Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

NI 24-102 Clearing Agency Requirements, Forms and Companion Policy

NI 24-102 Clearing Agency Requirements, Forms and Companion Policy

NATIONAL INSTRUMENT 24-102

CLEARING AGENCY REQUIREMENTS

TABLE OF CONTENTS

|

PART 1 |

-- |

DEFINITIONS, INTERPRETATION AND APPLICATION |

|

|

||

|

PART 2 |

-- |

CLEARING AGENCY RECOGNITION OR EXEMPTION FROM RECOGNITION |

|

|

||

|

PART 3 |

-- |

PFMI PRINCIPLES APPLICABLE TO RECOGNIZED CLEARING AGENCIES |

|

|

||

|

PART 4 |

-- |

OTHER REQUIREMENTS OF RECOGNIZED CLEARING AGENCIES |

|

|

||

|

|

|

Division 1 -- Governance |

|

|

||

|

|

|

Division 2 -- Default management |

|

|

||

|

|

|

Division 3 -- Operational risk |

|

|

||

|

|

|

Division 4 -- Participation requirements |

|

|

||

|

PART 5 |

-- |

BOOKS AND RECORDS AND LEGAL ENTITY IDENTIFIER |

|

|

||

|

PART 6 |

-- |

EXEMPTIONS |

|

|

||

|

PART 7 |

-- |

EFFECTIVE DATE AND TRANSITION |

|

|

||

|

FORMS |

|

Form 24-102F1 -- Clearing Agency Submission to Jurisdiction and Appointment of Agent for Service of Process |

|

|

||

|

|

|

Form 24-102F2 -- Cessation of Operations Report for Clearing Agency |

NATIONAL INSTRUMENT 24-102 CLEARING AGENCY REQUIREMENTS

PART 1 DEFINITIONS, INTERPRETATION AND APPLICATION

Definitions

1.1 In this Instrument

"accounting principles" means accounting principles as defined in National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards;

"auditing standards" means auditing standards as defined in National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards;

"board of directors" means, in the case of a recognized clearing agency that does not have a board of directors, a group of individuals that acts for the clearing agency in a capacity similar to a board of directors;

"central counterparty" means a person or company that interposes itself between the counterparties to securities or derivatives transactions in one or more financial markets, acting functionally as the buyer to every seller and the seller to every buyer or the counterparty to every party;

"central securities depository" means a person or company that provides centralized facilities as a depository of securities, including securities accounts, central safekeeping services and asset services, which may include the administration of corporate actions and redemptions;

"exempt clearing agency" means a clearing agency that has been granted a decision of the securities regulatory authority pursuant to securities legislation exempting it from the requirement in such legislation to be recognized by the securities regulatory authority as a clearing agency;

"link" means, in relation to a clearing agency, contractual and operational arrangements that directly or indirectly through an intermediary connect the clearing agency and one or more other systems for the clearing, settlement or recording of securities or derivatives transactions;

"participant" means a person or company that has entered into an agreement with a clearing agency to access the services of the clearing agency and is bound by the clearing agency's rules and procedures;

"PFMI Disclosure Framework Document" means a disclosure document completed substantially in the form of Annex A: FMI disclosure template of the December 2012 report Principles for financial market infrastructures: Disclosure framework and Assessment methodology published by the Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions, as amended, supplemented or superseded from time to time, or a similar disclosure document required to be completed regularly and disclosed publicly by a clearing agency in accordance with the regulatory requirements of a foreign jurisdiction in which the clearing agency is located;

"PFMI Principle" means a principle, including applicable key considerations, in the April 2012 report Principles for financial market infrastructures published by the Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions, as amended from time to time;

"publicly accountable enterprise" means a publicly accountable enterprise as defined in Part 3 of National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards;

"securities settlement system" means a system that enables securities to be transferred and settled by book entry according to a set of predetermined multilateral rules.

Interpretation -- Affiliated Entity, Controlled Entity and Subsidiary Entity

1.2

(1) In this Instrument, a person or company is considered to be an affiliated entity of another person or company if one is a subsidiary entity of the other or if both are subsidiary entities of the same person or company, or if each of them is a controlled entity of the same person or company.

(2) In this Instrument, a person or company is considered to be controlled by a person or company if

(a) in the case of a person or company,

(i) voting securities of the first-mentioned person or company carrying more than fifty percent of the votes for the election of directors are held, otherwise than by way of security only, by or for the benefit of the other person or company, and

(ii) the votes carried by the securities are entitled, if exercised, to elect a majority of the directors of the first-mentioned person or company;

(b) in the case of a partnership that does not have directors, other than a limited partnership, the second-mentioned person or company holds more than fifty percent of the interests in the partnership; or

(c) in the case of a limited partnership, the general partner is the second-mentioned person or company.

(3) In this Instrument, a person or company is considered to be a subsidiary entity of another person or company if

(a) it is a controlled entity of

(i) that other,

(ii) that other and one or more persons or companies, each of which is a controlled entity of that other, or

(iii) two or more persons or companies, each of which is a controlled entity of that other; or

(b) it is a subsidiary entity of a person or company that is the other's subsidiary entity.

Interpretation -- Extended Meaning of Affiliated Entity

1.3 For the purposes of the PFMI Principles, a person or company is considered to be an affiliate of a participant, the person or company and the participant each being described in this section as a "party", where,

(a) a party holds, otherwise than by way of security only, voting securities of the other party carrying more than 20 percent of the votes for the election of directors, or

(b) in the event paragraph (a) is not applicable,

(i) a party holds, otherwise than by way of security only, an interest in the other party that allows it to direct the management or operations of the other party; or

(ii) financial information in respect of both parties is consolidated for financial reporting purposes.

Interpretation -- Clearing Agency

1.4 For the purposes of this Instrument, in Québec, a clearing agency includes a clearing house, a central securities depository and a settlement system within the meaning of the Québec Securities Act and a clearing house and a settlement system within the meaning of the Québec Derivatives Act.

Application

1.5

(1) Part 3 applies to a recognized clearing agency that operates as any of the following:

(a) a central counterparty;

(b) a central securities depository;

(c) a securities settlement system.

(2) Unless the context otherwise indicates, Part 4 applies to a recognized clearing agency whether or not it operates as a central counterparty, central securities depository or securities settlement system.

(3) In Québec, if there is a conflict or an inconsistency between section 2.2 and the provisions of the Québec Derivatives Act governing the self-certification process with respect to a clearing agency implementing a significant change or a fee change, the provisions of the Québec Derivatives Act prevail.

(4) The requirements of section 2.2 or 2.5 apply only to the extent that the subject matters of the section are not otherwise governed by the terms and conditions of a decision of the securities regulatory authority that recognizes a clearing agency or that exempts a clearing agency from a recognition requirement.

PART 2 CLEARING AGENCY RECOGNITION OR EXEMPTION FROM RECOGNITION

Application and initial filing of information

2.1

(1) An applicant for recognition as a clearing agency under securities legislation, or for exemption from the requirement to be recognized as a clearing agency under securities legislation, must include in its application all of the following:

(a) if applicable, the applicant's most recently completed PFMI Disclosure Framework Document;

(b) sufficient information to demonstrate that the applicant is in compliance with

(i) provincial and territorial securities legislation, or

(ii) the regulatory regime of a foreign jurisdiction in which the applicant's head office or principal place of business is located;

(c) any additional relevant information sufficient to demonstrate that it is in the public interest for the securities regulatory authority to recognize or exempt the applicant, as the case may be.

