Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

CSA Staff Notice 51-355 Continuous Disclosure Review Program Activities for the fiscal years ended March 31, 2018 and March 31, 2017

CSA Staff Notice 51-355 Continuous Disclosure Review Program Activities for the fiscal years ended March 31, 2018 and March 31, 2017

July 19, 2018

Introduction

As announced on July 27, 2017, the Canadian Securities Administrators (CSA) will now publish the CSA Staff Notice (Notice) detailing the results of the Continuous Disclosure Review Program (CD Review Program) on a biennial instead of an annual basis.

This Notice contains the results of the reviews conducted by the CSA within the scope of their CD Review Program. The goal of the program is to improve the completeness, quality and timeliness of continuous disclosure provided by reporting issuers{1} (issuers) in Canada. This program was established to assess the compliance of continuous disclosure (CD) documents and to help issuers understand and comply with their obligations under the CD rules so that investors receive high quality disclosure.

In this Notice, we summarize the results of the CD Review Program for the fiscal year ended March 31, 2018 (fiscal 2018) and the fiscal year ended March 31, 2017 (fiscal 2017). Appendix A -- Financial Statement, MD&A and Other Regulatory Deficiencies (Appendix A) includes information about areas where common deficiencies were noted, with examples in certain instances, to help issuers address these deficiencies and to illustrate best practices.

For further details on the CD Review Program, see CSA Staff Notice 51-312 (revised) Harmonized Continuous Disclosure Review Program.

Results for Fiscal 2018 and Fiscal 2017

Issuers selected for a CD review (full or issue-oriented review (IOR)) are identified using a risk-based and outcomes-focused approach using both qualitative and quantitative criteria. IORs may be based on a specific accounting, legal or regulatory issue, an emerging issue or industry, implementation of recent rules or on matters where we believe there may be a heightened risk of investor harm. A review may also stem from general monitoring of our issuers through news releases, media articles, complaints and other sources.

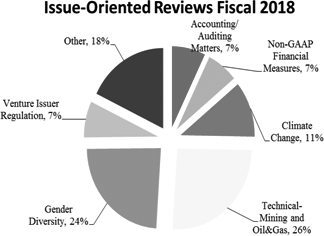

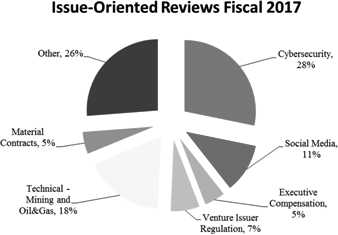

During fiscal 2018, a total of 840 CD reviews (fiscal 2017 -- 1,014 CD reviews) were conducted with IORs consisting of 81% of the total (fiscal 2017 -- 80%). The nature of an IOR will impact the time spent and outcome obtained from the review. The following are some of the IORs conducted by one or more jurisdictions:

The "Other" category includes, but is not limited to, reviews of:

• Emerging industries (including cryptocurrencies and cannabis)

• Certification of disclosure

• Social media

• News releases

• Public complaints

The "Other" category includes, but is not limited to, reviews of:

• Gender diversity

• Corporate governance

• Financial statement/MD&A

• Change of auditor notice

• Public complaints

CD Outcomes for Fiscal 2018 and Fiscal 2017

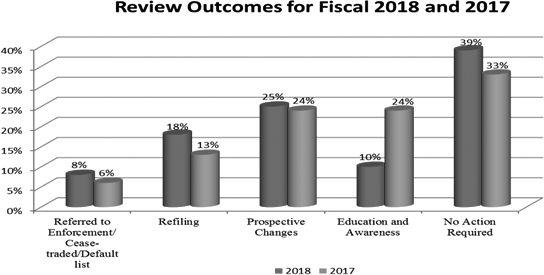

In fiscal 2018, 51% (fiscal 2017 -- 43%) of our review outcomes required issuers to take action to improve and/or amend their disclosure or resulted in the issuer being referred to enforcement, cease traded or placed on the default list.

We classify the outcomes of the full reviews and IORs into five categories as described in Appendix B -- Categories of Outcomes. Some CD reviews may generate more than one category of outcome. For example, an issuer may have been required to refile certain documents and also make certain changes on a prospective basis.

Given our risk-based approach noted above, the outcomes on a year to year basis may vary and cannot be interpreted as an emerging trend. The issues as well as the issuers reviewed each year might be different. In fiscal 2018 we continued to see substantive outcomes being obtained as a result of our reviews as noted in the categories of refilings and referred to enforcement/default list/cease traded.

We have highlighted below some of the deficiencies that we have encountered during our CD reviews in fiscal 2018 and 2017. We have discussed some of these deficiencies in further detail in Appendix A to this Notice.

• Financial Statements: compliance with recognition, measurement and disclosure requirements in International Financial Reporting Standards (IFRS), which included, but was not limited to, statement of cash flows, fair value measurements, disclosure of accounting policies, accounting for business combinations, revenue recognition, related party transactions and significant judgements and estimates.

