Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

CSA Notice and Request for Comment - Mandating a Summary Disclosure Document for Exchange-Traded Mutual Funds and Its Delivery - Proposed Amendments to NI 41-101 General Prospectus Requirements and to Companion Policy 41-101CP to NI 41-101 General Prospec

CSA Notice and Request for Comment - Mandating a Summary Disclosure Document for Exchange-Traded Mutual Funds and Its Delivery - Proposed Amendments to NI 41-101 General Prospectus Requirements and to Companion Policy 41-101CP to NI 41-101 General Prospec

CSA NOTICE AND REQUEST FOR COMMENT

MANDATING A SUMMARY DISCLOSURE DOCUMENT

FOR EXCHANGE-TRADED MUTUAL FUNDS AND ITS DELIVERY

PROPOSED AMENDMENTS TO

NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS

AND TO

COMPANION POLICY 41-101CP TO

NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS

AND

RELATED CONSEQUENTIAL AMENDMENTS

June 18, 2015

Introduction

The Canadian Securities Administrators (the CSA or we) are publishing for a comment period of 90 days proposed amendments to National Instrument 41-101 General Prospectus Requirements (the Rule), Companion Policy 41-101CP to National Instrument 41-101 General Prospectus Requirements (the Companion Policy) and related consequential amendments to National Instrument 81-106 Investment Fund Continuous Disclosure and Companion Policy 81-106CP to National Instrument 81-106 Investment Fund Continuous Disclosure (the Consequential Amendments). New Form 41-101F4 Information Required in an ETF Facts Document (Form 41-101F4) is part of the Rule. We refer to the proposed amendments to the Rule, the proposed changes to the Companion Policy and the Consequential Amendments together as the Proposed Amendments.

The Proposed Amendments are part of Stage 3 of the CSA's implementation of the point of sale disclosure project (the POS Project).

The Proposed Amendments will require mutual funds in continuous distribution, the securities of which are listed and traded on an exchange or an alternative trading system (ETFs), to produce and file a summary disclosure document called "ETF Facts", which must be made available on the ETF's or the ETF manager's website. The Proposed Amendments also introduce a new delivery regime which will require dealers that receive an order to purchase ETF securities to deliver an ETF Facts to investors within two days of the purchase. Delivery of the prospectus will not be required, but there will be a requirement for the prospectus to be made available to investors upon request, at no cost.

We think the introduction of the ETF Facts will help provide investors with access to key information about an ETF, in language they can easily understand. Delivery of the ETF Facts to investors will also help improve the consistency with which disclosure is provided to investors of ETFs, and help create a more consistent disclosure framework between conventional mutual funds and ETFs. Implementation of this initiative is also responsive to comments received throughout the course of the POS Project, from both industry and investor stakeholders, regarding the need to ensure greater consistency in terms of the disclosure regime for conventional mutual funds and ETFs, which are generally both sold to retail investors.

The text of the Proposed Amendments follows this Notice and is available on the websites of members of the CSA.

We expect the Proposed Amendments to be adopted in each jurisdiction of Canada. Some jurisdictions may need to seek legislative amendments, which will need to be enacted prior to implementing the Proposed Amendments.{1}

Background

CSA Staff Notice 81-319 Status Report on the Implementation of Point of Sale Disclosure for Mutual Funds{2} outlined the CSA's decision to implement the POS Project in three stages.

With the publication of final amendments on December 11, 2014, the POS Project for conventional mutual funds is now complete. Since July 2011, every mutual fund has been required to prepare a fund facts document{3} (Fund Facts) for each class and series. Since June 2014, every dealer has been required to deliver the Fund Facts instead of the prospectus in connection with the purchase of mutual fund securities. On May 30, 2016, dealers will be required to deliver the Fund Facts at or before the point of sale.

As part of final stage of the POS Project, two concurrent workstreams are under way:

1. ETF summary disclosure document and a new delivery model -- The Proposed Amendments will require the filing of an ETF Facts and delivery of the ETF Facts within two days of an investor purchasing securities of an ETF; and

2. CSA risk classification methodology -- The CSA is currently developing a CSA risk classification methodology to be applied in determining a fund's investment risk level on the scale in the Fund Facts and, now, the ETF Facts. CSA Notice 81-324 and Request for Comment on Proposed CSA Mutual Fund Risk Classification Methodology for Use in Fund Facts was published for comment on December 12, 2013. A status update{4} was published on January 29, 2015.

The ETF Distribution Model

The Proposed Amendments recognize the differences in the distribution model for ETFs and conventional mutual funds. In particular, unlike mutual funds, individual investors seeking to purchase an ETF generally cannot subscribe directly for ETF securities. Instead, they must purchase ETF securities over an exchange. In addition, unlike conventional mutual funds where each purchase results in a distribution, in the case of ETFs, a purchase results in a distribution only when it is a trade in securities of the ETF that have not been previously issued (the Creation Units).

Since the prospectus delivery requirement under securities legislation is triggered by a distribution, prospectus delivery would generally only apply to an investor's purchase if the order is filled with Creation Units. Creation Units are issued by ETFs to dealers that are authorized to purchase newly issued securities directly from the ETF. The dealers, in turn, re-sell these Creation Units on an exchange.{5}

The first re-sale of a Creation Unit on an exchange or another marketplace in Canada will generally constitute a distribution. If, however, the ETF investor's purchase order is filled through a secondary market trade of previously issued existing ETF securities, the prospectus delivery requirement would not apply. This means that investors who purchase ETF securities that are trading in the secondary market may not be entitled to receive a prospectus under securities legislation unless they specifically request it.

Exemptive Relief and the Delivery of an ETF Summary Disclosure Document

To deal with issues arising from the ETF distribution model, in Fall 2013, the CSA granted exemptive relief (the Exemptive Relief) to ETF managers and a group of dealers from the existing prospectus delivery requirements under securities legislation in order to permit the delivery of a summary disclosure document (Summary Document) in place of the prospectus.{6}

The Exemptive Relief requires dealers that are parties to the relief to deliver to investors a Summary Document within two days of the investor buying an ETF, whether or not the investor's purchase order is filled with Creation Units.{7} This delivery obligation applies to dealers acting as agents of the purchaser on the "buy" side of the transaction, rather than to dealers acting in a distribution on the "sell" side of the transaction, as currently required under securities legislation.

The Proposed Amendments, along with related legislative amendments, codify the concepts of the Exemptive Relief, to make it applicable to all dealers who act as agent of the purchaser of an ETF security.

Substance and Purpose

Consistent with the principles of the POS Project, we think the Proposed Amendments will provide investors with the opportunity to make more informed investment decisions, by giving investors access to key information about an ETF, in language they can easily understand.{8} Furthermore, investors in conventional mutual funds and ETFs will be treated more equally with respect to the disclosure available in connection with a purchase of securities.

The proposed ETF Facts has been tested with investors and the content of the ETF Facts is informed by the results of the testing. The ETF Facts will allow investors to review key information about the potential benefits, risks and costs of investing in an ETF in an accessible format. It also highlights for investors where they can find further information about an ETF. We encourage advisors and investors to use ETF Facts as a tool in their conversations.

As was the case with the Exemptive Relief, the Proposed Amendments recognize the differences in the current ETF distribution model. In particular, as outlined above:

• not all ETF purchases are distributions;

• the dealer on the "sell" side of an ETF trade may not be able to readily discern whether a particular ETF trade is a distribution;

• there may be different dealers on the "sell" side and "buy" side of an ETF trade;

• the dealer on the "sell" side of an ETF trade that is a distribution cannot readily identify the purchaser over the exchange; and

• the dealer on the "buy" side of an ETF trade that is a distribution is not subject to the delivery obligation if it acts solely for the purchaser.

Summary of the Proposed Amendments

Application

The Proposed Amendments apply only to ETFs.

ETF Facts

The creation of a summary disclosure document that highlights key information that is important for investors to consider when they purchase an investment product has been a central component of the POS Project. As was the case for the Fund Facts, the ETF Facts is a critical element of the new delivery regime that is being proposed for ETFs.