(2) In addition to the requirement set out in subsection (1), an applicant that has a head office or principal place of business located in a foreign jurisdiction must

(a) certify that it will assist the securities regulatory authority in accessing the applicant's books and records and in undertaking an onsite inspection and examination at the applicant's premises, and

(b) certify that it will provide the securities regulatory authority, if requested by such authority, with an opinion of legal counsel that the applicant has, as a matter of law, the power and authority to

(i) provide the securities regulatory authority with prompt access to its books and records, and

(ii) submit to onsite inspection and examination by the securities regulatory authority.

(3) In addition to the requirements set out in subsections (1) and (2), an applicant whose head office or principal place of business is located in a foreign jurisdiction must file a completed Form 24-102F1 Submission to Jurisdiction and Appointment of Agent for Service.

(4) An applicant must inform the securities regulatory authority in writing of any material change to the information provided in its application, or if any of the information becomes materially inaccurate for any reason, as soon as the change occurs or the applicant becomes aware of any inaccuracy.

Significant changes, fee changes and other changes in information

2.2

(1) In this section, for greater certainty, a "significant change" includes, in relation to a clearing agency,

(a) any change to the clearing agency's constating documents or by-laws;

(b) any change to the clearing agency's corporate governance or corporate structure, including any change of control of the clearing agency, whether direct or indirect;

(c) any material change to an agreement among the clearing agency and participants in connection with the clearing agency's operations and services, including those agreements to which the clearing agency is a party and those agreements among participants to which the clearing agency is not a party, but that are expressly referred to in the clearing agency's rules or procedures and are made available by participants to the clearing agency;

(d) any material change to the clearing agency's rules, operating procedures, user guides, manuals, or other documentation governing or establishing the rights, obligations and relationships among the clearing agency and participants in connection with the clearing agency's operations and services;

(e) any material change to the design, operation or functionality of any of the clearing agency's operations and services;

(f) the establishment or removal of a link or any material change to an existing link;

(g) commencing to engage in a new type of business activity or ceasing to engage in a business activity in which the clearing agency is then engaged;

(h) any other matter identified as a significant change in the recognition terms and conditions.

(2) Subject to subsection (4), a recognized clearing agency must not implement a significant change unless it has filed a written notice of the significant change with the securities regulatory authority at least 45 days before implementing the change.

(3) If a proposed significant change referred to in subsection (2) would affect the information set out in its PFMI Disclosure Framework Document filed with the securities regulatory authority, a recognized clearing agency must complete and file with the securities regulatory authority, concurrently with providing the written notice referred to in subsection (2), an appropriate amendment to its PFMI Disclosure Framework Document.

(4) If a recognized clearing agency proposes to modify a fee or introduce a new fee for any of its clearing, settlement or depository services, the clearing agency must notify in writing the securities regulatory authority of such fee change before implementing the fee change within a period stipulated by the terms and conditions of a decision of the securities regulatory authority that recognizes the clearing agency.

(5) An exempt clearing agency must notify in writing the securities regulatory authority of any material change to the information provided to the securities regulatory authority in its PFMI Disclosure Framework Document and related application materials, or if any of the information becomes materially inaccurate for any reason, as soon as the change occurs or the exempt clearing agency becomes aware of any inaccuracy.

Ceasing to carry on business

2.3

(1) A recognized clearing agency or exempt clearing agency that intends to cease carrying on business in the local jurisdiction as a clearing agency must file a report on Form 24-102F2 Cessation of Operations Report for Clearing Agency with the securities regulatory authority

(a) at least 180 days before ceasing to carry on business if a significant reason for ceasing to carry on business relates to the clearing agency's financial viability or any other matter that is preventing, or may potentially prevent, it from being able to provide its operations and services as a going concern, or

(b) at least 90 days before ceasing to carry on business for any other reason.

(2) A recognized clearing agency or exempt clearing agency that involuntarily ceases to carry on business in the local jurisdiction as a clearing agency must file a report on Form 24-102F2 Cessation of Operations Report for Clearing Agency with the securities regulatory authority as soon as practicable after it ceases to carry on that business.

Filing of initial audited financial statements

2.4

(1) An applicant must file audited financial statements for its most recently completed financial year with the securities regulatory authority as part of its application under section 2.1.

(2) The financial statements referred to in subsection (1) must

(a) be prepared in accordance with Canadian GAAP applicable to publicly accountable enterprises, IFRS or the generally accepted accounting principles of the foreign jurisdiction in which the person or company is incorporated, organized or located,

(b) identify in the notes to the financial statements the accounting principles used to prepare the financial statements,

(c) disclose the presentation currency, and

(d) be audited in accordance with Canadian GAAS, International Standards on Auditing or the generally accepted auditing standards of the foreign jurisdiction in which the person or company is incorporated, organized or located.

(3) The financial statements referred to in subsection (1) must be accompanied by an auditor's report that

(a) expresses an unmodified or unqualified opinion,

(b) identifies all financial periods presented for which the auditor's report applies,

(c) identifies the auditing standards used to conduct the audit,

(d) identifies the accounting principles used to prepare the financial statements,

(e) is prepared in accordance with the same auditing standards used to conduct the audit, and

(f) is prepared and signed by a person or company that is authorized to sign an auditor's report under the laws of a jurisdiction of Canada or a foreign jurisdiction, and that meets the professional standards of that jurisdiction.

Filing of annual audited and interim financial statements

2.5

(1) A recognized clearing agency or exempt clearing agency must file annual audited financial statements that comply with the requirements set out in subsections 2.4(2) and (3) with the securities regulatory authority no later than the 90th day after the end of the recognized clearing agency or exempt clearing agency's financial year.

(2) A recognized clearing agency or exempt clearing agency must file interim financial statements that comply with the requirements set out in paragraphs 2.4(2)(a) and (2)(b) with the securities regulatory authority no later than the 45th day after the end of each interim period.

PART 3 PFMI PRINCIPLES APPLICABLE TO RECOGNIZED CLEARING AGENCIES

PFMI Principles

3.1 A recognized clearing agency must establish, implement and maintain rules, procedures, policies or operations designed to ensure that it meets or exceeds PFMI Principles 1 to 3, 10, 13, 15 to 19, 20 other than key consideration 9, 21 to 23 and the following:

(a) if the clearing agency operates as a central counterparty, PFMI Principles 4 to 9, 12 and 14;

(b) if the clearing agency operates as a securities settlement system, PFMI Principles 4, 5, 7 to 9 and12; and

(c) if the clearing agency operates as a central securities depository, PFMI Principle 11.

PART 4 OTHER REQUIREMENTS OF RECOGNIZED CLEARING AGENCIES

Division 1 -- Governance:

Board of directors

4.1

(1) A recognized clearing agency must have a board of directors.

(2) The board of directors must include appropriate representation by individuals who are

(a) independent of the clearing agency, and

(b) not employees or executive officers of a participant or their immediate family members.

(3) For the purposes of paragraph (2)(a), an individual is independent of a clearing agency if he or she has no direct or indirect material relationship with the clearing agency.

(4) For the purposes of subsection (3), a "material relationship" is a relationship that could, in the view of the clearing agency's board of directors, be reasonably expected to interfere with the exercise of a member's independent judgment.

Documented procedures regarding risk spill-overs

4.2 The board of directors and management of a recognized clearing agency must have documented procedures to manage possible risk spill over where the clearing agency provides services with a different risk profile than its depository, clearing and settlement services.

Chief Risk Officer and Chief Compliance Officer

4.3

(1) A recognized clearing agency must designate a chief risk officer and a chief compliance officer, who must report directly to the board of directors or, if determined by the board of directors, to the chief executive officer of the clearing agency.

