Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

OSC Staff Notice: 51-721 - Forward-Looking Information Disclosure

OSC Staff Notice: 51-721 - Forward-Looking Information Disclosure

OSC Staff Notice 51-721

Forward-Looking Information Disclosure

1. Executive Summary

Forward-looking information ("FLI") is a key area of interest for investors. Investors want transparent and clear disclosure about present and future corporate operations and performance. When prepared properly, FLI can be used to enhance transparency and provide opportunities to increase an investor's understanding of a reporting issuer's business and future prospects. Staff of the Ontario Securities Commission ("we") recognize that FLI is a challenging area. Reporting issuers need to address investors' demands by providing reliable and relevant information. Disclosure must be both useful and understandable. Disclosure should include the most relevant information in a format that investors can understand.

FLI requirements have been in place for several years with the most recent changes coming into effect on December 31, 2007. We note that most reporting issuers include some FLI in either a continuous disclosure ("CD") document, a news release or on their website. We conducted FLI reviews (the "Review") of Ontario reporting issuers from several industries and the issues identified were consistent across all industries. Despite the fact that more than five years have passed since the most recent changes to the requirements, we note that for many reporting issuers there continues to be a need for improvement relating to the quality of the required FLI disclosure.

Our Review identified four common areas where improvement is needed:

• clear identification of FLI

• disclosure of the material factors or assumptions used to develop FLI

• updating previously disclosed FLI

• comparison of actual results to the future oriented financial information (FOFI) or financial outlook previously disclosed

The purpose of the Review was to assess the overall quality of FLI disclosure. This notice provides guidance and examples to assist reporting issuers in preparing FLI.

2. Introduction

FLI is a key area of interest for investors. Investors want transparent and clear disclosure about present and future corporate operations and performance. When prepared properly, FLI can be used to enhance transparency and provide opportunities to increase the investor's understanding of a reporting issuer's business and future prospects. Reporting issuers need to address investors' demands by providing reliable and relevant information in a format that investors can understand.

FLI should provide valuable insight about a reporting issuer's business and how that reporting issuer intends to attain its corporate objectives and targets. Clear, specific and relevant information allows investors to better understand the performance of a reporting issuer, enabling investors to make effective and efficient decisions in the capital markets.

Many reporting issuers find incorporating key performance indicators ("KPIs") into FLI disclosure provides investors with valuable and meaningful information about their company. Ongoing disclosure of KPIs demonstrates how a reporting issuer is progressing toward its objectives and targets. KPIs should be relevant and meaningful. Examples of KPIs include:

• customer retention

• capital expenditures

• same store sales

• exploration success rate

The purpose of this publication is to assist reporting issuers and management in understanding FLI securities requirements so that they provide more effective and relevant disclosure to investors. This notice:

• clarifies the disclosure requirements related to FLI, including FOFI and financial outlook

• provides disclosure examples

• highlights common areas of non-compliance

We reviewed the disclosure and presentation of FLI for 60 issuers, including FOFI and financial outlook, with a focus on the following main areas:

• clear identification of FLI

• disclosure of material factors and assumptions

• updating previously disclosed FLI (including expected differences)

• comparison of actual results to previously disclosed FOFI or financial outlook

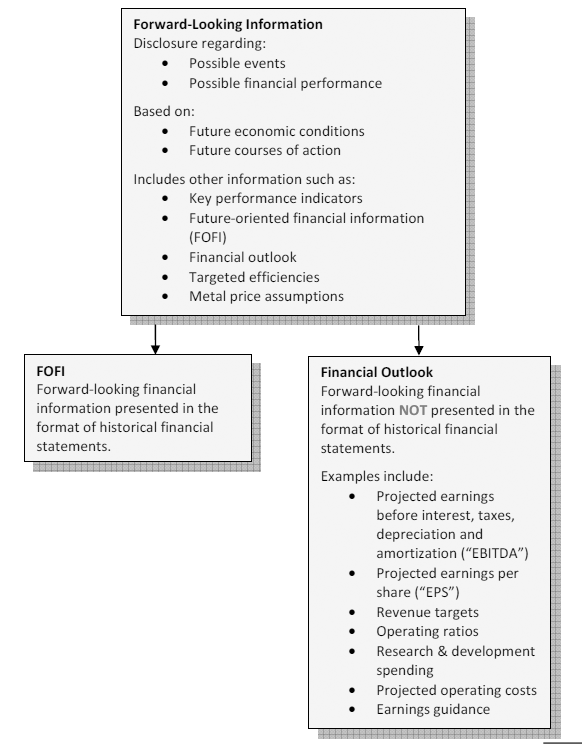

What is Forward-Looking Information?

