Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

OSC Notice & Request for Comment-Proposed OSC Rule 81-502 Restrictions on the Use of the Deferred Sales Charge Option for Mutual Funds & Proposed CP 81-502 to OSC Rule 81-502 Restrictions on the Use of the DSC Option for Mutual Funds & Related Amendments

OSC Notice & Request for Comment-Proposed OSC Rule 81-502 Restrictions on the Use of the Deferred Sales Charge Option for Mutual Funds & Proposed CP 81-502 to OSC Rule 81-502 Restrictions on the Use of the DSC Option for Mutual Funds & Related Amendments

ONTARIO SECURITIES COMMISSION NOTICE AND REQUEST FOR COMMENT

PROPOSED ONTARIO SECURITIES COMMISSION RULE 81-502

RESTRICTIONS ON THE USE OF THE DEFERRED SALES CHARGE OPTION FOR MUTUAL FUNDS

AND

PROPOSED COMPANION POLICY 81-502 TO

ONTARIO SECURITIES COMMISSION RULE 81-502

RESTRICTIONS ON THE USE OF THE DEFERRED SALES CHARGE OPTION FOR MUTUAL FUNDS

AND

RELATED CONSEQUENTIAL AMENDMENTS

February 20, 2020

Introduction

The Ontario Securities Commission (the OSC or we) are publishing for comment:

• proposed Ontario Securities Commission Rule 81-502 Restrictions on the Use of the Deferred Sales Charge Option for Mutual Funds (the Proposed Rule),

• proposed Companion Policy 81-502CP to Ontario Securities Commission Rule 81-502 Restrictions on the Use of the Deferred Sales Charge Option for Mutual Funds (the Proposed CP), and

• proposed consequential amendments to National Instrument 81-105 Mutual Fund Sales Practices (the Proposed Consequential Amendments).

The text of the Proposed Rule, Proposed CP and Proposed Consequential Amendments are contained in Annexes A to C of this notice and will also be available on the OSC website at <<www.osc.gov.on.ca>>.

Substance and Purpose

The purpose of the Proposed Rule is to implement the OSC's policy response to address the investor protection issues arising from the use of the deferred sales charges option (DSC option){1} in the sale of mutual fund securities. The Proposed Rule introduces restrictions on the use of the DSC option that are designed to mitigate potential negative investor outcomes. In particular, the restrictions are intended to address the "lock-in"{2} effect associated with the DSC option and reduce the potential for mis-selling, while allowing dealers to offer the DSC option to clients with smaller accounts.

The Proposed CP explains the Proposed Rule.

Background

The 2018 Consultation

On September 13, 2018, the Canadian Securities Administrators (the CSA) published for comment proposed amendments to National Instrument 81-105 Mutual Fund Sales Practices (NI 81-105) that would prohibit:

• the payment of upfront sales commissions by fund organizations to dealers, and in so doing, discontinue sales charge options that involve such payments, such as all forms of the DSC option (DSC ban), and

• trailing commission payments by fund organizations to dealers who do not make a suitability determination, such as order-execution-only (OEO) dealers (OEO trailer fee ban)

(collectively, the 2018 Consultation).

CSA Staff Notice 81-332

On December 19, 2019, the CSA published CSA Staff Notice 81-332 Next Steps on Proposals to Prohibit Certain Investment Fund Embedded Commissions to announce that final amendments to implement a DSC ban will be published in early 2020. The OSC stated that, while it will participate in the OEO trailer fee ban, it will not be implementing a DSC ban.

OSC Staff Notice 81-730

Also, on December 19, 2019, the OSC published OSC Staff Notice 81-730 Consideration of Alternative Approaches to Address Concerns Related to Deferred Sales Charges to announce that the OSC will explore alternative approaches for addressing the investor protection concerns arising from the use of the DSC option.

Summary of Comments Received on the 2018 Consultation

On February 20, 2020, the CSA, with the exception of Ontario, published Multilateral CSA Notice of Amendments to National Instrument 81-105 Mutual Fund Sales Practices, Changes to Companion Policy 81-105CP to National Instrument 81-105 Mutual Fund Sales Practices and Changes to Companion Policy 81-101CP to National Instrument 81-101 Mutual Fund Prospectus Disclosure relating to Prohibition of Deferred Sales Charges for Investment Funds (the 2020 Multilateral CSA Notice). Please refer to the 2020 Multilateral CSA Notice for a summary of comments received on the 2018 Consultation.

Summary of the Proposed Rule

As discussed above, the Proposed Rule introduces restrictions on the use of the DSC option that are designed to mitigate negative investor outcomes. The following chart sets out the Proposed Rule section reference, along with the corresponding restrictions and the policy rationale for each restriction.

Investment Fund Manager Restrictions

|

Proposed Rule Section Reference |

Description |

Policy Rationale |

|

|

||

|

1. Section 3(a)(i) |

Maximum term of DSC redemption fee schedule limited to 3 years |

Reduce the negative implications of the lock-in feature associated with the DSC option by shortening the maximum term during which a redemption fee can be applied. The proposed term limit represents a significant reduction compared to current industry practice where the maximum term can be up to 7 years. |

|

|

||

|

2. Section 3(a)(ii) |

Clients can redeem 10% of the value of their investment without redemption fees annually, on a cumulative basis |

Reduce the negative implications of the lock-in feature associated with the DSC option by ensuring that clients have the ability to redeem a portion of their investment without incurring fees. This codifies a general industry practice, but we are also requiring the "free redemption amount" to be cumulative in order to provide greater flexibility for investors. |

|

|

||

|

3. Section 3(a)(iii) |

Separate DSC series |

Prevents potential for cross-subsidization by ensuring that investors who purchase on a no-load or front-end sales charge basis do not indirectly incur costs related to financing the upfront commissions typically associated with the DSC option. This could result in lower management fees for standalone no-load or front-end sales charge series. |

Dealer Restrictions

|

Proposed Rule Section Reference |

Description |

Policy Rationale |

|

|

||

|

1. Section 3(b)(i) |

No sales of the DSC option to clients aged 60 and over |

Reduces potential for mis-selling by requiring dealers to avoid use of the DSC option when making recommendations to seniors. |

|

|

||

|

2. Section 3(b)(ii) |

Maximum client account size of $50k |

Limits use of the DSC option to clients with smaller accounts. |

|

|

||

|

3. Section 3(b)(iii) |

No sales of the DSC option to clients whose investment time horizon is shorter than the DSC schedule |