(2) The chief risk officer must

(a) have full responsibility and authority to maintain, implement and enforce the risk management framework established by the clearing agency,

(b) make recommendations to the clearing agency's board of directors regarding the clearing agency's risk management framework,

(c) monitor the effectiveness of the clearing agency's risk management framework, and

(d) report to the clearing agency's board of directors on a timely basis upon becoming aware of any significant deficiency with the risk management framework.

(3) The chief compliance officer must

(a) establish, implement, maintain and enforce written policies and procedures to identify and resolve conflicts of interest and ensure that the clearing agency complies with securities legislation,

(b) monitor compliance with the policies and procedures described in paragraph (a),

(c) report to the board of directors of the clearing agency as soon as practicable upon becoming aware of any circumstance indicating that the clearing agency, or any individual acting on its behalf, is not in compliance with securities legislation and one or more of the following apply:

(i) the non-compliance creates a risk of harm to a participant,

(ii) the non-compliance creates a risk of harm to the broader financial system,

(iii) the non-compliance is part of a pattern of non-compliance, or

(iv) the non-compliance may have an impact on the ability of the clearing agency to carry on business in compliance with securities legislation,

(d) prepare and certify an annual report assessing compliance by the clearing agency, and individuals acting on its behalf, with securities legislation and submit the report to the board of directors,

(e) report to the clearing agency's board of directors as soon as practicable upon becoming aware of a conflict of interest that creates a risk of harm to a participant or to the capital markets, and

(f) concurrently with submitting a report under paragraphs (c), (d) or (e), file a copy of such report with the securities regulatory authority.

Board or advisory committees

4.4

(1) The board of directors of a recognized clearing agency must, at a minimum, establish and maintain committees on risk management, finance and audit.

(2) If a committee is a board committee, it must be chaired by a sufficiently knowledgeable individual who is independent of the clearing agency.

(3) Subject to subsection (4), a committee must have an appropriate representation by individuals who are independent of the clearing agency.

(4) An audit or risk committee must have an appropriate representation by individuals who are

(a) independent of the clearing agency, and

(b) not employees or executive officers of a participant or their immediate family members.

Division 2 -- Default management:

Use of own capital

4.5 A recognized clearing agency that operates as a central counterparty must dedicate and use a reasonable portion of its own capital to cover losses resulting from one or more participant defaults.

Division 3 -- Operational risk:

Systems requirements

4.6 For each system operated by or on behalf of a recognized clearing agency that supports the clearing agency's clearing, settlement and depository functions, the clearing agency must

(a) develop and maintain

(i) an adequate system of internal controls over that system, and

(ii) adequate information technology general controls, including, without limitation, controls relating to information systems operations, information security, change management, problem management, network support and system software support,

(b) in accordance with prudent business practice, on a reasonably frequent basis and, in any event, at least annually

(i) make reasonable current and future capacity estimates, and

(ii) conduct capacity stress tests to determine the ability of that system to process transactions in an accurate, timely and efficient manner, and

(c) promptly notify the regulator or, in Québec, the securities regulatory authority of any material systems failure, malfunction, delay or security breach, and provide timely updates on the status of the failure, malfunction, delay or security breach, the resumption of service, and the results of the clearing agency's internal review of the failure, malfunction, delay or security breach.

Systems reviews

4.7

(1) A recognized clearing agency must annually engage a qualified party to conduct an independent systems review and vulnerability assessment and prepare a report in accordance with established audit standards and best industry practices to ensure that the clearing agency is in compliance with paragraph 4.6(a) and section 4.9.

(2) The clearing agency must provide the report resulting from the review conducted under subsection (1) to

(a) its board of directors, or audit committee, promptly upon the report's completion, and

(b) the regulator or, in Québec, the securities regulatory authority, by the earlier of the 30th day after providing the report to its board of directors or the audit committee or the 60th day after the calendar year end.

Clearing agency technology requirements and testing facilities

4.8

(1) A recognized clearing agency must make available to participants, in their final form, all technology requirements regarding interfacing with or accessing the clearing agency

(a) if operations have not begun, sufficiently in advance of operations to allow a reasonable period for testing and system modification by participants, and

(b) if operations have begun, sufficiently in advance of implementing a material change to technology requirements to allow a reasonable period for testing and system modification by participants.

(2) After complying with subsection (1), the clearing agency must make available testing facilities for interfacing with or accessing the clearing agency

(a) if operations have not begun, sufficiently in advance of operations to allow a reasonable period for testing and system modification by participants, and

(b) if operations have begun, sufficiently in advance of implementing a material change to technology requirements to allow a reasonable period for testing and system modification by participants.

(3) The clearing agency must not begin operations before

(a) it has complied with paragraphs (1)(a) and (2)(a), and

(b) the chief information officer of the clearing agency, or an individual performing a similar function, has certified in writing to the regulator or, in Québec, the securities regulatory authority, that all information technology systems used by the clearing agency have been tested according to prudent business practices and are operating as designed.

(4) The clearing agency must not implement a material change to the systems referred to in section 4.6 before

(a) it has complied with paragraphs (1)(b) and (2)(b), and

(b) the chief information officer of the clearing agency, or an individual performing a similar function, has certified in writing to the regulator or, in Québec, the securities regulatory authority, that the change has been tested according to prudent business practices and is operating as designed.

(5) Subsection (4) does not apply to the clearing agency if the change must be made immediately to address a failure, malfunction or material delay of its systems or equipment and if

(a) the clearing agency immediately notifies the regulator or, in Québec, the securities regulatory authority, of its intention to make the change, and

(b) the clearing agency discloses to its participants the changed technology requirements as soon as practicable.

Testing of business continuity plans

4.9 A recognized clearing agency must

(a) develop and maintain reasonable business continuity plans, including disaster recovery plans, and

(b) test its business continuity plans, including its disaster recovery plans, according to prudent business practices and on a reasonably frequent basis and, in any event, at least annually.

Outsourcing

4.10 If a recognized clearing agency outsources a critical service or system to a service provider, including to an affiliated entity of the clearing agency, the clearing agency must do all of the following:

(a) establish, implement, maintain and enforce written policies and procedures to conduct suitable due diligence for selecting service providers to which a critical service and system may be outsourced and for the evaluation and approval of those outsourcing arrangements;

(b) identify any conflicts of interest between the clearing agency and the service provider to which a critical service and system is outsourced, and establish, implement, maintain and enforce written policies and procedures to mitigate and manage those conflicts of interest;

(c) enter into a written contract with the service provider to which a critical service or system is outsourced that

(i) is appropriate for the materiality and nature of the outsourced activities,

(ii) includes service level provisions, and

(iii) provides for adequate termination procedures;

(d) maintain access to the books and records of the service provider relating to the outsourced activities;

(e) ensure that the securities regulatory authority has the same access to all data, information and systems maintained by the service provider on behalf of the clearing agency that it would have absent the outsourcing arrangements;

(f) ensure that all persons conducting audits or independent reviews of the clearing agency under this Instrument have appropriate access to all data, information and systems maintained by the service provider on behalf of the clearing agency that such persons would have absent the outsourcing arrangements;

(g) take appropriate measures to determine that the service provider to which a critical service or system is outsourced establishes, maintains and periodically tests an appropriate business continuity plan, including a disaster recovery plan;

(h) take appropriate measures to ensure that the service provider protects the clearing agency's proprietary information and participants' confidential information, including taking measures to protect information from loss, thefts, vulnerabilities, threats, unauthorized access, copying, use and modification, and discloses it only in circumstances where legislation or an order of a court or tribunal of competent jurisdiction requires the disclosure of such information;

(i) establish, implement, maintain and enforce written policies and procedures to monitor the ongoing performance of the service provider's contractual obligations under the outsourcing arrangements.