FLI is disclosure about possible events, conditions or financial performance that is based on assumptions about future economic conditions and courses of action. FLI includes two subcategories dealing with financial information: (a) FOFI and (b) financial outlook. Both FOFI and financial outlook are FLI about prospective financial performance, financial position or cash flows, based on assumptions about future economic conditions and courses of action. The difference between FOFI and financial outlook is the format in which the financial information is presented. In the case of FOFI, the information is presented in the format of a historical financial statement. Examples are provided in the chart below.

3. Requirements

Disclosure of FLI is not mandatory for reporting issuers. However, we recognize that many reporting issuers provide FLI, generally, in news releases, management's discussion and analysis ("MD&A"), annual information forms, marketing materials or on their website. FLI is by definition likely to be less reliable than historical information because it is based on management's best judgment and assumptions on how future trends will impact their business. As such, it is important that FLI be clearly identified so that readers understand the limitation of this information, are not confused and don't treat FLI as historical information. Further, it is critical that readers understand the basis on which the FLI was determined. This basis must be reasonable. In addition, material risk factors and related assumptions used to develop the FLI must accompany the disclosure. In determining what constitutes a "reasonable basis" for FLI, a reporting issuer should consider the reasonableness of the assumptions underlying the FLI and the process followed in preparing and reviewing the FLI. Updates on FLI help investors understand how actual results are reasonably likely to differ materially from previously disclosed FLI and how the reporting issuer is progressing towards the achievement of its disclosed targets and objectives.

The disclosure of FLI is subject to securities requirements under National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102){1}, irrespective of where FLI is located within a document or the nature of the document where FLI is disclosed. Therefore, the rules apply regardless of whether FLI is on a website, in a news release or in the MD&A. The requirements can be divided in two parts: (a) requirements relating to the initial disclosure of FLI, and (b) requirements relating to the ongoing obligations to update, compare to actual results and, if appropriate, withdraw previously disclosed FLI. We have summarized these requirements in Appendix A Requirements.

Exceptions

Oral statements

The rules do not apply to FLI presented orally. However, if oral statements containing FLI are transcribed, for example, if the issuer transcribes the quarterly conference call with analysts where management of a reporting issuer discusses their results, these statements would be subject to the requirements under NI 51-102.

Disclosure for Oil and Gas Activities or for Mineral Projects

Part 4B and section 5.8 of NI 51-102 do not apply to disclosure of FOFI or financial outlook subject to requirements in National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities or National Instrument 43-101 Standards of Disclosure for Mineral Projects. This disclosure is still subject to the requirements under Part 4A of NI 51-102, including identifying FLI, stating material factors and assumptions used, and providing the required disclaimers and cautionary language. We note that frequently, scientific and technical information about a mineral project includes or is based on FLI. Examples of FLI include metal price assumptions, cash flow forecasts, projected capital and operating costs, metal or mineral recoveries, mine life and production rates, and other assumptions used in preliminary economic assessments, pre-feasibility studies, and feasibility studies.

Update and withdrawal

Updating or notification that FLI is being withdrawn must be included in the MD&A or in a news release. Section 5.8 of NI 51-102 provides flexibility to allow the updated information to be included in a news release as long as it is filed prior to the MD&A. In this case, the MD&A must refer to the news release to satisfy the requirements. The disclosure and discussion of material differences between actual results and previously disclosed FOFI or financial outlook must be included in the MD&A; including this information in a news release instead of the MD&A is not permitted.

Audit Committee and Board of Directors

Section 5.5 of NI 51-102 requires the annual and interim MD&A to be approved by the board of directors before being filed{2} and National Instrument 52-110 Audit Committees requires that an audit committee review an issuer's financial statements, MD&A, and interim and annual profit or loss press releases before a reporting issuer publicly discloses this information. This includes FLI included in the MD&A or in a press release.

The audit committee and board of directors' role in the oversight of FLI helps ensure the dissemination of timely and transparent information to investors. As such, the audit committee and board of directors should consider reviewing and approving the initial FLI disclosure, determining whether updates are required, questioning management on the assumptions being used to develop FLI, and approving the targets before they are disclosed publicly.

4. What We Found

In our review of 60 reporting issuers we identified four common areas where improvement is needed:

• clear identification of FLI

• material factors and assumptions

• updating previously disclosed FLI

• comparison of actual results to previously disclosed FOFI or financial outlook

To help reporting issuers improve their disclosure, in this section we provide examples of frequently identified boilerplate/non-compliant disclosure, along with suggestions to improve disclosure with entity-specific compliant FLI.