• Management's Discussion and Analysis (MD&A): compliance with Form 51-102F1 of NI 51-102 (Form 51-102F1), which included, but was not limited to, non-GAAP financial measures, discussion of operations including disaggregation of investment portfolios, additional information about concentrated investments, liquidity, related party transactions and forward looking information.

• Other Regulatory Requirements: compliance with other regulatory matters, which included, but was not limited to, mining technical reports, gender diversity disclosure, executive compensation disclosure, climate change, unbalanced and misleading social media posts, filing of previously unfiled documents, such as material contracts, and clarifying news releases or material change reports to address concerns around unbalanced or insufficient disclosure.

Results by Jurisdiction

All CSA jurisdictions participate in the CD review program and some local jurisdictions may publish staff notices and reports communicating results and findings of the CD reviews conducted in their jurisdictions. Refer to the individual regulator's website for copies of these notices and reports:

• www.bcsc.bc.ca• www.albertasecurities.com• www.osc.gov.on.ca• www.lautorite.qc.ca

{1} In this Notice "issuers" means those reporting issuers contemplated in National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102).

APPENDIX A

FINANCIAL STATEMENT, MD&A AND OTHER REGULATORY DEFICIENCIES

Our CD reviews identified a number of financial statement, MD&A and other regulatory deficiencies that resulted in issuers enhancing their disclosure and/or refiling their CD documents. To help issuers better understand and comply with their CD obligations, we present the key observations from our reviews. The hot buttons section includes observations along with considerations for issuers including the relevant authoritative guidance. We have also included in some instances, examples of deficient disclosure contrasted against more robust entity-specific disclosure or a more in-depth explanation of the matters we observed.

Issuers must ensure that their CD record complies with all relevant securities legislation. The volume of disclosure filed does not necessarily equate to full compliance.

The following observations are provided for illustrative purposes only. This is not an exhaustive list and does not represent all the requirements that could apply to a particular issuer's situation.

FINANCIAL STATEMENT DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

FINANCIAL STATEMENTS |

||||

|

|

||||

|

Statement of Cash Flows |

|

|

|

|

|

|

• |

Some issuers incorrectly classify cash flows as investing or financing activities on the statement of cash flows when they should be classifying them as operating activities. |

• |

Cash flows from operating activities is often an important metric for issuers and stakeholders as it may provide an indication of the financial health of the issuer. Classifying items of an operating nature in investing or financing activities may present a misleading picture of the issuer's operations. |

|

|

|

|

• |

Cash flows that are primarily derived from the principal revenue-producing activities of the issuer should be classified as cash flows from operating activities. |

|

|

|

|

• |

For example, financial institutions should classify cash advances or loans as operating activities. For rental companies, payments to acquire assets held for rental and the cash receipts from rents and the subsequent sales of such assets should be classified as cash flows from operating activities. |

|

|

||||

|

|

• |

Some issuers reclassify items on the statement of cash flows without disclosing the reasons for the reclassification. |

• |

If an entity changes the presentation or classification of items in its financial statements in a period, it should reclassify comparative amounts unless reclassification is impracticable. |

|

|

|

|

• |

When an entity reclassifies comparative amounts, it should disclose: (1) the nature of the reclassification; (2) the amount of each item or class of items that is reclassified; and (3) the reason for the reclassification. |

|

|

||||

|

|

|

|

Reference: IAS 1 Presentation of Financial Statements paragraph 41; IAS 7 Statement of Cash Flows paragraphs 14 and 15. |

|

|

|

||||

|

Fair Value Measurements -- Level 3 |

|

|

|

|

|

|

• |

Some issuers do not provide sufficient disclosure of the valuation techniques, processes and policies used in the fair value measurements categorized within Level 3 of the fair value hierarchy. |

• |

Fair value disclosures help users of financial statements assess the techniques and inputs used to develop the fair value measurements. |

|

|

• |

In addition, some issuers do not provide disclosure of quantitative information about the significant unobservable inputs used in the fair value measurement categorized within Level 3, and are not providing a narrative description of the sensitivity of the fair value measurement to changes in those unobservable inputs. |

• |

For fair value measurements categorized within Level 3 of the fair value hierarchy, issuers must describe the valuation technique(s) and the inputs used in the fair value measurement. Disclosure of quantitative information about the significant unobservable inputs used in the fair value measurement may also be required. Generally, where issuers simply provide a list of the inputs, we ask issuers to quantify those inputs. |

|

|

|

|

• |

Issuers must also provide a narrative description of the sensitivity of the fair value measurement to changes in unobservable inputs if the change results in a significantly higher or lower fair value measurement. If a change in one or more of the unobservable inputs to reflect reasonably possible alternative assumptions would change fair value significantly, issuers should state that fact and disclose the effect of those changes quantitatively. |

|

|

|

|

• |

For example, in the cannabis industry, issuers must account for biological assets at fair value less costs to sell. We are of the view that these are Level 3 fair value measurements and are subject to all the disclosure requirements noted above as well as the other requirements in IFRS 13. |

|

|

||||

|

|

|

|

Reference: IFRS 13 Fair Value Measurement paragraphs 91, 93(d), 93(g) and 93(h). |

|

|

|

||||

|

Adoption of New Accounting Policies |

|

|

|

|

|

|

• |

Some issuers do not provide sufficient qualitative and quantitative disclosures regarding the possible impact that the initial adoption of an IFRS standard is expected to have on its financial statements in the period of initial application. |