Division 4 -- Participation requirements:

Access requirements and due process

4.11

(1) A recognized clearing agency must not

(a) unreasonably prohibit, condition or limit access by a person or company to the services offered by the clearing agency,

(b) unreasonably discriminate among its participants or indirect participants,

(c) impose any burden on competition that is not reasonably necessary and appropriate,

(d) unreasonably require the use or purchase of another service for a person or company to utilize the clearing agency's services offered by it, and

(e) impose fees or other material costs on its participants that are unfairly or inequitably allocated among the participants.

(2) For any decision made by the clearing agency that terminates, suspends or restricts a participant's membership in the clearing agency or that declines entry to membership to an applicant that applies to become a participant, the clearing agency must ensure that

(a) the participant or applicant is given an opportunity to be heard or make representations, and

(b) it keeps records of, gives reasons for, and provides for reviews of its decisions, including, for each applicant, the reasons for granting access or for denying or limiting access to the applicant, as the case may be.

(3) Nothing in subsection (2) limits or prevents the clearing agency from taking timely action in accordance with its rules and procedures to manage the default of one or more participants or in connection with the clearing agency's recovery or orderly wind-down, whether or not such action adversely affects a participant.

PART 5 BOOKS AND RECORDS AND LEGAL ENTITY IDENTIFIER

Books and records

5.1

(1) A recognized clearing agency or exempt clearing agency must keep books, records and other documents as are necessary to account for the conduct of its clearing, settlement and depository activities, business transactions and financial affairs and must keep those other books, records and documents as may otherwise be required under securities legislation.

(2) The clearing agency must retain the books and records maintained under this section

(a) for a period of seven years from the date the record was made or received, whichever is later,

(b) in a safe location and a durable form, and

(c) in a manner that permits them to be provided promptly to the securities regulatory authority.

Legal Entity Identifier

5.2

(1) In this section,

"Global Legal Entity Identifier System" means the system for unique identification of parties to financial transactions developed by the LEI Regulatory Oversight Committee, and

"LEI Regulatory Oversight Committee" means the international working group established by the Finance Ministers and the Central Bank Governors of the Group of Twenty nations and the Financial Stability Board, under the Charter of the Regulatory Oversight Committee for the Global Legal Entity Identifier System dated November 5, 2012.

(2) For the purposes of any recordkeeping and reporting requirements required under securities legislation, a recognized clearing agency or exempt clearing agency must identify itself by means of a single legal entity identifier assigned to the clearing agency in accordance with the standards set by the Global Legal Entity Identifier System.

(3) If the Global Legal Entity Identifier System is unavailable to the clearing agency, all of the following apply:

(a) the clearing agency must obtain a substitute legal entity identifier that complies with the standards established by the LEI Regulatory Oversight Committee for pre-legal entity identifiers;

(b) the clearing agency must use the substitute legal entity identifier until a legal entity identifier is assigned to the clearing agency in accordance with the standards set by the Global Legal Entity Identifier System;

(c) after the holder of a substitute legal entity identifier is assigned a legal entity identifier in accordance with the standards set by the Global Legal Entity Identifier System, the clearing agency must ensure that it is identified only by the assigned identifier.

PART 6 EXEMPTIONS

Exemption

6.1

(1) The regulator or the securities regulatory authority may grant an exemption from the provisions of this Instrument, in whole or in part, subject to such conditions or restrictions as may be imposed in the exemption.

(2) Despite subsection (1), in Ontario, only the regulator may grant an exemption.

(3) Except in Ontario, an exemption referred to in subsection (1) is granted under the statute referred to in Appendix B of National Instrument 14-101 Definitions opposite the name of the local jurisdiction.

PART 7 EFFECTIVE DATE AND TRANSITION

Effective date and transition

7.1

(1) This Instrument comes into force on February 17, 2016.

(2) Despite section 3.1, until December 31, 2016, a recognized clearing agency is not required to implement rules, procedures, policies or operations designed to ensure that a recognized clearing agency meets or exceeds the following:

(a) PFMI Principle 14;

(b) key consideration 4 of PFMI Principle 3 and key consideration 3 of PFMI Principle 15 with respect to a clearing agency's recovery and orderly wind-down plans; and

(c) PFMI Principle 19.

(3) In Saskatchewan, despite subsection (1), if these regulations are filed with the Registrar of Regulations after February 17, 2016, these regulations come into force on the day on which they are filed with the Registrar of Regulations.

FORM 24-102F1 CLEARING AGENCY SUBMISSION TO JURISDICTION AND APPOINTMENT OF AGENT FOR SERVICE OF PROCESS

1. Name of clearing agency (the "Clearing Agency"):

______________________________

2. Jurisdiction of incorporation, or equivalent, of Clearing Agency:

______________________________

3. Address of principal place of business of Clearing Agency:

______________________________

4. Name of the agent for service of process (the "Agent") for the Clearing Agency:

______________________________

5. Address of the Agent in __________ [name of local jurisdiction]:

______________________________

6. The _______________ [name of securities regulatory authority] ("securities regulatory authority") issued an order recognizing the Clearing Agency as a clearing agency pursuant to securities legislation, or the securities regulatory authority issued an order exempting the Clearing Agency from the requirement to be recognized as a clearing agency pursuant to such legislation, on _______________.

7. The Clearing Agency designates and appoints the Agent as its agent upon whom may be served a notice, pleading, subpoena, summons or other process in any action, investigation or administrative, criminal, quasi-criminal, penal or other proceeding arising out of or relating to or concerning the activities of the Clearing Agency in __________ [province of local jurisdiction]. The Clearing Agency hereby irrevocably waives any right to challenge service upon its Agent as not binding upon the Clearing Agency.

8. The Clearing Agency agrees to unconditionally and irrevocably attorn to the non-exclusive jurisdiction of (i) the courts and administrative tribunals of __________ [name of local jurisdiction] and (ii) any proceeding in any province or territory arising out of, related to, concerning or in any other manner connected with the regulation and oversight of the activities of the Clearing Agency in __________ [name of local jurisdiction].

9. The Clearing Agency must file a new submission to jurisdiction and appointment of agent for service of process in this form at least 30 days before the Clearing Agency ceases to be recognized or exempted by the securities regulatory authority, to be in effect for six years from the date it ceases to be recognized or exempted unless otherwise amended in accordance with section 10.

10. Until six years after it has ceased to be a recognized or exempted by the securities regulatory authority, the Clearing Agency must file an amended submission to jurisdiction and appointment of agent for service of process at least 30 days before any change in the name or above address of the Agent.

11. The Clearing Agency agrees that this submission to jurisdiction and appointment of agent for service of process is to be governed by and construed in accordance with the laws of __________ [name of local jurisdiction].

|

Dated: ____________________ |

|

|

|

|

|

|

____________________ |

|

|

Signature of the Clearing Agency |

|

|

|

|

|

____________________ |

|

|

Print name and title of signing officer of the Clearing Agency |

AGENT CONSENT TO ACT AS AGENT FOR SERVICE

I, ____________________ [name of Agent in full; if a corporation, full corporate name] of ____________________ [business address], hereby accept the appointment as agent for service of process of ____________________ [insert name of Clearing Agency] and hereby consent to act as agent for service pursuant to the terms of the appointment executed by ____________________ [insert name of Clearing Agency] on _______________ [insert date].

|

Dated: ____________________ |

|

|

|

|

|

|

____________________ |

|

|

Signature of Agent |

|

|

|

|

|

____________________ |

|

|

Print name of person signing and, if Agent is not an individual, the title of the person |

FORM 24-102F2 CESSATION OF OPERATIONS REPORT FOR CLEARING AGENCY

1. Identification:

A. Full name of the recognized or exempted clearing agency:

B. Name(s) under which business is conducted, if different from item 1A:

2. Date clearing agency proposes to cease carrying on business as a clearing agency:

3. If cessation of business was involuntary, date clearing agency has ceased to carry on business as a clearing agency:

Exhibits

File all exhibits with the Cessation of Operations Report. For each exhibit, include the name of the clearing agency, the date of filing of the exhibit and the date as of which the information is accurate (if different from the date of the filing). If any exhibit required is inapplicable, a statement to that effect must be provided instead of the exhibit.