Prevents potential for mis-selling by requiring dealers to adequately consider time horizon as part of the KYC process in order to ensure that recommendations made are suitable for the client. |

|

|

||

|

4. Section 3(b)(iv)(A) |

Client cannot use borrowed money to purchase mutual funds with the DSC option |

Prevents clients from having to incur redemption fees in the event they need to redeem their investment to repay loans used to fund their purchase. |

|

|

||

|

5. Section 3(b)(iv)(B) |

Upfront commissions only for new contributions to a client's account |

Prevents dealers from engaging in unnecessary trading in a client's account where the purpose of those transactions would be solely to earn additional upfront commissions. |

|

|

||

|

6. Section 3(b)(iv)(C) |

No upfront commissions on reinvested distributions |

Prevents dealers from earning additional upfront commissions on distributions of investments where upfront commissions were previously paid. |

|

|

||

|

7. Section 3(b)(v) |

No redemption fees applicable to investor redemptions upon: |

Allows clients to redeem their mutual fund investment in financial hardship circumstances without being negatively impacted by redemption fees. |

|

|

(a) Death of client, |

|

|

|

(b) Involuntary loss of full-time employment, |

|

|

|

(c) Permanent disability, and |

|

|

|

(d) Critical illness. |

|

The Proposed CP

Short-Term Trading Fees

The Proposed CP clarifies that the Proposed Rule does not restrict investment fund managers from using redemption fees or penalties payable to the fund as part of policies aimed at protecting mutual fund investors in cases such as short-term trading.

Conflict of Interest Rules under National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103)

We are of the view that there is an inherent conflict of interest for registrants to accept upfront commissions associated with the sale of mutual fund securities under the DSC option.

We expect registered firms to address this conflict consistent with the requirements under NI 31-103 by implementing policies and procedures sufficient to mitigate the risk to clients' interests and to closely monitor for compliance with (i) these policies and procedures, (ii) the Proposed Rule, if and when it comes into force, and (iii) their obligations when making suitability determinations.

The Proposed Consequential Amendments

The Proposed Consequential Amendments in Annex C are the same as the final amendments to NI 81-105 published with the 2020 Multilateral CSA Notice. Comments on the Proposed Consequential Amendments are not being sought as these amendments have no impact in Ontario. The Proposed Consequential Amendments will be published as part of the final amendments to implement the Proposed Rule in Ontario for harmonization purposes.

Anticipated Costs and Benefits of the Proposed Rule

In Annex E, we provide a regulatory impact analysis of the anticipated costs and benefits of the Proposed Rule.

Transition

We expect that registrants will require some time to operationalize the Proposed Rule. At this time, we anticipate that the Proposed Rule would apply from June 1, 2022. This date coincides with the effective date of the DSC ban that will be implemented by the CSA jurisdictions, other than Ontario.

Unpublished Materials

In developing the Proposed Rule, we have not relied on any significant unpublished study, report or other written materials.

Request for Comments

We welcome your comments on the Proposed Rule, the Proposed CP and the specific consultation questions related to the Proposed Rule. We cannot keep submissions confidential because securities legislation requires publication of a summary of written comments received during the comment period. All comments received will be posted on the website of the Ontario Securities Commission at www.osc.gov.on.ca. Therefore, you should not include personal information directly in comments to be published. It is important you state on whose behalf you are making the submissions.

Deadline for Comments

Please submit your comments in writing on or before May 21, 2020. If you are not sending your comments by email, please send a USB flash drive containing the submissions (in Microsoft Word format).

Where to Send Your Comments

Address your submission to the Ontario Securities Commission. Deliver your comments to the address below:

The SecretaryOntario Securities Commission20 Queen Street West22nd FloorToronto, Ontario M5H 3S8Fax: (416) 593-2318

Contents of Annexes

The text of the Proposed Rule, Proposed CP, Proposed Consequential Amendments is contained in the following annexes to this Notice and is available on the OSC website:

Annex A: Proposed Rule

Annex B: Proposed CP

Annex C: Proposed Consequential Amendments

Annex D: Specific Consultation Questions Relating to the Proposed Rule

Annex E: Regulatory Impact Analysis of the Proposed Rule to Address Concerns Related to Deferred Sales Charges

Annex F: Local Information

Questions

Please refer your questions to any of the following:

Stephen PagliaManager, Investment Funds and Structured Products BranchOntario Securities Commission(416) 593-2393Irene LeeSenior Legal Counsel, Investment Funds and Structured Products BranchOntario Securities Commission(416) 593-3668

{1} Under the traditional deferred sales charge option, the investor does not pay an initial sales charge for fund securities purchased but may have to pay a redemption fee to the investment fund manager (i.e. a deferred sales charge) if the securities are sold before a predetermined period of typically 5 to 7 years from the date of purchase. Redemption fees decline according to a redemption fee schedule that is based on the length of time the investor holds the securities. While the investor does not pay a sales charge to the dealer, the investment fund manager pays the dealer an upfront commission (typically equivalent to 5% of the purchase amount). The investment fund manager may finance the payment of the upfront commission and accordingly incur financing costs that are included in the ongoing management fees charged to the fund. The low-load purchase option is a type of deferred sales charge option but has a shorter redemption fee schedule (usually 2 to 4 years). The upfront commission paid by the investment fund manager and redemption fees paid by investors are correspondingly lower than the traditional deferred sales charge option.

{2} The "lock-in" feature refers to the redemption fee schedule associated with the DSC option which has the potential to deter investors from redeeming an investment or changing their asset allocation, even in the face of consistently poor fund performance, unforeseen liquidity events, or changes in their financial circumstances.

ANNEX A

PROPOSED ONTARIO SECURITIES COMMISSION RULE 81-502 RESTRICTIONS ON THE USE OF THE DEFERRED SALES CHARGE OPTION FOR MUTUAL FUNDS

Definitions

1.

(1) In this Rule,

"a member of the organization" for a mutual fund has the same meaning as in National Instrument 81-105 Mutual Fund Sales Practices;

(2) Terms defined in National Instrument 81-102 Investment Funds and used in this Rule have the respective meanings ascribed to them in National Instrument 81-102 Investment Funds.

Application

2. This Rule applies to

(a) a distribution of securities of a mutual fund that offers or has offered securities under a prospectus or simplified prospectus in the period throughout which the mutual fund is a reporting issuer; and

(b) a person or company in respect of activities in that period pertaining to a mutual fund referred to in paragraph (a).