• |

Issuers should provide progressively more detailed qualitative and quantitative information in their filings about the expected effect a new IFRS standard will have on their financial statements as they progress in their implementation efforts and the effective dates approach. This is particularly important if the new IFRS standard is expected to have a material impact. |

|

|

• |

Some issuers provide general disclosures about the new IFRS standard without providing entity-specific effects the new IFRS standard will have on the issuer. |

• |

If the quantitative impact cannot yet be reasonably estimated, issuers should consider providing additional qualitative information to enable users to understand the expected impact on future financial statements, including the anticipated directional impact of applying the new IFRS standard. |

|

|

|

|

• |

If the impact of adopting a new IFRS standard is not expected to be material, issuers should disclose this fact. |

|

|

|

|

• |

IFRS 16 Leases is effective for years beginning on or after January 1, 2019, and we remind issuers to provide the required disclosure for this upcoming standard in their CD documents during the fiscal year. |

|

|

||||

|

|

|

|

Reference: IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors, paragraphs 28, 30 and 31; Item 1.13 of Form 51-102F1. |

|

MD&A DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

|||

|

|

|||||

|

MD&A |

|||||

|

|

|||||

|

Investment Entities/Non-Investment Entities that Record Investments at Fair Value |

|

|

|

|

|

|

|

• |

We continue to see investment entities (IEs) and non-investment entities (NIEs) record investments at fair value, that do not provide sufficient qualitative and quantitative information about their investments. |

• |

Where a significant concentration exists in the issuer's investment portfolio, we expect the issuer to provide sufficient disclosure about the material investments in the portfolio to enable investors to evaluate the performance, operations and risks of the investee. |

|

|

|

|

|

• |

Information about a material investee is particularly important when the investee is private and disclosure is not otherwise available to investors. |

|

|

|

|

|

• |

At a minimum, we may request issuers to provide summary financial information about a material investee company in the MD&A including a discussion of those results. |

|

|

|

|

|

• |

If an IE's operations are dependent on a single investment, we may also have similar policy concerns and request standalone financial statements of the investee company as contemplated by National Policy 41-201 Income Trust and Other Indirect Offerings (NP 41-201). |

|

|

|

|

|

• |

We note that these issues may also be raised at the time of the issuer's prospectus. As such, we encourage issuers to pre-file and consult with staff in these circumstances. |

|

|

|

|||||

|

|

• |

Some IEs and NIEs with a portfolio of investments do not provide sufficient disaggregation of the investment portfolio in their annual and interim financial statements and MD&A. |

• |

The investment portfolio should be presented with sufficient disaggregation and transparency to allow an investor to understand the key characteristics of the portfolio composition including the associated risks and the drivers of any change in fair value. |

|

|

|

|

|

• |

Given the nature of an IE's business and the importance of understanding the investment portfolio, we believe this objective is best met by disclosing a statement of investment portfolio. |

|

|

|

|||||

|

|

|

|

Reference: Item 1.2, 1.4 of Form 51-102F1; Multilateral Staff Notice 51-349 Report on the Review of Investment Entities and Guide for Disclosure Improvements; IFRS 10 Consolidated Financial Statements. |

||

|

|

|||||

|

Non-GAAP financial measures (NGM) -- real estate industry |

|

|

|

|

|

|

|

• |

Several real estate issuers do not provide adequate transparency about the various adjustments made in arriving at NGMs, such as adjusted funds from operations (AFFO), particularly when the adjustments are management estimates. For example, adjustments for maintenance capital expenditures are often not explained in sufficient detail. |

• |

Issuers should ensure that all adjustments made as part of the reconciliation to the most directly comparable GAAP measure are consistent with the purpose of the NGM and sufficiently explain why and how the adjustment was determined. |

|

|

|

|

|

• |

If the issuer adjusts for maintenance capital expenditures using a reserve, the issuer should provide disclosure including the method used to determine the reserve, why that method was chosen and why it is appropriate. It should also disclose how the reserve compares to actual expenditures and why management's estimate is more relevant than the actual capital expenditures. |

|

|

|

|||||

|

|

• |

Some issuers with equity-accounted joint ventures include in the MD&A a full set of non-GAAP financial statements, creating a NGM for each financial statement line item. This effectively unwinds the equity method of accounting required by IFRS 11 (non-GAAP pro rata financial results). Some issuers also focus the discussion in the MD&A on these non-GAAP pro-rata financial results, with little to no discussion of the comparable GAAP results, thereby creating prominence concerns. |