Exhibit A

The reasons for the clearing agency ceasing to carry on business as a clearing agency.

Exhibit B

A list of all participants in Canada during the last 30 days prior to ceasing business as a clearing agency.

Exhibit C

A description of the alternative arrangements available to participants in respect of the services offered by the clearing agency immediately before the cessation of business as a clearing agency.

Exhibit D

A description of all links the clearing agency had immediately before the cessation of business as a clearing agency with other clearing agencies or trade repositories.

CERTIFICATE OF CLEARING AGENCY

The undersigned certifies that the information given in this report is true and correct.

DATED at __________ this __________ day of _______________ 20_____

______________________________

(Name of clearing agency)

______________________________

(Name of director, officer or partner -- please type or print)

______________________________

(Signature of director, officer or partner)

______________________________

(Official capacity -- please type or print)

COMPANION POLICY 24-102CP TO NATIONAL INSTRUMENT 24-102 CLEARING AGENCY REQUIREMENTS

TABLE OF CONTENTS

|

PART 1 |

-- |

GENERAL COMMENTS |

|

|

|

|||

|

PART 2 |

-- |

CLEARING AGENCY RECOGNITION OR EXEMPTION FROM RECOGNITION |

|

|

|

|||

|

PART 3 |

-- |

PFMI PRINCIPLES APPLICABLE TO RECOGNIZED CLEARING AGENCIES |

|

|

|

|||

|

PART 4 |

-- |

OTHER REQUIREMENTS OF RECOGNIZED CLEARING AGENCIES |

|

|

|

|||

|

|

|

Division 1 -- Governance |

|

|

|

|||

|

|

|

Division 2 -- Default management |

|

|

|

|||

|

|

|

Division 3 -- Operational risk |

|

|

|

|||

|

|

|

Division 4 -- Participation requirements |

|

|

|

|||

|

PART 5 |

-- |

BOOKS AND RECORDS AND LEGAL ENTITY IDENTIFIER |

|

|

|

|||

|

PART 6 |

-- |

EXEMPTIONS |

|

|

|

|||

|

ANNEX I |

|

JOINT SUPPLEMENTARY GUIDANCE DEVELOPED BY THE BANK OF CANADA AND CANADIAN SECURITIES ADMINISTRATORS |

|

|

|

|||

|

|

|

PFMI Principle 2: Governance |

|

|

|

|||

|

|

|

|

Box 2.1: Joint Supplementary Guidance -- Financial Stability and Other Public Interest Considerations |

|

|

|||

|

|

|

|

Box 2.2: Joint Supplementary Guidance -- Vertically and Horizontally Integrated FMIs |

|

|

|||

|

|

|

PFMI Principle 5: Collateral |

|

|

|

|||

|

|

|

|

Box 5.1: Joint Supplementary Guidance -- Collateral |

|

|

|||

|

|

|

PFMI Principle 7: Liquidity risk |

|

|

|

|||

|

|

|

|

Box 7.1: Joint Supplementary Guidance -- Liquidity Risk |

|

|

|||

|

|

|

PFMI Principle 15: General business risk |

|

|

|

|||

|

|

|

|

Box 15.1: Joint Supplementary Guidance -- General Business Risk |

|

|

|||

|

|

|

PFMI Principle: Custody and investment risks |

|

|

|

|||

|

|

|

|

Box 16.1: Joint Supplementary Guidance -- Custody and Investment Risks |

|

|

|||

|

|

|

PFMI Principle: Disclosure of rules, key procedures, and market data |

|

|

|

|||

|

|

|

|

Box 23.1: Joint Supplementary Guidance -- Disclosure of Rules, Key Procedures and Market Data |

COMPANION POLICY 24-102CP TO NATIONAL INSTRUMENT 24-102 CLEARING AGENCY REQUIREMENTS

PART I GENERAL COMMENTS

Introduction

1.1

(1) This Companion Policy (CP) sets out how the Canadian Securities Administrators (the CSA or we) interpret or apply provisions of National Instrument 24-102 Clearing Agency Requirements (the Instrument) and related securities legislation.

(2) Except for this Part 1 of the CP, section 3.2 and 3.3 of Part 3 of this CP, and the text boxes in Annex I to this CP, the numbering of Parts, sections and subsections in this CP generally corresponds to the numbering in the Instrument. Any general guidance or introductory comments for a Part appears immediately after the Part's name. Specific guidance on a section or subsection in the Instrument follows any general guidance. If there is no guidance for a Part, section or subsection, the numbering in this CP will skip to the next provision that does have guidance.

(3) Unless otherwise stated, any reference in this CP to a Part, section, subsection, paragraph or defined term is a reference to the corresponding Part, section, subsection, paragraph or defined term of the Instrument. The CP also makes references to certain paragraphs in the April 2012 report Principles for financial market infrastructures (the PFMIs or PFMI Report, as the context requires) and the PFMI Principles set out therein. A reference to a PFMI Principle may include a reference to an applicable key consideration (see definition of "PFMI Principle" in section 1.1).

Background and overview

1.2

(1) Securities legislation in certain jurisdictions of Canada requires an entity seeking to carry on business as a clearing agency in the jurisdiction to be (i) recognized by the securities regulatory authority in that jurisdiction, or (ii) exempted from the recognition requirement.{1} Accordingly, Part 2 sets out certain requirements in connection with the application process for recognition as a clearing agency or exemption from the recognition requirement. Guidance on the CSA's regulatory approach to such an application is set out in this CP.

(2) Parts 3 and 4 set out on-going requirements applicable to a recognized clearing agency. Part 3 adopts the PFMI Principles generally but does restrict their application only to a clearing agency that operates as a central counterparty (CCP), securities settlement system (SSS) or central securities depository (CSD), as relevant. Part 4 applies to a clearing agency whether or not it operates as a CCP, SSS or CSD. The PFMI Principles were developed jointly by the Committee on Payments and Market Infrastructures (CPMI){2} and the International Organization of Securities Commissions (IOSCO).{3} The PFMI Principles harmonize and strengthen previous international standards for financial market infrastructures (FMIs).{4}

(3) Annex I to this CP includes supplementary guidance in text boxes that applies to recognized domestic clearing agencies that are also overseen by the Bank of Canada (BOC). The supplementary guidance (Joint Supplementary Guidance) was prepared jointly by the CSA and BOC to provide additional clarity on certain aspects of the PFMI Principles within the Canadian context.

Definitions, interpretation and application

1.3

(1) Unless defined in the Instrument or this CP, defined terms used in the Instrument and this CP have the meaning given to them in the securities legislation of each jurisdiction or in National Instrument 14-101 Definitions.