Restrictions on the Use of Deferred Sales Charge Option for Mutual Funds

3. Despite section 3.1 of National Instrument 81-105 Mutual Fund Sales Practices,

(a) a member of the organization for a mutual fund must not pay to a dealer a commission in money for the distribution of security of the mutual fund made through the dealer, if any of the following apply:

(i) a fee or charge may be collected by a member of the organization for the mutual fund on a redemption of the security that occurs more than 3 years after the date of the distribution;

(ii) the client is not provided an opportunity in a calendar year to redeem at no cost at least the total of

(A) 10% of the number of securities that would otherwise be subject to a fee or charge upon redemption in the calendar year, and

(B) for each preceding calendar year, the amount, if any, by which

(I) 10% of the number of securities that would otherwise be subject to a fee or charge on redemption in the preceding calendar year

exceeds

(II) the number of securities that the client redeemed in the preceding calendar year;

(iii) the security is not in a separate series or class of securities of the mutual fund that are subject to a fee or charged on redemption; and

(b) a dealer must not accept a commission from a member of the organization of a mutual fund a commission in money for the distribution of securities of a mutual fund made through the dealer, if any of the following apply:

(i) the dealer knows or reasonably ought to know that the client is 60 years of age or over at the time of distribution;

(ii) the dealer knows the balance in the client's account immediately after the distribution would be in excess of $50,000;

(iii) at the time of the distribution, the dealer knows or reasonably ought to know that the client likely would need to redeem the security at any time during the period in which a fee or charge would be payable on the redemption of the securities;

(iv) at the time of the distribution, the dealer knows or reasonably ought to know that the source of funds to be used to purchase the security consists of

(A) borrowed money;

(B) money from the redemption of securities that had been subject to a redemption fee or could have been subject to a redemption fee if the securities had been redeemed earlier; or

(C) reinvestment of distributions received on securities that are subject to a redemption fee or had been subject to a redemption fee;

(v) at the time of distribution, the dealer does not have a policy that would compel the dealer to reimburse a fee to the client for a redemption of the security in the event that the redemption occurs after the death of the client or after one of the following events:

(A) the involuntary loss of full-time employment by the client,

(B) the client becomes subject to an impairment entitling the client to a tax credit under subsection 118.3(1) of the ITA,

(C) the client begins to suffer a critical illness such that the client has a high risk of dying in the next year as a result of illness, injuries, or any combination of illnesses and injuries.

Exemption

4. The Director may grant an exemption from the provisions in this Rule, in whole or in part, subject to such condition or restriction as may be imposed in the exemption.

Effective Date

5. This Rule comes into force on June 1, 2022.

ANNEX B

PROPOSED COMPANION POLICY TO ONTARIO SECURITIES COMMISSION RULE 81-502 RESTRICTIONS ON THE USE OF THE DEFERRED SALES CHARGE OPTION FOR MUTUAL FUNDS

Short-Term Trading Fees

1. Section 3 of the Rule does not restrict the investment fund manager from adopting policies and procedures that deter short term or excessive trading, or that minimize the potential impact of sizable transactions. More specifically, short term-trading fees or penalties on large redemptions that are charged to investors and collected for the benefit for the mutual fund would not be caught by section 3 of the Rule since no amount would be payable to the investment fund manager.

Conflict of Interest Rules in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations

2. We are of the view that there is an inherent conflict of interest for registrants to accept upfront commissions associated with the sale of mutual fund securities under the deferred sales charge option.

We expect registered firms to address this conflict consistent with the requirements under National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations by implementing policies and procedures sufficient to mitigate the risk to clients' interests and to closely monitor for compliance with (i) these policies and procedures, (ii) the Rule, and (iii) their obligations when making suitability determinations.

3. This Companion Policy becomes effective on June 1, 2022.

ANNEX C

PROPOSED AMENDMENTS TO NATIONAL INSTRUMENT 81-105 MUTUAL FUND SALES PRACTICES

1. National Instrument 81-105 Mutual Fund Sales Practices is amended by this Instrument.

2. Section 1.1 is amended in paragraph (d) of the definition of "member of the organization" by adding "associate or" before "affiliate".

3. Section 3.1 is amended

(a) by renumbering section 3.1 as subsection 3.1(1), and

(b) by adding the following subsection:

(2) Subsection (1) does not apply to a distribution of a security of a mutual fund to a client resident in British Columbia, Alberta, Saskatchewan, Manitoba, Quebec, New Brunswick, Nova Scotia, Newfoundland and Labrador, Prince Edward Island, Northwest Territories, Nunavut and Yukon..

4. This Instrument comes into force on June 1, 2022.

ANNEX D

SPECIFIC CONSULTATION QUESTIONS RELATING TO THE PROPOSED RULE

1. On January 10, 2017, the Canadian Securities Administrators (the CSA) published for comment CSA Consultation Paper 81-408 Consultation on the Option of Discontinuing Embedded Commissions (the Consultation Paper). The Consultation Paper stated that some investors may indirectly subsidize certain dealer compensation costs that are not attributable to their investment in the fund, which means they indirectly pay excess fees{1}. As an example of this "cross-subsidization", the Consultation Paper made reference to the financing costs incurred by investment fund managers in connection with the payment of the upfront commission to dealers that is typically associated with the DSC sales charge option. This financing cost could be embedded in a mutual fund's management fee, which would result in some investors in a fund, such as the front-end load investors, cross-subsidizing the costs attributable to DSC investors in the fund. As a result, we are proposing to require the DSC sales charge option to be included in a separate series of the fund, which would have its own management fee. We note that some investment fund mangers already use this practice. Do you agree that mandating a separate DSC series will help in curtailing the cross-subsidization of the costs attributable to DSC investors? Why or why not?

2. The effective date of the Proposed Rule coincides with the effective date of the final amendments to implement a DSC ban in the other CSA jurisdictions. Are there additional transition issues that we should consider?

3. Annex E sets out the anticipated costs and benefits of the Proposed Rule. Are there any other significant costs or benefits that have not been identified in this analysis? Please explain with concrete examples and provide data to support your views.

{1} See page 13, https://www.osc.gov.on.ca/documents/en/Securities-Category8/sn_20170110_81-408_consultation-discontinuing-embedded-commissions.pdf.