1. Identification of FLI

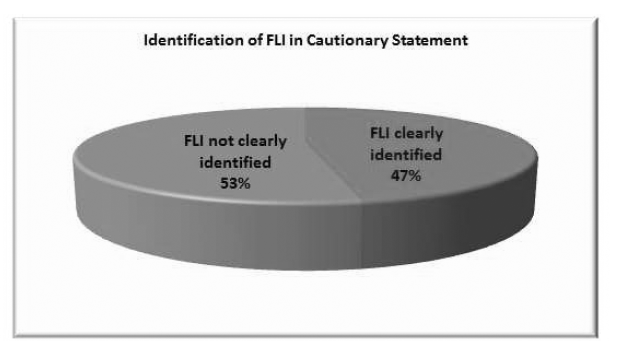

Section 4A.3 of NI 51-102 requires reporting issuers to clearly identify material FLI. All but one reporting issuer that we reviewed included cautionary language which identified the existence of FLI in their financial reporting document. However, our review revealed that only 47% of reporting issuers clearly identified entity-specific FLI.

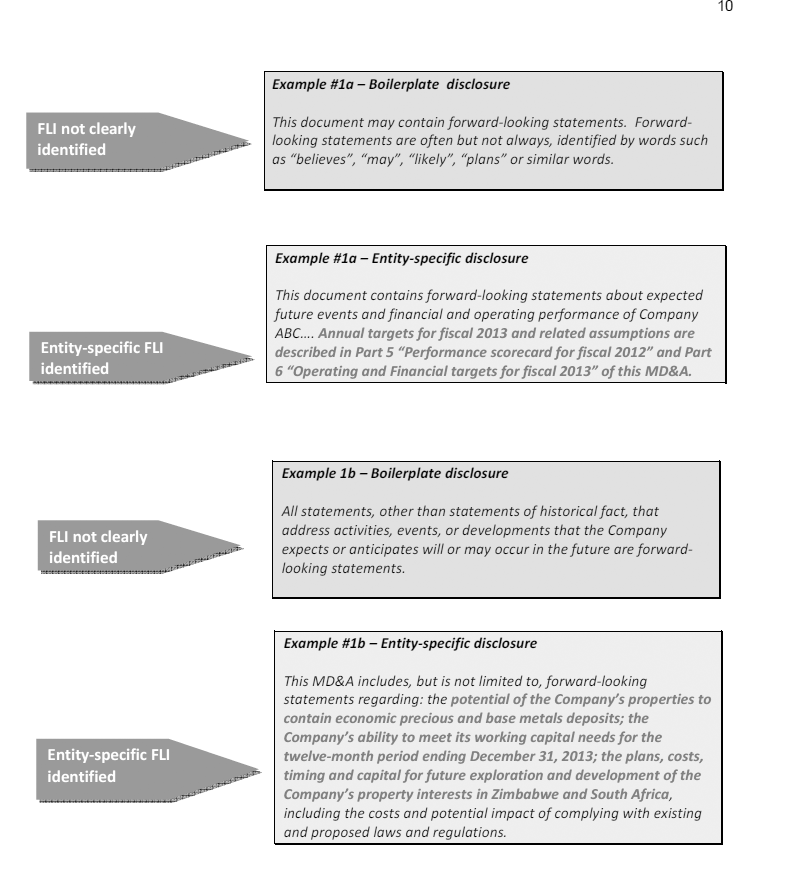

As indicated previously in this notice, it is important that FLI be clearly identified so that readers are not confused and treat it as historical information. The identification of material FLI in a generic and boilerplate manner does not allow users of the financial information to specifically identify and understand that a forward-looking statement is being provided by the reporting issuer in a document or website.

The boilerplate disclosure in the two examples above does not contain details that clearly identify the FLI relating to the issuer's business. As illustrated in the entity-specific examples, FLI is clearly identified allowing a user of the information to understand that it is FLI that is being disclosed and not historical information.

