Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

OSC Staff Notice: 33-728 - 2007 Annual Report - Compliance Team

OSC Staff Notice: 33-728 - 2007 Annual Report - Compliance Team

OSC STAFF NOTICE 33-728

2007 ANNUAL REPORT -- COMPLIANCE TEAM

Introduction

The 2007 Compliance team report summarizes our activities from April 1, 2006 to March 31, 2007. This report includes the results of our reviews of investment counsel and portfolio managers (ICPMs), fund managers and limited market dealers (LMDs) (collectively, market participants).

This year, we have added a new section covering new and proposed rules published by the Ontario Securities Commission (OSC) that may affect market participants.

We use a risk-based approach in selecting market participants for review. However, we also select market participants for review on a random basis. We encourage market participants to use this report as a self-assessment tool to strengthen their compliance with Ontario securities law and to improve their internal controls.

This report is divided into nine sections:

1. Compliance initiatives. This section describes focused reviews or sweeps we conducted in 2006-07 and reviews we are planning for 2007-08.

2. New and proposed rules. This section describes new and proposed rules published by the OSC and how they may affect the business operations of market participants.

3. Compliance process. This section describes how we update our risk assessment models and review programs.

4. Fund manager reviews. This section describes the key areas we reviewed and the deficiencies we identified in our ongoing reviews of fund managers.

5. LMD reviews. This section describes our ongoing reviews of LMDs.

6. Common ICPM deficiencies. This section deals with common deficiencies we identified during our reviews of ICPMs. We have included suggested practices to help ICPMs improve existing procedures and establish procedures in areas where they are lacking, and to give general guidance on improving overall compliance. We have also highlighted changes in our findings from the previous years' annual reports for comparison.

7. Significant ICPM deficiencies. This section summarizes the top three significant deficiencies of ICPMs.

8. Addressing the deficiencies. This section describes how we monitor market participants after we issue a compliance review report and various regulatory tools that we may use to address serious conduct issues or violations of securities law.

9. Seeking input from our market participants. This section describes our new process of seeking input from our market participants through surveys and how we use this information to improve our regulatory services.

1. Compliance initiatives

This section describes focused reviews or sweeps that the Compliance team conducted in 2006-07 and reviews that we are planning for the next fiscal year. These reviews are in addition to the regular, ongoing reviews of market participants that we conduct each year.

2006-07 reviews

Marketing sweep

In late 2006, we conducted focused reviews of the marketing practices of a sample of ICPMs. Our goals were to broaden our understanding of the type and content of marketing materials used by ICPMs, assess their compliance with Ontario securities law and identify any regulatory gaps.

The sample included ICPMs that were managers of pooled products and hedge funds, ICPMs that catered to large institutional investors and ICPMs with a variety of clients, including private clients.

We reviewed a variety of marketing documents, including brochures, newspaper and magazine advertisements, one-on-one presentations, websites, market commentaries and offering documents relating to pooled products or hedge funds managed by the ICPM.

In the near future, we will publish an industry report that summarizes the findings of our focused reviews and provides guidance on best practices and on how to comply with applicable legislation. We encourage ICPMs to look to the industry report to identify areas where they can improve their marketing practices. We will continue to review the marketing practices of ICPMs as part of our regular field reviews of ICPMs.

Sweep of Part 5 of National Instrument 81-105 -- Mutual Fund Sales Practices (NI 81 105)

Part 5 of NI 81-105 deals with marketing and educational practices sponsored by fund companies. In the fall of 2006, staff from the Compliance team and the Investment Funds Branch conducted focused, onsite reviews of 20 fund managers. Our goals were to assess fund managers' compliance with Part 5, to determine whether guidance was required and to assess whether amendments to Part 5 were necessary.

On April 27, 2007, we issued OSC Staff Notice 11-760 -- Report on Mutual Fund Sales Practices under Part 5 of National Instrument 81-105 -- Mutual Fund Sales Practices (OSC Staff Notice 11-760). The notice summarizes the results of our findings and provides guidance to market participants on complying with the legislation. We encourage market participants to look to the report to identify areas where they can make improvements.

We will continue to review the sales practices of fund managers as part of our regular fund manager reviews.

Planned reviews for 2007-08

New registrant reviews

During the next fiscal year, we will conduct focused reviews of a sample of newly registered ICPMs. Our goals are to meet with senior management of the registrant and gain a high level understanding of their business, review compliance with Ontario securities law, verify the registrant's activities and assess their financial condition. Reviews of new registrants will form part of our ongoing oversight of registrants.

Sweeps

Similar to last year, we will conduct two sweeps in the next fiscal year. We have not yet finalized the topics. One sweep will focus on fund managers and the other will focus on ICPMs.

2. New and proposed rules

During the year, the OSC published several new and proposed rules that may affect the operations of market participants. We have summarized some of the major rules below.

This summary may not include all the rules that affect your business and should not be considered or relied upon as legal advice. Interpretations and comments do not replace or modify any provisions of the rule. Please refer to the specific rules, their forms and companion policies. Where appropriate, you should consult a lawyer with expertise in securities law for advice on how to comply with the regulation.