ANNEX E

REGULATORY IMPACT ANALYSIS OF THE PROPOSED RULE TO ADDRESS CONCERNS RELATED TO DEFERRED SALES CHARGES

A. Overview of investments in mutual funds

Canadians held approximately $1.6 trillion in mutual fund assets as at November 2019{1}. Ontario investors held approximately $700 billion of these assets or about 45% of all mutual fund assets in Canada{2}. We estimate that, of this amount, approximately $76 billion or 10.9% of mutual fund assets in Ontario were purchased using the deferred sales charge (DSC) option{3}.

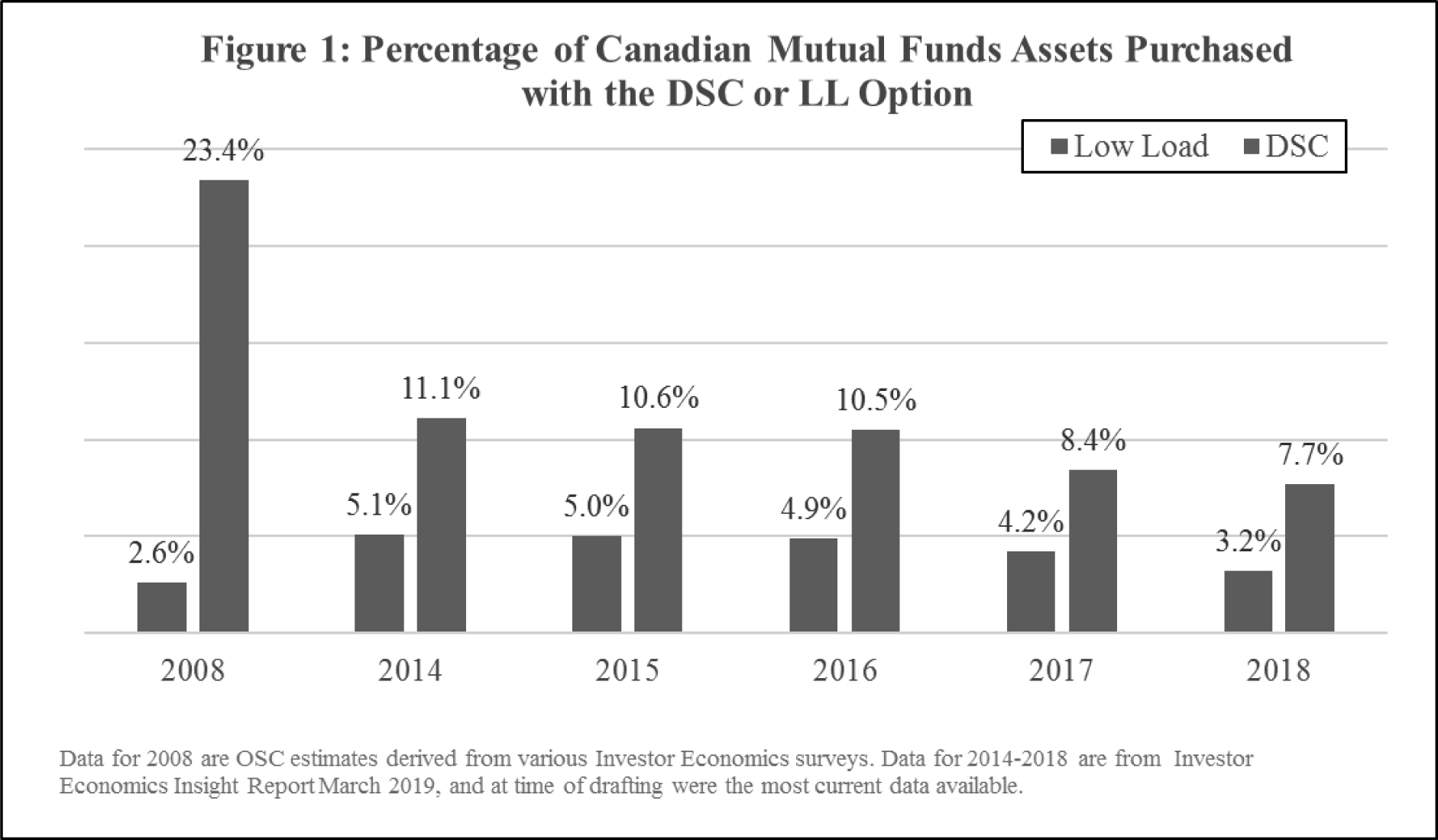

As noted in CSA Consultation Paper 81-408 Consultation on the Option of Discontinuing Embedded Commission (CP 81-408), the use of the DSC option{4} has been gradually on the decline since 2008 (Figure 1), and in the past few years several investment fund managers{5} have stopped using this type of sales charge. While the prevalence of the DSC option is declining, the continued use of this purchase option creates potential investor protection issues that require regulatory intervention.

We estimate that 38% of all households in Ontario own mutual funds{6}. Typically the DSC purchase option is used by households with an account size less than $100,000 and these sales are through dealers, primarily financial advisory firms in the MFDA channel{7}. While deposit-taker dealers{8} in the MFDA channel offer the low-load sales option, only a small share of their total assets is held in this sales option{9} as funds sold in this channel are typically sold without a sales charge.

B. Rationale for intervention

CP 81-408 examined the following two key investor protection and market efficiency issues arising from the use of embedded commissions:

• Embedded commissions raise conflicts of interest that misalign the interests of investment fund managers and dealers and representatives with those of investors, which can impair investor outcomes (conflicts of interest); and

• Embedded commissions paid generally do not align with the services provided to investors (cost and service alignment){10}.

The Proposed Rule seeks to address the negative implications of the DSC purchase option through restrictions on its use. These restrictions should address the following issues arising from the use of this specific type of embedded commission:

• The DSC option is unsuitable for a subset of investors,{11}

• Mutual fund purchases that are financed with loans and sold with the DSC option,

• It is costly for investors to redeem funds before the fee redemption schedule expires, and

• Funds may unnecessarily be churned to generate additional upfront dealer commission.

C. Proposed intervention

The Proposed Rule, if implemented, will enhance investor protection measures for those who purchase mutual funds using the DSC option. This is to be achieved by introducing the following investment fund manager and dealer restrictions.