2. Material Factors and Assumptions

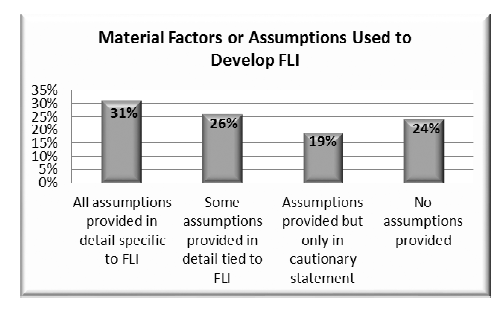

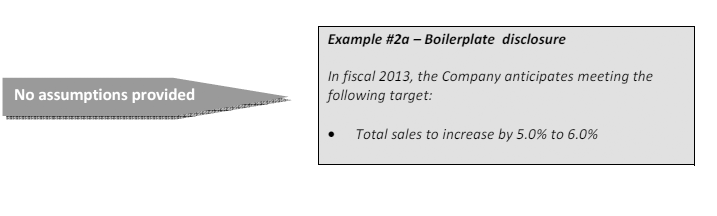

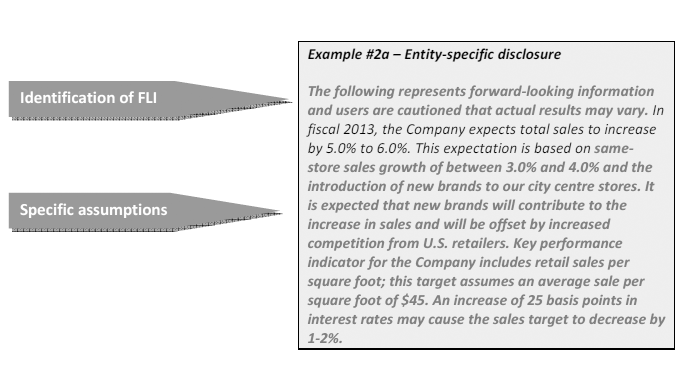

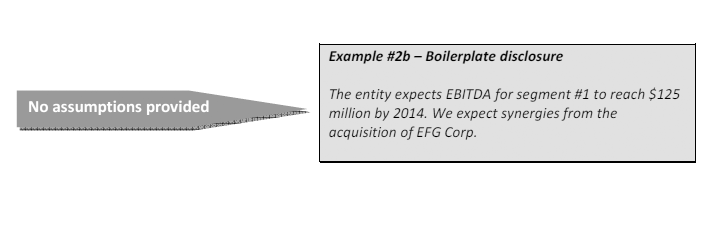

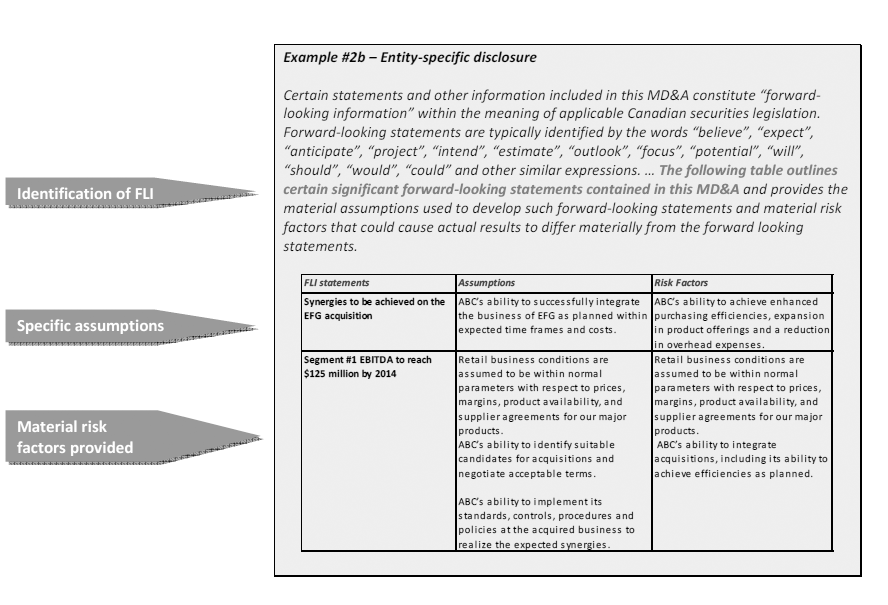

Disclosure of specific relevant material factors or assumptions including material risk factors underlying the FLI is necessary for investors to understand how actual results may vary from FLI. Based on our review, 24% of reporting issuers did not disclose any material factors or assumptions used to develop their FLI. In addition, 19% of reporting issuers only provided generic factors and assumptions within the cautionary statement. Reporting issuers should carefully analyze the assumptions that underlie FLI. Assumptions should be reasonable, supportable and entity-specific. Whenever possible, assumptions should be quantified as this provides valuable information for investors.

Material factors and assumptions must be:

• reasonable

• supportable

• entity-specific

• tied to FLI

• disclosed

The majority of issuers reviewed did not quantify their assumptions. Reporting issuers continue to provide general boilerplate disclosure that does not adequately describe the key assumptions used and how primary risks may impact future performance. Assumptions disclosed are not specific to the reporting issuers' business and do not tie directly to the disclosure being provided. Example 2a below, is a common example where assumptions supporting the sales target were not provided.

