Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

CSA Consultation Paper 25-402 – Consultation on the Self-Regulatory Organization Framework

CSA Consultation Paper 25-402 – Consultation on the Self-Regulatory Organization Framework

June 25, 2020

1. Introduction

On December 12, 2019, the Canadian Securities Administrators (CSA) issued a news release (News Release){1} announcing that it would undertake a review of the regulatory framework for the Investment Industry Regulatory Organization of Canada (IIROC) and the Mutual Fund Dealers Association of Canada (MFDA).

The idea to review the regulatory framework for self-regulatory organizations (SROs) in Canada is not new, and the merits and timing of such a review have been considered many times by the CSA, as well as recently in public forums. The current SRO regulatory framework has been in place for almost twenty years, and in that time, the delivery of financial services and products has continued to evolve. In response to the evolution of the industry and submissions formulated by a group of industry participants, the CSA believes that it is appropriate to revisit the current structure of the SRO regulatory framework and to seek comments from all stakeholders at this time.

While the CSA conducts this review, it is not intended to have a disruptive impact on the SROs' ability to perform their regulatory operations, or on the activity of their dealer members to service the investing public.

Since the issuance of the News Release, the CSA staff met with a wide variety of stakeholder groups to informally discuss the benefits, challenges and issues of the current SRO regulatory framework. The CSA is publishing this consultation paper (Consultation Paper) for a 120-day comment period to seek input from all industry representatives and stakeholders, investor advocates, and the public. The CSA is asking for general feedback on how innovation and the evolution of the financial services industry has impacted the current regulatory framework, as well as specific comments on the issues and targeted outcomes set out in the Consultation Paper.

The comment period will end on October 23, 2020.

2. Self-Regulatory Organization Regulatory Framework in Canada and Internationally

An SRO is an entity created for the purpose of regulating the operations and the standards of practice and business conduct of its members and their representatives with a view to promote investor protection and the public interest. In Canada, provincial and territorial securities regulators (Securities Regulators), operating together as the CSA, have a long history of utilizing SROs as part of their regulatory framework. The securities industry SROs operate under the authority and supervision of the CSA.

The current SRO regulatory framework in Canada requires investment dealers to be members of IIROC and mutual fund dealers to be members of the MFDA, except in Québec where mutual fund dealers are directly regulated by the Autorité des marchés financiers (AMF).{2}

While each SRO performs the primary oversight of investment (IIROC) and mutual fund (MFDA) dealers, as applicable, both IIROC and MFDA members remain subject to regulation by the CSA and must comply with national rules, such as National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103), as well as applicable provincial and territorial securities legislation. To avoid duplication of regulation, IIROC and MFDA dealers are exempt from compliance with certain sections of NI 31-103 in cases where the dealers comply with the corresponding requirements under IIROC or MFDA rules.

The Regulatory Landscape

i) The Investment Industry Regulation Organization of Canada

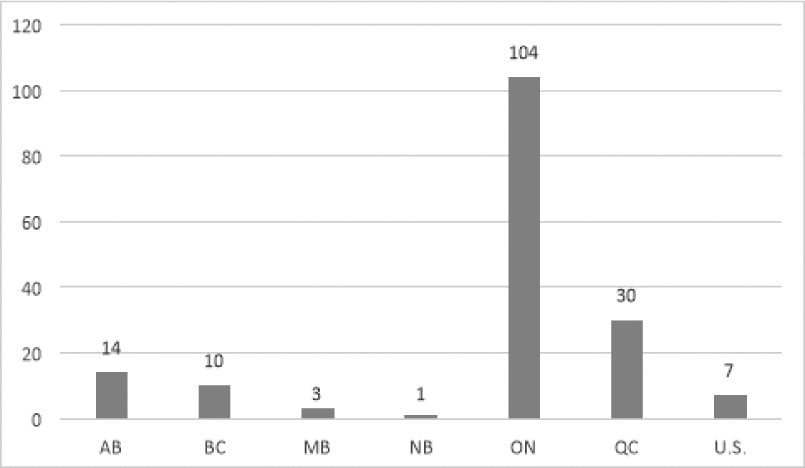

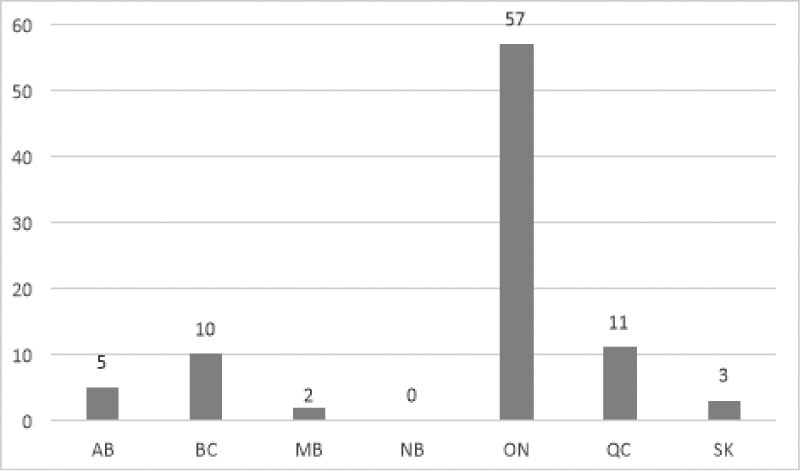

IIROC is the national SRO which oversees all investment dealers and trading activity on debt and equity marketplaces in Canada. IIROC is recognized as an SRO by the CSA (IIROC Recognizing Regulators){3} pursuant to applicable legislation. IIROC's head office is in Toronto with regional offices in Montréal, Calgary and Vancouver. Additional information about IIROC's governance structure, enforcement practices and more, including statistical charts, can be found in Appendix A.

Development and history of IIROC

The Investment Dealers Association of Canada

The Investment Dealers Association of Canada (IDA) was founded in 1916 as the Bond Dealers Section of the Toronto Board of Trade. The IDA evolved into a national SRO for investment dealers. Over the years, Securities Regulators issued orders under their respective legislation to formally recognize the IDA as an SRO. All investment dealers were required by provincial and territorial securities law to be members of a recognized SRO.

The IDA initially had a dual self-regulatory and trade association mandate. In 2006, the Investment Industry Association of Canada was organized and took on the trade association advocacy and member activities. As a result, the sole function of the IDA was the regulation of its members and their registered employees, which was carried out by monitoring and enforcing compliance with IDA rules.

Market Regulation Services Inc.

Market Regulation Services Inc. (RS) was formed in 2002 to provide independent regulation services to Canadian marketplaces and was subsequently recognized as an SRO by some Securities Regulators. The Toronto Stock Exchange and TSX Venture Exchange then chose to outsource to RS, through regulation services agreements, the surveillance, trade desk compliance, investigation and enforcement functions they had historically conducted in-house. The RS mandate was to develop, administer, monitor and enforce marketplace rules applicable to trading practices.

Creation of IIROC

IIROC was created in 2008 through the combination of the IDA and RS into a single organization. At the time, the creation of this new SRO was viewed as a fundamental step to ensuring strong, streamlined, expert self-regulation of Canada's capital markets.

IIROC carries out its regulatory responsibilities by overseeing trading activity on Canadian debt and equity marketplaces, and through setting and enforcing market integrity rules and dealer member rules regarding the proficiency, business and financial conduct of its member firms and their registered representatives. The CSA has also selected IIROC to act as the information processor on trading in Canadian corporate debt securities.{4}

IIROC members also sponsor the Canadian Investor Protection Fund (CIPF), an investor protection fund authorized to provide coverage within prescribed limits to eligible clients in case of an IIROC member's insolvency.