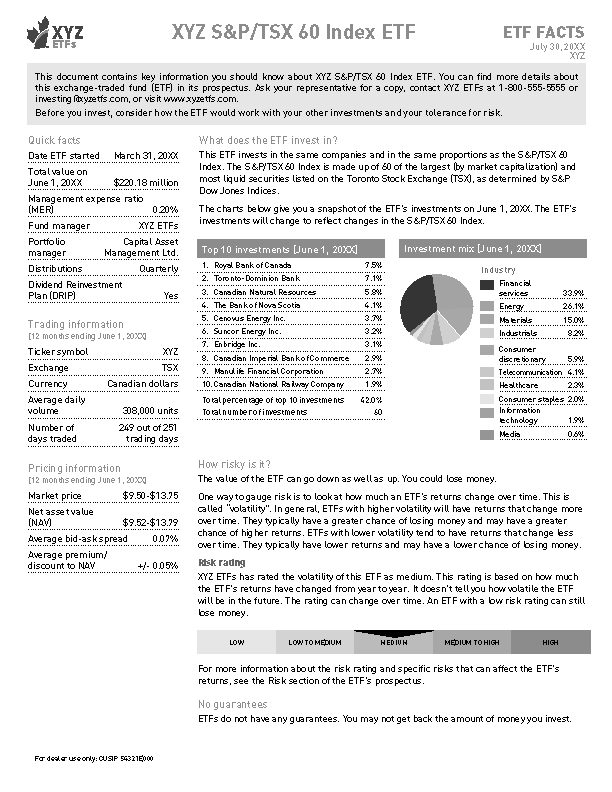

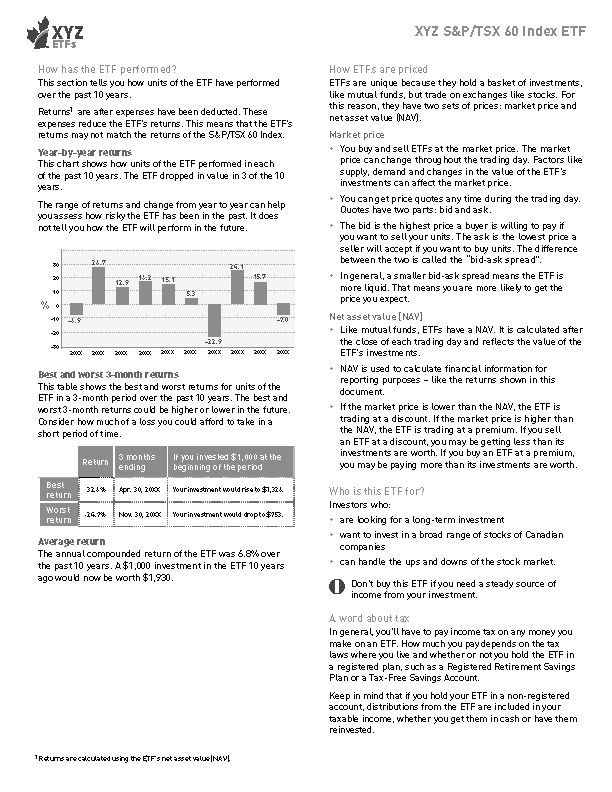

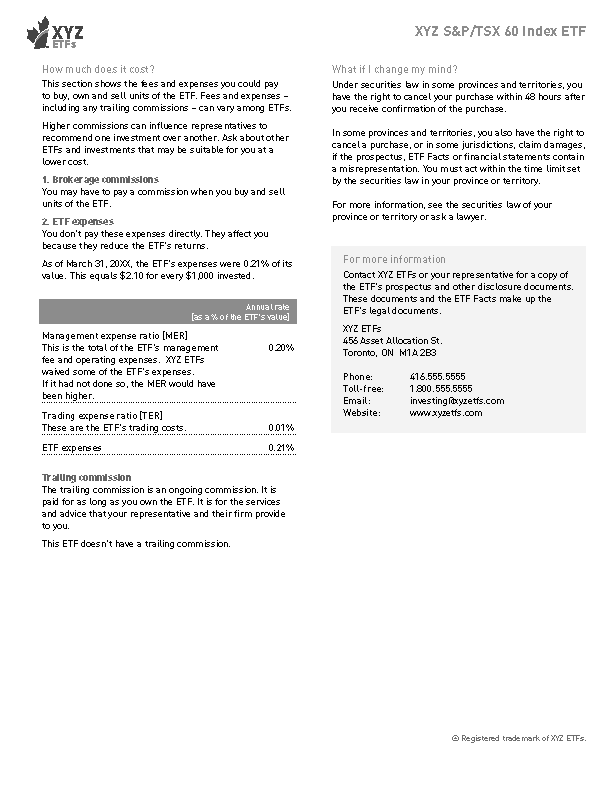

The starting point for the development of the ETF Facts was the Fund Facts, which was the result of extensive research, consultation and testing. Like the Fund Facts, the ETF Facts is required to be in plain language, no more than two pages double-sided and highlights key information that is important to investors, including risks, past performance, and the costs of investing in an ETF.

Although ETFs are substantially similar to conventional mutual funds, they are different in one significant aspect. Individual investors cannot subscribe for ETF securities directly from the fund. Instead, ETF securities are bought and sold over an exchange like stocks. Therefore, we have included additional content in the ETF Facts that speaks to trading and pricing characteristics of ETFs. For example, we have proposed the inclusion of information related to market price, bid-ask spread, as well as premium/discount of market price to net asset value. We have also proposed the inclusion of content that explains some of the pricing issues to consider when trading ETFs.

The form requirements for the ETF Facts are set out in the Proposed Amendments as Form 41-101F4. A separate ETF Facts is required for each class or series of securities of an ETF. For illustrative purposes, a sample ETF Facts is set out as Annex A to this Notice.

- - - - - - - - - - - - - - - - - - - -

The CSA is developing a CSA risk classification methodology for use in the Fund Facts and the ETF Facts. Once implemented, it is anticipated that the "risk rating" currently proposed in the ETF Facts will be determined according to the CSA risk classification methodology

- - - - - - - - - - - - - - - - - - - -

Please see Annex B to this Notice which sets out some specific issues for comment relating to the specific content of the ETF Facts.

Testing of the ETF Facts

The CSA tested the proposed ETF Facts with investors during Summer/Fall 2014 using Allen Research Corporation of Toronto, Ontario.

The research was conducted in two phases: (1) qualitative research conducted through 28 one-on-one in-depth interviews and (2) quantitative research conducted through an online questionnaire with 533 retail investors, including 348 ETF investors. The ETF Facts was tested both in English and French.

The testing showed that investors generally find the ETF Facts contains important information, and that it is expressed in easy-to-read language. Other key findings included:

• investors generally considered the ETF Facts to be a useful document and were committed to using it as a major component of their decision-making process for ETF investing;

• investors generally understood the terms "currency", "exchange", "average daily volume" and "total value" in the "Trading information" section;

• investors generally did not understand that ETFs have both a market price and a "NAV";

• investors found it hard to understand the concepts "bid-ask spread" and "premium and discount" in the "Trading ETFs" section and asked for examples;

• investors did not understand "CUSIP" in the "Trading information" section; and

• investors wanted to know about the trailing commission even if the trailing commission is zero.

The results of this testing helped to inform the content of the proposed ETF Facts form requirements in the Proposed Amendments. The following changes to the proposed ETF Facts were made in response to the testing results:

• the "Trading ETFs" section is replaced with the "How ETFs are priced" section, which describes the concepts of "market price" versus "NAV" with respect to pricing of ETFs;

• in the "How ETFs are priced" section, the concepts of "bid-ask spread" and "premium and discount" are discussed in the context of how ETFs are priced;

• metrics for "market price", "NAV", "average bid-ask spread" and "average premium/discount to NAV" are added to illustrate each of these concepts under a new "Pricing information" section;

• CUSIP is now identified as "for dealer use only" and moved out of the "Trading Information" section; and

• an explanation of "trailing commission" is added, which is consistent with the Fund Facts.

The final report, "CSA Point of Sale Disclosure Project: ETF Facts Document Testing," is available on the websites of the Ontario Securities Commission and the Autorité des marchés financiers at www.osc.gov.on.ca and www.lautorite.qc.ca, respectively. Copies are also available from any CSA member.

Filing Requirements

Consistent with the Exemptive Relief, the ETF Facts must be filed concurrently with the ETF's prospectus. The certificate page for the ETF, which verifies the disclosure in the prospectus, applies to the ETF Facts just as it applies to all documents incorporated by reference into the prospectus.

If a material change to the ETF relates to a matter that requires a change to the disclosure in the ETF Facts, an amendment to the ETF Facts must be filed. If ETF managers want to update information in the ETF Facts at their discretion, they may choose to amend the ETF Facts at any time. In all instances, an amendment to an ETF Facts must be accompanied by an amendment to the ETF's prospectus. In cases where the ETF prospectus would not have any changes, it would be sufficient to simply file an updated certificate page.

Any ETF Facts filed after the date of the prospectus is intended to supersede the ETF Facts previously filed. Once filed, the ETF Facts must be posted to the ETF's or the ETF manager's website.

Delivery of the ETF Facts Instead of the Prospectus

The Proposed Amendments require delivery of the most recently filed ETF Facts to a purchaser within two days of purchase of ETF securities, pursuant to the proposed delivery requirement. The proposed delivery requirement shifts the current prospectus delivery obligation under securities legislation from the dealer acting as underwriter in an ETF distribution (the "sell" side of an ETF transaction) to the dealer when acting as agent of the purchaser of an ETF security (the "buy" side of an ETF transaction). The proposed delivery requirement also provides a carve-out from the existing prospectus delivery requirement for ETF securities.

Under the Exemptive Relief, a Summary Document is being delivered to investors that are clients of dealers that account for approximately 80% of all ETF assets under management held by retail investors in Canada today.{9} Implementation of the Proposed Amendments means that all investors, including those that are not clients of dealers that are parties to the Exemptive Relief, would receive an ETF Facts within two days of purchase.