A description of key specific risks and uncertainties that may impact a reporting issuer's future performance will assist an investor's understanding of an issuer's business and will lead to better reporting. This is illustrated in the entity-specific example below. General risk factors and assumptions provide investors with limited information and do not provide insight on how they relate to and impact the FLI being disclosed.

In example 2b (boilerplate disclosure), the reporting issuer has provided targets for the fiscal year but has not provided assumptions that support the FLI provided. The statement about the issuer achieving synergies does not help an investor understand how these synergies will help the issuer attain EBITDA of $125 million for segment #1.

The entity-specific example below is an illustration of how a reporting issuer can clearly identify FLI statements and disclose relevant and specific material risk factors and assumptions.

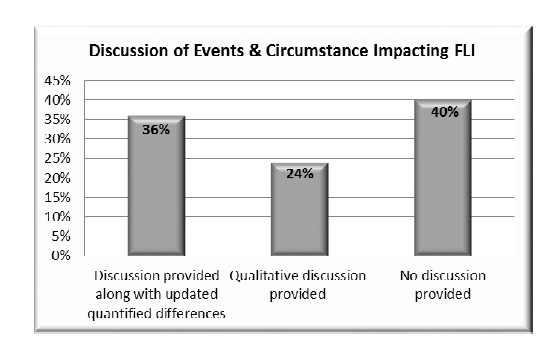

3. Updating previously disclosed FLI

A reporting issuer is required under Section 5.8 of NI 51-102 to discuss in the MD&A or in a press release, events and circumstances that are reasonably likely to cause actual results to differ materially from previously disclosed FLI. The expected differences must also be disclosed. For example, economic and market events may cause actual results to differ materially from previously disclosed material FLI.

Forty percent of reporting issuers reviewed did not disclose the events and circumstances impacting their previously reported FLI that occurred during the period. Overall, only 36% of reporting issuers included a quantified discussion of events and circumstances that are reasonably likely to cause actual results to differ materially from previously reported FLI. Failure to provide disclosure of material differences in events and circumstances prevents investors from assessing how well the reporting issuer is progressing towards the achievement of its disclosed targets and objectives. For example, updated quantified data that relates to factors and assumptions that may impact the future performance of the issuer will clarify how and why these changes may impact future performance; this will lead to a clearer understanding of events and circumstances that occurred in the business environment in which the reporting issuer operates.

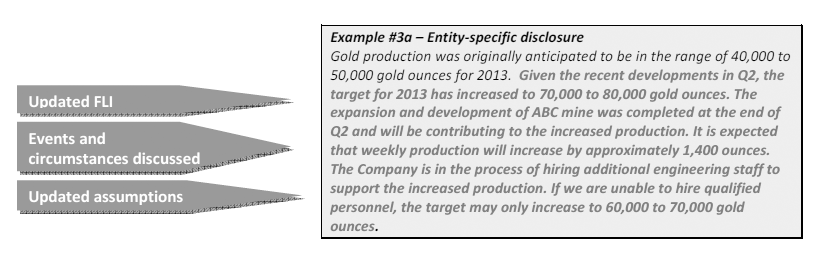

In example 3a (boilerplate disclosure), the reporting issuer did not disclose events or circumstances that occurred during the period and how they impact previously disclosed FLI. Simply providing an update of previously disclosed FLI without the data that relates to the underlying factors and assumptions provides no insight on why and how the target has changed.

In the example above, the reporting issuer provides a discussion of the event that occurred during the period and the impact it has on the original target. Updated assumptions and risks are also included, which provides investors greater insight on the issuer's future performance.