IIROC does not perform any trade association functions for its member firms or individual representatives.

ii) The Mutual Fund Dealers Association of Canada

The MFDA is an SRO responsible for the oversight of mutual fund dealers in Canada, except, as already noted, in Québec. The MFDA is recognized as an SRO by the CSA (MFDA Recognizing Regulators){5} pursuant to applicable legislation. The MFDA head office is in Toronto, with regional offices in Calgary and Vancouver. Additional information about the MFDA's governance structure, enforcement practices, statistical charts and more can be found in Appendix B.

Development and history of the MFDA

The MFDA was established in mid-1998 at the initiative of the CSA{6} in response to the rapid growth of mutual funds from $40 billion to $400 billion in Canada in the late 1980s. At the time, there was a concern that the business and regulatory risks associated with dealers that restricted their business largely to the distribution of mutual funds differed significantly from those with market intermediaries (such as investment dealers) that distributed and advised in a wide range of financial products and services (including equities, securities underwriting and providing margin). The CSA determined that the mutual fund industry and investors would benefit from a separate and distinct self-regulatory structure to accommodate for those differences.

MFDA dealer members also contribute to the MFDA Investor Protection Corporation (MFDA IPC), an investor protection fund established by the MFDA to provide coverage within prescribed limits to eligible clients in case of a MFDA dealer member's insolvency.

The MFDA does not perform any trade association functions for its member firms or individual representatives.

iii) Oversight of SROs in Canada

IIROC and the MFDA are formally recognized as SROs through their respective recognition orders,{7} which are largely harmonized between each jurisdiction. The recognition orders set out the authority of each SRO to carry out certain regulatory functions including: regulating dealer members, establishing and administering its rules and policies, ensuring compliance by dealer members with SRO rules and performing investigation and enforcement functions. In the case of IIROC, this includes monitoring trading activity, providing services to marketplace members and registration functions.

The recognition orders also set out terms and conditions each SRO must comply with in carrying out their regulatory functions. The terms and conditions of recognition require each SRO to operate on a not-for-profit basis and continue to meet set criteria such as:

• ensuring an effective governance structure

• regulating to serve the public interest in protecting (i) investors and (ii) in the case of IIROC, market integrity

• effectively identifying and managing conflicts of interest

• operating on a cost-recovery basis

• maintaining capacity to effectively (i) perform its regulatory functions and (ii) establish and maintain rules and

• complying with ongoing reporting requirements to the applicable recognizing regulators.

The CSA's oversight is coordinated through separate memoranda of understanding (MoUs) for IIROC and the MFDA.{8} The objective of each MoU is to coordinate the CSA's oversight of the SRO's performance of its self-regulatory activities and services, and to ensure it is acting in accordance with its public interest mandate, specifically by complying with the terms and conditions of recognition.

Each MoU provides for a separate oversight committee comprised of staff from the IIROC and MFDA Recognizing Regulators. For purposes of efficiency and to reduce burden on the SROs, a principal regulator is assigned to lead and coordinate the CSA's oversight of each SRO. Each MoU sets out a coordinated oversight program which includes: annual risk assessments, oversight reviews, review and approval of rule proposals, review of various periodic reports and information filed by the SROs, and discussion of ongoing issues with the SROs, among other oversight activities.

iv) Other Registration Categories Regulated Directly by the CSA

CSA members are responsible for the direct regulation and oversight of registrants in the category of exempt market dealer (EMD), portfolio manager (PM), scholarship plan dealer (SPD){9} and investment fund manager (IFM). For a complete description of these categories, please refer to Part 7 of the Companion Policy to NI 31-103.{10} Appendix C also contains statistical information on various registration categories.

The CSA carries out oversight of directly regulated registrants on a harmonized basis through the application of consistent requirements set out under securities laws. Regulated firms must have effective compliance systems, meet certain business conduct requirements, and are subject to financial reporting, working capital, insurance and bonding requirements. The registration requirements and ongoing requirements of registration for both firms and individuals are set out in NI 31-103.{11}

The CSA accomplishes its oversight by activities such as conducting on-site and desk reviews of firms, monitoring capital requirements, participating in "sweep reviews" of targeted issues, and providing guidance through staff notices and outreach. Compliance practices are aligned across Canada to the extent possible by using common examination programs and harmonizing compliance initiatives related to monitoring the activities of regulated firms.

If an individual or firm is not complying with applicable securities laws and the matter is not satisfactorily resolved, a number of actions are possible including the imposition of terms and conditions on a registration, or where appropriate, enforcement actions.

EMDs and their registered dealing representatives may act as a dealer or underwriter for any securities that are distributed to investors in reliance on a prospectus exemption, including securities of a reporting issuer.{12} EMDs are not permitted to act as a dealer or underwriter in a distribution that is being made under a prospectus. Purchasers of securities of issuers that are not reporting issuers may not have the benefit of ongoing information about the security that they are buying or the company selling it, and there may be limited resale opportunities. An EMD is not permitted to participate in the resale of securities that are freely tradeable, if the securities are listed, quoted or traded on a marketplace.

SPDs and their registered dealing representatives may only act as a dealer in respect of a security of a scholarship plan, an educational plan or an educational trust. An SPD typically pools contributions from numerous investors who purchase scholarship plan units through a group registered education savings plan. An IFM affiliated with the SPD typically manages the pooled funds. The units in the pool represent the investor's share of the plan. SPDs are required to provide scholarship plan investors with a plan summary that provides key information highlighting the benefits and risks of the plan.

PMs and their advising representatives provide advice to clients, and typically manage investment portfolios on a discretionary basis on behalf of their clients and based on each client's investment profile. PMs manage investment portfolios on behalf of individual clients, investment funds, foundations, pensions and other institutional clients.

IFMs direct the business, operations or affairs of an investment fund. They organize the fund and are responsible for its management and administration. IFMs do not have individual registrants other than an ultimate designated person and a chief compliance officer.

The CSA can also place restrictions on a dealer or adviser category of registration. For example, a restricted dealer may be limited to specific activities or be allowed to carry on a limited trading business. Similarly, a restricted portfolio manager might be limited to advising in respect of a specific sector, such as oil and gas issuers. CSA registrants can also be registered in more than one category of registration depending on their business activities.

v) Selected International Regulatory Models

United States (U.S.) -- Financial Industry Regulatory Authority (FINRA)

SROs have formed part of securities regulation in the U.S. since 1939 when the National Association of Securities Dealers (NASD) was created in response to the Great Depression through the Maloney Act of 1938. In 2007, the NASD merged with the self-regulatory function of the New York Stock Exchange (the NYSE Regulation, Inc.) to become FINRA which regulates the largest number of securities firms and their brokers in the U.S. today.{13} Additional information about FINRA's governance structure, enforcement practices and more can be found in Appendix D.

For FINRA specifically, and its predecessor, the NASD, the rationale in the U.S. for self regulation was to find a balance that was mutually beneficial to the government and securities industry.

Though other models have been considered by the U.S. Securities and Exchange Commission (SEC), including repatriation of FINRA's functions, the SEC has generally concluded that an SRO would best serve the U.S. markets. The SEC considered multiple SROs to be less favourable because of the increased risk of regulatory capture, where the SRO struggles to act in the public interest or effectively enforce their rules due to funding concerns or other influence from their members. Additionally, the SEC determined that a multiple SRO structure could contribute to market fragmentation.{14}

There are some registrants in the U.S. that are not required to be members of an SRO.

The U.K. Financial Conduct Authority (FCA)

Unlike the U.S., the United Kingdom (U.K.) has moved away from an SRO model by recently establishing two statutory regulators: the FCA, which is the conduct regulator for financial services firms and markets in the U.K., and the Prudential Regulation Authority (PRA), which acts as the prudential regulator for large investment firms, among others. Additional information about the FCA's governance structure, enforcement practices and more can be found in Appendix E.