National Instrument 24-101 -- Institutional trade matching and settlement (NI 24-101)

Although NI 24-101 came into force on April 1, 2007, specific reporting and documentation requirements will not come into force until October 1, 2007.

NI 24-101 provides a framework for ensuring more efficient and timely processing and settlement of trades, particularly for institutional trades. The main goal of NI 24-101 is to ensure that registered dealers, ICPMs and other related trade-matching parties establish, maintain and enforce policies and procedures designed to achieve matching of delivery-against-payment (DAP) or receipt-against-payment (RAP) trades no later than the end of the day on which the trade was executed or "T".

Matching essentially means that the relevant parties to the DAP/RAP trade process (trade-matching parties) have agreed to the details and settlement instructions of the trade. Under NI 24-101, 95% of all institutional trades must be matched by end-of-day on T. This benchmark is being gradually phased in over approximately a three-year period.

NI 24-101 will affect ICPMs whose clients use DAP or RAP accounts. Assets in these accounts are normally held with a custodian or dealer that is separate from the dealer that executes the client's trades. The rule will likely affect ICPMs that manage money for institutional clients and in some cases, individual clients.

Under NI 24-101, ICPMs are required to:

• establish, maintain and enforce policies and procedures designed to achieve matching of DAP and RAP trades as soon as practical after the trade has been executed and in any event no later than the end of T

• enter into a trade-matching agreement with each trade-matching party or be provided a trade-matching statement before opening a DAP or RAP account or giving an order to execute a DAP or RAP trade for an institutional investor

• complete and deliver an exception report for all calendar quarters in which they do not meet stated objectives

For more details, please visit www.osc.gov.on.ca.

National Instrument 81-107 -- Independent review committee for investment funds (NI 81-107)

On November 1, 2006, NI 81-107 came into force with a one-year transition period. The rule requires investment funds that are a reporting issuer to have an independent review committee (IRC). The IRC must include at least three members and be fully independent. The IRC oversees all decisions involving actual or perceived conflicts of interest that the fund manager faces in operating the fund.

NI 81-107 applies to all publicly offered mutual funds and non-redeemable investment funds, including:

• labour sponsored or venture capital funds

• scholarship plans

• mutual funds and closed-end funds listed and posted for trading on a stock exchange or quoted on an over-the-counter market

• investment funds not governed by National Instrument 81-102 -- Mutual Funds (NI 81-102)

The rule does not apply to pooled funds.

The rule deals with two types of conflicts:

• "business" or "operational" conflicts, which relate to the fund manager's operations that are not specifically regulated under securities legislation except through the general duties of loyalty and care imposed on the fund manager

• "structural" conflicts, which result from transactions that the fund manager proposes with related entities of the manager, fund or portfolio manager and that are currently prohibited or restricted by securities legislation

The rule also requires fund managers to establish written policies and procedures on conflict matters and to refer these matters to the IRC for its review.

Fund managers were required to appoint IRC members no later than May 1, 2007. Investment funds that are a reporting issuer are required to be fully compliant with the rule by November 1, 2007. For more details, please visit www.osc.gov.on.ca.

Proposed National Instrument 31-103 -- Registration Requirements (NI 31-103)

On February 20, 2007, the Canadian Securities Administrators (CSA) published proposed NI 31-103 for comment. The comment period ended on June 30, 2007. The purpose of the proposed rule is to harmonize, streamline and modernize the registration regime across Canada. The registration requirements are designed to protect investors from unfair, improper or fraudulent practices and therefore, enhance the integrity of capital markets.

The following is a summary of some of the major changes proposed by NI 31-103 that may affect your business operations as a market participant if they are implemented:

• the introduction of a business trigger for dealer registration

• requiring persons that deal in prospectus-exempt securities to register as Exempt-Market Dealers

• permanent registration

• investment fund manager registration

• two new individual categories of registration for all types of registered firms: Ultimate Designated Person and Chief Compliance Officer

• harmonized proficiency requirements for non-Self Regulatory Organization (SRO) registrants

• modernized proficiency requirements by moving from course-based to exam-based requirements

• increased minimum capital requirements for most non-SRO registrants, other than portfolio managers with access to clients' cash or assets

• modernized insurance requirements for non-SRO registrants

• new client relationship disclosure document requirements for most registrants

• requirements for complaint handling procedures and dispute resolution

• new referral arrangement requirements

For more details, please visit www.rrp-info.ca.

Proposed National Instrument 23-102 -- Use of Client Brokerage Commissions as Payment for Order Execution Services or Research ("Soft Dollar" Arrangements) (NI 23-102)

On July 21, 2006, the CSA published proposed NI 23-102 for comment. The comment period ended on October 19, 2006.

The proposed NI 23-102 provides a specific framework for the use of client brokerage commissions by ICPMs and dealers and proposes disclosure requirements for ICPMs. The proposed Companion Policy provides additional guidance on the requirements of the national instrument, including guidance on the types of goods and services that may be obtained with client brokerage commissions, as well as non-permitted goods and services. For more details, please visit www.osc.gov.on.ca.