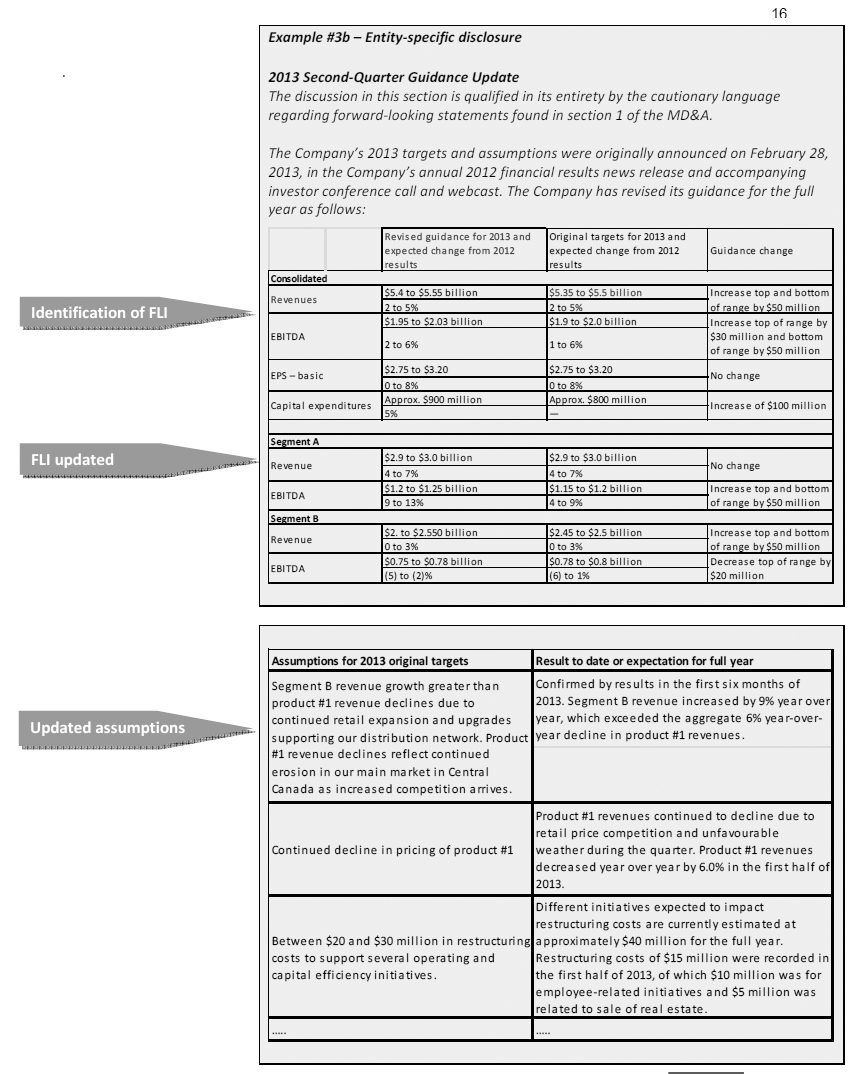

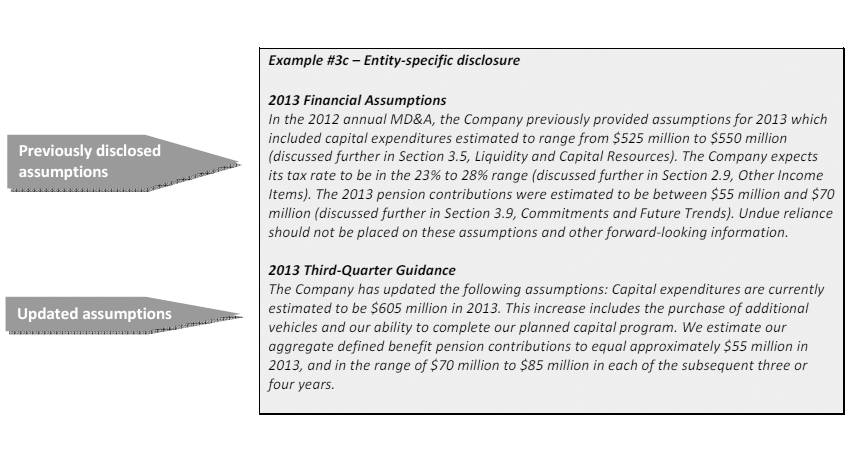

Finally, we have included two examples on the following pages illustrating different approaches on how reporting issuers can clearly identify FLI and update previously disclosed FLI by explaining why the original assumptions changed with supporting numbers. Using tables is an effective approach to clearly communicate FLI and update the information.