Originally, securities regulation in the U.K. was performed by three separate SROs: the Securities and Futures Authority, the Investment Management Regulatory Organization, and the Personal Investment Authority. This was viewed as overly burdensome by industry and parliament, resulting in duplicative costs and regulatory fragmentation. Consequently, the Financial Services and Markets Act 2000 dissolved these SROs, with a single statutory regulator, the Financial Services Authority (FSA), taking their place from 2001 -- 2013.

The FSA was abolished by the Financial Services Act 2012{15} in favour of the FCA and the PRA due to failures identified during the Great Recession of 2008 -- 2009. Since its establishment in 2013, the FCA has been tasked with monitoring conduct, supervising trading infrastructures, and operating the U.K. listing regime,{16} while the PRA is tasked with enforcing rules related to sufficient capital and the related risk controls.{17}

3. Informal Consultation Process

Stakeholders Consulted

As noted in the introduction, in late 2019 and early 2020, the CSA completed informal consultations with a wide variety of stakeholder groups in order to solicit views regarding the current SRO regulatory framework. In response to the News Release, CSA staff met with a variety of stakeholders, including those who made a request.

The stakeholder groups included SROs, investor protection funds, groups representing various registrant categories, investment industry associations, and investor advocacy groups.

The objective of the informal consultations was to solicit feedback from stakeholders on the benefits, strengths and challenges of the current SRO regulatory framework as well as to identify opportunities for improvement. The feedback from these informal consultations informed the drafting of this Consultation Paper.

Consultation Questions

The following questions were used to facilitate the informal consultations:

1. What are the benefits of the current SRO regulatory framework?

2. What are the challenges of the current SRO regulatory framework?

3. Overall, how efficient and how effective is the current SRO regulatory framework in Canada?

4. Is the status quo viable in the shorter (under 5 years) or longer (5 years +) terms?

5. What are the key developments in the industry (i.e. innovation, technology, advice, products, consolidation, etc.) since the advent of the two SRO structure and the impact these have had on the current SRO regulatory framework?

6. Is the convergence of registration categories a significant issue? Are there other registration issues that need to be addressed?

7. If there are issues with the current SRO regulatory framework, what options are available to resolve or manage issues?

a) What are the pros and cons of each?

b) What could be the unintended consequences and the likelihood that they could be realized?

c) How could these unintended consequences be mitigated?

8. If not already expressed, what is the ideal solution for the Canadian SRO regulatory framework?

Common Themes

Stakeholders were largely supportive of the informal consultation process. Industry groups and associations, as well as investor advocates all expressed a desire for change to the current regulatory framework given changes that have occurred in the business environment, client needs and expectations, and registrant demographics. Some stakeholders generally prefaced this desire for change with an equal desire for a realistic and achievable plan, potentially considered in several phases.

Although many of the stakeholders commended the SROs' specialized expertise and the benefits of their national scope and reach, they also expressed concerns respecting the current structure. Specifically, stakeholders expressed concern that duplicative costs and a lack of common oversight standards have resulted in multiple compliance teams and differing interpretations of similar rules. Operationally, using different platforms and back-office services have also contributed to higher costs. From an investor standpoint, layers of regulation have contributed to investor confusion as clients are unable to access a broad range of products from one representative or are unsure where to turn to if an issue arises. Lastly, certain stakeholders considered this project an opportunity to enhance the SROs' governance structures to clearly focus on their public interest mandate and strengthen complaint resolution mechanisms.

Though many stakeholders provided suggestions to resolve the challenges with the current regulatory framework, there was no consensus or overall theme noted for solutions, largely due to differing perspectives of the stakeholders.

4. Benefits and Strengths Identified during the Informal Consultations

During the informal consultations, stakeholders identified various benefits and strengths of the current SRO regulatory framework.

National scope of SROs

Numerous stakeholders, including some investment industry associations and investor advocates, agreed that the national structure of an SRO is important in light of the provincial and territorial regulation of the securities industry in Canada. They stated that national SROs{18} provide for a more uniform level of regulation and supervision across the country with one set of rules applicable to all SRO members.{19}

An investments industry association noted that the national structure of the SROs is also important for providing a single point of cooperation with foreign regulatory authorities, such as FINRA, which has a close working relationship with IIROC.

Specialized industry expertise of SROs

Numerous stakeholders commented that SROs' specialized expertise and proximity to the industry enables them to develop appropriate rules, and as needed, propose amendments to those rules in response to changes in the industry. In addition to each SRO having equal numbers of industry and independent board members, both IIROC and the MFDA have industry advisory committees{20}that serve as a forum for advising the SROs on regulatory and policy initiatives, industry trends and practices, as well as voicing industry concerns directly to the regulators. Furthermore, it was noted that SRO staff have developed specialized skills and expertise in their roles, assisting them in delivering oversight of the industry.

Benefits of a two SRO framework

Fit for purpose regulation

Some stakeholders noted that a two SRO model might be well-suited to address the unique aspects of IIROC and MFDA membership whose business models and risks are typically quite different. For example, IIROC dealers are able to offer clients the ability to trade securities and other investment products on margin, or engage in institutional or proprietary trading, which generally results in more complex risks than MFDA dealers who service primarily retail clients and facilitate the trading of fully paid mutual funds. In addition, some IIROC dealer members engage in the business of securities underwriting, and some MFDA dealer members are dually licensed as EMDs or insurance brokers. Historically, IIROC and the MFDA have been able to accommodate these differences through customized rule-making and regulation.

Investor access to two SRO protection funds

As noted in section 2 above, there are two separate member-sponsored investor protection funds in Canada that protect investor assets held by dealer member firms within prescribed limits in the event that the firms become insolvent. IIROC dealer members sponsor CIPF{21}, and MFDA dealer members contribute to the MFDA IPC.{22} Some stakeholders commented that this structure is beneficial for investors with accounts at both IIROC and MFDA dealer member firms, as such investors may have access to coverage by both protection funds.

Marketplace surveillance

In the current SRO regulatory framework, the debt and equity marketplaces in Canada have outsourced their responsibility for monitoring trading activity to IIROC. As part of its mandate, IIROC conducts market surveillance and trading review analysis for these markets to ensure that trading is carried out in accordance with Universal Market Integrity Rules (UMIR) and applicable jurisdictional securities law. Several stakeholders noted that, overall, marketplace surveillance by IIROC works well.

5. Issues Identified During the Informal Consultations

During the informal consultations, stakeholders were asked to provide their perspective on key issues with the current SRO regulatory framework. The issues stakeholders identified generally fell into three broad categories:

- - - - - - - - - - - - - - - - - - - -

Issues At-a-Glance

Structural inefficiencies

1. Duplicative operating costs for dual platform dealers

2. Product-based regulation

3. Regulatory inefficiencies

4. Structural inflexibility

Investor confidence

5. Investor confusion

6. Public confidence in the regulatory framework

Market surveillance

7. Separation of market surveillance from statutory regulators

- - - - - - - - - - - - - - - - - - - -

6. Issues, Targeted Outcomes and Public Consultation

The issues raised by stakeholders have been summarized in this section, and as noted, grouped under the following three categories: structural inefficiencies, investor confidence, and market surveillance. Additionally, these were further subcategorized into seven distinct issues, as informed by those consultations. For each issue, the CSA has noted a targeted regulatory outcome. As this section contains the results of the informal consultations, the views expressed by stakeholders may not necessarily represent the views of the CSA.

In providing comments, some stakeholders referenced various publicly accessible documents to support their views. A collection of those documents is listed in Appendix F. The views, opinions or conclusions expressed in those documents do not necessarily represent the views of the CSA.