The proposed investment fund manager restrictions are:

• Maximum DSC schedule of 3 years

• Clients can redeem 10% of the value of their investment without redemption fees annually, on a cumulative basis

• Separate DSC series

The proposed dealer restrictions are:

• No sales of the DSC option to clients aged 60 and over

• Maximum client account size of $50,000

• No sales of the DSC option to clients whose investment time horizon is shorter than the DSC schedule

• Clients cannot use borrowed money to purchase mutual funds with the DSC option

• Upfront commissions only apply for new contributions to a client's account

• No upfront commissions on reinvested dividends

• No redemption fees applicable to investor redemptions upon:

• Death of client,

• Involuntary loss of full-time employment,

• Permanent disability, and

• Critical illness.

D. Stakeholders affected by the Proposed Rule

The stakeholders who will be impacted by the Proposed Rule are investment fund managers, dealers and their registered individuals, and investors.

1. Investment Fund Managers

There are 106{12} investment fund managers managing prospectus-qualified mutual funds in Canada. We estimate that 93{13} of these investment fund managers could be impacted by the Proposed Rule because they may distribute funds that can be purchased with the DSC option.

2. Dealers

Under the Proposed Rule, only investors with an account size of $50,000 or less can purchase mutual funds using the DSC option. Investors typically need a minimum account size of $500,000{14} to access the IIROC channel and $1 million to access the private wealth management channel. However, because the DSC option is generally not used in the IIROC and private wealth management channels, we have excluded these dealer firms and their registered individuals from our analysis.

With respect to the MFDA channel, there are 91 MFDA firms and 79,580 registered individuals in Canada{15}. We estimate that 65 MFDA firms and 14,000{16} of the 18,000 registered individuals in the MFDA financial advisory channel may be affected by the Proposed Rule in Ontario. These 14,000 registered individuals have a book of business that is less than $10 million in assets under administration and tend to rely primarily on DSC commissions to finance their operations{17}. Additionally, most of their clients have account sizes less than $100,000.

3. Investors

Investors{18} may be impacted by the Proposed Rule in the following ways:

• Investors who are at least 60 years old will no longer be able to purchase mutual funds using the DSC option,

• Investors who are under 60 years old can purchase mutual funds using the DSC option but only under certain conditions,

• Investors whose account size is greater than $50,000 will no longer be able to purchase mutual funds using the DSC options,

• Investors whose account size is $50,000 or smaller can purchase mutual funds using the DSC option but only under certain conditions,

• Investors who borrow money to finance mutual fund purchases cannot use that money to purchase mutual funds using the DSC option,

• Investors with an investment time horizon that is shorter than the DSC redemption schedule cannot purchase a mutual fund using the DSC option, and

• Investors experiencing involuntary loss of full-time employment, permanent disability, critical illness or death will not have to pay redemption fees in instances where the redemption schedule has not expired.

We estimate that in Ontario between 33% and 36% of investors{19} who own mutual funds are 60 years old or older.

The $50,000 account size threshold will impact two distinct groups of investors. The first group of investors includes those whose account size is $50,000 or smaller. This group of investors can continue to purchase mutual funds with the DSC option, but only if none of the other restrictions apply to them. We estimate that 17%{20} of investors owning securities, including mutual funds, have an account size that is equal to or less than $50,000, and, the average value of their account size is $13,000{21}. The second group of investors includes those whose account size is greater than $50,000 but less than $100,000. We estimate that 28%{22} of investors owning securities, including mutual funds, belong to this market segment and the average value of their accounts is $68,000{23}. This subset of investors will no longer be able to purchase mutual funds using the DSC option. We note that the remaining 55%{24} of investors have account sizes greater than $100,000 and these investors are less likely to purchase mutual funds using the DSC option{25}.

An investor's time horizon for an investment is not static and can vary depending on changing personal and financial circumstances and investment objectives at any point in time. We anticipate that at some point during their investing life cycle, all Ontario investors purchasing a mutual fund and, in particular, older investors nearing age 60 may be impacted by the time horizon restriction.

Investors can also experience involuntary loss of full-time employment, permanent disability or critical illness or death at any point during their life. We anticipate that many Ontario investors at some point in their investing life cycle may be (positively) impacted by the financial hardship provisions. Due to limitations of the available information, we are unable to reliably estimate the proportion of investors who may experience these circumstances.

E. Benefits of Proposed Rule

In this section we present our qualitative assessment of the anticipated benefits of the Proposed Rule on investment fund managers, dealers and investors. The baseline underpinning our analysis is the current set of regulatory requirements pertaining to the distribution and sale of prospectus-qualified mutual funds in Ontario.

1. Dealers and registered individuals

Registered individuals working in the MFDA financial advisory channel will benefit from the Proposed Rule in two key ways. The Proposed Rule, by explicitly setting out some of the circumstances when the DSC option cannot be used, will aid registered individuals in making recommendations that are more likely to be suitable for their clients. For dealers, the restricted use of the DSC option will preserve recruitment and succession planning of registered individuals because registered individuals new to the business can use the revenue from DSC commissions to finance their operations{26}. This is particularly important given the significant number of registered individuals who are approaching retirement age.{27}

2. Investors

By addressing investor protection issues related to conflicts of interest and costs, the Proposed Rule is anticipated to lead to the following benefits for investors.

Investor payment option is maintained

As noted earlier in our analysis, the subset of investors who would be affected by the Proposed Rule are investors with small amounts of money to invest and who work with a registered individual in the MFDA financial advisory channel{28}. By restricting the use of the DSC option, the Proposed Rule would preserve the business model that is used to serve this segment of investors and would, in doing so, maintain payment choice{29}.

Lower redemption costs

The cost for investors of redeeming their investments before reaching the end of the redemption schedule is anticipated to decline. The elements of the proposal that should lead to this outcome are:

• The shortened redemption schedule and corresponding lower redemption fees{30},

• Restrictions on levying redemption fees in situations of financial hardship,

• The ability to redeem 10% of their investment per year without incurring redemption fees{31} and to carry forward any unused allowance.

We estimate that under various redemption scenarios, investors' redemption fee costs will decrease between 50% and 70% from today's levels. Investors may take advantage of the lower redemption costs by rebalancing their account holdings or selling underperforming funds, while the redemption schedule is still in effect, and in doing so minimize investment losses or potentially improve their investment returns{32}.

Enhanced suitability of purchases using the DSC option

The account size, age, time horizon, and leverage restrictions provide registered individuals with explicit factors that must be considered when they are assessing whether the DSC option is an appropriate payment option for their clients. By articulating some of the specific factors that must be taken into account when using the DSC option, the Proposed Rule would provide registered individuals with greater regulatory clarity on the appropriate use of this sales charge. We anticipate that investors will benefit from this greater clarity in the form of improved product recommendations{33} that are more aligned with their investment needs and objectives.