(2) The terms "clearing agency" and "recognized clearing agency" are generally defined in securities legislation. For the purposes of the Instrument, a clearing agency includes, in Quebec, a clearing house, central securities depository and settlement system within the meaning of the Québec Securities Act and a clearing house and settlement system within the meaning of the Québec Derivatives Act. See section 1.4. The CSA notes that, while Part 3 applies only to a recognized clearing agency that operates as a CCP, CSD or SSS, the term "clearing agency" may incorporate certain other centralized post-trade functions that are not necessarily limited to those of a CCP, CSD or SSS, e.g., an entity that provides centralized facilities for comparing data respecting the terms of settlement of a trade or transaction may be considered a clearing agency, but would not be considered a CCP, CSD or SSS. Except in Québec, such an entity would be required to apply either for recognition as a clearing agency or an exemption from the requirement to be recognized.{5} The CSA considers that a recognized clearing agency, which is not a CCP, CSD or SSS, should not be subject to the application of Part 3. Such a clearing agency is, however, subject to provisions in Part 2 and all of Parts 4 and 5.

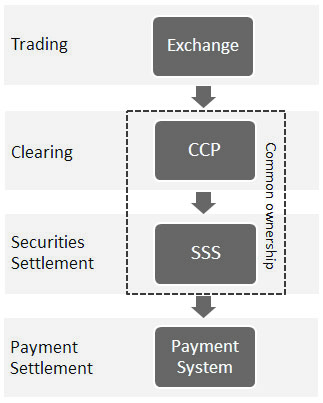

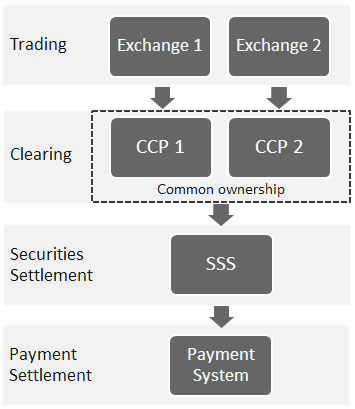

(3) A clearing agency may serve either or both the securities and derivatives markets. A clearing agency serving the securities markets can be a CCP, CSD or SSS. A clearing agency serving the derivatives markets is typically only a CCP.

(4) In this CP, FMI means a financial market infrastructure, which the PFMI Report describes as follows: payment systems, CSDs, SSSs, CCPs and trade repositories.

PART 2 CLEARING AGENCY RECOGNITION OR EXEMPTION FROM RECOGNITION

Recognition and exemption

2.0

(1) An entity seeking to carry on business as a clearing agency in certain jurisdictions in Canada is required under the securities legislation of such jurisdictions to apply for recognition or an exemption from the recognition requirement. For greater clarity, a foreign-based clearing agency that provides, or will provide, its services or facilities to a person or company resident in a jurisdiction would be considered to be carrying on business in that jurisdiction.

-- Recognition of a clearing agency

(2) The CSA takes the view that a clearing agency that is systemically important to a jurisdiction's capital markets, or that is not subject to comparable regulation by another regulatory body, will generally be recognized by a securities regulatory authority.{6} A securities regulatory authority may consider the systemic importance of a clearing agency to its capital markets based on the following list of guiding factors: value and volume of transactions processed, cleared and settled by the clearing agency;{7} risk exposures (particularly credit and liquidity) of the clearing agency to its participants; complexity of the clearing agency;{8} and centrality of the clearing agency with respect to its role in the market, including its substitutability, relationships, interdependencies and interactions.{9} The list of guiding factors is non-exhaustive, and no single factor described above will be determinative in an assessment of systemic importance. A securities regulatory authority retains the ability to consider additional quantitative and qualitative factors as may be relevant and appropriate.{10}

(3) Because of the approach described in subsection 2.0(2) of this CP, a securities regulatory authority may require a foreign-based clearing agency to be recognized if the clearing agency's proposed business activities in the local jurisdiction are systemically important to the jurisdiction's capital markets, even if it is already subject to comparable regulation in its home jurisdiction. In such circumstances, the recognition decision would focus on key areas that pose material risks to the jurisdiction's market and rely, where appropriate, on the current regulatory requirements and processes to which the entity is already subject in its home jurisdiction. Terms and conditions of a recognition decision that require a foreign clearing agency to report information to a Canadian securities regulatory authority may vary among foreign clearing agencies. Among other factors, they will depend on whether Canadian securities regulatory authorities have entered into an agreement or memorandum of understanding with the home regulator for sharing information and cooperation.

-- Exemption from recognition

(4) Depending on the circumstances, a clearing agency may be granted an exemption from recognition pursuant to securities legislation and subject to appropriate terms and conditions, where it is not considered systemically important or where it does not otherwise pose significant risk to the capital markets. For example, such an approach may be considered for an entity that provides limited services or facilities, thereby not warranting full regulation, such as a clearing agency that does not perform the functions of a CCP, CSD or SSS. However, in such cases, terms and conditions may be imposed. In addition, a foreign-based clearing agency that is already subject to a comparable regulatory regime in its home jurisdiction may be granted an exemption from the recognition requirement as full regulation may be duplicative and inefficient when imposed in addition to the regulation of the home jurisdiction. The exemption may be subject to certain terms and conditions, including reporting requirements and prior notification of certain material changes to information provided to the securities regulatory authority.

Application and initial filing of information

2.1 The application process for both recognition and exemption from recognition as a clearing agency is similar. The entity that applies will typically be the entity that operates the facility or performs the functions of a clearing agency. The application for recognition or exemption will require completion of appropriate documentation. This will include the items listed in subsection 2.1(1). Together, the application materials should present a detailed description of the history, regulatory structure, and business operations of the clearing agency. A clearing agency that operates as a CCP, CSD or SSS will need to describe how it meets or will meet the requirements of Parts 3 and 4. An applicant based in a foreign jurisdiction should also provide a detailed description of the regulatory regime of its home jurisdiction and the requirements imposed on the clearing agency, including how such requirements are similar to the requirements in Parts 3 and 4.

Where specific information items of the PFMI Disclosure Framework Document are not relevant to an applicant because of the nature or scope of its clearing agency activities, its structure, the products it clears or settles, or its regulatory environment, the application should explain in reasonable detail why the information items are not relevant.

The application filed by an applicant will generally be published for public comment for a 30-day period. Other materials filed with the application, which the applicant wishes to maintain confidential, will generally be kept confidential in accordance with securities and privacy legislation. However, the clearing agency will be required to publicly disclose its PFMI Disclosure Framework Document. See PFMI Principle 23, key consideration 5.

Significant changes, fee changes, and other changes in information

2.2 Section 2.2 is subject to the application provisions of subsections 1.5(3) and (4). For example, where the terms and conditions of a recognition decision made by a securities regulatory authority require a recognized clearing agency to obtain the approval of the authority before implementing a new fee for a service, the process to seek such approval set forth in the terms and conditions will apply instead of the prior notification requirement in subsection 2.2(4).

(2) The written notice should provide a reasonably detailed description of the significant change (as defined in subsection 2.2(1)) and the expected date of the implementation of the change. It should enclose or attach updated relevant documentation, including clean and blacklined versions of the documentation that show how the significant change will be implemented. If the notice is being filed by a foreign-based clearing agency, the notice should also describe the approval process or other involvement by the primary or home-jurisdiction regulator for implementing the significant change. The clearing agency is required to file concurrently with the notice any changes required to be made to the clearing agency's PFMI Disclosure Framework Document as a result of implementing the significant change, in accordance with subsection 2.2(3).