3. Compliance process

Updating our risk assessment models

We are planning to update our risk assessment models for ICPMs and fund managers. As part of this process, we may send a revised risk assessment questionnaire to ICPMs and fund managers in the near future. This information is important for us in updating our risk models.

New review areas

We review and update our review programs for market participants on an ongoing basis to reflect changes in securities law or industry practices. Described below are areas we added to our reviews this year.

Dormant accounts

An account is dormant if the account holder cannot be located after a period of time because their address is out-dated or they are deceased, among other reasons.

As a fiduciary, fund managers are responsible for ensuring securityholders' records are current and up-to-date. We added dormant accounts to our fund manager review program because we would like to gain a better understanding of how fund managers deal with unclaimed property held in these accounts. For example, we would like to find out what policies and procedures fund managers have in place to identify and monitor the activities in dormant accounts and how they treat unclaimed balances.

Dormant accounts may not be an issue for fund managers where the majority of the funds are held under nominee name. However, fund managers that are also distributors or have client name accounts should have appropriate procedures for dealing with unclaimed property or dormant accounts.

Business Continuity Plan (BCP)

We added business continuity planning to our market participant reviews. An effective BCP enables a firm to resume providing services to its clients within a reasonable amount of time after a disaster. Market participants should have a BCP to mitigate, respond and recover from a potential disaster. Each firm's BCP should be tailored to the risks, size, nature and complexities of its operations.

4. Fund manager reviews

In fiscal 2007, the Compliance team completed reviews of some fund managers.

During a review, we focus on the following key areas of the fund manager's business operations:

• transfer agency

• fund accounting

• trust accounting

• sales practices

• marketing

Our main objectives are to ensure that:

• securityholders' records are accurate and up-to-date

• all transactions are appropriately authorized and recorded

• the fund's net asset value (NAV) is correctly calculated by ensuring that the securities in the fund are properly valued and all income and expenses of the fund have been accounted for

• purchase and redemption proceeds are accounted for appropriately

• controls are in place to safeguard securityholders' assets against misappropriation

• marketing materials are adequately reviewed to ensure they are not misleading and do not contain any misrepresentations

• all applicable legislation is being followed

Fund managers may perform all of their core functions in-house or outsource some of them to third-party service providers. When fund managers perform these functions in-house, they should have an appropriate compliance infrastructure to ensure that each function is performed properly. If the fund manager outsources these functions, it must have adequate policies and procedures for overseeing the service provider and ensuring that the provider performs the functions effectively and in accordance with securities legislation.

Subsection 116(1) of the Securities Act (Ontario) (the Act) requires fund managers to exercise their duties honestly, in good faith and in the best interests of the mutual fund. In doing so, fund managers exercise the degree of care, diligence and skill that a reasonably prudent person would exercise in the circumstances.

We identified deficiencies in a variety of areas. We also continue to find issues with sales practices (see OSC Staff Notice 11-760). The most deficiencies were in the following three areas:

• marketing

• oversight of service providers

• written policies and procedures

Marketing

Fund managers must prepare marketing materials in accordance with the standard of care under subsection 116(1) of the Act. In addition, subsection 15.2(1) of NI 81-102 provides that no sales communication shall be untrue or misleading, or include a statement that conflicts with information that is contained in the simplified prospectus or annual information form of a mutual fund.

We observed the following in our reviews of marketing materials:

• Marketing materials contained out-of-date information.

• When marketing materials included performance data, they did not include the required warning disclosures.

• Fund returns were compared to inappropriate benchmarks.

• Misleading performance returns were used.

• Fund profiles disclosing management expense ratios (MERs) did not include disclosure indicating that certain fund expenses otherwise payable by the funds were waived or paid by the fund manager.

• Published mutual fund ratings in sales communications did not disclose ratings for all the required periods.

• Website communications included incorrect rating information.

• Disclosure on websites contained information that was inconsistent with the simplified prospectus or was incorrect.

• Disclaimers stated that fund managers did not have any responsibility for errors or omissions that may be contained in the marketing materials.

Suggested practices

• All marketing materials must include information that is accurate, complete and not misleading.

• Ensure that mutual fund sales communications contain the required warning prescribed by NI 81-102.

• When a performance rating or ranking for a mutual fund is presented, the rating or ranking must be presented for all periods where standard performance data is required.

• Establish and enforce procedures for preparing, reviewing and approving marketing materials. This includes having marketing materials reviewed by someone who is not involved in preparing them.

Oversight of service providers

Some fund managers that outsourced the fund accounting, trust accounting and/or transfer agency function did not have adequate oversight procedures.

Suggested practices

Fund managers should have appropriate procedures for monitoring the functions that they outsource and ensuring that these functions are performed properly.

Written policies and procedures

Some fund managers did not have adequate written policies and procedures for the major functional areas of their business.

Suggested practices

Fund managers should have written policies and procedures for key functional areas, such as transfer agency, fund accounting, trust accounting, marketing, sales practices, complaint handling and monitoring of outsourced functions.