• |

Issuers should ensure they identify the non-GAAP pro-rata financial results as NGMs, and label them in a way that distinguishes them from the comparable GAAP financial statement line items, in order to not be misleading. |

|

|

|

|

|

• |

Issuers should ensure the narrative discussion in the MD&A is not solely focused on the non-GAAP results. The GAAP discussion should be presented with equal or greater prominence. |

|

|

|

|||||

|

|

|

|

Reference: CSA Staff Notice 52-329, Distribution Disclosures and Non-GAAP Financial Measures in the Real Estate Industry; CSA Staff Notice 52-306(Revised) Non-GAAP Financial Measures (CSA SN 52-306); NP 41-201. |

||

|

|

|||||

|

Discussion of Operations --Disclosure of Capital Spending & Milestones |

|

|

|

|

|

|

|

• |

We continue to see issuers disclose or announce significant projects that are in the early stages of development, but fail to disclose sufficient information about the project. This deficiency is often observed with issuers who had a change of business and/or are in emerging industries. |

• |

In order to meet the requirements of the MD&A and provide investors with sufficient information, issuers should disclose the following: |

|

|

|

|

|

|

• |

Overall plan for the project and/or business: This should include a discussion of both current and long-term plans. The disclosure should be robust and include a discussion of the key milestones and what specific events need to occur for the issuer to meet those milestones. |

|

|

|

|

|

• |

Project Timeline: The expected timeline of the project must be clearly disclosed, including the issuer's progress compared to the timeline and the date at which it expects to begin generating revenues. |

|

|

|

|

|

• |

Budget: The estimated total expenditures related to the project, expenditures to date, expected timing of remaining expenditures and how the issuer anticipates funding the remaining expenditures. |

|

|

|

|

|

• |

Regulatory and licensing requirements: A discussion of license(s) and regulatory approval(s) the issuer must obtain. The discussion should include the anticipated timeline and expenditures associated with obtaining the license/regulatory approval and risks and associated impact if regulatory approval and licenses are not obtained. |

|

|

|

|

|

• |

Updates: The issuer must include an update on the status of the project in each MD&A, including any delays in the disclosed timeline and/or anticipated cost overruns. In addition, the MD&A must include a discussion of events and circumstances that occurred during the period that are reasonably likely to cause actual results to differ materially from material forward-looking information previously disclosed and the expected differences. |

|

|

|

|

Reference: Items 1.4(d), 1.6(a) and 1.7(a)(iii) of Form 51-102F1 and section 5.8 of NI 51-102. |

||

|

|

|||||

|

Related Party Transactions |

|

|

|

|

|

|

|

• |

We continue to see issuers who fail to provide the required disclosures pertaining to related party transactions. In particular, we note that many issuers do not identify the related person or entity (e.g. naming a director and/or officer), and do not discuss the business purpose of the transaction. |

• |

Issuers should identify the related person or entity. In addition to identifying the related party as the issuer's president, chairman, CEO or CFO, issuers should disclose the name of a director and/or an officer, where it is necessary, to specifically identify the individual. |

|

|

|

|

|

• |

Issuers should discuss the business purpose of the related party transaction. The discussion should be specific and include both qualitative and quantitative characteristics that are necessary for an understanding of the transaction's business purpose and economic substance. For example, we often see consulting fees paid to related parties without an appropriate discussion of the nature and purpose of those fees. |

|

|

|

|||||

|

|

• |

Some issuers disclose the recorded amount of the transaction but do not describe the measurement basis used. |

• |

Issuers are required to describe the measurement basis used for recording the amount of related party transactions. However, issuers should refrain from disclosing that related party transactions were recorded at the exchange amount, which is equivalent to fair value, unless such terms can be substantiated. |

|

|

|

|||||

|

|

|

|

Reference: Item 1.9 of Form 51-102F1. |

||

DISCLOSURE EXAMPLES

1. FORWARD-LOOKING INFORMATION

Forward-looking information (FLI) is disclosure regarding possible events, conditions or financial performance that is based on assumptions about future economic conditions and courses of action and includes future-oriented financial information with respect to prospective financial performance, financial position or cash flows that is presented as a forecast or a projection. Many issuers disclose FLI in news releases, MD&A, prospectus filings, marketing materials, investor presentations or on their website. This FLI disclosure is subject to the requirements of Parts 4A and 4B of NI 51-102.

Some issuers disclose FLI for a period beyond the issuer's next fiscal year end without providing reasonable and sufficient assumptions to support the FLI. Issuers must not disclose a financial outlook unless the financial outlook is based on assumptions that are reasonable in the circumstances. The FLI must be limited to a period for which the information in the financial outlook can be reasonably estimated. In many cases, that time period will not go beyond the end of the issuer's next fiscal year. Where FLI is presented for multiple years and is not sufficiently supported by reasonable qualitative and quantitative assumptions, we may ask issuers to limit the disclosure of FLI to a shorter period (for example, one or two years), for which reasonable support exists. For investors to assess whether the assumptions underlying the issuer's FLI are reasonable, the issuer should disclose those assumptions, both quantitatively and qualitatively. For example, an issuer projecting aggressive growth targets without the benefit of historical experience should be able to show (i) a reasonable basis for those targets, including the key drivers behind the projected growth with reference to specific plans and objectives that support the projected growth, and (ii) why management believes that each of the targets/FLI are reasonable.