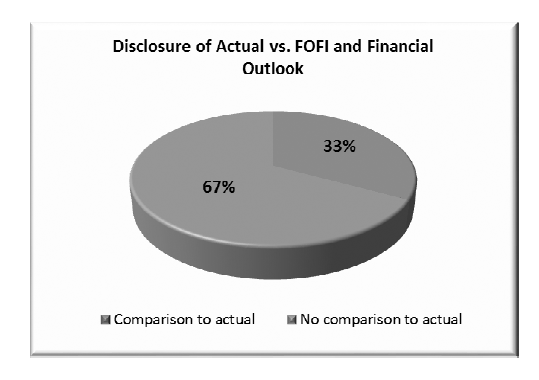

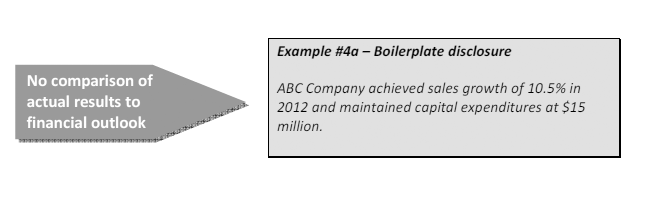

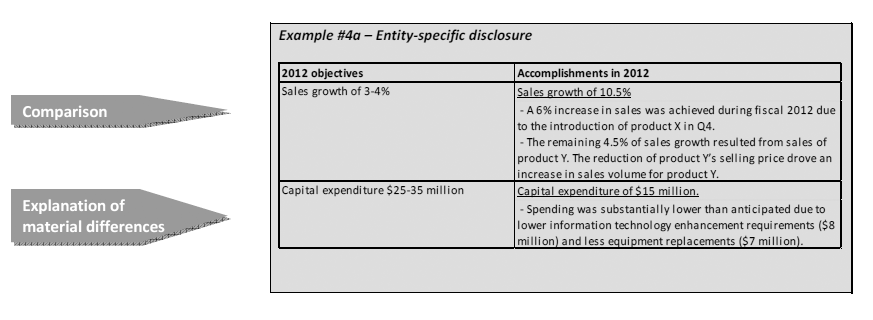

4. Comparison of actual results vs. FOFI and Financial Outlook in MD&A

The comparison of actual results to previously disclosed FOFI and financial outlook is important for investors in their assessment of the effectiveness of management and of the current and future business performance of the issuer. Only 33% of reporting issuers reviewed provided this comparison. Under subsection 5.8(4) of NI 51-102, reporting issuers are required to provide such a comparison in the MD&A if actual amounts differ materially from previously disclosed FOFI or financial outlook for that period.

The disclosure in the example below does not provide a comparison between actual results and previously disclosed financial outlook. A comparison of the actual results to the FOFI or financial outlook originally disclosed in previous documents will allow investors the opportunity to assess the reasonableness of previous disclosure and adjust their expectations.

The disclosure in the entity-specific example below provides a comprehensive discussion comparing actual results to previously disclosed financial outlook. The discussion includes a qualitative and quantitative explanation of the material differences. Investors will be able to clearly understand whether the targets were or were not achieved and why.

5. Practice Points

Effective communication of FLI enables investors to have a better understanding of a reporting issuer's business, their long term objectives, and their progress in achieving those objectives. The following practice points will assist issuers and their advisors in promoting clear, transparent disclosure for FLI.

1. Quality of assumptions

Assumptions should be reasonable and specific to a reporting issuer. Material factors and assumptions should be provided where FLI is disclosed. Qualitative, entity-specific and quantitative assumptions are informative and useful to investors.

2. Timely updating of ongoing progress

Updating of ongoing progress as compared to previously disclosed FLI allows investors to assess corporate performance during the fiscal year. Affirmation of targets, disclosure of affected material differences, as well as updates on trends likely to impact future performance on a timely basis is informative information for investors. Disclosure of expected material differences is also important.

3. Key Performance Indicators -- financial and non-financial

KPIs can help both reporting issuers and investors understand how well an issuer is progressing towards their objectives. Disclosure of an issuer's objectives along with their related KPIs is an important tool to measure success of corporate performance. KPIs can be both quantitative and qualitative in nature.

4. Separate Presentation

Having a separate section with all FLI enables investors to easily identify information that constitutes material FLI and what represents historical information. The FLI for an issuer can be presented in a narrative format or through the use of tables and charts. A table that sets out objectives, key specific assumptions and risks will clarify the relationship between the underlying key components and the FLI.

5. Role of the Audit Committee and Board of Directors

The audit committee and board of directors play a key role in the oversight of FLI. As such, they should consider reviewing and approving all FLI disclosure before it is publicly disclosed, including the underlying assumptions being used to develop the FLI.

The following is an illustration of an entity-specific example where the reporting issuer provides comprehensive and understandable FLI disclosure. The table includes discussion of the original target for the KPI, a comparison to actual results, inclusion of entity-specific related assumptions and updated targets for the upcoming year.

|

Scorecard |

What we targeted |

How we did |

Commentary |

What we are targeting to do in 2013 |

|

|

||||

|

Same store sales growth |

3%-5% |

6.30% |

Our same-store sales growth was driven mainly by changes to our clothing lines with quality products introduced at targeted price points which contributed to positive product mix, and combined with pricing, resulted in a higher average sale per consumer. Additional advertising targeted at our core growth markets in Eastern U.S. also contributed favourably, and we believe was a significant factor in the strong performance during the period. |

4%-6% |

|

|

||||

|

EPS (fully diluted) |

$2.30 -- $2.40 |

$2.35 |

A combination of operating income growth driven primarily by continued strength in corporate sales in the Americas, a lower effective tax rate, and our share repurchase program contributed to our EPS performance in fiscal 2012. |

$2.35 -- $2.45 |

6. Conclusions

The findings of our review illustrate that the quality of FLI continues to be an area where disclosure needs improvement. Investors continue to demand forward-looking information. Clear identification of FLI, detailed disclosure of entity-specific material factors and assumptions, updating FLI, and providing comparisons is important, required information for reporting issuers and can provide clear and informative information to investors.