5. LMD reviews

As a result of issues found during our sweep of LMDs in 2005, we added LMDs to our ongoing, regular review program this year. We conducted the first of these reviews in early 2007. We found deficiencies similar to some of those noted during our LMD sweep (see OSC Staff Notice 11-758 -- Review of Limited Market Dealers). We are working with registrants to ensure that these deficiencies are resolved to our satisfaction.

6. Common ICPM deficiencies

This section discusses the results of our reviews of ICPMs from April 1, 2006 to March 31, 2007. We use a risk-based approach in selecting ICPMs for review. We also select ICPMs for review on a random basis. Please note that the ICPMs selected for review year over year are different firms with different operations that vary in size, based on assets under management.{1} The majority of ICPMs we reviewed during the past fiscal year were small firms with assets under management of less than $250 million.

The table below summarizes the ten most common areas of deficiency we identified and how they compare with the previous three years.{2}

We identified a number of issues under each category. An ICPM is included in a category if it had at least one issue in that area.

2007

2005/06{3}

2004

2003

Common deficiency

Ranking

Ranking

Ranking

Ranking

1.

Maintenance of books and

1

3

5

1

records

2.

Policy for fairness in the

2

6

2

2

allocation of investment

opportunities (fairness policy)

3.

Know your client (KYC) and

3

8

10

9

suitability information

4.

Marketing

4

2

8

8

5.

Portfolio management,

5

9

4

7

including advisory contracts

6.

Statement of policies

6

5

3

5

7.

Policies and procedures

7

1

1

3

manual

8.

Personal trading

8

7

9

10

9.

Capital calculations

9

4

6

4

10.

Registration issues

10

10

7

6

Trends

Compared to previous years, it appears that ICPMs have fallen behind in the following areas:

• maintenance of books and records

• fairness policy

• KYC and suitability information

The increase in these areas is likely because the majority of our reviews in 2007 focused on smaller ICPMs. It is more common to find issues such as inadequate books and records in small firms. Some small ICPMs had generic fairness policies and did not have a process in place to collect and document KYC information. As a result, the increase in these common deficiencies may not generally reflect industry practices.

Some of the firms we reviewed consist of one or two principals who were the key people operating the company. Under this scenario, we generally expect less detailed written policies and procedures. However, we review and assess their current processes and procedures to ensure compliance with securities legislation.

We also found that some small ICPMs were not active in marketing their services, as most of their clients were obtained through word of mouth or close friends. Others had very aggressive marketing materials on their new funds and we noted problems with how they constructed performance composites.

The overall decline in the relative ranking of common deficiencies in policies and procedures and marketing may be due to the following reasons:

• Some of the ICPMs we reviewed did not prepare marketing materials.

• In general, we did not raise issues on written policies and procedures manuals with smaller firms if we were satisfied with their processes and procedures.

Detailed discussion of common deficiencies

The following is a discussion of specific issues we identified under the ten most common deficiencies, the applicable legislation and suggested practices for addressing the deficiencies. We encourage all ICPMs to use this as a self-assessment tool to strengthen their compliance with Ontario securities law.

1. Maintenance of books and records

ICPMs are required to maintain books and records necessary to properly record their business transactions, trading transactions and other financial affairs. Subsection 113(1) of R.R.O. 1990, Regulation 1015 made under the Act (the Regulation) requires ICPMs to maintain the books and records that are necessary to properly record their business transactions and financial affairs.

The following are examples of books and records that were missing or incomplete:

• trade blotters

• copies of trade orders or instructions

• trade orders (not time-stamped)

• a log of failed trades and trading errors

• advisory agreements

• client investment objectives and restrictions

• a complaints log, including the nature of the complaint and the outcome

• proxies voted or proxy logs

• cash and security reconciliations

• monthly financial statements

• written agreements with third parties

Suggested practices

Regulation 113(3) lists the books and records that ICPMs are required to maintain. ICPMs should also keep any other books and records necessary to properly record their business transactions, trading transactions and other financial affairs.

2. Fairness policy

Regulation 115(1) requires ICPMs to have standards to ensure that investment opportunities are allocated fairly among their clients. ICPMs are required to prepare written fairness policies dealing with the allocation of investment opportunities among clients, file these policies with the OSC and distribute them to all clients.

During our reviews, we observed the following:

• The most current fairness policy was not filed with the OSC or was not provided to all clients, or both.

• Clients did not get a complete fill on their orders because ICPMs included proprietary, employee and/or personal accounts in block trades and allocated a pro-rata share of partially filled blocked trades or initial public offerings (IPOs) to these accounts.

• The fairness policy stated that preference may be given to weaker performing accounts or accounts of a certain size. As well, weaker performing accounts were shown preference during the allocation of a partial fill of a block trade.

• The fairness policy did not reflect actual trading practices.

Suggested practices

ICPMs should tailor their fairness policy to address all relevant areas of their business. See OSC Staff Notice 33-723 Fair Allocation of Investment Opportunities Compliance Team Desk Review for additional guidance.