Lower management fees and higher net returns on funds purchased with a front-end load

At present, the mutual fund series commonly known as "Series A" is the series that is typically distributed to retail investors and is sold under both the front-end load option and the DSC option. This industry-wide practice{34} means that all investors purchasing Series A of a fund, including front-end load investors, bear the costs associated with the payment of upfront commissions on DSC and low-load sales{35}. This form of cross-subsidization results in investors who purchased the Series A fund with a front-end load option paying management fees and trailing commissions that are higher than they would have been had they been segregated in a series of their own. The requirement for a separate DSC series will end this form of cross-subsidization and should result in lower management fees and correspondingly higher net returns for investors who choose the front-end load option. We analyzed the management expense ratios and investment returns for a limited number of funds that offer a separate DSC series for the same fund. We found that on average the MER for the DSC series was 20 basis points higher than the MER for the front-end load series. Assuming an initial investment of $10,000, in January 2010, in a fund that invests in Canadian large cap equity, the value of this investment in January 2020 would be $26,901 for the DSC series{36} and $27,556 for the front-end load series{37}, a difference of $655 or 2.4%.

3. Investment fund managers

Management fee revenue, which is generated from managing assets, is typically the biggest revenue source for investment fund managers. Our analysis of financial statements found that management fee revenue can account for 75% to 90% of a firm's revenue. Investment fund managers who have other business segments such as the administration and distribution of mutual funds are less reliant on revenue generated from asset management. As previously noted, an estimated $76 billion of mutual fund assets in Ontario was purchased with the DSC option. Assuming that the average net management fee is 1%{38}, investment fund managers would have generated $760 million in management fee revenue as a result of managing assets accumulated through the DSC option. We anticipate that the share of management fee revenue resulting from the management of DSC-related assets is likely to decrease because of the smaller investor base with smaller amounts of money to invest who can potentially purchase mutual funds with the DSC option. In spite of the potential reduction in management fee revenues, the Proposed Rule would allow investment fund managers to continue their practice of accumulating assets under management using the DSC option and thereby maintain the revenue stream arising from the management of these assets.

Investment fund managers finance the payment of the upfront commission paid to dealers and they incur financing costs that are included in the ongoing management fees charged to the fund. The introduction of a shorter redemption schedule and correspondingly lower upfront commission fees may lead to lower financing-related expenses.

F. Compliance costs, impacts on business models and investors

In this section we present a qualitative assessment of the costs of complying with the Proposed Rule for investment fund managers and dealers in addition to discussing the impacts on existing business models and investors. Similar to our approach for the benefits analysis, the baseline underpinning the analysis here is the current set of regulatory requirements pertaining to the distribution and sale of prospectus-qualified mutual funds in Ontario. As such, only regulatory compliance costs have been analyzed.

1) Investment fund managers

The table below lists each proposed restriction and identifies the anticipated compliance-related changes that may be required.

|

Proposed Restriction |

Areas of Anticipated Compliance Change |

|

|

|

||

|

• |

Maximum 3 year redemption schedule |

IT systems |

|

|

|

Policies and procedures |

|

|

||

|

• |

10% free redemption allowance annually and cumulatively |

IT systems |

|

|

|

Policies and procedures |

|

|

||

|

• |

Separate DSC series |

IT systems |

|

|

|

Policies and procedures |

|

|

|

Fund Facts, simplified prospectus and related disclosure documents |

IT systems, policies and procedures costs

Because the proposed restrictions are modifying existing industry practices, we anticipate that investment fund managers may have to change their IT systems and related policies and procedures to comply with the new restrictions. For this reason, we are of the view that implementation costs will be incremental to existing costs associated with industry practices that are now codified into regulation.

Implementation costs will vary by firm and will be influenced by the number of funds that can be sold using the DSC option that investment fund managers continue to offer; whether fund administration activities{39} are carried out in-house or externally, and, if externally, whether a single or multiple service providers are used to carry out these activities.

We anticipate ongoing costs will be similar to levels that investment fund managers currently incur in complying with current regulatory requirements.

Fund Facts, simplified prospectus and related disclosure costs

Investment fund managers who choose to continue offering the DSC option will have to produce new Fund Facts as a result of the requirement to offer a separate DSC series for each fund available with the DSC option. Updates to simplified prospectuses or the production of related disclosure documents{40} will also be required to comply with the rules pertaining to a shortened redemption schedule, and the cumulative 10% free redemption allowance. We anticipate the initial costs of producing a new Fund Facts and updating the simplified prospectus or producing related disclosure document to be incremental to existing compliance costs. Investment fund managers already have in place a framework for these undertakings, and we assume that the framework can be modified to address the requirements in the Proposed Rule.

We do not anticipate any direct ongoing costs associated with the Proposed Rule. Rather, ongoing costs for these disclosure documents will be triggered and dictated by other disclosure requirements pertaining to prospectus-qualified mutual funds, such as the requirement to update Fund Facts annually.

Business model impacts

The Proposed Rule transforms the DSC option into a modified low-load sales charge option while narrowing the investor base who can purchase funds with the DSC option. We anticipate the Proposed Rule may have an impact on the business model of investment fund managers who use the DSC option to generate asset growth and management fee revenue. The extent of the impact will vary and will heavily depend on a firm's revenue and cost structures, the short-- and long-term profitability of serving a subset of the investing population who occupy the lower end of the investible asset continuum, and how competing firms choose to respond to the Proposed Rule.

2) Dealers

Many of the dealer-related restrictions can be addressed within a firm's existing compliance approach to the NI 31-103 requirements{41} pertaining to conflicts of interest, know your product, know your client, and suitability. For this reason, we are of the view that firms may incur some minimal direct initial and ongoing costs with respect to the restrictions pertaining to age, account size, time horizon, and use of leverage.

The only new requirement pertains to the elimination of redemption fees in instances of demonstrable financial hardship; specifically, death, involuntary loss of full-time employment, permanent disability and critical illness. This requirement builds upon the existing requirement in NI 31-103 for a registrant to take reasonable steps to ensure that it has sufficient information about a client's financial circumstances and upon existing guidance about know your client obligations generally. We note that once all the Client Focused Reforms amendments take effect on December 31, 2021, registered individuals will be explicitly required to take reasonable steps to ensure that they have sufficient information about their clients' personal and financial circumstances when making a suitability determination. Firms will need to decide how best to establish that their clients are experiencing any of these financial hardship conditions and implement the necessary policies and procedures to comply with this new requirement. The initial and ongoing costs of this undertaking will largely be dictated by a firm's approach to compliance.