- - - - - - - - - - - - - - - - - - - -

General Consultation Questions:

A. The CSA is seeking general comments from the public on the issues and targeted outcomes identified, as well as any other benefits and strengths not listed in section 4 that should be considered. In addition, please identify if there is any other supporting qualitative or quantitative information that could be used to evidence each issue and/or quantify the impact of the issues noted in the Consultation Paper.

B. Are there other issues with the current regulatory framework that are important for consideration that have not been identified? If so, please describe the nature and scope of those issues, including supporting information if possible.

C. Are any of the CSA targeted outcomes listed more important from your perspective than other outcomes? Please explain.

D. With respect to Appendix F, are there other documents or quantitative information / data that the CSA should consider in evaluating the issues in light of the targeted outcomes noted in this Consultation Paper? If so, please refer to such documents.

- - - - - - - - - - - - - - - - - - - -

Issue 1: Duplicative Operating Costs for Dual Platform Dealers

Dual platform dealers are entities with affiliated firms that are registered with each of IIROC and the MFDA in order to service different segments of the investing public. As at December 31, 2019, there were 169 active IIROC dealer members and 88 active MFDA dealer members, of which 25 were dual platform dealers.

Stakeholders indicated that dual platform dealers experience higher operating costs and difficulty in realizing economies of scale. Higher operating costs affect the ability of the dual platform dealers to minimize costs for investors and enhance innovation in the delivery of products and services.

An SRO, an investor protection fund, and two investment industry associations expressed concerns about duplicative costs for dual platform dealers, and that these costs are ultimately borne by investors. Examples of increased operating costs for dual platform dealers include:

i) Separate compliance functions

Dual platform dealers typically maintain separate compliance and supervisory functions. The need to maintain separate compliance and supervisory staff for each platform is the result of differences in requirements and nuances for each registration category, which make it difficult for dealer supervisory staff to effectively monitor for both SRO requirements. In some instances, compliance staff may be required to register with both SROs in order to perform their roles. As the business in each platform continues to grow, compliance and supervision costs grow without the opportunity to capitalize on economies of scale.

ii) Information technology systems

As dual platform dealers are subject to two different sets of rules, their compliance systems and the underlying internal controls are typically different and necessitate separate information technology (IT) back-office systems. Consequently, the associated costs with system upgrades or enhancements are duplicated across both platforms. These upgrades may be required in order to respond to cybersecurity needs or to deliver an enhanced client experience to remain competitive. The prevalence and frequency of these IT changes are expected to increase over time.

iii) Non-regulatory costs

Dual platform dealers, operating as distinct entities may also maintain other separate administrative departments such as financial reporting, legal services, and human resources (HR). The impact of these duplicative costs can be significant, impacting their ability to adapt to an increasingly competitive industry.

iv) Multiple fees

Dual platform dealers incur both IIROC and MFDA membership fees and contribute via quarterly assessments to the respective investor protection funds. Stakeholders indicated that these costs are duplicative and may not be indicative of a corresponding increase in regulatory value{23}. Furthermore, stakeholders noted the incremental cost of maintaining financial institution bond coverage for separate dealers is a regulatory burden.

Targeted Outcome for Consideration

A regulatory framework that minimizes redundancies that do not provide corresponding regulatory value.

- - - - - - - - - - - - - - - - - - - -

Consultation Questions on Duplicative Operating

Costs for Dual Platform Dealers

Question 1.1: What is your view on the issue of duplicative operating costs, and the stakeholder comments described above? Are there other concerns in respect of this issue that have not been identified? If possible, please provide specific reasons for your position and provide supporting information, including the identification of data sources to quantify the impact or evidence your position.

In addressing the question above, please consider and respond to the following, as applicable:

a) Describe instances whereby the current regulatory framework has contributed to duplicative costs for dealer members and increased the cost of services to clients.

b) Describe instances whereby those duplicative costs are necessary and warranted.

c) How have changes in client preferences and dealer business models impacted the operating costs of dealer member firms?

Question 1.2: Is the CSA targeted outcome for issue 1 described appropriately? If yes, how can the targeted outcome be best achieved? If no, what outcome(s) do you suggest and how can they be best achieved?

- - - - - - - - - - - - - - - - - - - -

Issue 2: Product-Based Regulation

Stakeholders noted that there are different rules, or different interpretations of similar rules between each SRO, and also between the SROs in general and the CSA with respect to similar products and services. Stakeholders noted that the products and services offered to clients by different registration categories appear to be converging. Stakeholders also noted that these issues have created an unlevel playing field and opportunities for registrants to take advantage of the differences in rules and interpretations between each SRO and between the SROs and the CSA.

i) Converging registration categories

Many stakeholders including the SROs, the investor advocacy groups, an investor protection fund, and several investment industry associations noted that registrants in different registration categories are providing similar products and services to similar clients but are overseen by different entities (i.e. the SROs and the CSA) and subject to different rules. Specifically, two investment industry associations felt that there is a lack of rule harmonization among each of the SROs and with the CSA, and although regulatory initiatives like the client focused reforms are intended to harmonize registration-related rules, the application and interpretation of those rules across the SROs and the CSA may nevertheless be materially different. For example, the same two investment industry associations noted that the SROs apply similar regulatory requirements (e.g. know-your-client (KYC) and suitability requirements) differently with respect to the same products. They noted that IIROC's rules are more principles-based while the MFDA tends to be more prescriptive. Also, they asserted that a dealer distributing mutual funds may encounter a different level of compliance oversight depending on whether they are a mutual fund dealer or an investment dealer because the SROs evaluate the risks associated with the distribution of retail mutual funds differently.

Two investment industry associations also noted different approaches across the SROs with respect to other significant issues including how client securities are registered (e.g. in client name vs. nominee name) and the permissibility of directed commissions.{24} In addition, an investment industry association and an SRO expressed concerns that there is investor confusion regarding the different registration categories, and that client preferences for "one-stop financial solutions" have evolved beyond the current registration categories. These concerns are described in more detail in Issue 5: Investor Confusion. Possibly due to the concerns cited above, one investor advocacy group noted that the current SRO regulatory framework has not succeeded in promoting the majority of mutual and eligible investment funds to be distributed by one registration category, and under the oversight of one SRO, as originally intended.

ii) Regulatory arbitrage

Two investment industry associations stated that inconsistent application of rules and approaches to compliance between the SROs, and between the SROs and the CSA, create an unlevel playing field and opportunities for registrants to take advantage of these differences.

For the purposes of this Consultation Paper, an activity where registrants can exploit differences in regulatory frameworks to their advantage, in ways that the Securities Regulators did not intend, is referred to as "regulatory arbitrage".

Stakeholders provided some examples of potential regulatory arbitrage where different registration categories are subject to different rules and different oversight. For example:

• mutual funds can be sold by mutual fund dealers, investment dealers, and exempt market dealers,{25}

• exempt market securities can be sold by exempt market dealers, mutual fund dealers,{26} and investment dealers, and

• discretionary portfolio management services can be provided by both investment dealers and portfolio managers.

The same product or service offered by multiple registration categories creates many opportunities for regulatory arbitrage, which can result in inconsistent treatment for registrants engaging in similar activity, and different experiences for investors trying to access similar products and services.

Targeted Outcome for Consideration

A regulatory framework that minimizes opportunities for regulatory arbitrage, including the consistent development and application of rules.

- - - - - - - - - - - - - - - - - - - -

Consultation Questions on Product-Based Regulation

Question 2.1: What is your view on the issue of product-based regulation, and the stakeholder comments described above? Are there other concerns in respect of this issue that have not been identified? If possible, please provide specific reasons for your position and provide supporting information, including the identification of data sources to quantify the impact or evidence your position.