At a minimum, the fairness policy should state:

• how prices and commissions are allocated among client accounts when trades are blocked

• how block trades and IPOs are allocated among client accounts when there is only a partial fill (e.g. pro-rata)

• the process for determining which clients will participate in IPOs

• the process for allocating prices and commissions for block trades that are filled in different lots and/or at different prices

• policies on filling clients' trades before filling accounts of proprietary or personal accounts when blocked trades are partially filled

3. KYC and suitability information

ICPMs are required to collect and document current KYC information so they can assess the general investment needs of their clients and the suitability of proposed transactions (see section 1.5 of OSC Rule 31-505 -- Conditions of Registration (OSC Rule 31-505)). ICPMs should collect and document client information such as investment objectives, risk tolerance, investment restrictions, investment timeframe, annual income and net worth.

During our reviews, we observed the following:

• No KYC and suitability information was collected or documented.

• KYC information was incomplete.

• KYC information was not updated periodically.

• KYC information was not formally documented.

• Written policies and procedures on collecting and documenting KYC and suitability information did not reflect actual practices.

Suggested practices

• Collect complete KYC information for all clients, including clients who buy non-prospectus qualified investment offerings.

• Update KYC information at least once a year.

• Ensure that clients sign the KYC form.

• Maintain a pending file for incomplete KYC forms and clear them on a timely basis, in particular before executing any trades for the client.

4. Marketing

All marketing materials must include information that is accurate, complete and not misleading to clients. Subsection 2.1(1) of OSC Rule 31-505 requires ICPMs to deal fairly, honestly, and in good faith with clients.

During our reviews, we observed the following:

• Internal marketing requirements were not met (e.g. procedures in policies and procedures manual were not followed).

• Marketing materials had incorrect information (e.g. incorrect data or statistics).

• Marketing materials had not been reviewed or approved.

• There was no disclosure to clients about whether performance returns were calculated gross or net of fees.

• Returns were compared to inappropriate benchmarks or there was inadequate disclosure about relevant differences between benchmarks and the investment strategies.

• Composites were not constructed properly, for example, all relevant accounts in a composite were not included or new accounts were not included in a composite on a timely basis.

• Marketing materials included claims of compliance with the Global Investment Performance Standards (GIPS) when not all of the requirements were met.

• Exaggerated and/or unsupported claims were made in marketing materials.

Suggested practices

• Update marketing material regularly to ensure all information is complete, accurate and not misleading to clients.

• Establish and enforce procedures for preparing, reviewing and approving marketing materials.

• Establish guidelines on preparing performance data, using benchmarks and constructing composites.

• Require someone not involved in preparing marketing materials to review and approve the content for accuracy and compliance with securities legislation.

5. Portfolio management, including advisory contracts

Section 1.2 of OSC Rule 31-505 requires ICPMs to develop written procedures for dealing with clients. The written procedures should conform to prudent business practice and enable ICPMs to serve their clients adequately. This includes advisory agreements for portfolio management of discretionary accounts and for portfolio management activities that advisers perform on behalf of their clients.

Advisory agreements should contain adequate disclosure of all material facts, including the responsibilities of each party, the client's investment objectives and restrictions, the timing and billing of fees, the degree of discretion in managing client assets and terms for ending the agreement.

During our reviews, we observed the following:

• There were no advisory agreements with clients.

• The client's investment objectives and restrictions were not documented.

• Portfolio holdings were inconsistent with the stated investment restrictions.

• Responsibility for voting client proxies was not addressed.

• Responsibility for insider reporting or early warning reporting on the client's behalf was not addressed.

• No written consent was obtained for investments in issuers where responsible persons are directors or officersof the issuers of the issuers.

Suggested practices

• Have clients sign advisory agreements before ICPMs begin managing the account.

• Update advisory agreements when terms change.

• Include details about the roles and responsibilities of each party in advisory agreements.

• Review client holdings frequently to ensure that they are consistent with stated investment objectives and restrictions.

• Obtain written consent from the client before investing in issuers where responsible persons are directors or officers.

6. Statement of policies

ICPMs are required to disclose certain relationships when they provide advice relating to their own securities or to securities of certain issuers who are connected or related to them. Every registrant is required to include this disclosure in a statement of policies. Regulation 223 requires that registrants prepare and file a statement of policies with the OSC and provide a copy to their clients.

During our reviews, we observed the following:

• There was no statement of policies.

• The most current statement of policies was not filed with the OSC or provided to clients, or both.

• ICPMs did not describe their policies regarding their activities as an adviser on securities of related issuers and in the course of distribution, securities of connected issuers.

• ICPMs did not list related issuers who were reporting issuers.

• ICPMs did not adequately describe the nature of their relationships with related issuers that are reporting issuers.

Suggested practices

• Prepare and file a current statement of policies with the OSC and distribute it to all clients.

• If a significant change occurs, file a revised statement of policies with the OSC and distribute it to all clients.

• Include in the statement of policies a complete listing of all related issuers that are reporting issuers and a concise description of the nature of the relationship with each related issuer.

• Include in the statement of policies the disclosure required in Regulation 223(1)(d) in bold type.

7. Policies and procedures manual

Section 1.2 of OSC Rule 31-505 requires ICPMs to establish and enforce written policies and procedures that will enable them to serve their clients adequately. ICPMs are required to maintain a policies and procedures manual, which also includes all relevant regulatory requirements.