Given its importance to investors, this is an area of disclosure we will continue to assess in our CD and prospectus review programs. Issuers who have not complied with the FLI requirements will be expected to take corrective action.

7. Questions and Additional Resources

If you have any questions about this report, please contact:

Sandra HeldmanSenior Accountant, Corporate Finance416-593-2355Ritu KalraSenior Accountant, Corporate Finance416-593-8063Marie-France BourretAccountant, Corporate Finance416-593-8083

8. Appendix A -- Requirements

|

|

Rule Reference & Subsection |

Description |

FLI |

FOFI and financial outlook |

||

|

|

||||||

|

Definitions |

1.1 of NI 51-102 |

Definitions for FLI, FOFI and financial outlook |

• |

• |

||

|

|

||||||

|

Reasonable Basis |

4A.2 of NI 51-102 |

Reasonable basis for FLI required |

• |

• |

||

|

|

4A.2 of NI 51-102CP |

|

|

|

|

|

|

|

||||||

|

Assumptions |

4B.2 of NI 51-102 |

Reasonable assumptions in the circumstances supporting financial outlook or FOFI required |

|

• |

||

|

|

|

• |

Financial outlook or FOFI must |

|

|

|

|

|

|

|

• |

be limited to a period for which information can be reasonably estimated (generally not more than a year) |

|

|

|

|

|

|

• |

use the accounting policies the reporting issuer expects to use to prepare its historical F/S for the period covered by the FOFI or financial outlook |

|

|

|

|

||||||

|

Disclosure |

4A.3(a) of NI 51-102 |

Information must be identified as FLI |

• |

• |

||

|

|

||||||

|

|

4A.3(b) of NI 51-102 |

Users must be cautioned that actual results may vary from FLI |

• |

• |

||

|

|

||||||

|

|

4A.3(b) of NI 51-102 |

Material risk factors that could cause actual results to differ materially from the FLI must be identified |

• |

• |

||

|

|

4A.5 of NI 51-102CP |

|

|

|

|

|

|

|

||||||

|

|

4A.3(c) of NI 51-102 |

Material factors and assumptions used to develop FLI must be identified |

• |

• |

||

|

|

4A.6 of NI 51-102CP |

|

|

|

|

|

|

|

||||||

|

|

4A.3(c) of NI 51-102 |

Description of the issuer's policy for updating FLI if it includes procedures in addition to those required under Section 5.8 of NI 51-102 (described below) |

• |

• |

||

|

|

||||||

|

Additional disclosure for financial outlook and FOFI |

4B.3(a) of NI 51-102 |

If the document containing the disclosure is not dated, include the date management approved the FOFI or financial outlook |

|

• |

||

|

|

||||||

|

|

4B.3(b) of NI 51-102 |

Purpose of financial outlook or FOFI must be explained |

|

• |

||

|

|

||||||

|

|

4B.3(b) of NI 51-102 |

Readers must be cautioned that information may not be appropriate for other purposes |

|

• |

||

|

|

||||||

|

Updating FLI in interim or annual MD&A |

5.8(2) of NI 51-102 |

Disclose events or circumstances that have occurred in the period that are reasonably likely to cause actual results to differ materially from the previously publicly disclosed material FLI. Discuss the expected differences. This applies to FLI for a financial period that is not yet complete. |

• |

• |

||

|

|

||||||

|

Comparison to Actual |

5.8(4) of NI 51-102 |

Disclose material differences between actual annual or interim results and any FOFI or financial outlook previously disclosed for the period |

|

• |

||

|

|

||||||

|

Withdrawal |

5.8(5) of NI 51-102 |

Disclose any decision to withdraw previously disclosed FLI. The events and circumstances that led to this decision must be discussed as are the assumptions underlying the FLI that are no longer valid. |

• |

• |

||

{1} Part 4A -Forward-Looking Information, Part 4B -- FOFI and Financial Outlook and Section 5.8 -- Disclosure Relating to Previously Disclosed Material Forward-Looking Information.

{2} The approval of the interim MD&A by the board of directors may be delegated to the audit committee.