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure -- FLI in MD&A

An excerpt from an issuer's MD&A:

Since starting operations in 2016, we have focused on growing the number of new stores, and have seen a substantial increase in the pace of store openings as of the most recent quarter (with 17 of the 20 new stores for fiscal 2017 opened in Q4 2017), leading to accelerated sales. New store openings, sales levels and net income for the last two fiscal years are shown below.

|

(in millions) |

Year ended Dec 31, 2017 |

Year ended Dec 31, 2016 |

|

|

||

|

# new stores/locations |

20 |

16 |

|

|

||

|

Sales |

15.0 |

12.6 |

|

|

||

|

Net Income |

($8.4) |

($15.5) |

Growth targets{1}

We will aggressively pursue growth opportunities, and anticipate that we will increase our store count by 70 new stores in 2018, to reach 106 stores by end of fiscal 2018. We also anticipate that we will reach 256 stores by end of fiscal 2019, and 400 stores by end of fiscal 2020. By rapidly growing our store base, we expect to grow sales to $500 million by the end of fiscal 2020. Management believes these growth targets are achievable, and is committed to pursuing new growth opportunities and partnerships.

- - - - - - - - - - - - - - - - - - - -

In the above example, the issuer presented FLI for the next three years which did not appear to be supported by reasonable assumptions given the historical performance of the issuer's business. The issuer also failed to disclose the assumptions used to develop this FLI or the related material risk factors.

A better example of disclosure might be as follows:

- - - - - - - - - - - - - - - - - - - -

Example of Robust Disclosure -- FLI in MD&A

Growth targets{1}

We will aggressively pursue growth opportunities, and anticipate that we will increase our store count by 70 new stores in 2018, to reach 106 stores by end of fiscal 2018, which corresponds to expected sales of $50 to 80 million for fiscal 2018. We are focussed on expanding our number of stores in a responsible manner and using a reasoned growth strategy, targeting major urban centres which meet pre-defined population and income criteria.

Management believes this growth target is achievable based on the assumptions and factors disclosed below, and is committed to pursuing new growth opportunities and partnerships.

Assumptions:

• we have agreements, leases and planned launch dates in place for 40 of the 70 new store openings planned for 2018;

• we have substantially negotiated the terms for 15 of the 70 new store openings planned for 2018, but launch dates and locations are still being finalized;

• we are in active discussions with major retail partners for 15 of the 70 new store openings planned for 2018;

• we assume stores are opened evenly throughout the year, and generate on average approximately $0.7-- $1.1 million in sales, depending on location.

- - - - - - - - - - - - - - - - - - - -

In the example above, the financial outlook has been limited to a period of one fiscal year for which the information in the outlook can reasonably be estimated. The assumptions supporting the outlook are clearly disclosed, and are reasonable given the issuer's limited operating history. The issuer has also disclosed (elsewhere in the MD&A) the material risk factors that could cause actual results to differ materially from the FLI disclosed.

2. NON-GAAP FINANCIAL MEASURES -- USEFULNESS

NGMs are frequently used by issuers to supplement and explain changes in financial performance, cash flows or financial condition. When used and disclosed appropriately, NGMs can provide investors with additional insight. However, we are continuing to see an increased prevalence of NGMs where the stated purpose and usefulness of the measure is unclear and fails to align with the nature of the adjustments that are being made in the reconciliation. Without clear disclosure accompanying NGMs and the adjustments being made, there is the potential that investors may be confused or even misled.

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure -- NGMs in MD&A

An excerpt from an issuer's MD&A:

Adjusted operating income{1} provides investors with an indication of operating results between periods. It has been reconciled to operating income (loss) being the most directly comparable measure calculated in accordance with IFRS.

|

|

2016 |

2015 |

|

|

||

|

Operating income (loss){2} |

60 |

(70) |

|

|

||

|

Add: |

|

|

|

|

||

|

Impairment expense |

10 |

40 |

|

|

||

|

Inventory write-down |

5 |

15 |

|

|

||

|

Depreciation |

<<16>> |

<<18>> |

|

|

||

|

Adjusted operating income{1} |

91 |

3 |

{1} Adjusted operating income does not have any standardized meaning as prescribed by IFRS and, therefore, is considered a non-GAAP financial measure and may not be comparable to similar measures presented by other issuers.

{2} Operating income (loss) is a line item presented on the issuer's financial statements.

- - - - - - - - - - - - - - - - - - - -

In the above example, the issuer has presented an operating performance measure however it has not clearly explained why this NGM provides useful information to investors. In addition, in calculating the NGM, the issuer made adjustments for impairment expense, inventory write-down and depreciation. Since the issuer has suggested the measure is a useful measure of operations, we believe these adjustments are inconsistent with that use since they are operational in nature.