Consistent with securities legislation in some jurisdictions today, the Proposed Amendments do not require delivery of the ETF Facts if the purchaser has already received the most recently filed ETF Facts.

The Proposed Amendments will restrict the documents that may be combined with the ETF Facts on delivery.

We have not made any changes to an ETF's obligation to file its prospectus. There will be a requirement to provide investors with a copy of the prospectus upon request, at no cost.

The delivery requirement in the Proposed Amendments is drafted to reflect current differences in the legislative authority of members of the CSA. While drafting may differ among the members of the CSA, each jurisdiction will achieve the same outcome of requiring delivery of the ETF Facts to ETF investors within 2 days of purchase. Prior to implementing the Proposed Amendments, legislative amendments may be sought and enacted in some jurisdictions to achieve a harmonized provision.

The method for delivery of the ETF Facts is expected to be consistent with the method for delivery of a prospectus under securities legislation. For example, it could be in person, by mail, by fax, electronically or by other means. Access will not equal delivery, nor will a referral to the website on which the ETF Facts is posted.

Investor Rights

Right for failure to deliver the ETF Facts

If the investor does not receive the ETF Facts, the investor has a right to seek damages or to rescind the purchase. The rights of the investor for failure of delivery of the ETF Facts will be enacted by legislative amendments and will be consistent with the rights under securities legislation today for failure to deliver the prospectus within two days of purchasing securities of an ETF.

Right for withdrawal of purchase

The Proposed Amendments do not extend the current right of withdrawal of purchase to investors of ETF securities. Currently, under securities legislation, investors have a right for withdrawal of purchase within two business days after receiving the prospectus. This right only applies in respect of a distribution for which prospectus delivery is required. As indicated, not all ETF purchases are distributions. Only purchase orders filled with Creation Units trigger a prospectus delivery requirement and would therefore also be subject to a withdrawal right. As a result, this right does not today apply to all ETF investors, nor is there a way for an ETF investor today to know whether they have received Creation Units and are therefore eligible for a withdrawal right.

In some jurisdictions, investors have a right of rescission with delivery of the trade confirmation for the purchase of mutual fund securities, including ETF securities.{10} This right remains unchanged under the Proposed Amendments.

Please see Annex B to this Notice which sets out specific issues for comment relating to this approach.

Right for misrepresentation

The ETF Facts is incorporated by reference into the prospectus. This means that the existing statutory rights of investors that apply for misrepresentations in a prospectus will also apply to misrepresentations in the ETF Facts. Furthermore, as most ETF purchases occur on the secondary market, investors may also have a right of action for civil liability for secondary market disclosure.

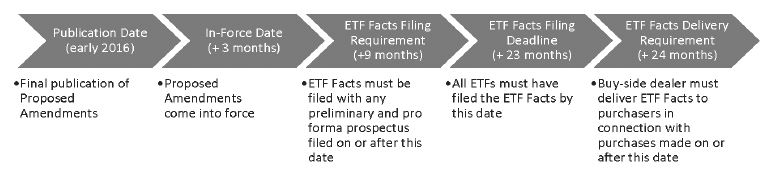

Transition

The Proposed Amendments have two transition periods. The first relates to the requirement for ETF managers to file and make available an ETF Facts for each class or series of securities of the ETF (the ETF Facts Filing Requirement). The second relates to the requirement for dealers to deliver an ETF Facts in connection with a purchase of an ETF security (the ETF Facts Delivery Requirement).

Subject to the nature of comments received, as well as the rule approval process, we anticipate publishing final rules aimed at implementing the Proposed Amendments in early 2016 (the Publication Date). We anticipate the Proposed Amendments will be proclaimed into force three months after the Publication Date (the In-Force Date).

The proposed transition period timeline in the Proposed Amendments is illustrated below:

ETF Facts Filing Requirement

We are proposing the ETF Facts Filing Requirement would take effect 9 months after the Publication Date (the ETF Facts Effective Date) of the Proposed Amendments in final form. This means that ETF managers will have 6 months from the In-Force Date to make any changes to compliance and operational systems that are necessary to produce the ETF Facts.

As of the ETF Facts Effective Date, an ETF that files a preliminary or pro forma prospectus must concurrently file an ETF Facts for each class or series of securities of the ETF offered under the prospectus and post the ETF Facts to the ETF's or ETF manager's website. Until such time, ETF managers that are subject to the Exemptive Relief will continue to prepare and file the Summary Document.

In order to fully implement the Proposed Amendments within a reasonable time period, we propose that an ETF manager must, if it has not already done so, file an ETF Facts for each class or series of securities of the ETF within 14 months of the ETF Facts Effective Date. Based on the prospectus renewal cycle for ETFs, we anticipate that it would take approximately 13 months for ETF Facts to be filed for all ETFs. This final deadline date, however, will ensure that ETF Facts for all ETFs will be available prior to implementation of the ETF Facts Delivery Requirement.

ETF Facts Delivery Requirement

We are proposing the ETF Facts Delivery Requirement would take effect 24 months after the Publication Date (the Delivery Effective Date).

This means that dealers that are subject to Exemptive Relief will be required to deliver either the most recently filed ETF Facts, or until the initial ETF Facts is filed, the most recently filed Summary Document. The sunset provisions of the Exemptive Relief will generally expire by the end of the transition period for the Proposed Amendments. We do not anticipate that there will be any significant issues related to the transition from the delivery of the Summary Document to delivery of the ETF Facts.

Dealers that are not subject to the Exemptive Relief will have 21 months from the In-Force Date to make any changes to compliance and operational systems that are necessary to effect ETF Facts delivery.

Please see Annex B to this Notice which sets out some specific issues for comment relating to the two transition periods.

Anticipated Costs and Benefits

Similar to the delivery of Fund Facts for mutual funds, we think delivery of the ETF Facts, as set out in the Proposed Amendments, would benefit both investors and market participants by helping address the "information asymmetry" that exists between participants in the ETF industry and investors. Unlike industry participants, investors often do not have key information about an ETF and may not know where to find the information. We also know that many investors do not use the information in the prospectus because they have trouble finding and understanding the information they need. The CSA designed the ETF Facts to make it easier for investors to find and use key information, which should help bridge this information gap.

The earlier publications related to the POS Project outlined some of the anticipated costs and benefits of implementation of the point of sale disclosure regime for mutual funds. We consider the costs and benefits set out in prior publications to still be valid and we consider them to be equally applicable to ETFs.{11} You can find these documents on the websites of members of the CSA.

Overall, we continue to believe that the potential benefits of the changes to the disclosure regime for ETFs as contemplated by the Proposed Amendments are proportionate to the costs of making them.

Benefits

As stated throughout the POS Project, the benefits of a more effective disclosure regime can be subtle and difficult to measure. It is difficult to quantify the value of investors having the opportunity to make more informed investment decisions. Research suggests that certain behavioral biases of investors may impact the effectiveness of policy initiatives that are designed to encourage better choices about financial products. However, research on investor preferences for mutual fund information, including our own testing of the Fund Facts and ETF Facts, indicates investors prefer a concise summary of the information that they can use to make a decision. The Proposed Amendments would also improve the consistency with which disclosure is provided to investors of ETFs and help create a more consistent disclosure framework between conventional mutual funds and ETFs.

Some anticipated benefits of delivery of the ETF Facts include:

• less risk of investors buying inappropriate products;

• investors being in a position to better understand, discuss, and compare one ETF to another, particularly the costs of investing in the ETFs;

• greater transparency in areas such as charges and commissions, which may enhance the overall efficiency of the market; and

• investors becoming better informed overall, which reinforces investor confidence in ETFs.

Costs

We think the costs of a new disclosure regime for ETFs fall into two main categories: the one-time costs of change in moving to the new regime and the ongoing costs of maintaining the new system, in comparison with the cost of the existing regime.

We anticipate that costs to industry stakeholders will fall into the following general categories:

• preparation of the ETF Facts;

• reprogramming and updating information delivery systems;

• regulatory filings; and

• compliance and staff costs in overseeing and maintaining the delivery regime.

As all ETF managers already prepare and file a Summary Document pursuant to the Exemptive Relief, we think the costs to prepare the ETF Facts will be incremental in nature and the costs for regulatory filings of the ETF Facts will be more or less the same.

For the dealers that already deliver a Summary Document to ETF investors under the Exemptive Relief, we think delivery systems are already in place and the compliance and staff costs in overseeing and maintaining the delivery regime should be more or less the same.

For the dealers that are not parties to the Exemptive Relief, we think there will be one-time costs to reprogram and update information delivery systems and ongoing costs relating to compliance and staff to oversee and maintain the delivery regime. However, there are a number of third party service providers that have expertise in creating automated programs and applications for delivery of disclosure documents. To the extent that affected dealers already have systems in place to accommodate post-sale delivery of the Fund Facts, it may also be possible for those dealers to leverage those existing systems to implement delivery of the ETF Facts. For these dealers, we request specific data on the anticipated costs of delivering the ETF Facts.