During our reviews, we observed the following:

• The procedures used in practice were inconsistent with the procedures outlined in the manual.

• The procedures outlined in the manual did not apply to the type of business conducted (i.e. they were generic and were not customized to the ICPM's business).

• Procedures for key areas of the business were missing.

• There was insufficient detail about policies and procedures.

Suggested practices

Policies and procedures that are clearly documented and enforced contribute to a strong compliance environment. ICPMs should establish and enforce written policies and procedures that are sufficiently detailed and cover all areas of their business. ICPMs should also regularly evaluate, review and update their policies and procedures for changes in industry practice or securities legislation. A copy of the manual should be readily accessible by all employees of the ICPM.

The following is a list of topics and guidelines that should be included in a standard manual:

Marketing

• how to prepare, review and approve marketing materials to prevent false or misleading statements and to ensure compliance with securities legislation

• how to prepare performance data, use benchmarks and construct composites to be used in marketing materials

• procedures for ensuring:

- marketing materials are reviewed and approved by someone other than the preparer

- compliance with securities legislation, including prohibitions on holding out a non-registered person as being registered, on advertising of registration, representations that the OSC has endorsed the financial standing, fitness or conduct of any registrant

Portfolio management

• how to collect and document client KYC and suitability information and how frequently it should be updated

• guidance on proxy voting to deal with issues such as executive compensation (e.g. stock options), take-over protection (poison pills) and acquisitions

• procedures to ensure compliance with clients' specified investment restrictions or other instructions

• guidelines on:

- performing sufficient research to support investment decisions

- supervising sub-advisers and associate portfolio managers

• procedures for ensuring:

- that investments and trades are suitable for each client

- compliance with regulatory and other investment restrictions, for example NI 81-102

Trading and brokerage

• guidelines on:

- how brokers are selected

- soft dollar arrangements with brokers

• policies for:

- obtaining best price and best execution for clients

- allocating investment opportunities fairly among client accounts

- executing trades in a timely manner and according to instructions

• procedures for monitoring and resolving failed trades and trading errors

Personal trading and conflicts of interest

• procedures for approving personal trades, including requiring written pre-approval

• definition of material non-public information

• policies and procedures to restrict the dissemination of any non-public information

Referral arrangements

• criteria used for setting up referral arrangements

• procedures for reviewing and approving referral arrangements before they are signed

• guidelines for ensuring that clients receive appropriate and adequate disclosure of referral arrangements

Money laundering prevention

• definition of "money laundering" and examples of suspicious transactions

• handling of prescribed and suspicious transactions

• procedures to report prescribed and suspicious transactions to the Financial Transactions and Reports Analysis Centre of Canada

• documenting the records that should be maintained under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act and Regulations, and the period for which these records should be maintained

• establishing a compliance regime to ensure you meet your obligations under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act and Regulations

Compliance and supervision structure

• handling of client complaints

• opening and closing of client accounts

• insider and early warning reporting, including collecting and updating clients' status as insiders of reporting issuers

• identification, monitoring and resolution of client complaints

• dealing with clients resident in jurisdictions where their adviser is not registered

• preparation, review and monitoring of monthly capital calculations

• guidelines on the maintenance of books and records

8. Personal trading

ICPMs are required to establish and enforce written procedures on dealing with clients. These procedures must conform to prudent business practice.

The establishment and enforcement of a policy on the personal trading of all employees is a prudent business practice. This ensures compliance with Part XXI - Insider Trading and Self-Dealing of the Act and helps prevent and detect conflicts of interest and abusive practices. For example, under section 119 of the Act, no person can purchase or sell securities for his or her account where a client's investment portfolio holds the same security and where the person has information relating to the securities and uses the information to his or her benefit or advantage.

In this report, employees who have access to investment information about client portfolios are referred to as "access persons".

During our reviews, we observed the following:

• There were no personal trading policies.

• Personal trades did not require pre-clearance.

• Employees were not required to sign a code of ethics or annual certification of compliance with the code.

• Individuals with access to investment decision making were not subject to personal trading policies.

• There was no evidence that personal trading had been reviewed.

• Personal trading policies and procedures were not adequately enforced.

Suggested practices

• Distribute clear personal trading restrictions and reporting obligations to all employees and access persons.

• Develop and implement personal trading policies.

• Include blackout periods, the requirement for pre-approval of all personal trades and a timely review of brokerage statements in personal trading procedures.

• Require all access persons to acknowledge every year in writing that they understand and will follow the firm's personal trading policies.

• Require all access persons to direct their brokers to send statements of their accounts directly to the officer responsible for monitoring the personal trading policy.

• Maintain a record of personal trade pre-approvals and brokerage statements of access persons as proof that personal trading is being monitored.

• Have the Compliance Officer review and oversee all personal trading records.

9. Capital calculations

ICPMs are required to prepare monthly calculations of minimum free capital and capital required within a reasonable period of time after each month end (see paragraph 10 of Regulation 113(3)). Capital calculations must be based on monthly financial statements prepared in accordance with generally accepted accounting principles (GAAP). If an ICPM becomes capital deficient, it is required to inform the OSC immediately and to correct the capital deficiency within 48 hours.