Ceasing to carry on business

2.3 A recognized or exempt clearing agency that ceases to carry on business in a local jurisdiction as a clearing agency, either voluntarily or involuntarily, must file a completed Form 24-102F2 Cessation of Operations Report for Clearing Agency within the appropriate timelines. In certain jurisdictions, the clearing agency intending to cease carrying on business must also make an application to voluntarily surrender its recognition to the securities regulatory authority pursuant to securities legislation. The securities regulatory authority may accept the voluntary surrender subject to terms and conditions.{11}

PART 3 PFMI PRINCIPLES APPLICABLE TO RECOGNIZED CLEARING AGENCIES

Introduction

3.0

(1) Section 3.1 adopts the PFMI Principles generally but excludes the application of specific PFMI Principles for certain types of clearing agencies. We have adopted only those PFMI Principles that are relevant to clearing agencies operating as a CCP, CSD or SSS.{12}

(2) Part 3, together with the PFMI Principles, is intended to be consistent with a flexible and principles-based approach to regulation. In this regard, Part 3 anticipates that a clearing agency's rules, procedures, policies and operations will need to evolve over time so that it can adequately respond to changes in technology, legal requirements, the needs of its participants and their customers, trading volumes, trading practices, linkages between financial markets, and the financial instruments traded in the markets that a clearing agency serves.

PFMI Principles

3.1 The definition of PFMI Principles in the Instrument includes the applicable key considerations for each principle. Annex E to the PFMI Report provides additional guidance on how each key consideration will apply to the specified types of clearing agencies. In interpreting and implementing the PFMI Principles, regard is to be given to the explanatory notes in the PFMI Report, as appropriate, unless otherwise indicated in section 3.1 or this Part 3 of the CP.{13} As discussed in subsection 1.2(3) of this CP, the CSA and BOC have together developed Joint Supplementary Guidance to provide additional clarity on certain aspects of some PFMI Principles within the Canadian context. The Joint Supplementary Guidance is directed at recognized domestic clearing agencies that are also overseen by the BOC. The Joint Supplementary Guidance is included in separate text boxes in Annex I to this CP under the relevant headings of the PFMI Principles. Except as otherwise indicated in this Part 3 of the CP, other recognized domestic clearing agencies should assess the applicability of the Joint Supplementary Guidance to their respective entity as well.

PFMI Principle 5: Collateral

3.2 Notwithstanding section 3.1 of the CP and the Joint Supplementary Guidance relating to PFMI Principle 5: Collateral (see Box 5.1 in Annex I to this CP), we are of the view that letters of credit may be permitted as collateral by a recognized domestic clearing agency operating as a CCP serving derivatives markets that is not also overseen by the BOC, provided that the collateral and the clearing agency's collateral policies and procedures otherwise meet the requirements of PFMI Principle 5: Collateral. However, the recognized clearing agency must first obtain regulatory approval of its rules and procedures that govern the use of letters of credit as collateral before accepting letters of credit.

PFMI Principle 14: Segregation and portability for CCPs serving cash markets

3.3 PFMI Principle 14: Segregation and portability requires, pursuant to section 3.1, that a CCP have rules and procedures that enable the segregation and portability{14} of positions and related collateral of a CCP participant's customers, particularly to protect the customers from the default or insolvency of the participant. The explanatory notes in the PFMI Report offer an "alternate approach" to meeting PFMI Principle 14. The report notes that, in certain jurisdictions, cash market CCPs operate in legal regimes that facilitate segregation and portability to achieve the protection of customer assets by alternate means that offer the same degree of protection as the approach in PFMI Principle 14.{15} The features of the alternate approach are described in the PFMI Report.{16}

-- Customers of IIROC dealer members:

Currently, most participants of domestic cash market CCPs that clear for customers are investment dealers.{17} They are required to be members of the Investment Industry Regulatory Organization of Canada (IIROC){18} and to contribute to the Canadian Investor Protection Fund (CIPF).{19} The CSA is of the view that the customer asset protection regime applicable to investment dealers (IIROC-CIPF regime) is an appropriate alternative framework for customers of investment dealers that are direct participants of a cash-market CCP. The IIROC-CIPF regime meets the criteria for the alternate approach for CCPs serving certain domestic cash markets because:

• IIROC's requirements governing, among other things, an investment dealer's books and records, capital adequacy, internal controls, client account margining, and segregation of client securities and cash help ensure that customer positions and collateral can be identified timely,

• customers of an investment dealer are protected by CIPF, and

• through a combination of IIROC's member rules and oversight powers, CIPF's role in the administration of the bankruptcy of a dealer, and the overarching policy objectives of Part XII of the federal Bankruptcy and Insolvency Act (BIA) (discussed below), customer accounts can be moved from a failing dealer to another dealer in a timely manner and customers' assets can be restored.

Part XII of the BIA sets out a special bankruptcy regime for administering the insolvency of a securities firm. The regime generally provides for all cash and securities of a bankrupt securities firm, whether held for its own account and for its customers, to vest in the appointed trustee in bankruptcy. The trustee, in turn, is directed to pool such assets into a "customer pool fund" for the benefit of the customers, which are entitled to a pro rata share of the customer pool fund according to their respective "net equity" claims as a priority claim before the general creditors are paid. To the extent there is a shortfall in customer recovery from the customer pool fund and any remaining assets in the insolvent estate, the assets are allocated among the customers on a pro rata basis. CIPF, which works in conjunction with IIROC and the bankruptcy trustee,{20} provides protection to eligible customers for losses up to $1 million per account.{21}

-- Customers of other types of participants:

A recognized clearing agency operating as a cash market CCP for participants that are not IIROC investment dealers will need to have segregation and portability arrangements at the CCP level that meet PFMI Principle 14. Where the clearing agency is proposing to rely on an alternate approach for the purposes of protecting the customers of such participants, the clearing agency will need to demonstrate how the applicable legal or regulatory framework in which it operates achieves the same degree of protection and efficiency for such customers that would otherwise be achieved by segregation and portability arrangements at the CCP level described in PFMI Principle 14. See the PFMI Report, at paragraph 3.14.6.

PART 4 OTHER REQUIREMENTS OF RECOGNIZED CLEARING AGENCIES

Introduction

4.0 As discussed in section 1.2(2) of this CP, the provisions of Part 4 are in addition to the requirements of Part 3, and apply to a clearing agency whether or not it operates as a CCP, SSS or CSD.

Division 1 -- Governance:

Board of directors

4.1

(4) Consistent with the explanatory notes in the PFMI Report (see paragraph 3.2.10), we are of the view that the following individuals have a relationship with a clearing agency that would reasonably be expected to interfere with the exercise of the individual's independent judgment:

(a) an individual who is, or has been within the last year, an employee or executive officer of the clearing agency or any of its affiliated entities;

(b) an individual whose immediate family member is, or has been within the last year, an executive officer of the clearing agency or any of its affiliated entities;

(c) an individual who beneficially owns, directly or indirectly, voting securities carrying more than ten per cent of the voting rights attached to all voting securities of the clearing agency or any of its affiliated entities for the time being outstanding;

(d) an individual whose immediate family member beneficially owns, directly or indirectly, voting securities carrying more than ten per cent of the voting rights attached to all voting securities of the clearing agency or any of its affiliated entities for the time being outstanding;

(e) an individual who is, or has been within the last year, an executive officer of a person or company that beneficially owns, directly or indirectly, voting securities carrying more than ten per cent of the voting rights attached to all voting securities of the clearing agency or any of its affiliated entities for the time being outstanding; and

(f) an individual who accepts or who received within the last year, directly or indirectly, any audit, consulting, advisory or other compensatory fee from the clearing agency or any of its affiliated entities, other than as remuneration for acting in his or her capacity as a member of the board of directors or any board committee, or as a part-time chair or vice-chair of the board or any board committee.