When presenting NGMs, it may be misleading to present a NGM without an accompanying statement explaining why the NGM presents useful information to investors. This disclosure should be entity-specific and should clearly align with the nature and type of adjustments that are being included or excluded in the calculation of the NGM.

In addition, when multiple NGMs are disclosed for the same or similar purpose, issuers should carefully consider whether this will obscure the most directly comparable GAAP measure and if all NGMs are useful.

This discussion focused on one aspect of the NGM disclosure expectations. Issuers should ensure that they refer to all of the guidance set forth in CSA SN 52-306 in preparing their disclosure documents.

OTHER REGULATORY DISCLOSURE DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

OTHER REGULATORY |

||||

|

|

||||

|

Statement of Executive Compensation -- External Management Companies |

|

|

|

|

|

|

• |

Some issuers with executive management services provided by an external management company did not disclose the amounts paid to the named executive officers (NEOs) in the Summary Compensation Table (SCT). |

• |

If an external management company employs or retains any NEO(s) or directors, the issuer must disclose compensation paid by the external management company to the individual that is attributable to the services they provided to the issuer directly or indirectly. |

|

|

|

|

• |

It is not appropriate for an issuer to report a nil balance in the SCT for an NEO who is indirectly compensated by the issuer. |

|

|

|

|

• |

In line with the objectives of the Form, in disclosing all compensation paid directly or indirectly by the issuer to each NEO, we are of the view that the issuer should disclose the portion of the management fee (% or $) that the issuer believes relates to the compensation paid to the NEOs in instances where an issuer pays a management fee to an external management company that provides, among other things, NEO services to the issuer. |

|

|

||||

|

|

|

|

Reference: Items 1.3(1) and (4) of Form 51-102F6 Statement of Executive Compensation and items 1.3(1) and 2.2 of Form 51-102F6V Statement of Executive Compensation-- Venture Issuers. |

|

|

|

||||

|

Statement of Executive Compensation -- Filing Deadline |

|

|

|

|

|

|

• |

Some issuers do not file the disclosure of executive compensation within the required filing deadline. |

• |

Issuers must file the disclosure of executive compensation within 140 days after the end of their most recently completed financial year, or 180 days in the case of a venture issuer. |

|

|

|

|

• |

To comply with this filing deadline, issuers can either include the information in their information circular, their annual information form (AIF) or file a standalone "Statement of Executive Compensation." |

|

|

||||

|

|

|

|

Reference: Section 9.3.1 of NI 51-102. |

|

|

|

||||

|

Non-GAAP Financial Measures on Issuers' Websites |

|

|

|

|

|

|

• |

Many issuers disclose NGMs in their corporate presentations, investor fact sheets, news releases, or on social media and give excessive prominence to the NGMs. In some instances, the most directly comparable measure specified, defined or determined under the issuer's GAAP is not presented or discussed, or is disclosed in a less prominent location, most often when the GAAP measure is less favourable. |

• |

To avoid the potential to mislead investors when disclosing NGMs on websites, news releases or investor presentations, we remind issuers that the guidance in CSA SN 52-306 applies. |

|

|

|

|

• |

NGMs should not be the primary focus of the issuer's website content or the key messaging conveyed to investors. |

|

|

||||

|

|

|

|

Reference: CSA SN 52-306. |

|

|

|

||||

|

Social Media |

|

|

|

|

|

|

• |

Some issuers provide material information on social media sites before it is generally disclosed to all investors, which may constitute selective or early disclosure. |

• |

Issuers should have a robust social media governance policy that specifies, amongst other things, who is authorized to post what type of information on which social media websites. |

|

|

• |

Some issuers provide misleading or unbalanced information that may be inconsistent with information already posted on SEDAR or exceedingly promotional. |

• |

Issuers should be mindful of commonly observed pitfalls in social media disclosure, such as FLI that is selectively disclosed on social media websites alone. |

|

|

|

|

• |

In some cases, it may be difficult to provide balanced disclosure on social media due to length restrictions often inherent to social media posts. In these cases issuers should provide a link to additional information. |

|

|

||||

|

|

|

|

Reference: CSA Staff Notice 51-348 Staff's Review of Social Media Used by Reporting Issuers. |

|

|

|

||||

|

Climate change-related disclosure |

|

|

|

|

|

|

• |

Many issuers across a wide range of industries could be materially impacted by climate change. Many of these issuers either provide boilerplate disclosure or fail to provide disclosures of climate change-related risks and opportunities. |

• |

The AIF must include disclosure of risk factors relating to the issuer and its business that would be likely to influence an investor's decision to purchase the issuer's securities. |

|

|

|

|

• |

When assessing the materiality of climate change-related risks and impacts, issuers should consider a wide range of risks including physical (acute/chronic), regulatory, reputational and business model risks. |

|

|

|

|

• |

In addition to disclosure in the AIF, the MD&A would also require a discussion and analysis of its operations, including commitments, events, risks or uncertainties that the issuer reasonably believes will materially affect its future performance. |

|

|

||||

|

|

• |

Many issuers disclose general climate risks but these risks are not sufficiently specific to the issuer and its operations or fail to disclose the potential impact resulting from climate change. |