Our practice is to impose terms and conditions on all registrants that are identified as capital deficient. This includes providing us with unaudited financial statements and capital calculations each month.

During our reviews, we observed the following:

• Capital calculations were not prepared monthly or were not prepared on a timely basis. This suggested that the firm was not regularly monitoring its capital.

• Capital calculations were incorrect.

• The insurance deductible on the financial institution bond was not included in the calculation or was incorrect.

• The minimum capital deduction was incorrect.

• Financial statements were not prepared in accordance with GAAP.

• There was no evidence that someone other than the preparer reviewed the calculation.

• Copies of monthly capital calculations were not maintained.

• ICPMs were capital deficient for a period of time.

Suggested practices

• Calculate the capital position monthly and base it on financial statements prepared in accordance with GAAP.

• Maintain copies of the calculations.

• Have someone other than the preparer review the calculations to ensure they are accurate. Keep a record of the review.

• Inform the OSC immediately if the ICPM's capital position becomes deficient or it repays subordinated debt.

10. Registration issues

Paragraph (1)(c) of section 25 of the Act states that no person or company shall act as an adviser unless registered to do so. ICPMs are responsible for ensuring that they maintain appropriate registration for the activities conducted.

ICPMs are required to notify the OSC of any change in the status of directors and/or officers within five business days. ICPMs are also required to notify the OSC of the opening of any office or branch, and of any changes in the status of the compliance officer, portfolio managers and representatives. Multilateral Instrument 33-109 -- Registration Information sets out the requirements for changes to registered firm and individual information.

During our reviews, we observed the following:

• Affiliated entities of the ICPMs were performing advisory activities but were not registered.

• Portfolio managers, representatives or compliance officers were not registered with the OSC.

• The OSC was not notified of changes in registration.

• Trade names or parent company names were used in signage, correspondence, business cards and marketing materials without notifying the OSC.

• ICPMs were performing activities that require registration as an LMD, but were not registered as an LMD.

• ICPMs had advisory clients in jurisdictions where they were not registered and had not taken appropriate steps to determine whether they required registration in those jurisdictions.

Suggested practices

• Promptly notify the OSC of all changes to registration.

• Promptly register branch office locations.

• Notify the OSC when trade names are used.

• Ensure that individuals who provide advice to others are appropriately registered as portfolio managers.

7. Significant ICPM deficiencies

As noted in our 2006 annual report, we have made several enhancements to our deficiency reports. One of the major changes was identifying significant deficiencies in reports issued after April 1, 2005 (fiscal 2005-06). This information is intended to assist senior management of the ICPM in focusing on the key issues. It also highlights the areas of regulatory concern so we can take appropriate action to improve compliance.

We have established various criteria to assess whether a deficiency is significant, including:

• risk to client assets

• conflicts of interest

• misleading information to clients

• ineffective compliance structure

We also take into account other factors, including:

• current issues, such as best execution and referral arrangements

• the frequency of findings

• the impact of the deficiency on the market participant's operations

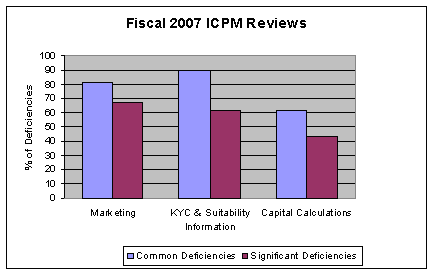

The field reviews of ICPMs in fiscal year 2007 resulted in an average of 17 deficiencies per review. An average of six or 35% of these deficiencies were identified as significant.

The following chart shows the top three significant deficiencies of ICPMs for the year ended March 31, 2007 and the corresponding frequency of common deficiencies{4}. For suggested practices, please refer to section 6 of this report.

We only showed the top three significant deficiencies as the percentages were relatively higher than other deficiencies category. Please also note that the top three significant deficiencies are not the same as the top three common deficiencies. As mentioned above, we applied various criteria and professional judgment when determining whether a deficiency should be identified as significant.

Note: The percentage of deficiencies is calculated based on the ICPM reviews we performed during fiscal 2007 and does not represent the whole ICPM population.

1. Marketing

Marketing still remains the top significant deficiency. We found issues in the following major areas during our field reviews:

(a) Improperly constructed performance composites. Some ICPMs did not have adequate procedures and controls for ensuring that performance composites are constructed consistently and accurately. For example, ICPMs did not include all clients with the same investment strategy in the composite and they tended to "cherry pick" the accounts included in the performance composites. In addition, there was no disclosure about whether the performance returns were calculated gross or net of fees.

(b) Inappropriate use of benchmarks. Some ICPMs compared the return of their funds or accounts to benchmarks that were inappropriate or not relevant. For example, they used benchmarks that differed significantly from the composition and investment strategy of their funds or accounts without adequate disclosure to make the comparison fair and not misleading.