Firms will incur initial costs associated with providing initial training to their registered individuals on the requirements of the Proposed Rule. Ongoing training costs are anticipated to be significantly lower as we assume that training will only be provided to new employees or when material changes are made to the firm's approach to compliance.

Business model impacts

We anticipate the business models of dealer firms in the MFDA financial advisory channel may be impacted by the Proposed Rule. Specifically, business models that are focused on serving a narrow segment of investors with small amounts of money to invest, and the use of DSC-generated commission revenue by newly registered individuals to build a book of business at the start of their career may not be economically viable. If we assume that commission rates will be reduced to levels currently offered for low-load funds, registered individuals starting their business may then need larger book sizes to offset a reduction in revenue from sales commissions and a smaller potential client base. Registered individuals who are unable to generate a profitable book size in the early years of their business may need to exit the industry{42}.

3. Impacts on Investors

The subset of investors who will be impacted by the Proposed Rule are those whose investment account size is greater than $50,000 but less than $100,000, and who purchase mutual funds in the MFDA channel through a financial advisory firm. Currently, investors matching this profile have a high concentration of assets in funds purchased using the DSC option. If the Proposed Rule is adopted, these investors will have to purchase their mutual funds using a different sales charge option. We anticipate that investors will migrate to the front-end sales charge option because the front-end sales charge option is the second most common sales charge option used by this segment of investors. We note that while this segment of investors will have to switch to a different sales charge option, the upfront cost of buying a mutual fund with a front-end sales charge is typically waived{43}.

G. Risks and Uncertainties

The CSA jurisdictions other than Ontario have announced their intention to prohibit all forms of the DSC option and the upfront sales commissions associated with this purchase option. This decision would lead to the end of the DSC option and associated upfront dealer commission payments outside of Ontario. It is unclear how investment fund managers, dealers, and investors in Ontario may respond to these regulatory changes. Changing industry trends and market conditions, such as the shift to online advisers and ETFs, and the decision by several large investment fund managers to voluntarily discontinue the use of the DSC option, may also affect their responses to the Proposed Rule. The risk posed by these uncertainties is that our assessment of the impacts of the Proposed Rule may not reflect all the key costs and benefits that could arise.

This analysis only considers stakeholder responses to the proposed regulatory change in Ontario and is underpinned by assumptions based on current industry trends and market conditions.

{1} Source: https://www.ific.ca/wp-content/uploads/2019/12/News-Release-November-Monthly-Statistics-Mutual-Funds-and-ETFs-December-23-2019.pdf/23889/

{2} OSC estimate based on data from Investor Economics October 2019 Insight Report and IFIC data.

{3} Estimate is based on the assumption that the percentage of assets that were purchased with a DSC or low-load (LL) sales option in Ontario mirrors national figures. As at December 2018, 7.7% of mutual fund assets in Canada were purchased with a DSC sales option and another 3.2% was purchased with a LL sales option. Source: Investor Economics Insight Report March 2019. Unless otherwise noted, references to the DSC option hereinafter include the low-load sales option.

{4} There are several different purchase options for mutual funds and they fall into one of two categories -- load and no-load purchase options. The load purchase option comprises three different types of sales charges -- front-end sales charge, deferred sales charge and low-load sales charge. Under the front-end sales charge option an investor pays a sales commission at the time of purchase. Under the deferred sales charge and low-load sales charge options an investor pays a sales commission if the mutual fund is redeemed within a specified holding period. If the mutual fund is redeemed after the specified holding period the investor does not pay a sales commission. The no-load purchase option does not charge a sales commission either at the time of purchase or at the time of redemption. As at December 2018 the share of Canadian mutual fund assets by load option was 62.9% no-load, 26.2% front-end, 7.7% deferred sales charge and 3.2% low-load. While load funds account for 37% of mutual fund assets these types of funds account for 62% of all mutual funds. As at December 2018, there were 1,987 load funds and 1,205 no load funds. A more thorough discussion of mutual fund fees in Canada be found in the Canadian Securities Administrators' Discussion Paper 81-407 Mutual Fund Fees.

{5} These investment fund managers include IG Wealth Management, Dynamic Funds, Capital Group, and BMO Investments.

{6} We estimate that 50% of all households in Ontario have investments and that 75% of these households own mutual funds. OSC analysis of Ipsos Reid's Canadian Financial Monitor data and various investor surveys.

{7} Financial advisory firms are comprised of independent firms and firms that are affiliated with or owned by an investment fund manager or insurance company. Within the MFDA channel 39% of assets are held by financial advisory firms, 59% of assets are held by deposit-takers and credit unions, and 2% of assets are held by direct-to-consumer firms. We estimate that an additional $800 billion of mutual fund assets are held outside of the MFDA channel, i.e., in the private wealth management and discount and full service brokerages channels. These channels are dominated by firms owned by deposit-takers and insurance companies. Sales of mutual funds in these channels typically do not use the DSC option. OSC analysis of data from the 2017 MFDA Client Research Report, IFIC statistics, and various Investor Economics reports.

{8} Deposit-takers refer to banks and credit unions. Within the MFDA channel, 59% of assets are held by deposit-takers. OSC analysis of data from the 2017 MFDA Client Research Report and Investor Economics Insight Report March 2019, and discussions with the MFDA.

{9} Investor Economics Insight Report March 2019.

{10} The policy response to this investor protection issue will be published later in 2020 when the CSA publishes final rules related to the payment of trailing commissions to dealers who do not make a suitability determination.

{11} Investors whose investment time horizon is shorter than the DSC redemption schedule; investors who are 60 years old or older.

{12} https://www.ific.ca/wp-content/uploads/2019/01/IFIC-2018-Investment-Funds-Report.pdf/21611/

{13} Investment fund managers who are owned by deposit-takers or who have a direct-to-consumer business model typically do not distribute mutual funds with the DSC option. We have excluded these 13 firms from our analysis as they would not be materially impacted by the Proposed Rule. We note that the top 10 investment fund managers who have the largest amount of assets sold with the DSC option collectively manage 36.4% ($579 billion) of all mutual fund assets in Canada as at September 2019. Five of these investment fund managers are also amongst the top 10 largest investment fund managers in Canada, as measured by assets. OSC analysis based on regulatory data, IFIC industry statistics, Morningstar data, and data from various Investor Economics reports.

