered individual of the restricted dealer funding portal may only act as intermediaries in connection with

(a) a distribution of securities made in reliance on the crowdfunding prospectus exemption, and