Please see Annex B to this Notice which sets out some specific issues for comment relating to the anticipated costs and benefits of the Proposed Amendments.

Local Matters

Annex G to this Notice is being published in any local jurisdiction that is making related changes to local securities laws, including local notices or other policy instruments in that jurisdiction. It also includes any additional information that is relevant to that jurisdiction only.

Some jurisdictions may require amendments to local securities legislation, in order to implement the Proposed Amendments. If statutory amendments are necessary in a jurisdiction, these changes will be initiated and published by the local provincial or territorial government.

Unpublished Materials

In developing the Proposed Amendments, we have not relied on any significant unpublished study, report or other written materials.

Request for Comments

We welcome your comments on the Proposed Amendments. To allow for sufficient review, we are providing you with 90 days to comment. In addition to any general comments you may have, we also invite responses to the specific questions for comment identified in Annex B to this Notice.

We cannot keep submissions confidential because securities legislation in certain provinces requires publication of a summary of the written comments received during the comment period.

Please submit your comments in writing on or before September 16, 2015. If you are not sending your comments by email, please send a CD containing your submissions (in Microsoft Word format).

Where to Send Your Comments

Address your submission to all of the CSA as follows:

British Columbia Securities CommissionAlberta Securities CommissionFinancial and Consumer Affairs Authority of SaskatchewanManitoba Securities CommissionOntario Securities CommissionAutorité des marchés financiersFinancial and Consumer Services Commission (New Brunswick)Office of the Superintendent of Securities, Prince Edward IslandNova Scotia Securities CommissionOffice of the Superintendent of Securities, Newfoundland and LabradorOffice of the Superintendent of Securities, Northwest TerritoriesOffice of the Yukon Superintendent of SecuritiesOffice of the Superintendent of Securities, Nunavut

Deliver your comments only to the addresses below. Your comments will be distributed to the other participating CSA members.

The Secretary

Ontario Securities Commission

20 Queen Street West

22nd Floor

Toronto, Ontario M5H 3S8

Fax: 416-593-2318

Me Anne-Marie Beaudoin

Corporate Secretary

Autorité des marchés financiers

800, square Victoria, 22e étage

C.P. 246, tour de la Bourse

Montréal (Québec) H4Z 1G3

Fax : 514-864-6381

Contents of Annexes

The text of the Amendments is contained in the following annexes to this Notice and is available on the websites of members of the CSA:

Annex A

--

Sample ETF Facts Template

Annex B

--

Issues for Comment

Annex C

--

Proposed Amendments to National Instrument 41-101 General Prospectus Requirements

Annex D

--

Proposed Changes to Companion Policy 41-101CP to National Instrument 41-101 General Prospectus Requirements

Annex E

--

Proposed Amendments to National Instrument 81-106 Investment Fund Continuous Disclosure

Annex F

--

Proposed Changes to Companion Policy 81-106CP to National Instrument 81-106 Investment Fund Continuous Disclosure

Annex G

--

Local Information

Questions

Please refer your questions to any of the following:

{1} In Ontario, legislative amendments have been passed and are awaiting proclamation upon the effective date of the Proposed Amendments.

{2} Published on June 18, 2010.

{3} See Form 81-101F3 Contents of Fund Facts Document.

{4} CSA Staff Notice 81-325 Status Report on Consultation under CSA Notice 81-324 and Request for Comment on Proposed CSA Mutual Fund Risk Classification Methodology for Use in Fund Facts.

{5} This initial re-sale from a "creation unit" on an exchange would be considered a trade in the securities of an issuer that have not been previously issued and a purchase and re-sale by the dealer in the course of or incidental to a distribution.

{6} In the Matter of BMO Nesbitt Burns Inc. and BMO Investorline Inc. (July 19, 2013); In the Matter of CIBC World Markets Inc. and CIBC Investor Services Inc. (July 19, 2013); In the Matter of ITG Canada Corp. (November 18, 2014); In the Matter of National Bank Financial Inc. and National Bank Direct Brokerage Inc. (July 19, 2013); In the Matter of RBC Dominion Securities Inc. and RBC Direct Investing Inc. (July 19, 2013); In the Matter of Scotia Capital Inc. and DWM Securities Inc. (July 19, 2013); In the Matter of TD Securities Inc. and TD Waterhouse Canada Inc. (July 19, 2013); In the Matter of Timber Hill Canada Co. (November 5, 2014); In the Matter of Blackrock Asset Management Canada Limited et. al. (July 19, 2013); In the Matter of BMO Asset Management Inc. et. al. (July 19, 2013); In the Matter of First Asset Investment Management Inc. et. al. (July 19, 2013); In the Matter of FT Portfolios Canada Co. et. al. (July 19, 2013); In the Matter of Horizons ETFs Management (Canada) Inc. and AlphaPro Management Inc. et. al. (July 19, 2013); In the Matter of Invesco Canada Ltd. et. al. (July 19, 2013); In the Matter of Purpose Investments Inc. et. al. (August 6, 2013); In the Matter of Questrade Wealth Management Inc. et. al. (January 23, 2015); In the Matter of RBC Global Asset Management Inc. et. al. (July 19, 2013); and In the Matter of Vanguard Investments Canada Inc. et. al. (July 19, 2013).

{7} Similar to delivery of the Fund Facts, delivery would only be required in instances where the investor has not previously received the latest Summary Document of the ETF.

{8} This is consistent with the International Organization of Securities Commission (IOSCO) Principles on Point of Sale Disclosure published in February 2011. See, for example: Principles on Point of Sale Disclosure, Final Report, Technical Committee of the IOSCO, February 2011; G20 High-level principles on Financial consumer protection, Organization for Economic Co-operation and Development (OECD), October 2011; and Regulation of Retail Structured Products, Consultation Report, IOSCO, April 2013.

Principle 2 of the IOSCO Principles on Point of Sale Disclosure specifies: "key information should be delivered, or made available, for free, to an investor before the point of sale, so that the investor has the opportunity to consider the information and make an informed decision about whether to invest."

{9} Source: Investor Economics.

{10} See for example section 137 of the Securities Act (Ontario). In Ontario, this right only applies in respect of purchases that are less than $50,000. An investor that exercises this right is entitled to receive the lesser of their original investment amount and the net asset value of the shares/units at the time of exercise. The investor would also be entitled to receive all costs incurred in connection with their purchase.

{11} The costs and benefits of pre-sale delivery are not applicable as the Proposed Amendments only contemplate delivery of the ETF Facts within two days of purchase of ETF securities.

ANNEX A

SAMPLE ETF FACTS TEMPLATE

[The template follows on separately numbered pages.]