In addressing the question above, please consider and respond to the following, as applicable:

a) Are there advantages and/or disadvantages associated with distributing similar products (e.g. mutual funds) and services (e.g. discretionary portfolio management) to clients across multiple registration categories?

b) Are there advantages and/or disadvantages associated with representatives being able to access different registration categories to service clients with similar products and services?

c) What role should the types of products distributed and a representative's proficiency have in setting registration categories?

d) How has the current regulatory framework, including registration categories contributed to opportunities for regulatory arbitrage?

Question 2.2: Is the CSA targeted outcome for issue 2 described appropriately? If yes, how can the targeted outcome be best achieved? If no, what outcome(s) do you suggest and how can they be best achieved?

- - - - - - - - - - - - - - - - - - - -

Issue 3: Regulatory Inefficiencies

Stakeholders noted that there is inefficient access to certain products and services for some registration categories. Stakeholders also noted inefficiencies and duplicative costs for the CSA in overseeing two SROs, and duplicative fixed costs and overhead at the SROs.

i) Product access by registrants

The SROs and an investment industry association stated that mutual fund dealers are not able to easily distribute exchange traded funds (ETFs) because they have limited access to the necessary back-office and clearing systems servicing primarily investment dealers. These stakeholders stated that although mutual fund dealers can use cumbersome workarounds to service clients (including referring the investor to another dealer, entering into a service arrangement with an IIROC dealer or advising the client to purchase an investment fund that wraps ETFs), these are typically more costly for the investor and, consequently, inefficient alternatives. One investment industry association noted that the barrier to distributing ETFs had more to do with the cost and complexity of integrating different back-office systems between dealers.

ii) Regulatory costs and other inefficiencies

One SRO noted that the current regulatory framework, with multiple registration categories, makes it difficult for any one regulator (i.e. an SRO, a statutory regulator, or the CSA collectively) to identify or effectively resolve issues that span multiple registration categories. Coupled with similar investment products available outside the securities industry to the same clients (e.g. insurance segregated funds), from a regulatory perspective, it is difficult and costly to determine if patterns exist that would warrant regulatory intervention.

An SRO and an investment industry association noted the regulatory burden and inefficiencies associated with the CSA's oversight of two SROs.{27} They noted potential redundancies associated with two SROs that oversee similar dealer activity. For example, there may be duplicative costs related to non-regulatory functions such as HR, IT, and administration. Another SRO noted that the degree of overlap in issues and initiatives among the CSA and the SROs results in more time and resources required for coordination, rather than for regulatory action, resulting in regulatory inefficiencies.

Targeted Outcome for Consideration

A regulatory framework that provides consistent access, where appropriate, to similar products and services for registrants and investors.

- - - - - - - - - - - - - - - - - - - -

Consultation Questions on Regulatory Inefficiencies

Question 3.1: What is your view on the issue of regulatory inefficiencies and the stakeholder comments described above? Are there other concerns in respect of this issue that have not been identified? If possible, please provide specific reasons for your position and provide supporting information, including the identification of data sources to quantify the impact or evidence your position.

In addressing the question above, please consider and respond to the following, as applicable:

a) Describe which comparable rules, policies or requirements are interpreted differently between IIROC, the MFDA and/or CSA; and the resulting impact on business operations.

b) Describe regulatory barriers to the distribution of similar products (e.g. ETFs) available in multiple registration categories.

c) Describe any regulatory risks that make it difficult for any one regulator to identify or effectively resolve issues that span multiple registration categories.

Question 3.2: Is the CSA targeted outcome for issue 3 described appropriately? If yes, how can the targeted outcome be best achieved? If no, what outcome(s) do you suggest and how can they be best achieved?

- - - - - - - - - - - - - - - - - - - -

Issue 4: Structural Inflexibility

Stakeholders noted that evolving business models are limited by the current regulatory framework. Stakeholders also noted that structural inflexibility is creating challenges for dealers to accommodate changing investor preferences, as well as limiting investor access to a broader range of products and services from a single registrant. Lastly, stakeholders noted that the current regulatory framework limits opportunities for professional advancement.

i) Business models

Most stakeholders noted that evolving business models are limited by the current regulatory structure. For example, two investment industry associations noted that the current regulatory structure is creating succession planning challenges for mutual fund dealers and their representatives due to the limited product shelf they can offer to clients. Specifically, these stakeholders noted that many mutual fund dealer representatives who are in the earlier stages of their careers want to provide their clients with access to a broader range of products but are only able to do so by transferring to an investment dealer. As a result, more experienced mutual fund dealer representatives are limited in available options for succession planning for their business. In addition, investment dealers are limited in their ability to grow their business by attracting mutual fund dealer representatives due to the additional proficiency requirements.

The SROs noted that the regulatory framework has not evolved to accommodate the changing scope of advice sought by clients. Specifically, one SRO noted that the complexity of the current regulatory framework affects the ability of its members to launch and grow new business models to meet evolving client needs.

An SRO and an investment industry association noted that the inability for representatives of investment dealers to direct their commissions to be paid to personal corporations creates an unlevel playing field and, in some circumstances, discourages some representatives of mutual fund dealers from transferring their registration and client accounts to investment dealers.

Furthermore, one investment industry association stated, in respect of the IIROC proficiency upgrade rule requirement{28} that requires an individual to be qualified within 270 days of approval as a representative on the IIROC platform, that: (i) the requirement is a burdensome barrier, and (ii) the 270 days to upgrade seems like an artificial time period. That stakeholder also noted that these issues were creating barriers to the ability of investment dealers to attract representatives from mutual fund dealers.

An SRO noted that the current regulatory structure prohibits mutual fund dealers from trading for clients on a limited discretionary basis{29} which has prevented mutual fund dealers from creating certain business models.

ii) Investor preferences

An investment industry association noted that many investors are demanding more transparency and control in the wealth management process, and the ability to move seamlessly between different types of services without having to transfer back and forth across business lines and open new accounts. For example, they noted that under the current regulatory framework, investors need to create and manage separate accounts across different lines of business at the same financial institution in order to access both dedicated full-service and order-execution-only services.

In addition, two investment industry associations indicated that there are several barriers to transferring accounts within a dual platform dealer, including:

• the need to re-paper the client account (e.g. by re-collecting KYC information), and

• loss of historical performance data for client securities and accounts transferred from one of the dual platform dealers to its affiliate (as the SROs consider the holdings transferred to be in a new account).

iii) Access to advice

One investor advocacy group and an investment industry association expressed concern about how the current regulatory framework is affecting clients' access to a broader range of products and services. For example, investment dealers are able to provide clients with access to a broader range of products and services than mutual fund dealers; however, a client's access to an investment dealer may depend on the market value of that client's investment account. An investor advocacy group also noted that clients located in smaller geographic centers and rural communities have difficulty accessing a broad range of products and services because the dealers located in those areas are predominantly mutual fund dealers. This means that geography as well as the size of a client's investment account may have a direct impact on access to different products and services.

An investment industry association also noted that there is a significant increase in technology costs associated with a firm switching from a mutual fund dealer to an investment dealer, which causes some mutual fund dealers not to switch and has the effect of reducing access to a broader range of products and services for some clients.

iv) Technological advancements

An SRO indicated that with technological advancements and changing investor preferences and expectations (e.g. offering holistic investment advice through robo-advice, online investing services or hybrid human/digital advisory models, etc.), the current regulatory framework has not provided sufficient flexibility for industry to adapt to changing investor needs.

v) Professional advancement

One investment industry association noted that the existing higher IIROC proficiency standard makes the transition from mutual fund dealer to investment dealer representative challenging. That same stakeholder noted that as representatives become more experienced and deal with larger client accounts, the 270 days is too short a time period to actually upgrade proficiency, and therefore artificially limits access to a broader range of services and products (e.g. ETFs) needed to meet clients' changing investment needs and preferences.

Targeted Outcome for Consideration

A flexible regulatory framework that accommodates innovation and adapts to change while protecting investors.

- - - - - - - - - - - - - - - - - - - -

Consultation Questions on Structural Inflexibility

Question 4.1: What is your view on the issue of structural inflexibility, and the stakeholder comments described above? Are there other concerns in respect of this issue that have not been identified? If possible, please provide specific reasons for your position and provide supporting information, including the identification of data sources to quantify the impact or evidence your position.

In addressing the question above, please consider and respond to the following, as applicable:

a) How does the current regulatory framework either limit or facilitate the efficient evolution of business?

b) Describe instances of how the current regulatory framework limits dealer members' ability to utilize technological advancements, and how this has impacted the client experience.

c) Describe factors that limit investors' access to a broad range of products and services.

d) How can the regulatory framework support equal access to advice for all investors, including those in rural or underserved communities?

e) How have changes in client preferences impacted the business models of registrants that are required to comply with the current regulatory structure?

Question 4.2: Is the CSA targeted outcome for issue 4 described appropriately? If yes, how can the targeted outcome be best achieved? If no, what outcome(s) do you suggest and how can they be best achieved?

- - - - - - - - - - - - - - - - - - - -

Issue 5: Investor Confusion

Several stakeholders expressed concern that investors are generally confused by the current regulatory structure; specifically, the inability to access similar investment products and services from a single source, the complaint process, investor protection fund coverage, and multiple registration categories and titles.

i) Regulatory overlap

Several stakeholders stated that the current regulatory framework is complex and/or fragmented. They indicated that investors are confused by the number of regulatory organizations and the role or jurisdiction these organizations are responsible for respecting securities regulation in Canada. Investors struggle to distinguish between the roles of an SRO and the Securities Regulators, as well as the services and products provided by IIROC and MFDA dealer members.{30} Furthermore, an investment industry association noted that a separate regime for mutual fund dealers in Québec{31} further adds to the complex nature of the regulatory framework. These overlapping regulatory environments may increase investor confusion and contribute to differing views regarding the SROs' roles and their relationships with the Securities Regulators.

Specifically, two SROs and an investment industry association indicated that investors may not be able to discern between the products and services provided by an IIROC dealer and an MFDA dealer:

• IIROC and the MFDA perform similar types of member regulation, but for different entities and, for the most part, different investment products. IIROC regulates investment dealers and all types of trading (including stocks, bonds and mutual funds), whereas the MFDA regulates mutual fund dealers and trading limited primarily to mutual funds. Investors may not realize that other products or services are only available in another registration category and that their representative may not be able to provide access. Thus, investors may have limited access to products and services unless they are directed to another category of registrant.

• Some firms with affiliated IIROC and MFDA members operate in the same location where clients may purchase securities from IIROC or MFDA representatives. However, the client is not necessarily aware that the same, or other, investment products or services may be available from an affiliate firm, each of which is subject to a separate and distinct regulatory regime.

From the investors' perspective, their IIROC dealer and MFDA dealer provide the same service or product offering, which may not always be the case. As their net worth and investment knowledge grows, many investors naturally progress from investing in mutual funds to ETFs to other products and services that are not offered by an MFDA dealer. To facilitate this growth, the investor may be required to change firms or representatives, resulting in confusion and unnecessary inconvenience.

ii) Complaint resolution

Many stakeholders noted that investors have difficulty understanding and accessing the complaint process to pursue recourse caused by misconduct. Specifically, they raised concerns regarding where to direct complaints, how to file a complaint and from which regulatory body or organization to seek redress. While investors can rely on many avenues of recourse in the current securities regulatory framework, they may not be able to efficiently access them or may choose not to access them. The avenues of recourse available to investors include:

• the internal complaint resolution process of the entity from which they purchased the security (e.g. customer service group and internal ombudsman),

• the independent dispute resolution services of the Ombudsman for Banking Services and Investments (OBSI){32} notwithstanding that such decisions are not legally binding and are subject to compensation limits,

• making a complaint directly with the applicable SRO,

• an arbitration mechanism, or

• litigation.

Additionally, in Québec, the AMF also processes complaints filed by consumers and provides them with access to dispute resolution services.

iii) Investor protection fund coverage

Some stakeholders noted that differences in the availability of investor protection fund coverage among registration categories, and the types of investments and losses that are covered, creates confusion for investors.

As noted, CIPF and the MFDA IPC are the approved investor protection funds for investors of IIROC and MFDA dealer members, respectively.{33} There are no approved investor protection funds for investors of other registration categories that are regulated directly by the CSA; however, portfolio managers can enter into a service arrangement to custody client assets at IIROC dealer members which may result in CIPF coverage.{34}

Both investor protection funds expressed concern that investors are confused and unsure of the coverage, if any, provided upon the insolvency of an SRO dealer member. They further noted that investors are uncertain as to the types of eligible claims covered by investor protection funds and may mistakenly believe that market losses qualify for coverage.

Specifically, one investor protection fund referred to an example where investors dealing with the insolvency of an SRO dealer member and several affiliates with similar names, some regulated by the CSA, faced confusion regarding coverage due to complexities in the regulatory framework and lack of proper disclosure. Investors were confused about the availability of coverage and ultimately discovered that no coverage was available under any investor protection fund.

While both the SROs require members to inform their clients regarding the protection fund coverage available to them, there is no corresponding obligation for other categories of registrants to inform their clients about the lack of direct coverage prior to opening a new account. Accordingly, it appears that investment decisions regarding coverage may not be made based on complete and accurate information, resulting in investor confusion in the event of a registrant's insolvency.

iv) Multiple registration categories and titles

Two investor advocacy groups stated that there is investor confusion regarding the different rules for different registration categories{35} and the number and variety of business titles used by representatives in various registration categories. This confusion contributes to investors not understanding that investment choice is limited based on a registration category. It also contributes to investors having expectations of registrants that are not aligned with the duties and qualifications of that category of registrant. For example, clients may not view registered firms and the representatives that they deal with as salespeople. Instead, they may see a relationship with a trusted financial advisor designed to deliver the products and services they need. This can result in client suitability issues and unnecessary efforts to find the appropriate distribution channel and service provider for the desired investments.

Targeted Outcome for Consideration

A regulatory framework that is easily understood by investors and provides appropriate investor protection.

- - - - - - - - - - - - - - - - - - - -

Consultation Questions on Investor Confusion

Question 5.1: What is your view on the issue of investor confusion, and the stakeholder comments described above? Are there other concerns in respect of this issue that have not been identified? If possible, please provide specific reasons for your position and provide supporting information, including the identification of data sources to quantify the impact or evidence your position.

In addressing the question above, please consider and respond to the following, as applicable:

a) What key elements in the current regulatory framework (i) mitigate and (ii) contribute to investor confusion?

b) Describe the difficulties clients face in easily navigating complaint resolution processes.

c) Describe instances where the current regulatory framework is unclear to investors about whether or not there is investor protection fund coverage.

Question 5.2: Is the CSA targeted outcome for issue 5 described appropriately? If yes, how can the targeted outcome be best achieved? If no, what outcome(s) do you suggest and how can they be best achieved?

- - - - - - - - - - - - - - - - - - - -

Issue 6: Public Confidence in the Regulatory Framework

Stakeholders noted concerns regarding a possible lack of public confidence in the current SRO regulatory framework. Some stakeholders stated that the SRO governance structure does not adequately support the SROs' public interest mandate due to an industry-focused board of directors and lack of a formal mechanism to incorporate investor feedback. In addition, these stakeholders expressed concern regarding regulatory capture and ineffective SRO compliance and enforcement practices contributing to the erosion of public confidence in the SROs' ability to deliver on their public interest mandate.

i) Public interest mandate

Investor advocacy groups stated that the SRO boards of directors are mainly composed of current and former securities industry participants. They are concerned that independent directors{36} with close ties to industry limit the ability of the SROs to carry out their regulatory responsibilities and public interest mandates, as set out in their recognition orders, due to their potential bias.{37} Two investor advocacy groups expressed concern that independent directors' possible bias in board decision making, or undue influence of specific industry stakeholder interests, may occur due to the following governance structure elements:

• rules and procedures on the composition of the SROs' board of directors, committees and councils,

• cooling off periods (which require a former industry member to have left industry for as little as one year before the candidate can be considered independent for the purposes of each SRO board) and term limits, and

• the definition of an independent director.{38}

Stakeholders indicated that if a public interest mandate is not actualized by an appropriate governance structure that manages conflicts of interest and ensures different stakeholders are fairly represented, there is a risk that a loss of confidence can occur in the SRO's ability to meet its public interest mandate.

ii) Formal investor advocacy mechanisms

Investor advocacy groups raised concerns that the lack of formal SRO mechanisms to facilitate investor consultation impedes the appropriate representation and consideration of investor concerns. Specifically, they noted a shortage of independent voices on SRO committees and councils, and a perception of unwillingness of one SRO to engage in regulatory policy discussions that raise investor concerns. In addition, these investor advocacy groups noted that the SROs' reliance on direct input through quantitative online surveys conducted by independent research firms to gauge the public's views on regulatory initiatives and/or other public interest matters, is no substitute for appropriately funded and resourced SRO investor advisory panels (of which there are currently none) which could be more effective in shaping the development of SRO rules, policies and other similar instruments.{39} Without full engagement between SROs and investor representatives, it may be difficult for an SRO to identify the interests of the public and thereby fulfill its public interest mandate effectively.

iii) Regulatory capture

In this Consultation Paper, "regulatory capture" refers to a regulatory agency that may become dominated by the industries or interests they are charged with regulating. The result is that an agency, charged with acting in the public interest, instead acts in ways that benefit the industry it is supposed to be regulating. Factors that cause regulatory capture include a regulator being subject to excessive levels of influence from industry stakeholders, a regulator not having sufficient tools and resources to obtain accurate information from industry or to deter industry wrongdoing, or regulatory incentives being skewed toward industry stakeholder interests.

An investor advocacy group stated that the inherent conflict between the SROs' obligation to their members and their public interest mandates may not be manageable under their current governance structures and may result in the erosion of public confidence. Specifically, they expressed concern about regulatory capture occurring when SRO actions are inappropriately influenced by industry stakeholder interests. By contrast, two investment industry associations stated that SROs need to be more responsive to industry, with one noting that its inability to directly access an SRO's board of directors runs contrary to the concept of 'self'-regulation.

iv) SRO compliance and enforcement concerns

Investor advocacy groups expressed general concern regarding the lack of transparency and the robustness of the SRO regulatory compliance and enforcement practices. They stated that slow regulatory reforms undermine the improvement of conduct standards, and that the following factors worsen enforcement outcomes:

• modest sanctions that are primarily designed as a deterrence tool (instead of delivering investor restitution),

• governance shortcomings, such as those noted in sub-issue i) above,

• SRO rules regarding complaint handling that lead to relatively low levels of complaints reaching litigation.

Specifically, two investor advocacy groups noted instances where SROs levied sanctions against representatives only, even when dealer member supervision and compliance deficiencies were also apparent. They expressed concern regarding a lack of transparency in notices of disciplinary actions, decisions and settlements regarding findings of potential culpability of dealer members and senior management. They concluded that this approach leaves the perception that SROs are more concerned about protecting member firms rather than the investing public, and accordingly, do not assist in effectively deterring misconduct, thereby not preserving public confidence, consumer protection and market integrity.

Two investment industry associations also raised concerns about one SRO taking a punitive approach to its enforcement proceedings, in contrast to another SRO which they viewed as more focused on remediation. One of these stakeholders noted the presence of inconsistencies among SRO sanctions for the same type of infraction or instance of non-compliance.

v) CSA oversight of SROs

Several stakeholders expressed concern that the current regulatory structure does not result in the SROs being sufficiently accountable to the CSA.{40} The following are examples of concerns raised by stakeholders:

• the CSA does not appoint or have veto over SRO board members or key executive staff, nor does the CSA have a seat on the board,

• the SRO rule exemption process is not designed to ensure SRO accountability to the CSA, and

• the CSA SRO oversight reviews leave a perception that the reviews focus mainly on technical issues.

Two investment industry associations representing registrants directly regulated by the CSA raised concerns that SROs are inherently conflicted, have compliance programs that are suited to larger firms and are not sustainable for small dealers due to the regulatory burden and related costs.

Targeted Outcome for Consideration

A regulatory framework that promotes a clear, transparent public interest mandate with an effective governance structure and robust enforcement and compliance processes.

- - - - - - - - - - - - - - - - - - - -

Consultation Questions on Public Confidence in the Regulatory Framework

Question 6.1: What is your view on the issue of public confidence in the regulatory framework, and the stakeholder comments described above? Are there other concerns in respect of this issue that have not been identified? If possible, please provide specific reasons for your position and provide supporting information, including the identification of data sources to quantify the impact or evidence your position.

In addressing the question above, please consider and respond to the following, as applicable:

a) Describe changes that could improve public confidence in the regulatory framework.

b) Describe instances in the current regulatory framework whereby the public interest mandate is underserved.

c) Describe instances of how investor advocacy could be improved.

d) Describe instances of regulatory capture in the current regulatory framework.

e) Do you agree, or disagree, with the concerns expressed regarding SRO compliance and enforcement practices? Are there other concerns with these practices?

Question 6.2: Is the CSA targeted outcome for issue 6 described appropriately? If yes, how can the targeted outcome be best achieved? If no, what outcome(s) do you suggest and how can they be best achieved?

- - - - - - - - - - - - - - - - - - - -

Issue 7: The Separation of Market Surveillance from Statutory Regulators (CSA)

IIROC was established through the combination of RS and the IDA and continues to carry out the functions of both its predecessors to this day. Accordingly, in addition to carrying out the oversight functions respecting investment dealers, IIROC also carries out the prior RS market surveillance functions, including supervision of member compliance with UMIR. Pursuant to the recognition orders with IIROC Recognizing Regulators, IIROC conducts surveillance of trading activity on Canadian debt and equity marketplaces. Any marketplace that retains IIROC as its regulation services provider to regulate equity trading activity is a marketplace member. All firms operating as alternative trading systems must become dealer members, in addition to being marketplace members.

Marketplace operations are regulated by the applicable Securities Regulators,{41} which require IIROC to provide information necessary for investigations into possible market misconduct.{42} IIROC coordinates surveillance capabilities with other jurisdictions as a member of the Intermarket Surveillance Group.{43} To enhance transparency in fixed income markets, the CSA selected IIROC to be the information processor for trading in Canadian corporate debt securities.{44}

Stakeholders raised concerns about possible information gaps and fragmented market visibility resulting from market surveillance functions being separated from Securities Regulators.

i) Regulatory fragmentation and systemic risk

The MFDA expressed concerns regarding the ability of statutory regulators to effectively monitor systemic risk and inform market structure policy without sufficient expertise and direct access and control over market data.

ii) Member vs market regulation functions

An investor protection fund raised a question about the integration of member and market surveillance in an SRO and the potential for conflicts that could possibly arise between the obligations respecting the disruption to markets and maintaining market integrity versus exposure to the investing public.

iii) Inefficient structure

The MFDA also questioned the appropriateness of the current market surveillance structure and whether the CSA ought to play a larger role. The SRO noted that IIROC and the CSA enforcement processes might be less effective, inefficient, and more costly as a result of the duplication of surveillance and data analysis efforts between IIROC and the CSA.