{14} Investor Economics 2012 Winter Retail Brokerage Report

{15} https://mfda.ca/members/membership-statistics/

{16} 2017 MFDA Client Research Report https://mfda.ca/wp-content/uploads/2017_MFDA_ClientResearchReport.pdf

{17} Ibid

{18} Our estimates of the proportion of investors who may be impacted by the Proposed Rule are based on current investing patterns of individuals who own mutual funds and the assumption that these patterns will continue if the Proposed Rule is adopted.

{19} OSC estimates using data from various investor surveys.

{20} Estimate is as at 2019 and is based on the OSC's analysis of various investors surveys. This estimate excludes investors who are age 60 and older because we have already accounted for this segment of investors in our age threshold analysis. Additionally, our estimate accounts for mutual fund ownership in all dealer channels and is not directly comparable to the figures in the 2017 MFDA Client Research Report. The MFDA research is confined to a subset of investors who have mutual fund holdings in the MFDA channel.

{21} OSC analysis of unpublished data from the 2017 MFDA Client Research. The average account size is at the household level and may over-report the average assets for single-person households.

{22} Estimate is as at 2019 and is based on the OSC's analysis of various investors surveys. This estimate excludes investors who are age 60 and older because we have already accounted for this segment of investors in our age threshold analysis. Additionally, our estimate accounts for mutual fund ownership in all dealer channels and is not directly comparable to the figures in the 2017 MFDA Client Research Report. The MFDA research is confined to a subset of investors who have mutual fund holdings in the MFDA channel.

{23} Unpublished analysis from the 2017 MFDA Client Research. The average account size is at the household level and may over-report the average assets for single-person households. As stated earlier in our analysis the DSC option is typically used by households where the account size is less than $100,000. For this reason we have excluded investors with account sizes greater than $100,000 from our analysis.

{24} Estimate is as at 2019 and is based on the OSC's analysis of various investors surveys. This estimate excludes investors who are age 60 and older because we have already accounted for this segment of investors in our age threshold analysis. Additionally, our estimate accounts for mutual fund ownership in all dealer channels and is not directly comparable to the figures in the 2017 MFDA Client Research Report. The MFDA research is confined to a subset of investors who have mutual fund holdings in the MFDA channel.

{25} 2017 MFDA Client Research Report.

{26} As advisors increase their book size they become less reliant on the DSC option to finance their operations and instead rely on other sources of revenue, including trailing commissions.

{27} Advocis submission in response to CSA Notice and Request For Comment -- Proposed Amendments to National Instrument 81-105 Mutual Fund Sales Practices and Related Consequential Amendments (December 13, 2018).

{28} CSA and OSC discussions with the MFDA about the data, analysis, and findings in its 2017 MFDA Client Research Report. CSA analysis of industry practices and trends -- refer to CSA Consultation Paper 81-408 Consultation on the Option of Discontinuing Embedded Commissions.

{29} The choice is to delay payment of sales charges at the point of redemption or to not pay sales charges at all if investors choose to hold their mutual funds to the end of the DSC redemption schedule.

{30} Our analysis assumes that investment fund managers will adopt fee redemption rates at levels that are typically charged by low-load funds.

{31} This is an existing industry practice that is being codified.

{32} Research undertaken by professor Douglas Cumming following the consultation on CSA Discussion Paper and Request for Comment 81-407 Mutual Fund Fees found that fee-based fund flows are much more sensitive to past performance when compared to DSC purchase options. Further, the research found that funds that have flows more sensitive to past performance tend to have better future performance. The full research report can be retrieved at https://www.osc.gov.on.ca/documents/en/Securities-Category5/rp_20151022_81-407_dissection-mutual-fund-fees.pdf

{33} Including a potential reduction in mis-selling.

{34} All but a handful of investment fund managers co-mingle the management fee revenue for funds sold with a DSC option and a front-end load option.

{35} Investment fund managers fund the costs of the DSC upfront sales commission from the management fee revenue they earn on their mutual fund assets.

{36} The realized annualized return is 10.40%.

{37} The realized annualized return is 10.66%.

{38} This reflects current industry rates.

{39} Activities carried out by registrars, transfer agents, and custodians.

{40} Our cost assessment assumes that investment fund managers will view the proposed requirements as material changes, which will then trigger corresponding changes to Fund Facts and the simplified prospectus or related disclosure documents such as an amendment to the simplified prospectus.

{41} NI 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations.

{42} Our analysis of publicly available financial information disclosure found that at least one dealer is shortening the time that newly registered individuals have to build a profitable book of business and are terminating registered individuals who are unable to achieve profitability early in their careers.

{43} 2017 MFDA Client Research Report.

ANNEX F

LOCAL MATTERS

ONTARIO RULE-MAKING AUTHORITY

AUTHORITY FOR THE PROPOSED RULE

The following provisions of the Securities Act (Ontario) (the Act) provide the Commission with authority to make the Proposed Rule:

Subparagraph 143(1)2(ii) of the Act authorizes the Commission to make rules prescribing requirements for registrants including requirements that are advisable for the prevention or regulation of conflicts of interest;

Paragraph 143(1)13 of the Act authorizes the Commission to make rules regulating trading or advising in securities to prevent trading or advising that is, among other things, unfairly detrimental to investors;

Paragraph 143(1)18of the Act authorizes the Commission to make rules designating activities, including the use of documents or advertising, in which registrants or issuers are permitted to engage or are prohibited from engaging in connection with distributions; and

Paragraph 143(1)31 of the Act authorizes the Commission to make rules regulating investment funds and the distribution and trading of the securities of investment funds, including

• making rules varying Part XV (Prospectuses -- Distribution) or Part XVIII (Continuous Disclosure) by prescribing additional disclosure requirements in respect of investment funds and requiring or permitting the use of particular forms or types of additional offering or other documents in connection with the funds;

• making rules respecting sales charges imposed by a distribution company or contractual plan service company under a contractual plan on purchasers of shares or units of an investment fund, and commissions or sales incentives to be paid to registrants in connection with the securities of an investment fund; and

• making rules prescribing procedures applicable to investment funds, registrants and any other person or company in respect of sales and redemptions of investment fund securities.