(c) Linking performance returns of other funds. Some ICPMs presented and linked the performance returns of a sample of managed accounts with another fund with similar investment objectives and risks that the ICPM managed. They used different methods of calculating returns for the managed accounts and the fund but linked the returns together as if they were the fund's returns. It is misleading to present and link these returns in the same graph because it appears that the track record for the fund is longer than it is.

(d) Exaggerated claims. Some marketing materials contained exaggerated claims about the ICPM's skills, performance or services. For example, statements such as "our investment experience and qualifications are outstanding" and "superior performance" were made in marketing materials. These claims were made without adequate support to ensure that clients were not misled by the claims.

Our response

Marketing remains the top significant deficiency. Some of the marketing issues we identified in our field reviews (noted above) are consistent with our findings in the marketing sweep. To improve compliance, we will be issuing an industry report in the near future on the results of our marketing sweep. The report will summarize our key findings and provide guidance to the industry on best practices. We strongly encourage ICPMs to look to the industry report to enhance compliance.

2. KYC and suitability information

We identified significant deficiencies in the area of KYC and suitability information. Examples included:

• Not collecting and documenting sufficient KYC and suitability information from clients, for example, investment objectives, risk tolerance and time horizon.

• ICPMs did not have a written investment mandate with clients and we could not determine whether the managed portfolios were suitable for clients.

• KYC information was not updated to reflect changes in clients' investment objectives, risk tolerance and financial condition.

We will continue to monitor and to focus on these areas in our regular compliance reviews.

3. Capital calculations

We identified significant deficiencies in the area of capital calculations. As mentioned in section 6, this year we focused our ICPM reviews on smaller registrants with assets under management of less than $250 million. We found that some ICPMs did not prepare monthly capital calculations. Some ICPMs were capital deficient in a number of instances during the review period and they did not notify the OSC immediately. To address this issue, we imposed terms and conditions on these registrants and required them to file monthly unaudited financial statements and capital calculations with the Compliance team. We will closely monitor these ICPMs to ensure compliance.

We will continue to monitor and to focus on these areas in our regular compliance reviews.

8. Addressing the deficiencies

At the end of each review, we issue a deficiency report identifying areas of non-compliance with securities law. A market participant has 30 days to respond to our report. The written response should set out the steps that the market participant will take, or has taken, to address the deficiencies. If we are not satisfied with the response, we will send follow-up letters until all matters are resolved. When we are satisfied, we issue a closing letter to the market participant, which concludes the field review process. However, there are situations where a report alone may not be adequate to address the deficiencies.

Depending on the severity of issues identified, we may use one or more of the following regulatory tools:

• closely monitor the market participant

• hold an examination of the registrant under Section 31

• impose terms and conditions on registration

• refer the matter to Enforcement for further follow up and appropriate action

During the past fiscal year, the majority of our reviews were resolved to our satisfaction. To a limited extent, we also imposed terms and conditions on registration or referred the matter to Enforcement.

9. Seeking input from our market participants

We recognize the importance of seeking input from our market participants and value their feedback. Over the past few years, we have consulted with our market participants on how we can improve our field review process. Last year, we introduced a more formal process with surveys.

In October 2006, we sent a survey to all ICPMs and asked them for input on our 2006 report on the following areas:

• content and clarity

• usefulness of the annual report

• new areas to be included in the annual report

• areas for improvement

We also asked ICPMs we reviewed in the prior two years to give us suggestions on how we can enhance or improve our compliance field review process.

We received very positive feedback from ICPMs on the content of our report and its usefulness in enhancing compliance. Some ICPMs suggested that a section on new and proposed rules would be helpful to them, which we incorporated into this year's annual report.

In January 2007, we started sending a survey to market participants after their field review. The purpose of the survey is to seek further input on our field review process. Although response to our survey is voluntary, we strongly encourage you to provide us with your input so that we can continue to improve our regulatory services.

Contact information

For more information, please contact:

|

Carlin Fung, CA

|

|

|

Senior Accountant, Compliance

|

phone (416) 593-8226

|

|

|

|

|

Dave Santiago, CA

|

|

|

Accountant, Compliance

|

phone (416) 593-8284

|

|

|

|

|

Marrianne Bridge, CA

|

|

|

Manager, Compliance

|

phone (416) 595-8907

|

|

|

|

|

August 24, 2007

|

|

{1} The median assets under management of the ICPMs that we reviewed for 2007 was $113 million, 2005/2006 was $136 million, 2004 was $205 million and 2003 was $1.5 billion.

{2} We also identified issues in many other areas, including statement of client's portfolio, conflicts of interest, cross transactions, soft dollars, related registrant disclosure, annual consent to trade securities of related and connected issuers, compliance function, adhering to the terms and conditions of registration, insurance coverage, exempt securities, early warning and insider trading reporting, proxy voting, referral arrangements, United Nations Suppression of Terrorism monthly reporting, internal controls, segregation of duties, trust accounts, agreements with service providers, confidentiality agreements and "holding out" issues.

{3} We combined the results for fiscal years 2005 and 2006 in this report.

{4} In our 2006 annual report, the top three significant deficiencies were marketing, personal trading, and KYC and suitability information.