For the purposes of paragraph (f) above, compensatory fees would not normally include the receipt of fixed amounts of compensation under a retirement plan (including deferred compensation) for prior service with the clearing agency if the compensation is not contingent in any way on continued service. Also, the indirect acceptance by an individual of any audit, consulting, advisory or other compensatory fee includes acceptance of a fee by (a) an individual's immediate family member; or (b) an entity in which such individual is a partner, a member, an officer such as a managing director occupying a comparable position or an executive officer, or occupies a similar position (except limited partners, non-managing members and those occupying similar positions who, in each case, have no active role in providing services to the entity) and which provides accounting, consulting, legal, investment banking or financial advisory services to the clearing agency or any of its affiliated entities.

In addition, an individual appointed to the board of directors or board committee of the clearing agency or any of its affiliated entities or of a person or company referred to in paragraph (e) above would not be considered to have a material relationship with the clearing agency solely because the individual acts, or has previously acted, as a chair or vice-chair of the board of directors or a board committee.

Documented procedures regarding risk spill-overs

4.2 For guidance on this provision, see the Joint Supplementary Guidance in Box 2.2 in Annex I of this CP.

Chief Risk Officer (CRO) and Chief Compliance Officer (CCO)

4.3 Section 4.3 is consistent with PFMI Principle 2, key consideration 5, which requires a clearing agency to have an experienced management with a mix of skills and the integrity necessary to discharge its operations and risk management responsibilities.

(3) The reference to "harm to the broader financial system" in subparagraph 4.3(3)(c)(ii) may be in relation to the domestic or international financial system. The CSA is of the view that the role of a CCO may, in certain circumstances, be performed by the Chief Legal Officer or General Counsel of the clearing agency, where the individual has sufficient time to properly carry out his or her duties and, provided that there are appropriate safeguards in place to avoid conflicts of interest.

Board or advisory committees

4.4 Section 4.4 is intended to reinforce the clearing agency's obligations to meet the PFMI Principles, particularly PFMI Principles 2 and 3. The CSA is of the view that the mandates of the committees should, at a minimum, include the following:

(a) providing advice and recommendations to the board of directors to assist it in fulfilling its risk management responsibilities, including reviewing and assessing the clearing agency's risk management policies and procedures, the adequacy of the implementation of appropriate procedures to mitigate and manage such risks, and the clearing agency's participation standards and collateral requirements;

(b) ensuring adequate processes and controls are in place over the models used to quantify, aggregate, and manage the clearing agency's risks;

(c) monitoring the financial performance of the clearing agency and providing financial management oversight and direction to the business and affairs of the clearing agency;

(d) implementing policies and processes to identify, address, and manage potential conflicts of interest of board members; and

(e) regularly reviewing the board of directors' and senior management's performance and the performance of each individual member.

Section 4.4 is a minimum requirement. Consistent with the explanatory notes in the PFMI Principles (see paragraph 3.2.9), a recognized clearing agency should also consider forming other types of board committees, such as a compensation committee. All committees should have clearly assigned responsibilities and procedures. The clearing agency's internal audit function should have sufficient resources and independence from management to provide, among other activities, a rigorous and independent assessment of the effectiveness of its risk-management and control processes. See section 4.1 for the concept of independence. A board will typically establish an audit committee to oversee the internal audit function. In addition to reporting to senior management, the audit function should have regular access to the board through an additional reporting line.

Division 2 -- Default management:

Use of own capital

4.5 The CSA is of the view that a CCP's own capital contribution should be used in the default waterfall, immediately after a defaulting participant's contributions to margin and default fund resources have been exhausted, and prior to non-defaulting participants' contributions. Such equity should be significant enough to attract senior management's attention, and separately retained and not form part of the CCP's resources for other purposes, such as to cover general business risk.

Division 3 -- Operational risk:

4.6 to 4.10 Sections 4.6 to 4.10 complement PFMI Principle 17, which requires a clearing agency to identify the plausible sources of operational risk, both internal and external, and mitigate their impact through the use of appropriate systems, policies, procedures, and controls. PFMI Principle 17 further requires that systems should be designed to ensure a high degree of security and operational reliability and should have adequate, scalable capacity, and business continuity management should aim for timely recovery of operations and fulfilment of the FMI's obligations, including in the event of a wide-scale or major disruption.

Systems requirements

4.6

(a) The intent of these provisions is to ensure that controls are implemented to support information technology planning, acquisition, development and maintenance, computer operations, information systems support, and security. Recognized guides as to what constitutes adequate information technology controls include 'Information Technology Control Guidelines' from the Canadian Institute of Chartered Accountants (CICA) and 'COBIT' from the IT Governance Institute.

(b) Capacity management requires that the clearing agency monitor, review, and test (including stress test) the actual capacity and performance of the system on an ongoing basis. Accordingly, under subsection 4.6(b), the clearing agency is required to meet certain standards for its estimates and for testing. These standards are consistent with prudent business practice. The activities and tests required in this subsection are to be carried out at least once a year. In practice, continuing changes in technology, risk management requirements and competitive pressures will often result in these activities being carried out or tested more frequently.

(c) A failure, malfunction or delay or other incident is considered to be "material" if the clearing agency would, in the normal course of operations, escalate the matter to or inform its senior management ultimately accountable for technology. It is also expected that, as part of this notification, the clearing agency will provide updates on the status of the failure and the resumption of service. Further, the clearing agency should have comprehensive and well-documented procedures in place to record, report, analyze, and resolve all operational incidents. In this regard, the clearing agency should undertake a "post-incident" review to identify the causes and any required improvement to the normal operations or business continuity arrangements. Such reviews should, where relevant, include the clearing agency's participants. The results of such internal reviews are required to be communicated to the securities regulatory authority as soon as practicable. Subsection 4.6(c) also refers to a material security breach. A material security breach or systems intrusion is considered to be any unauthorized entry into any of the systems that support the functions of the clearing agency or any system that shares resources with one or more of these systems. Virtually any security breach would be considered material and thus reportable to the securities regulatory authority. The onus would be on the clearing agency to document the reasons for any security breach it did not consider material.

Systems reviews

4.7

(1) A qualified party is a person or company or a group of persons or companies with relevant experience in both information technology and in the evaluation of related internal systems or controls in a complex information technology environment. Qualified persons may include external auditors or third party information system consultants, as well as employees of the clearing agency or an affiliated entity of the clearing agency, but may not be persons responsible for the development or operation of the systems or capabilities being tested. Before engaging a qualified party, a clearing agency should discuss its choice with the regulator or, in Québec, the securities regulatory authority.

Clearing agency technology requirements and testing facilities

4.8

(1) The technology requirements required to be disclosed under subsection 4.8(1) do not include detailed proprietary information.

(5) We expect the amended technology requirements to be disclosed as soon as practicable, either while the changes are being made or immediately after.

Testing of business continuity plans

4.9 Business continuity management is a key component of a clearing agency's operational risk-management framework. A recognized clearing agency's business continuity plan and its associated arrangements should be subject to frequent review and testing. At a minimum, under section 4.9, such tests must be conducted annually. Tests should address various scenarios that simulate wide-scale disasters and inter-site switchovers. The clearing agency's employees should be thoroughly trained to execute the business continuity plan and participants, critical service providers, and linked clearing agencies should be regularly involved in the testing and be provided with a general summary of the testing results. The CSA expects that the clearing agency will also facilitate and participate in industry-wide testing of the business continuity plan (domestically-based recognized clearing agencies are required to participate in all industry-wide business continuity tests, as determined by a regulation services provider, regulator, or in Québec, the securities regulatory authority, pursuant to National Instrument 21-101 Marketplace Operation). The clearing agency should make appropriate adjustments to its business continuity plan and associated arrangements based on the results of the testing exercises.

Outsourcing