• |

In order to provide useful information to investors, material climate change-related risks should provide specificity and additional quantitative discussion (e.g. the financial impact). |

|

|

|

|

• |

The AIF should also include a description of the environmental policies fundamental to the issuer's operations and the steps taken to implement them. When describing the policies, there should be sufficient information provided necessary for an understanding of the impact the policies may have on the operations. |

|

|

||||

|

|

|

|

Reference: Item 5.2 of Form 51-102F2, Annual Information Form, Item 1.4(g) of Form 51-102F1 and CSA Staff Notice 51-333 Environmental Reporting Guidance. |

|

|

|

||||

|

Disclosure of Material Relationships |

|

|

|

|

|

|

• |

Some issuers that disclosed significant transactions with a party with whom there was a familial or similar close relationship failed to disclose the relationship. |

• |

Securities legislation in Canada generally prohibits omitting material facts or statements that are in a material respect necessary to prevent other statements made from being false or misleading in the circumstances in which they are made. |

|

|

|

|

• |

When an issuer discloses a significant transaction and that transaction is with a party with whom the issuer or its principals has a familial or similar close relationship, the omission of that fact may be considered misleading or a misrepresentation. |

|

|

|

|

• |

In these circumstances we may ask the issuer to provide qualitative and quantitative disclosure sufficient for an investor to understand the relationship and terms of the transaction. |

|

|

||||

|

|

|

|

Reference: General Requirements in Securities Legislation. |

|

|

|

||||

|

Change of auditor reporting package |

|

|

|

|

|

|

• |

Some issuers file a letter from the predecessor auditor that is not in the required form (as part of their change of auditor reporting packages). In addition, the change in auditor reporting package is not filed within the required filing deadline. |

• |

Issuers should ensure they file the letter from the predecessor auditor in the required form, rather than a resignation letter or other communication intended for the issuer only. We remind issuers that incorrect SEDAR filings may remain public. |

|

|

|

|

• |

The issuer must file a change of auditor reporting package that includes the letter from the former auditor within 14 days after the date of auditor termination or resignation. If there is a delay between the termination or resignation of the former auditor and the appointment of the successor auditor, the issuer may have to file a separate change of auditor reporting package that includes the letter from the successor auditors upon auditor appointment. |

|

|

||||

|

|

• |

It is sometimes unclear from the predecessor or successor auditor's letter whether the auditor agrees or disagrees with the issuer's statements relating to a reportable event, as defined in NI 51-102. |

• |

If there is a reportable event, the issuer must file a news release describing the information in the change of auditor reporting package. |

|

|

|

|

• |

An auditor must report to the regulator or in Quebec, the securities regulatory authority, an issuer's non-compliance with the change of auditor reporting requirements within three days of the issuer's required filing date. |

|

|

|

|

• |

When it is unclear from the auditor's letter whether they agree with the issuer's statements relating to a reportable event, we generally require the issuer to request and file a new letter from the auditor. |

|

|

||||

|

|

|

|

Reference: Section 4.11 of NI 51-102. |

|

DISCUSSION OF OTHER REGULATORY DEFICIENCIES

1. MINERAL PROJECT DISCLOSURE

National Instrument 43-101 Standards of Disclosure for Mineral Projects (NI 43-101) governs public disclosure of scientific and technical information about issuer's mining and mineral exploration projects including written documents, websites, and oral statements. Issuers must base their scientific and technical disclosure on information provided by a "qualified person" (QP), as defined in section 1.1 of NI 43-101. NI 43-101 also requires issuers file a "technical report", in a prescribed format, Form 43-101F1 Technical Report (Technical Report), for significant corporate or mineral project milestones. The purpose of the Technical Report is to support disclosure of the issuer's exploration, development, and production activities with additional information to assist the public and analysts in making investment decisions and recommendations. In some circumstances, QPs authoring the Technical Report must be independent of the issuer and the mineral property.

During the course of our reviews over the past two fiscal years, we have observed some of the following deficiencies. Please note that this is not an exhaustive list.

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

MINERAL PROJECTS |

||||

|

|

||||

|

Technical Report Content |

|

|

|

|

|

|

• |

Some Technical Reports do not include adequate disclosure of important criteria the QP used to determine that the mineral resource has demonstrated reasonable prospects for eventual economic extraction. Specific examples include omission of the proposed mining method(s), metallurgical recovery factors, selected metal price(s) including justification for the selection, and the cut-off grade and how it was determined. |

• |

The Technical Report requires sufficient discussion of the key assumptions, parameters, and methods used to estimate the mineral resource for a reasonably informed reader to understand the basis for the mineral resource estimate and how it was generated. Absent these disclosures, it may be unclear if the mineral resource meets the threshold required by the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Definition Standards for mineral resources. |

|

|

• |

Authors of some Technical Reports improperly use the provision to rely on other experts for legal, political, environmental, and tax matters. Also, authors of some Technical Reports disclose reliances on other QP's for scientific and technical information. |