Targeted Outcome for Consideration

An integrated regulatory framework that fosters timely, efficient access to market data and effective market surveillance, to ensure appropriate policy development, enforcement, and management of systemic risk.

- - - - - - - - - - - - - - - - - - - -

Consultation Questions on the Separation of Market Surveillance from Statutory Regulators (CSA)

Question 7.1: What is your view on the separation of market surveillance from statutory regulators, and the stakeholder comments described above? Are there other concerns in respect of this issue that have not been identified? If possible, please provide specific reasons for your position and provide supporting information, including the identification of data sources to quantify the impact or evidence your position.

In addressing the question above, please consider and respond to the following, as applicable:

a) Does the current regulatory structure facilitate timely, efficient and effective delivery of the market surveillance function? If so, how? If not, what are the concerns?

b) Does the continued performance of market surveillance functions by an SRO create regulatory gaps or compromise the ability of statutory regulators to manage systemic risk? Please explain.

Question 7.2: Is the CSA targeted outcome for issue 7 described appropriately? If yes, how can the targeted outcome be best achieved? If no, what outcome(s) do you suggest and how can they be best achieved?

- - - - - - - - - - - - - - - - - - - -

7. Public Consultation Process and Next Steps

Public Consultation Process, Including Deadline for Comments

The CSA invites participants to provide input. You may submit written comments in electronic form (preferred) or in hard copy. Please submit your comments in writing on or before October 23, 2020. If you are not sending your comments by email, please send us an electronic file containing submissions provided (in Microsoft Word format).

Please address your comments to each of the following:

Alberta Securities Commission

Autorité des marchés financiers

British Columbia Securities Commission

Financial and Consumer Services Commission (New Brunswick)

Financial and Consumer Affairs Authority of Saskatchewan

Manitoba Securities Commission

Nova Scotia Securities Commission

Nunavut Securities Office

Office of the Superintendent of Securities, Newfoundland and Labrador

Office of the Superintendent of Securities, Northwest Territories

Office of the Yukon Superintendent of Securities

Ontario Securities Commission

Superintendent of Securities, Department of Justice and Public Safety, Prince Edward Island

Please send your comments only to the addresses below. Your comments will be forwarded to the other CSA member jurisdictions.

The Secretary

Ontario Securities Commission

20 Queen Street West, 22nd Floor

Toronto, Ontario M5H 3S8

Fax: 416-593-2318

E-mail: [email protected]

Me Philippe Lebel, Corporate Secretary and Executive Director, Legal Affairs

Autorité des marchés financiers

Place de la Cité, tour Cominar

2640, boulevard Laurier, bureau 400

Québec (Québec) G1V 5C1

Fax: 514-864-6381

E-mail: [email protected]

Certain CSA jurisdictions require publication of the written comments received during the comment period. All comments received will be posted on the websites of each of the ASC at www.albertasecurities.com, the AMF at www.lautorite.qc.ca and the OSC at www.osc.gov.on.ca. Please do not include personal information directly in comments to be published and state on whose behalf you are making the submission.

Questions

If you have any comments or questions, please contact any of the CSA staff listed below.

|

Doug MacKay |

Joseph Della Manna |

|

Co-Chair -- CSA Working Group |

Co-Chair -- CSA Working Group |

|

Manager, Market and SRO Oversight |

Manager, Market Regulation |

|

British Columbia Securities Commission |

Ontario Securities Commission |

|

604-899-6609 |

416-204-8984 |

|

Paula Kaner |

Jean-Simon Lemieux |

|

Manager, Market Oversight |

Analyste expert |

|

Alberta Securities Commission |

Autorité des marchés financiers |

|

403-355-6290 |

514-395-0337, ext. 4366 |

|

Liz Kutarna |

Jason Alcorn |

|

Deputy Director, Capital Markets |

Senior Legal Counsel and Special Advisor to the Executive Director |

|

Financial and Consumer Affairs Authority of Saskatchewan |

Financial and Consumer Services Commission (New Brunswick) |

|

306-787-5871 |

506-643-7857 |

|

Paula White |

Chris Pottie |

|

Deputy Director, Compliance and Oversight |

Deputy Director, Registration & Compliance |

|

Manitoba Securities Commission |

Nova Scotia Securities Commission |

|

204-945-5195 |

902-424-5393 |

Next Steps

The issues and CSA targeted outcomes in this Consultation Paper likely affect key stakeholders of the Canadian financial services industry. Upon the completion of the 120-day comment period, the CSA staff will review all public comments submitted. The CSA expects to gather a great amount of information from the consultation process, which will be used to inform our approach going forward. The outcome of the consultation process will result in a paper with a CSA proposed option whereby the CSA would seek further public comment.

{1} https://www.securities-administrators.ca/aboutcsa.aspx?id=1853

{2} In Québec, mutual fund dealers with operations and clients only within that province are directly supervised by the AMF, but those operating and/or advising clients also in other Canadian jurisdictions must be members of the MFDA. Registered individuals in the category of mutual fund representatives must also be members of the Chambre de la sécurité financière (CSF), a statutory SRO under the direct supervision of the AMF with responsibilities of maintaining discipline and overseeing the training and ethics of its members. The MFDA has entered into a Co-operative Agreement with the AMF and the CSF to facilitate information sharing and supervision of MFDA members with operations in that province.

{3} IIROC is recognized by the Alberta Securities Commission (ASC), the AMF, the British Columbia Securities Commission (BCSC), the Financial and Consumer Affairs Authority of Saskatchewan (FCAA), the Financial and Consumer Services Commission of New Brunswick (FCNB), the Manitoba Securities Commission (MSC), the Nova Scotia Securities Commission (NSSC), the Office of the Superintendent of Securities Service Newfoundland and Labrador (NL), the Ontario Securities Commission (OSC), the Prince Edward Island Office of the Superintendent of Securities Office (PEI), the Northwest Territories Office of the Superintendent of Securities, the Nunavut Securities Office, and the Office of the Yukon Superintendent of Securities.

{4} Amendments to National Instrument 21-101 Marketplace Operation (NI 21-101), in force as at August 31, 2020, subject to Ministerial approval, prescribe mandatory post-trade transparency of trades in government debt securities. IIROC's role as information processor will be expanded to include transactions in government debt securities.

{5} The MFDA is recognized by the ASC, BCSC, FCAA, FCNB, MSC, NSSC, OSC, and PEI.

{6} The CSA initiated discussions with the IDA and the Investment Funds Institute of Canada. The result of these efforts was the establishment of the MFDA as an SRO for mutual fund dealers.

{7} https://www.iiroc.ca/about/governance/Pages/default.aspx#recognitionorders; https://mfda.ca/about/sro-recognition

{8} https://www.iiroc.ca/about/governance/Documents/MemorandumOfUnderstanding_en.pdf; https://www.bcsc.bc.ca/Securities_Law/Policies/PolicyBCN/PDF/MFDA_Memorandum_of_Understanding_JRRP__October_10_2013/

{9} In Québec, registered individuals in the SPD category must also be members of the CSF.

{10} https://www.bcsc.bc.ca/Securities_Law/Policies/Policy3/PDF/31-103CP__CP___December_4__2017/

{11} https://www.bcsc.bc.ca/Securities_Law/Policies/Policy3/PDF/31-103__NI___June_12__2019/

{12} https://www.bcsc.bc.ca/Securities_Law/Policies/Policy4/PDF/45-106__NI___October_5__2018/

{13} https://www.sec.gov/news/press/2007/2007-151.htm