ANNEX B

ISSUES FOR COMMENT

Content of the ETF Facts

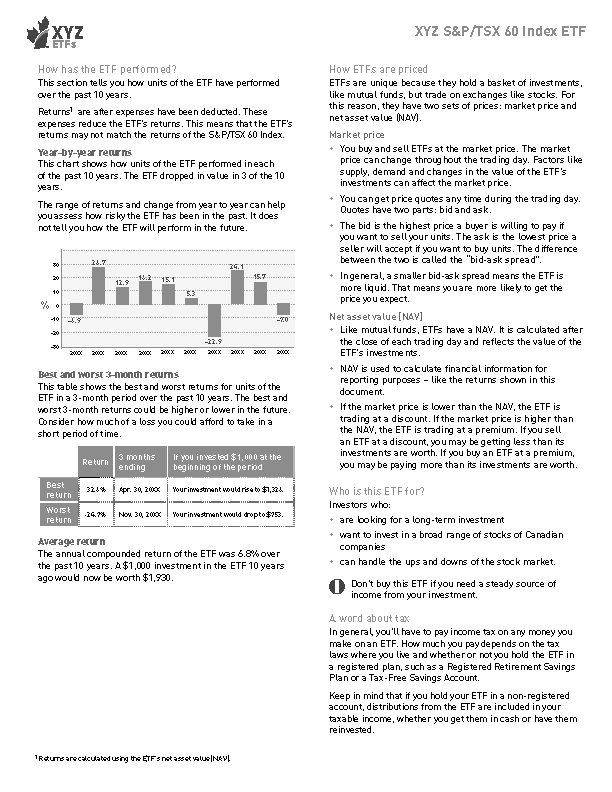

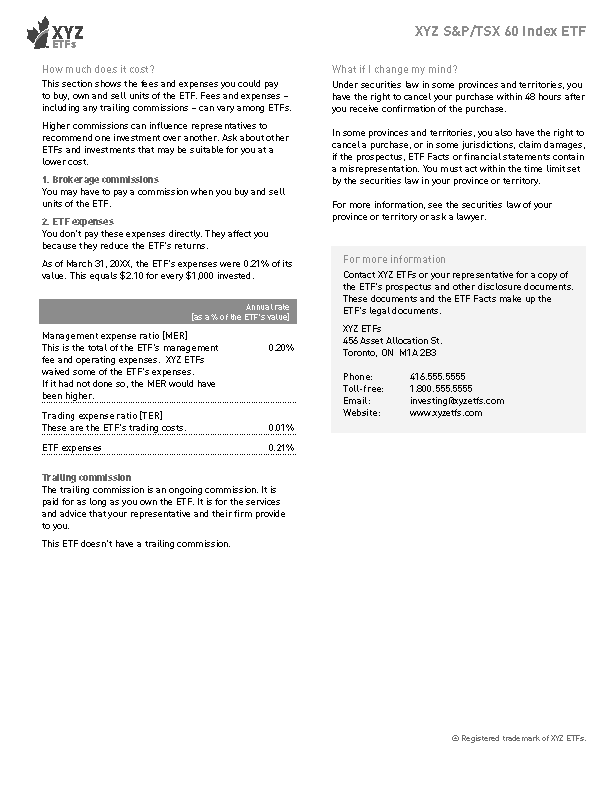

1. The ETF Facts is substantially similar to the Fund Facts, except for additional information related to trading and pricing (e.g., average daily volume, number of days traded, market price range, net asset value range, average bid-ask spread and average premium/discount to NAV). We seek specific feedback on these proposed elements of the ETF Facts. In particular, please comment on the disclosure instructions for these elements as outlined in Form 41-101F4. For example, should the range of market prices exclude odd lot trades? In terms of the calculation of the average bid-ask spread, should trading days that do not have a minimum number of quotes be excluded from the calculation? We also seek feedback on whether there are alternative methods or alternative metrics that can be used to convey this information in a more meaningful way for investors.

2. The "How ETFs are priced" section of the ETF Facts is intended to provide ETF investors with some additional information on the factors that influence trading prices and to explain the difference between market price and NAV. This section has been modified in response to investor testing, which showed that investors valued this type of information but were not necessarily aware of how to use it in practice. We seek feedback on whether there is an alternative form of presentation of this information that may better assist investors.

3. Please comment on whether there are other disclosure items/topics that should be added to reflect the differences between ETFs and conventional mutual funds.

Anticipated Costs of Delivery of the ETF Facts

4. We seek feedback on the anticipated costs of delivery of ETF Facts for those dealers who do not have Exemptive Relief and are not currently delivering ETF Facts; specifically, the anticipated one-time infrastructure costs and ongoing costs.

Transition Period

5. We seek feedback from dealers on the appropriate transition period for ETF Facts delivery under the Proposed Amendments. We are specifically interested in feedback from dealers who are not subject to the Exemptive Relief. Please comment on the feasibility of implementing the delivery requirement under the Proposed Amendments within 21 months of the date the Proposed Amendments come into force. In responding, please comment on the impact a 21 month transition period might have in terms of cost, systems implications, and potential changes to current sales practices.

6. We seek feedback from ETF managers on the appropriate transition period to file the initial ETF Facts. We currently contemplate that 6 months after the date the Proposed Amendments come into force, ETF managers will be required to file an initial ETF Facts concurrently with a preliminary or pro forma prospectus for their ETFs. Please comment on the feasibility of making the changes to compliance and operational systems that are necessary to produce the ETF Facts, instead of the summary disclosure document pursuant to the Exemptive Relief, within this timeline.

7. We seek feedback from ETF managers and dealers on whether they prefer a single switch-over date for filing the initial ETF Facts rather than following the prospectus renewal cycle as currently contemplated. The CSA implemented a single switch-over date for the Stage 2 Fund Facts, and recognize that there are challenges in doing so, especially for ETF managers, from a business planning and business cycle perspective. If a single switch-over date is preferred, are there specific months or specific periods of the year that should be avoided in terms of selecting a specific switch-over date? Please explain.

Right for Withdrawal of Purchase

8. Currently, under securities legislation, investors have a right for withdrawal of purchase within two business days after receiving the prospectus. This right only applies in respect of a distribution for which prospectus delivery is required. In the case of ETFs, today only purchases filled with Creation Units trigger a prospectus delivery requirement and are therefore subject to a withdrawal right.

Consistent with the approach taken in the Exemptive Relief, the Proposed Amendments do not extend the right of withdrawal of purchase to investors for the delivery of the ETF Facts. In some jurisdictions, investors will continue to have a right of rescission with delivery of the trade confirmation.{12}

We seek feedback on this proposed approach. Specifically, please highlight if any practical impediments exist to introducing a right of withdrawal for purchases made in the secondary market in connection with delivery of the ETF Facts, should we decide to pursue this.

{12} See footnote 10.

ANNEX C

PROPOSED AMENDMENTS TO NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS

1. National Instrument 41-101 General Prospectus Requirements is amended by this Instrument.

2. Section 1.1 is amended by adding the following definitions:

"ETF" means an exchange-traded mutual fund;

"ETF facts document" means a completed Form 41-101F4;

"exchange-traded mutual fund" means a mutual fund in continuous distribution, the securities of which are

(a) listed on an exchange, and

(b) trading on an exchange or an alternative trading system;

"Form 41-101F4" means Form 41-101F4 Information Required in an ETF Facts Document of this Instrument;

3. Subsection 1.2(6) is amended by replacing "and Form 41-101F3" with ", Form 41-101F3 and Form 41-101F4".

4. Subsection 2.1(1) is replaced with the following:

(1) Subject to subsection (2), this Instrument applies to a prospectus filed under securities legislation, a distribution of securities subject to the prospectus requirement and a purchase of securities of an ETF.

5. The Instrument is amended by adding the following Parts:

(a) PART 3B: ETF Facts Document Requirements

3B.1 Application

This Part applies only to an ETF.

3B.2 Plain language and presentation

(1) An ETF facts document must be prepared using plain language and be in a format that assists in readability and comprehension.

(2) An ETF facts document must

(a) be prepared for each class and each series of securities of an ETF in accordance with Form 41-101F4,

(b) present the items listed in the Part I section of Form 41-101F4 and the items listed in the Part II section of Form 41-101F4 in the order stipulated in those parts,

(c) use the headings and sub-headings stipulated in Form 41-101F4,

(d) contain only the information that is specifically required or permitted to be in Form 41-101F4,

(e) not incorporate any information by reference, and

(f) not exceed four pages in length.

3B.3 Preparation in the required form

Despite provisions in securities legislation relating to the presentation of the content of a prospectus, an ETF facts document for an ETF must be prepared in accordance with this Instrument.

3B.4 Websites

(1) If an ETF or the ETF's family has a website, the ETF must post to at least one of those websites an ETF facts document filed under this Part as soon as practicable and, in any event, within 10 days after the date that the document is filed.

(2) An ETF facts document posted to the website referred to in subsection (1) must

(a) be displayed in a manner that would be considered prominent to a reasonable person; and

(b) not be combined with another ETF facts document.

(3) Subsection (1) does not apply if the ETF facts document is posted to a website of the manager of the ETF in the manner required under subsection (2).

(b) PART 3C: Delivery of ETF Facts Documents for Investment Funds

3C.1 Application

This Part applies only to an ETF.

3C.2 Obligation to deliver ETF facts documents

(1) The obligation to deliver or send a prospectus under securities legislation does not apply in respect of an ETF.

(2) A dealer acting as agent for a purchaser who receives an order for the purchase of a security of an ETF must, unless the dealer has previously done so, deliver or send to the purchaser the most recently filed ETF facts document for the applicable class or series of securities of the ETF not later than midnight on the second business day after entering into the purchase of the security.

(3) In Ontario, an ETF facts document is a disclosure document prescribed under subsection 71(1.1) of the Securities Act (Ontario).

- - - - - - - - - - - - - - - - - - - -

(4) In Ontario, a security of an ETF is an investment fund security prescribed for the purposes of subsections 71(1.2) and (1.3) of the Securities Act (Ontario).

Note: In Ontario, subsections 71(1.2) and (1.3) of the Securities Act (Ontario) come into force on proclamation.

- - - - - - - - - - - - - - - - - - - -

3C.3 Combinations of ETF Facts Documents for Delivery Purposes

(1) An ETF facts document delivered or sent under section 3C.2 must not be combined with any other materials or documents including, for greater certainty, another ETF facts document, except one or more of the following:

(a) a general front cover pertaining to the package of combined materials and documents;

(b) a trade confirmation which discloses the purchase of securities of the ETF;

(c) an ETF facts document of another ETF if that ETF facts document is also being delivered or sent under section 3C.2;

(d) the prospectus of the ETF;

(e) any material or document incorporated by reference into the prospectus;

(f) an account application document;

(g) a registered tax plan application or related document.

(2) If a trade confirmation referred to in subsection (1)(b) is combined with an ETF facts document, any other disclosure documents required to be delivered or sent to satisfy a regulatory requirement for purchases listed in the trade confirmation may be combined with the ETF facts document.

(3) If an ETF facts document is combined with any of the materials or documents referred to in subsection (1), a table of contents specifying all documents must be combined with the ETF facts document, unless the only other documents combined with the ETF facts document are the general front cover permitted under paragraph (1)(a) or the trade confirmation permitted under paragraph (1)(b).

(4) If one or more ETF facts documents are combined with any of the materials or documents referred to in subsection (1), only the general front cover permitted under paragraph (1)(a), the table of contents required under subsection (3) and the trade confirmation permitted under paragraph (1)(b) may be placed in front of those ETF facts documents.

3C.4 Combinations of ETF Facts Documents for Filing Purposes

For the purposes of sections 6.2, 9.1 and 9.2, an ETF facts document may be combined with another ETF facts document in a prospectus.

- - - - - - - - - - - - - - - - - - - -

Note: Implementation of this initiative is dependent on each jurisdiction enacting the necessary legislative changes. Since the legislative model adopted may vary from jurisdiction to jurisdiction, the following provisions that have been set out in this textbox have been included for illustrative purposes and may need to be varied depending on any legislative changes that are adopted. For example, in Ontario, these provisions are not necessary because it is expected that equivalent legislative amendments will be proclaimed contemporaneously with the coming-into-force of this initiative.

3C.5 Time of receipt

(1) For the purpose of this Part, where the latest ETF facts document referred to in subsection 3C.2(2) is sent by prepaid mail, it shall be deemed conclusively to have been received in the ordinary course of mail by the person or company to whom it was addressed.

(2) Subsection (1) does not apply in Ontario.

[Note: In Ontario, the same time of receipt is reflected in an amendment to s. 71(4) of the Securities Act (Ontario) that comes into force on proclamation.]

3C.6 Dealer as agent

(1) For the purpose of this Part, a dealer acts as agent of the purchaser if the dealer is acting solely as agent of the purchaser with respect to the purchase and sale in question and has not received and has no agreement to receive compensation from or on behalf of the vendor with respect to the purchase and sale.

(2) Subsection (1) does not apply in Ontario.

[Note: In Ontario, the same agency rule is reflected in an amendment to s. 71(7) of the Securities Act (Ontario) in legislative amendments that comes into force on proclamation.]

3C.7 Purchaser's right of action for failure to deliver or send

(1) A purchaser has a right of action if an ETF facts document is not delivered or sent as required by subsection 3C.2(2), as the purchaser would otherwise have when a prospectus is not delivered or sent as required under securities legislation and, for that purpose, an ETF facts document is a prescribed document under the statutory right of action.

(2) In Alberta, instead of subsection (1), section 206 of the Securities Act (Alberta) applies.

(3) In Manitoba, instead of subsection (1), section 141.2 of the Securities Act (Manitoba) applies and the ETF facts document is a prescribed document for the purposes of section 141.2.

(4) In Ontario, instead of subsection (1), section 133 of the Securities Act (Ontario) applies.

[Note: In Ontario, the right of action is reflected in paragraph 2.1 of s. 133 of the Securities Act (Ontario) which comes into force on proclamation.

In Quebec, legislative changes are under consideration.]

- - - - - - - - - - - - - - - - - - - -

6. Section 5.2 is amended by replacing "or the amendment to the prospectus" with ", the amendment to the prospectus or the amendment to the ETF facts document".

7. Section 6.1 is amended by adding the following subsection:

(4) An amendment to an ETF facts document must be prepared in accordance with Form 41-101F4 without any further identification, and dated as of the date the ETF facts document is being amended.

8. Section 6.2 is amended by deleting "and" at the end of paragraph (c), by replacing"."at the end of paragraph (d) with ",and" and by adding the following paragraph:

(e) in the case of an ETF, if the amendment relates to information in the ETF facts document,

(i) file an amendment to the ETF facts document, and

(ii) deliver to the regulator a copy of the ETF facts document, blacklined to show changes, including text deletions, from the latest ETF facts document previously filed.

9. The Instrument is amended by adding the following section:

6.2.1 Required documents for filing an amendment to an ETF Facts -- An ETF that files an amendment to an ETF facts document must, unless section 6.2 applies,

(a) file an amendment to the corresponding prospectus, certified in accordance with Part 5,

(b) deliver to the regulator a copy of the ETF facts document, blacklined to show changes, including text deletions, from the latest ETF facts document previously filed, and

(c) file or deliver any other supporting documents required under this Instrument or other securities legislation, unless the documents originally filed or delivered are correct as of the date the amendment is filed.

10. Section 9.1 is amended:

(a) in paragraph (1)(a) by adding the following subparagraph:

(iv.2) if the issuer is an ETF, in addition to the documents filed under subparagraph (iv), an ETF facts document for each class or series of securities of the ETF;

(b) by replacing subparagraph (1)(b)(i) with the following:

(i) Blackline Copy of the Prospectus -- in the case of a pro forma prospectus, a copy of the pro forma prospectus blacklined to show changes from the latest prospectus filed;

(i.1) Blackline Copy of the ETF Facts Document -- in the case of a pro forma prospectus for an ETF, a copy of the pro forma ETF facts document for each class or series of securities of the ETF blacklined to show changes from the latest ETF facts document previously filed;

11. Section 9.2 is amended:

(a) by replacing "9.1(a)(ii)" with "9.1(1)(a)(ii)" in subparagraph (a)(ii),

(b) by replacing subparagraph (a)(iv) with the following:

(iv) Investment Fund Documents -- a copy of any document described under subparagraph 9.1(1)(a)(iv), (iv.1) or (iv.2) that has not previously been filed;

(c) by replacing "9.1(a)(v) or 9.1(a)(vi)" with "9.1(1)(a)(v) or (vi)" in clause (a)(v)(B),

(d) by replacing subparagraph (b)(i) with the following:

(i) Blackline Copy of the Prospectus -- a copy of the final long form prospectus blacklined to show changes from the preliminary or pro forma long form prospectus;

(i.1) Blackline Copy of the ETF Facts Document -- in the case of a final long form prospectus for an ETF, a copy of the ETF facts document for each class or series of securities of the ETF blacklined to show changes and the text of deletions from the preliminary or pro forma ETF facts document; and

12. The Instrument is amended by adding the following section:

15.3 Documents to be delivered or sent upon request --

(1) An ETF must deliver or send to any person or company that requests the prospectus of the ETF or any of the documents incorporated by reference into the prospectus, a copy of the prospectus or requested document.

(2) An ETF must deliver or send all documents requested under this section within three business days of receipt of the request and free of charge.

13. Form 41-101F2 Information Required in an Investment Fund Prospectus is amended

(a) by replacing item 1.15 under "Documents Incorporated by Reference" with the following:

For an investment fund in continuous distribution, state in substantially the following words:

"Additional information about the fund is available in the following documents:

• the most recently filed ETF Facts for each class or series of securities of the ETF; [insert if applicable]

• the most recently filed annual financial statements;

• any interim financial reports filed after those annual financial statements;

• the most recently filed annual management report of fund performance;

• any interim management report of fund performance filed after that annual management report of fund performance.

These documents are incorporated by reference into this prospectus which means that they legally form part of this prospectus. Please see the "Documents Incorporated by Reference" section for further details."

(b) by adding the following item:

12.2 Investment Risk Classification Methodology

For an ETF,

(a) briefly describe the methodology used by the manager for the purpose of identifying the investment risk level of the ETF as required by Item 4(2)(a) in Part I of Form 41-101F4;

(b) state how frequently the investment risk level of the ETF is reviewed; and

(c) disclose that the methodology that the manager uses to identify the investment risk level of the ETF is available on request, at no cost, by calling [toll-free/collect call telephone number] or by writing to [address].

INSTRUCTIONS:

Include a brief description of the formulas, methods or criteria used by the manager of the ETF in identifying the investment risk level of the ETF.

- - - - - - - - - - - - - - - - - - - -

Note: The CSA is currently working on the development of a CSA mutual fund risk classification methodology. Once that work is complete, we anticipate including an instruction to Form 41-101F2 regarding the use of the CSA mutual fund risk classification methodology.

- - - - - - - - - - - - - - - - - - - -

(c) by replacing the first paragraph in item 36.2 under "Mutual Funds" with the following:

If the investment fund is a mutual fund, other than an ETF, under the heading "Purchasers' Statutory Rights of Withdrawal and Rescission" include a statement in substantially the following form:

(d) by adding the following item:

36.2.1 Exchange-traded Mutual Funds

If the investment fund is an ETF, under the heading "Purchasers' Statutory Rights of Rescission" include a statement in substantially the following form:

Securities legislation in [certain of the provinces [and territories] of Canada/the Province of [insert name of local jurisdiction, if applicable]] provides purchasers with the right to withdraw from an agreement to purchase ETF securities within 48 hours after the receipt of a confirmation of a purchase of such securities. [In several of the provinces/provinces and territories], [T/t]he securities legislation further provides a purchaser with remedies for rescission [or [, in some jurisdictions,] revisions of the price or damages]] if the prospectus and any amendment contains a misrepresentation, or non-delivery of the ETF Facts, provided that the remedies for rescission [, revisions of the price or damages] are exercised by the purchaser within the time limit prescribed by the securities legislation of the purchaser's province [or territory].

The purchaser should refer to the applicable provisions of the securities legislation of the province [or territory] for the particulars of these rights or should consult with a legal adviser.

(e) by replacing item 37.1 under "Mandatory Incorporation by Reference" with the following:

37.1 Mandatory Incorporation by Reference

If the investment fund is in continuous distribution, incorporate by reference the following documents in the prospectus, by means of the following statement in substantially the following words under the heading "Documents Incorporated by Reference":

"Additional information about the fund is available in the following documents:

1. The most recently filed ETF Facts for each class or series of securities of the ETF, filed either concurrently with or after the date of the prospectus. [insert if applicable]

2. The most recently filed comparative annual financial statements of the investment fund, together with the accompanying report of the auditor.

3. Any interim financial reports of the investment fund filed after those annual financial statements.

4. The most recently filed annual management report of fund performance of the investment fund.

5. Any interim management report of fund performance of the investment fund filed after that annual management report of fund performance.

These documents are incorporated by reference into the prospectus, which means that they legally form part of this document just as if they were printed as part of this document. You can get a copy of these documents, at your request, and at no cost, by calling [toll-free/collect] [insert the toll-free telephone number or telephone number where collect calls are accepted] or from your dealer.

[If applicable] These documents are available on the [investment fund's/investment fund family's] Internet site at [insert investment fund's Internet site address], or by contacting the [investment fund/investment fund family] at [insert investment fund's /investment fund family's email address].

These documents and other information about the fund are available on the Internet at www.sedar.com."

14. The Instrument is amended by adding the following Form:

Form 41-101F4 -- Information Required in an ETF Facts Document

General Instructions:

General

(1) This Form describes the disclosure required in an ETF facts document for an ETF. Each Item of this Form outlines disclosure requirements. Instructions to help you provide this disclosure are in italic type.

(2) Terms defined in National Instrument 41-101 General Prospectus Requirements, National Instrument 81-102 Investment Funds, National Instrument 81-105 Mutual Fund Sales Practices or National Instrument 81-106 Investment Fund Continuous Disclosure and used in this Form have the meanings that they have in those national instruments.

(3) An ETF facts document must state the required information concisely and in plain language.

(4) Respond as simply and directly as is reasonably possible. Include only the information necessary for a reasonable investor to understand the fundamental and particular characteristics of the ETF.

(5) National Instrument 41-101 General Prospectus Requirements requires the ETF facts document to be presented in a format that assists in readability and comprehension. This Form does not mandate the use of a specific format or template to achieve these goals. However, ETFs must use, as appropriate, tables, captions, bullet points or other organizational techniques that assist in presenting the required disclosure clearly and concisely.

(6) This Form does not mandate the use of a specific font size or style but the text must be of a size and style that is legible. Where the ETF facts document is made available online, information must be presented in a way that enables it to be printed in a readable format.

(7) An ETF facts document can be produced in colour or in black and white, and in portrait or landscape orientation.

(8) Except as permitted by subsection (9), an ETF facts document must contain only the information that is specifically mandated or permitted by this Form. In addition, each Item must be presented in the order and under the heading or sub-heading stipulated in this Form.

(9) An ETF facts document may contain a brief explanation of a material change or a proposed fundamental change. The disclosure may be included in a textbox before Item 2 of Part I or in the most relevant section of the ETF facts document. If necessary, the ETF may provide a cross-reference to a more detailed explanation at the end of the ETF facts document.

(10) An ETF facts document must not contain design elements (e.g., graphics, photos, artwork) that detract from the information disclosed in the document.

Contents of an ETF Facts Document

(11) An ETF facts document must disclose information about only one class or series of securities of an ETF. ETFs that have more than one class or series of securities that are referable to the same portfolio of assets must prepare a separate ETF facts document for each class or series.

(12) The ETF facts document must be prepared on letter-size paper and must consist of two Parts: Part I and Part II.

(13) The ETF facts document must begin with the responses to the Items in Part I of this Form.

(14) Part I must be followed by the responses to the Items in Part II of this Form.

(15) Each of Part I and Part II must not exceed one page in length, unless the required information in any section causes the disclosure to exceed this limit. Where this is the case, an ETF facts document must not exceed a total of four pages in length.

(16) For a class or series of securities of the ETF denominated in a currency other than the Canadian dollar, identify the other currency under the heading "Quick Facts" and provide the dollar amounts in the other currency, where applicable, under the headings "How has the ETF performed?" and "How much does it cost?".

(17) For items that must be as at a date within 60 days before the date of the ETF facts document or over a period ending within 60 days before the date of the ETF facts document, the same date within 60 days before the date of the ETF facts document must be used and disclosed in the ETF facts document.

(18) An ETF must not attach or bind other documents to an ETF facts document, except those documents permitted under Part 3C of National Instrument 41-101 General Prospectus Requirements.

Consolidation of ETF Facts Document into a Multiple ETF Facts Document

(19) ETF facts documents must not be consolidated with each other to form a multiple ETF facts document, except as permitted by Part 3C of National Instrument 41-101 General Prospectus Requirements. When a multiple ETF facts document is permitted under the Instrument, an ETF must provide information about each of the ETFs described in the document on a fund-by-fund or catalogue basis and must set out for each ETF separately the information required by this Form. Each ETF facts document must start on a new page and may not share a page with another ETF facts document.

Multi-Class ETFs

20. As provided in National Instrument 81-102 Investment Funds, each section, part, class or series of a class of securities of an investment fund that is referable to a separate portfolio of assets is considered to be a separate investment fund. Those principles are applicable to this Form.

Part I -- Information about the ETF

Item 1 -- Introduction

Include at the top of the first page a heading consisting of:

(a) the title "ETF Facts";

(b) the name of the manager of the ETF;

(c) the name of the ETF to which the ETF facts document pertains;

(d) if the ETF has more than one class or series of securities, the name of the class or series described in the ETF facts document;

(e) specify the ticker symbol(s) for the class or series of securities of the ETF;

(f) the date of the document;

(g) if the final prospectus of the ETF includes textbox disclosure on the cover page, provide substantially similar textbox disclosure on the ETF facts document;

(h) a brief introduction to the document using wording substantially similar to the following:

This document contains key information you should know about [insert name of the ETF]. You can find more details about this exchange-traded fund (ETF) in its prospectus. Ask your representative for a copy, contact [insert name of the manager of the ETF] at [insert if applicable the toll-free number and email address of the manager of the ETF] or visit [insert the website of the ETF, the ETF's family or the manager of the ETF] [as applicable]; and

(i) state in bold type using wording substantially similar to the following:

Before you invest, consider how the ETF would work with your other investments and your tolerance for risk.

INSTRUCTIONS:

(1) The date for an ETF facts document that is filed with a preliminary prospectus or final prospectus must be the date of the preliminary prospectus or final prospectus, respectively. The date for an ETF facts document that is filed with a pro forma prospectus must be the date of the anticipated final prospectus. The date for an amended ETF facts document must be the date on which it is filed.

(2) If the investment objectives of the ETF are to track a multiple (positive or negative) of the daily performance of a specified underlying index or benchmark, provide textbox disclosure in bold type using wording substantially similar to the following:

This ETF is highly speculative. It uses leverage, which magnifies gains and losses. It is intended for use in daily or short-term trading strategies by sophisticated investors. If you hold this ETF for more than one day, your return could vary considerably from the ETF's daily target return. Any losses may be compounded. Don't buy this ETF if you are looking for a longer-term investment.

(3) If the investment objectives of the ETF are to track the inverse performance of a specified underlying index or benchmark, provide textbox disclosure in bold type using wording substantially similar to the following:

This ETF is highly speculative. It is intended for use in daily or short-term trading strategies by sophisticated investors. If you hold this ETF for more than one day, your return could vary considerably from the ETF's daily target return. Any losses may be compounded. Don't buy this ETF if you are looking for a longer-term investment.

(4) If the ETF is a commodity pool, and (2) or (3) do not apply, provide textbox disclosure in bold type using wording substantially similar to the following:

This ETF is a commodity pool and is highly speculative and involves a high degree of risk. You should carefully consider whether your financial condition permits you to participate in this investment. You may lose a substantial portion or even all of the money you place in the commodity pool.

Item 2 -- Quick Facts, Trading Information and Pricing Information

(1) Under the heading "Quick Facts", include disclosure in the form of the following table:

- - - - - - - - - - - - - - - - - - - -

Date ETF started

(see instruction 1)

Total value on [date]

(see instruction 2)

Management expense ratio (MER)

(see instruction 3)

Fund manager

(see instruction 4)

Portfolio manager

(see instruction 5)

Distributions

(see instruction 6)

Dividend Reinvestment Plan (DRIP)

(see instruction 7)

- - - - - - - - - - - - - - - - - - - -

(2) Under the heading "Trading Information (12 months ending [date])", include disclosure in the form of the following table:

- - - - - - - - - - - - - - - - - - - -

Ticker symbol

(see instruction 8)

Exchange

(see instruction 9)

Currency

(see instruction 10)

Average daily volume

(see instruction 11)

Number of days traded

(see instruction 12)

- - - - - - - - - - - - - - - - - - - -

(3) Under the heading "Pricing Information (12 months ending [date])", include disclosure in the form of the following table:

- - - - - - - - - - - - - - - - - - - -

Market price

(see instruction 13)

Net asset value (NAV)

(see instruction 14)

Average bid-ask spread

(see instruction 15)

Average premium/discount to NAV

(see instruction 16)

- - - - - - - - - - - - - - - - - - - -

(4) At the option of the ETF, include the Committee on Uniform Securities Identification Procedures (CUSIP) number for the class or series of securities of the ETF at the bottom of the first page by stating:

For dealer use only: CUSIP [insert CUSIP number]

INSTRUCTIONS:

(1) Use the date that the securities of the class or series of the ETF described in the ETF facts document first became available to the public.

(2) Specify the net asset value of the ETF as at a date within 60 days before the date of the ETF facts document. The amount disclosed must take into consideration all classes or series that are referable to the same portfolio of assets. For a newly established ETF, state that this information is not available because it is a new ETF.

(3) Use the management expense ratio (MER) disclosed in the most recently filed management report of fund performance for the ETF. The MER must be net of fee waivers or absorptions and, despite subsection 15.1(2) of National Instrument 81-106 Investment Fund Continuous Disclosure, need not include any additional disclosure about the waivers or absorptions. For a newly established ETF that has not yet filed a management report of fund performance, state that the MER is not available because it is a new ETF.

(4) Specify the name of the fund manager of the ETF.

(5) Specify the name of the portfolio manager of the ETF. The ETF may also name the specific individual(s) responsible for portfolio selection and if applicable, the name of the sub-advisor(s).

(6) Include disclosure under this element of the "Quick Facts" only if distributions are a fundamental feature of the ETF. Disclose the expected frequency and timing of distributions. If there is a targeted amount for distributions, the ETF may include this information.

(7) Indicate whether the class or series of securities of the ETF are eligible for a dividend reinvestment plan.

(8) Specify the ticker symbol(s) for the class or series of securities of the ETF.

(9) Specify the exchange(s) on which the class or series of securities of the ETF are listed.

(10) Specify the currency that the class or series of securities of the ETF is denominated.

(11) Show the consolidated (all trading venues) average daily trading volume of the class or series of securities of the ETF over a 12 month period ending within 60 days before the date of the ETF facts document. Include non-trading (zero volume) days in the average daily trading volume calculation. For a newly established ETF, state that this information is not available because it is a new ETF. For an ETF that has not completed 12 consecutive months, state that this information is not available because the ETF has not yet completed 12 consecutive months.

(12) Show the number of days the class or series of securities of the ETF has traded out of the total number of available trading days over a 12 month period ending within 60 days before the date of the ETF facts document. For a newly established ETF, state that this information is not available because it is a new ETF. For an ETF that has not completed 12 consecutive months, state that this information is not available because the ETF has not yet completed 12 consecutive months.

(13) Show the range for the market price of the class or series of securities of the ETF by specifying the highest and lowest prices at which the class or series of securities of the ETF have traded on all trading venues over a 12 month period ending within 60 days before the date of the ETF facts document. The dollar amounts shown under this Item may be rounded to two decimal places. For a newly established ETF, state that this information is not available because it is a new ETF. For an ETF that has not completed 12 consecutive months, state that this information is not available because the ETF has not yet completed 12 consecutive months.

(14) Show the range for the net asset value per share or unit of the class or series of securities of the ETF by specifying the highest and lowest net asset value per share or unit of the class or series of securities of the ETF over a 12 month period ending within 60 days of the date of the ETF facts document. The dollar amounts shown under this Item may be rounded to two decimal places. For a newly established ETF, state that this information is not available because it is a new ETF. For an ETF that has not completed 12 consecutive months, state that this information is not available because the ETF has not yet completed 12 consecutive months.

(15) Show the daily average bid-ask spread based on the national best bid and offer (NBBO) for the class or series of securities of the ETF over a 12 month period ending within 60 days before the date of the ETF facts document. Daily bid-ask spreads must be calculated by taking the average of the quoted spreads based on NBBO for each day the primary market or exchange for the class or series of securities of the ETF is open for trading over a 12 month period ending within 60 days of the date of the ETF facts document. Each quoted spread must be calculated by taking the difference between the national best bid and best ask price, expressed as a percentage of the midpoint of those prices. The percentages shown under this Item may be rounded to two decimal places. For a newly established ETF, state that this information is not available because it is a new ETF. For an ETF that has not completed 12 consecutive months, state that this information is not available because the ETF has not yet completed 12 consecutive months.

(16) Show the average premium/discount to NAV for the class or series of securities of the ETF over a 12 month period ending within 60 days before the date of the ETF facts document. To calculate the average premium/discount to NAV, calculate and record daily the absolute value of the percentage difference between (i) the last NBBO midpoint price quoted before the NAV per share or unit of the class or series of securities of the ETF is calculated and (ii) the NAV per share or unit of the class or series of securities of the ETF. The average of all daily absolute premium/discount to NAV must then be calculated for the 12 month period ending within 60 days before the date of the ETF facts document. The average premium/discount to NAV must be shown with a "+/-" sign preceding it. The percentages shown under this Item may be rounded to two decimal places. For a newly established ETF, state that this information is not available because it is a new ETF. For an ETF that has not completed 12 consecutive months, state that this information is not available because the ETF has not yet completed 12 consecutive months.

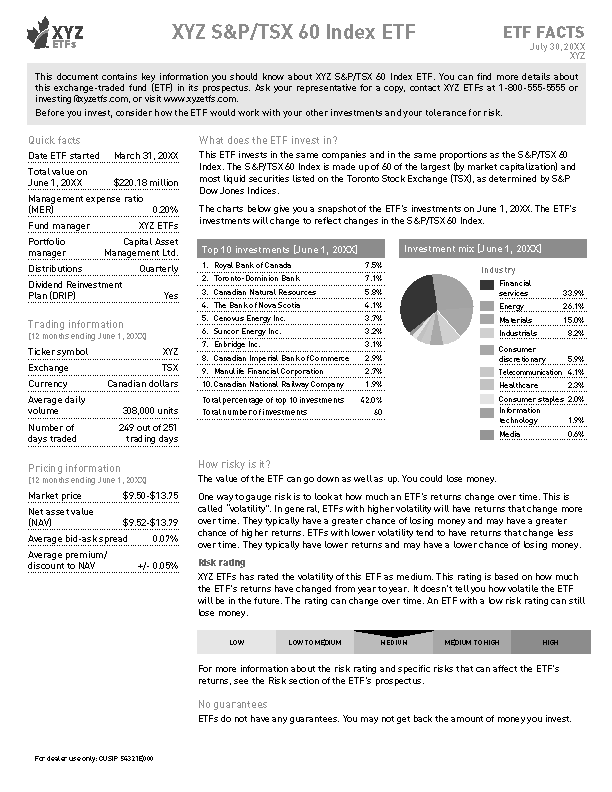

Item 3 -- Investments of the ETF

(1) Briefly set out under the heading "What does the ETF invest in?" a description of the fundamental nature of the ETF, or the fundamental features of the ETF that distinguish it from other ETFs.

(2) For an ETF that replicates an index,

(a) disclose the name or names of the permitted index or permitted indices on which the investments of the index ETF are based, and

(b) briefly describe the nature of that permitted index or those permitted indices.

(3) For an ETF that uses derivatives, state using wording substantially similar to the following:

It uses derivatives, such as options, futures and swaps, to get exposure to the [index/benchmark] without investing directly in the securities that make up the [index/benchmark].

(4) Include an introduction to the information provided in response to subsection (5) and subsection (6) using wording similar to the following:

The charts below give you a snapshot of the ETF's investments on [insert date]. The ETF's investments will change.

(5) Unless the ETF is a newly established ETF, include under the sub-heading "Top 10 investments [date]", a table disclosing the following:

(a) the top 10 positions held by the ETF, each expressed as a percentage of the net asset value of the ETF;

(b) the percentage of net asset value of the ETF represented by the top 10 positions; and

(c) the total number of positions held by the ETF.

(6) Unless the ETF is a newly established ETF, under the sub-heading "Investment mix [date]" include at least one, and up to two, charts or tables that illustrate the investment mix of the ETF's investment portfolio.

(7) For a newly established ETF, state the following under the sub-headings "Top 10 investments [date]" and "Investment mix [date]":

This information is not available because this ETF is new.

INSTRUCTIONS:

(1) Include in the information under "What does this ETF invest in?" a description of what the ETF primarily invests in, or intends to primarily invest in, or that its name implies that it will primarily invest in, such as

(a) particular types of issuers, such as foreign issuers, small capitalization issuers or issuers located in emerging market countries;

(b) particular geographic locations or industry segments; or

(c) portfolio assets other than securities.

(2) Include a particular investment strategy only if it is an essential aspect of the ETF, as evidenced by the name of the ETF or the manner in which the ETF is marketed.

(3) If an ETF's stated objective is to invest primarily in Canadian securities, specify the maximum exposure to investments in foreign markets.