• |

Item 3 of the Technical Report, Reliance on Other Experts, allows a limited disclaimer of responsibility for non-technical information concerning legal, political, environmental, or tax matters relevant to the mineral project by identifying the information source and the Technical Report section to which the disclaimer applies. |

|

|

||||

|

|

|

|

• |

A QP can supervise another QP's work, but the author of a Technical Report must accept responsibility for the disclosure. They cannot disclose that they are relying on another QP when they have accepted responsibility for that item in the Technical Report. |

|

|

||||

|

|

• |

Some Technical Reports do not adequately describe specific procedures the QP undertook in verifying the data or provide the QP's opinion on the adequacy of the data used in the Technical Report. |

• |

"Data verification" is a defined term and is not merely ensuring that assay results have been accurately transferred, for example, into a mineral resource estimation database. It encompasses all efforts by the QP to verify that the database is fit for purpose. |

|

|

|

|

• |

A QP is required to disclose the steps they have taken to verify the data used in the Technical Report and the QP cannot rely on data verification completed by other QP's in previous reports on behalf of other issuers. |

|

|

||||

|

|

|

|

Reference: Form 43-101F1, specifically Items 14 (a), Item 3, and Item 12; paragraph 6.4(1)(a), and section 1.1 of NI 43-101. |

|

|

|

||||

|

Preliminary Economic Assessments |

|

|

|

|

|

|

• |

Some disclosure of the results of a preliminary economic assessment (PEA) after mineral reserves have been determined on a mineral property can be potentially misleading if the results have the effect of adding, combining, or integrating the PEA outcomes with the economic analysis, cash flows, production schedules, or mine life based on a pre-feasibility, feasibility study, or life of mine plan. |

• |

"Preliminary economic assessment" is a defined term that means a study, other than a pre-feasibility or feasibility study that includes an economic analysis of the potential viability of mineral resources. |

|

|

|

|

• |

An issuer must not disclose an economic analysis which includes inferred mineral resources. Despite this restriction, section 2.3(3) of NI 43-101 allows for such disclosure under certain requirements and prescribed cautionary language. Nevertheless, if results of a PEA are disclosed after mineral reserves on the same property, the PEA results must be reported as a separate analysis (i.e. Item 24 of the Technical Report) that is distinct from the results of the pre-feasibility or feasibility study used to demonstrate economic viability and support mineral reserves. |

|

|

||||

|

|

|

|

Reference: Sections 1.1, paragraph 2.3 (1) (b), section 2.3(3) of NI 43-101 and Item 24 of Form 43-101F1. |

|

|

|

||||

|

Disclosure of Historical Estimates |

|

|

|

|

|

|

• |

Many issuers disclose historical estimates on their websites, in corporate presentations and other marketing documents but fail to provide information related to the estimate's original source and date, fail to identify the estimate as historic and omit the required cautionary statements. In some cases, the historical estimate is used in a way that treats the estimate as a current mineral resource or reserve estimate. |

• |

"Historical estimate" is a defined term, referring to an unverified estimate prepared before the issuer obtained an interest in the property. |

|

|

|

|

• |

Section 2.4 of NI 43-101 provides disclosure requirements and prescribed cautionary language related to historical estimates. |

|

|

||||

|

|

|

|

Reference: Sections 1.1 and 2.4 of NI 43-101. |

|

{1} Certain disclosures, including the number of new stores and store count as well as future sales levels, represent forward-looking information within the meaning of securities legislation. Readers are urged to consider the risks, uncertainties and assumptions carefully in evaluating the forward-looking information and are cautioned not to place undue reliance on such information. See "Forward-looking Statements" in this MD&A.

{1} Certain disclosures, including the number of new stores and store count as well as future sales levels, represent forward-looking information within the meaning of securities legislation. Readers are urged to consider the risks, uncertainties and assumptions carefully in evaluating the forward-looking information and are cautioned not to place undue reliance on such information. See "Forward-looking Statements" in this MD&A as well as "Material Risk Factors -- FLI".

APPENDIX B

CATEGORIES OF OUTCOMES

Referred to Enforcement/Cease-Traded/Default List

If the issuer has substantive CD deficiencies, we may add the issuer to our default list, issue a cease trade order and/or refer the issuer to enforcement.

Refiling

The issuer must amend and refile certain CD documents or must file a previously unfiled document.

Prospective Changes

The issuer is informed that certain changes or enhancements are required in its next filing as a result of deficiencies identified.

Education and Awareness

The issuer receives a proactive letter alerting it to certain disclosure enhancements that should be considered in its next filing or when staff of local jurisdictions publish staff notices and reports on a variety of continuous disclosure subject matters reflecting best practices and expectations.

No Action Required

The issuer does not need to make any changes or additional filings. The issuer could have been selected in order to monitor overall quality disclosure of a specific topic, observe trends and conduct research.

Questions -- Please refer your questions to any of the following: