Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

Notice and Request for Comment – Application for Recognition as a Clearing Agency – LCH.Clearnet Limited

A. Background

On March 1, 2011, subsection 21.2(0.1) of the Securities Act (Ontario) (OSA) came into force which prohibits clearing agencies from carrying on business in Ontario unless they are recognized as a clearing agency or are exempt from the requirement to be recognized by order of the Ontario Securities Commission (Commission).

LCH.Clearnet Limited (LCH) has applied (the Application) to the Commission for recognition as a clearing agency pursuant to subsection 21.2(0.1) of the OSA.

LCH is a recognized clearing house in the United Kingdom (U.K.) under the U.K.'s Financial Services and Markets Act 2000 and is regulated by the U.K. Financial Services Authority (FSA). Under the U.K. regulatory reform, which will be implemented in 2013, the FSA's regulatory oversight of systemically important financial market infrastructures such as LCH will be transferred to the Bank of England (FSA and Bank of England collectively referred to as U.K. Authorities).

LCH clears a broad range of assets classes including: securities, exchange traded derivatives, freight, interest rate swaps and euro and sterling denominated bonds and repo transactions. LCH is currently operating in Ontario as a clearing agency pursuant to an interim exemption order which exempts LCH from the requirement to be recognized as a clearing agency pursuant to subsection 21.2(0.1) of the OSA.

In assessing the Application, staff followed the process set out in OSC Staff Notice 24-702 -- Regulatory Approach to Recognition and Exemption from Recognition of Clearing Agencies (OSC Staff Notice 24-702).

B. Draft Order

In the Application, LCH has addressed the applicable criteria for recognition as a clearing agency. Subject to comments received, staff will recommend that the Commission grant a recognition order with terms and conditions to LCH based on the proposed draft recognition order (Draft Order) that is attached as Appendix A to the Application.

The terms and conditions in the Draft Order have been tailored to reflect the Commission's intention to focus its oversight of LCH on key matters that would have a significant impact on Ontario capital markets and rely on the U.K. Authorities for the day to day oversight of LCH.

The Draft Order requires LCH to comply with the following terms and conditions relating to:

1. Regulation and Ownership of LCH

2. Access

3. Rules and Rulemaking

4. Risk Controls

5. Crisis Management

6. Systems and Technology

7. Compliance

8. Information Sharing and Regulatory Cooperation

9. Submission to Jurisdiction and Agent for Service

10. Filing and Reporting Obligations

C. Comment Process

The Commission is publishing for public comment the Application and Draft Order. We are seeking comment on all aspects of the Application and Draft Order.

You are asked to provide your comments in writing and delivered on or before March 18, 2013, addressed to:

The Secretary

Ontario Securities Commission

20 Queen Street West

19th Floor, Box 55

Toronto, Ontario M5H 3S8

Fax: 416-593-2318

Email: [email protected]

We request that you also submit an electronic copy of your submission. The confidentiality of submissions cannot be maintained as a summary of written comments received during the comment period will be published.

Questions may be referred to:

Emily Sutlic

Senior Legal Counsel, Market Regulation

Tel: 416-593-2362

Aaron Ferguson

Clearing Specialist, Market Regulation

Tel.: 416-593-3673

APPLICATION FOR RECOGNITION AS A CLEARING AGENCY

PURSUANT TO SUBSECTION 21.2(0.1) OF THE SECURITIES ACT (ONTARIO)

LCH.CLEARNET LIMITED

January 24, 2013

LCH.Clearnet Limited ("LCH") is applying to the Ontario Securities Commission (the "OSC") for an order, pursuant to subsection 21.2(0.1) of the Securities Act (Ontario) (the "OSA"), recognizing LCH as a clearing agency pursuant to subsection 21.2(0.1) of the OSA.

LCH is currently carrying on business in Ontario by providing four services to Ontario-resident clearing members ("Clearing Members"), namely SwapClear, RepoClear, EnClear and LCH Nodal service, pursuant to an interim order granted by the OSC dated March 1, 2011, as subsequently varied and restated by the OSC on May 17, 2011, August 19, 2011 and August 28, 2012, which exempted LCH from the requirement to be recognized as a clearing agency.

PART I -- BACKGROUND

1. Legal and Ownership Structure of LCH

LCH is a clearing house incorporated under the laws of England and Wales. LCH operates as a central counterparty ("CCP") clearing house and receives most of its revenue from treasury income and thereafter clearing fees charged to its Clearing Members.

As of January 24, 2013 and the date of this application, LCH.Clearnet Group Ltd. ("LCH Group"), the parent holding company of LCH, is owned 77.5 percent by users (i.e., Clearing Members) and 22.5 percent by exchanges. As at December 31, 2012, there are no shareholders of LCH Group who hold 10% or more of LCH Group's issued and outstanding shares. On December 14, 2012, the Office of Fair Trading ("OFT") in the United Kingdom ("U.K.") announced that the proposed acquisition by the London Stock Exchange Group Plc of a majority stake in LCH was cleared unconditionally.

2. Regulatory Status

LCH Group, which is incorporated in the U.K., is regulated as a Compagnie financière by the Autorité de Contrôle Prudentiel (France).

LCH has approximately 130 Clearing Members representing one of the largest memberships among derivatives clearing organisations worldwide. The Clearing Members consist of banks, securities houses/investment banks, commodity brokers and traders and, to a very limited extent, industrial companies.

LCH is a Recognised Clearing House ("RCH") in the U.K. under the U.K.'s Financial Services and Markets Act 2000 ("FSMA") and, as such, is approved by the U.K. Financial Services Authority ("FSA") to clear a broad range of asset classes including: securities, exchange traded derivatives, energy, freight, interest rate swaps ("IRS") and euro and sterling denominated bonds and repurchase transactions. Proposed legislation was introduced into the U.K. Parliament on January 27, 2012 that will fundamentally reform the structure of financial services regulation in the U.K. Under the new framework, which will be implemented in 2013, the FSA's regulatory and oversight responsibilities of systemically important financial market infrastructures will be transferred to the Bank of England (the FSA and the Bank of England are hereinafter referred to collectively as the "U.K. Authorities"). As part of their regulatory oversight of LCH, the U.K. Authorities review, assess and enforce the on-going compliance by LCH with the requirements set out in FSMA including financial resources, the financial and operational requirements for Clearing Members, systems and controls, rule-making, and LCH's practices and procedures. LCH is required to provide to the U.K. Authorities, on request, access to all records and to cooperate with other regulatory authorities, including making arrangements for information-sharing.

Currently, LCH provides clearing services for the following U.K. "Recognised Investment Exchanges" and "Recognised Overseas Investment Exchanges" (as those terms are defined under the FSMA): NYSE Liffe US ("LIFFE") and the London Metal Exchange Limited, as well as for the London Stock Exchange ("LSE") and in Switzerland, the SIX Swiss Exchange AG ("SIX Exchange").

LCH clears a broad range of asset classes including securities, exchange traded derivatives, commodities, energy, freight, IRS, credit default swaps and euro and sterling denominated bonds and repurchase transactions, and works closely with market participants and exchanges to identify and develop clearing services for new asset classes. The exchange-traded futures and options on futures relate to underlyings in short-term interest rates (Euro, Sterling, Swiss Franc); government bonds (U.K. Gilts and Japanese Government Bonds); medium and long-term swap rates (Euro), equity indices (U.K.-related FTSE indices and FTSE and MSCI pan-European indices); and individual stocks (British, Dutch, French, German, Italian, Spanish and U.S. companies). In addition, LCH clears cash-settled over-the-counter ("OTC") freight forwards and options, OTC emissions contracts, iron and fertilizer swaps and clears cash-settled electricity futures for participants of the Nodal Exchange.

The following is an overview of (i) the requirements imposed by the FSA in the U.K. and (ii) how the oversight of LCH by the FSA ensures ongoing compliance with the criteria in Appendix A to OSC Staff Notice 24-702 Regulatory Approach to Recognition and Exemption from Recognition of Clearing Agencies ("Staff Notice 24-702"):

(a) Requirements imposed by the FSA on LCH

The following is a list of the main legislation relevant to RCHs in the U.K.{1}:

• The main primary legislation is FSMA, Part XVIII. (Recognised Investment Exchanges and Clearing Houses), which can be found here: http://www.legislation.gov.uk/ukpga/2000/8/contents.

• This is supplemented by FSMA (Recognition Requirements for Investment Exchanges and Clearing Houses) Regulations 2001 (SI 2001/995): http://www.legislation.gov.uk/uksi/2001/995/contents/made.

• In addition, there is the U.K. Investment Exchanges and Clearing Houses Act 2006: http://www.legislation.gov.uk/ukpga/2006/55/enacted.

• The main source of secondary legislation is the rules and guidance contained in the FSA Handbook 'Recognised Investment Exchanges and Recognised Clearing Houses' ("REC") which can be found here: http://fsahandbook.info/FSA/html/handbook/REC.

(b) Description of how the oversight of LCH by the FSA ensures ongoing compliance with the criteria in Staff Notice 24-702

'Close and continuous supervision'

LCH maintains a good relationship with the FSA overall. There are regular meetings between the FSA and LCH's Compliance and Regulation department, and also a significant schedule of meetings with senior management and key individuals within the business. The FSA has implemented a "close and continuous" regulatory supervision relationship with LCH through a number of formal and ad hoc meetings and other communications at many levels and of many frequencies.

The "close and continuous" model of supervision ensures that the relevant regulatory obligations continue to be met and would identify if activities at LCH pose any risks to the FSA's statutory objectives, including maintaining market confidence. This enables the FSA to have a broad picture of LCH's activities and ability to meet the recognition requirements (REC 2) (which include but are not limited to: the maintenance of sufficient financial resources to cover all aspects of risk, including Clearing Member default, fitness and propriety). LCH must also respect 'notification requirements' (REC 3) (covering inter alia: financial information, changes to the LCH Rulebook, complaints and disciplinary proceedings, major operational issues, default events).

The supervisory relationship consists of on-going communication (typically between the Regulatory Compliance Officer and the FSA Supervisor, on an almost daily basis), as well as a more structured series of meetings between the FSA and key individuals of LCH. The frequency and nature of these meetings may vary in accordance with the risk profile of LCH.

The FSA recognises that LCH is likely to develop and adapt their businesses in response to customer demand and new market opportunities. The FSA expects LCH to take its own steps to assure itself that it will continue to satisfy the recognition requirements, and other obligations in or under FSMA when considering any changes to its business or operations. However, the FSA also expects LCH to keep it informed of all significant developments and of progress with its plans and operational initiatives, and to provide it with appropriate assurance that the recognition requirements will continue to be satisfied.

Risk based supervision

The FSA requires information to support their risk based approach to the supervision of all regulated entities. Risk based supervision is intended to ensure that the allocation of supervisory resources and the supervisory process are compatible with the regulatory objectives and the FSA's general duties under FSMA. The central element of the process of risk based supervision is an assessment by the FSA (a risk assessment) of the main risks to its supervisory objectives posed by each regulated entity. The FSA will conduct a periodic risk assessment of LCH. This assessment will take into account relevant considerations including the special position of recognised bodies under FSMA, the nature of the U.K. recognised body's members, the position of other users of its facilities and the business environment more generally.

The risk assessment will guide the FSA's supervisory focus. The FSA initially reviews its risk assessment with the staff of LCH to ensure factual accuracy and a shared understanding of the key issues, and may discuss the results of the risk assessment with key individuals of LCH. It then sends the assessment and an action plan relating to work that it considers appropriate for LCH to undertake to LCH's Board of Directors for discussion and response.

Further information on the risk based supervision is available in chapter 4 of the REC, in particular:

4.2 The supervisory relationship with U.K. recognised bodies.

4.3 Risk assessments for U.K. recognised bodies.

4.4 Complaints.

4.5 FSA supervision of action by U.K. recognised bodies under their default rules.

4.6 The section 296 power to give directions.

4.7 The section 297 power to revoke recognition.

4.8 The section 298 procedure.

LCH expects that the FSA oversight regime described above will remain largely the same under the new framework headed by the Bank of England. The Bank of England has published its supervisory framework.{2}

LCH is also a designated clearing organization ("DCO") within the meaning of that term under the United States ("U.S.") Commodity Exchange Act. As a DCO, LCH is subject to regulatory supervision by the U.S. Commodity Futures Trading Commission ("CFTC"), a U.S. federal regulatory agency.

LCH's DCO registration allows it, in principle, to clear for any Exempt Contract Market in the U.S., which has to this point covered IRS and Commodity and Energy derivatives. In addition, it allows LCH to clear broad-based Credit Derivative Indices. LCH's relationship with the CFTC was more one of oversight; however, with the introduction of the Dodd Frank Wall Street Reform and Consumer Protection Act, the relationship is more in line with LCH's relationship with the FSA. In 2011 and 2012, the CFTC conducted a due diligence visit to LCH. The CFTC's findings and reports are outstanding. It should be noted that LCH has applied for a full DCO registration to encompass all of its services. The registration application is in progress.

3. CLEARING ACTIVITIES IN ONTARIO

LCH does not have any office or maintain any other physical installations in Ontario or any other Canadian province or territory. LCH does not currently have any plans to open such an office or to establish any such physical installations in Ontario or elsewhere in Canada.

However, LCH is currently offering the following four services to Ontario-resident Clearing Members: RepoClear (certain fixed income products), SwapClear (IRS), EnClear (OTC emissions contracts) and LCH Nodal. LCH currently has five Clearing Members who qualify as "Canadian financial institutions" (within the meaning of that term in subsection 1.1(3) of National Instrument 14-101 Definitions and that have a head office or principal place of business in Ontario. LCH currently does not offer client clearing services to its Ontario-resident clients.

Each of these services is described below. LCH acts as the CCP in all instances.

3.1 REPOCLEAR

RepoClear is a market leading service clearing cash bond and repurchase trades across a number of European markets and is the second largest clearer of fixed income and repurchase products in the world. LCH clears approximately 74% (based on outstanding balance as December 2011) of the cleared European government bond repurchase market. Q3 2012 volumes were down by 11% on 2011 with €36 trillion of nominal values cleared (approximately CAD $57 trillion).

Established in partnership with leading market makers in 1999, it was the first multi market centralized clearing and netting facility for the European government repurchase and cash bond (outright) markets. 2011 monthly volumes average €13 trillion and RepoClear clears cash bond and repurchase trades on the following securities: Austrian, Belgian, Dutch, German, Irish, Finnish, Portugese and U.K. government bonds, German Jumbo Pfandbriefe and Supranationals, Agency and Sovereign. RepoClear accepts the following types of specific bond repurchase trades: classic fixed rate repurchases with first leg settlement on a same day and forward start basis with a term not greater than one year.

Recently, LCH launched two new innovative repurchase products called Sterling GC and €GC. Both products are based on the clearing, netting and settlement of cash-led repurchase trades in standardized ranges of liquid bond baskets. The baskets are determined either by bond type or credit rating of issuer and trade anonymously on electronic trading platforms or bilaterally via voice brokers or inter-office. This enables users to benefit from the efficiencies of a standard process for addressing funding needs, the ability to move collateral quickly easily and with minimal manual intervention and from the cost benefits of maximized settlement netting opportunities.

RepoClear is a multilateral netting facility for European government and non-government debt repurchases and cash bond markets. LCH acts as CCP to wholesale market participants.

In clearing a trade, LCH becomes counterparty to, and responsible for, the corresponding trade obligations arising from the original bilaterally negotiated trade. This principle is known as novation or registration. LCH does not hold positions for its own account within the RepoClear service.

The fact that LCH becomes counterparty to each trade maximizes Clearing Members' balance sheet netting potential, frees up Clearing Members' credit lines and reduces Clearing Members' operational risk and operational costs.

LCH holds the trades within its clearing database. When settlement is due, LCH nets down all movements for a Clearing Member, in each issue, within the same depository. This results in a reduction in actual settlements that are to be made. Clearing Members can select the depository used for their settlements for each separate issue country (one depository per market, though two can be used for €GC).

In order to protect itself from market and credit risks, LCH calculates exposures and calls margin. All RepoClear positions are marked-to-market daily. LCH collects and pays variation margin amounts daily in cash. Delivery margin is called in order to cover LCH's settlement risk. Initial margin is taken from both sides to a trade to provide security against future price moves. Calculation of initial margin is conducted on a portfolio basis and cover may be provided in cash, bank guarantees or securities. RepoClear nets and shapes all delivery obligations due for settlement the next business day. In some markets, the settlement netting may result in several delivery obligations for LCH due to cross-border settlement or maximum delivery size requirements. Clearing Members are then notified of their own specific delivery obligations.

If there are no securities delivery obligations all net cash delivery obligations are aggregated into one amount per market, which is paid through the appropriate depository. Margin obligations from all exchange-traded and bilaterally-traded contracts, together with any coupon payments, are netted into a single payment per currency per day and paid through the Protected Payments System ("PPS").

In March 2012, LCH announced it would be restructuring the RepoClear Default Fund and associated Default Management process.

The restructuring of the segregation of the RepoClear element of the existing mutual Default Fund into a stand-alone Default Fund was implemented in August 2012.

The second phase of the restructuring plan (due Q1 2013) proposes to further enhance the stand-alone RepoClear Default Fund to incorporate the Service Close (i.e., "living will") provisions and implement the Default Management process and structure of the Default Management Group ("DMG"), a revolving group of senior rate traders from the major IRS market makers that are seconded to LCH in the event of default.

3.2 SwapClear

The SwapClear facility is a facility for the clearing and settlement of a range of OTC interest rate derivatives. SwapClear was launched in 1999 and has expanded over time to now offer clearing and settlement services in respect of a range of OTC interest rate swap transactions.

LCH clears OTC IRS through its SwapClear facility, and anticipates clearing an expanded list of interest rate swap products and OTC derivatives. In addition, LCH clears European government bonds and repurchase agreements relative to those instruments, through its RepoClear facility. Transactions cleared through SwapClear and RepoClear are executed by Clearing Members on a bilateral basis, either inter-office, or through brokers, or on automated trading systems recognized by LCH.

Under the LCH Regulations, there are three recognized participants in SwapClear including a SwapClear Clearing Member ("SCM") a SwapClear Futures Commission Merchant ("FCM") and a SwapClear Dealer ("SD"). . An applicant must enter into a Clearing Membership Agreement with LCH before it can become a Clearing Member. The Clearing Membership Agreement contains an acknowledgement that the applicant accepts the rules and procedures of the LCH Rulebook, which contains the operating rules of LCH.

A SCM or FCM may clear trades originally transacted by itself (including those in the name of one of its branches, being within the same legal entity), and may also clear trades transacted by an SD with whom it has entered into a SD Clearing Agreement.

LCH acts as central clearing counterparty to OTC swap transactions registered with it by a SCM, FCM or by a SD. On registration of a transaction with SwapClear, the counterparty's transactions, which can be entered by either a SCM, FCM or SD, are novated to the relevant Central Counterparty.

SwapClear's fundamental purpose is to ensure the financial performance of all interest rate derivatives cleared via our service, should a Clearing Member default. In a default, LCH becomes responsible for the cleared positions of the defaulted Clearing Member and must (a) make good on any losses borne by the defaulter and (b) hedge and transfer the defaulter's open positions. In order to manage outstanding notional volumes in excess of USD $300 trillion, we have designed safeguards to protect our clients, Clearing Members and the stability of the global financial system.

SwapClear calculates the potential loss it may have to cover in the event of a default of a Clearing Member. To cover this loss an amount, known as "initial margin," must be provided to SwapClear by both Clearing Members. It is held by SwapClear and only utilized in the event of the Clearing Member's default.

Initial margin is designed to cover normal market losses that would have occurred on the portfolio within recent history and is set at the portfolio's observed worst-case five-day loss (seven days for clients of Clearing Members) over the last five years. Additionally, members' portfolios are stress tested for extreme but plausible market events and the difference between this potential loss and that coverend by IM is deposited by members in the SwapClear default fund.

Also to ensure risks are maintained appropriately to the financial status of each Clearing Member and its portfolio, SwapClear uses a framework where initial margin multipliers are usedif the Clearing Member breaches predefined risk and concentration levels.

The value of individual interest rate swap contracts changes throughout each trading day. SwapClear conducts a valuation of each individual contract (known as "marking to market") and collects losses from Clearing Members on the losing side of the trade to pay gains to Clearing Members on the gaining side of the trade. A Clearing Member's daily gain or loss is known as the Clearing Member's "variation margin."

By collecting variation margin, SwapClear ensures that Clearing Members are current on all obligations and avoids default scenarios where Clearing Member losses have accumulated over a prolonged period of time.

Many of our valuation principles have become the market standard for cleared OTC IRS, including overnight index swap (OIS) discounting and price aligned interest.

In the event of a default of a Clearing Member, LCH must hedge and transfer the defaulter's positions while meeting the financial obligations of the defaulter. At inception, SwapClear's Default Management process was revolutionary for centrally cleared products. After the successful closeout of Lehman Brothers' OTC IRS portfolio in 2008, the process has become the market standard for OTC IRS.

To meet the financial obligations of the defaulter. To do so, SwapClear employs a robust default waterfall designed to ensure the performance of cleared IRS in the worst of scenarios.

In August 2012, LCH announced it would be restructuring the Default Fund. Through a membership Restrike project, LCH created a separate SwapClear Default Fund, amended the SwapClear Default Management process and made changes to the SwapClear Membership criteria.

The segregated SwapClear Default Fund is sized based on the sum of the two largest Clearing Members' stress test losses over Initial Margin using a carefully selected set of extreme but plausible stress test scenarios, looking back at each Clearing Member's positions over the previous 60 business days.

Full details of the LCH SwapClear Default Fund are set out under section 6.1 of this application. As detailed above in section 3, LCH currently has five Ontario domiciled Clearing Members.

3.3 EnClear -- OTC Emissions Clearing

The EnClear service provides independent multilateral netting and clearing for the global OTC spot and forward carbon allowance markets (e.g., OTC forward freight agreements and OTC emission contracts) that provide a risk management and delivery solution. The service clears contracts on EU Allowances ("EUA"{3}) and Certified Emissions Reductions ("CER"{4}).

LCH clears the following contracts:

• OTC Emissions -- EUAs and CERs;

• OTC Emissions -- EUA Spot and CER Spot;

• OTC Emissions -- EUA Options and CER Options.

Both EUAs and CERs are physically settled contracts for the forward delivery, and they trade in sizes of one lot of 1000 EUAs / CERs, in Euros.

EUA Spot contracts are physically settled day ahead contracts for the delivery of EUA Allowances in accordance with the terms of Directive 1003/87/EC. Contracts are traded in sizes of one lot, being equal to 1000 EUA units. A unit consists of the right to emit one tonne of CO2 equivalent.

CERs are physically settled day ahead spot contracts for the delivery of certified emissions reductions issued pursuant to Article 12 of the Kyoto Protocol that may be used for determining compliance with emissions limitation commitments in accordance with the EU Emissions Trading Scheme. Excluding allowances generated by hydroelectric projects with a generating capacity exceeding 20MW. Contracts are traded in one lot sizes.

LCH's focus on OTC transaction flow allows us to clear EUA's and CER's, previously concluded by bilateral parties through OTC brokers or directly, thereby minimizing counterparty risk for emissions traders.

LCH has seen continued growth in this area, due to the appetite for cost effective and operationally efficient OTC clearing services for emissions. In addition, five new Clearing Members joined the service in 2010, facilitating access and giving market participants the choice of 14 Clearing Members.

All transactions eligible for clearing are entered into Clearway, a registration system approved Brokers or, in the case of directly negotiated trades, by the selling participants' Clearing Member.

On receipt and confirmation of eligible transactions the trades pass to the Extensible Clearing System ("ECS") system, where trades are governed under the rules of the LCH Rulebook.

Daily and final settlement of emissions contracts is based on prices provided by London Energy Brokers' Association (LEBA). On expiry all net positions are physically delivered.

All existing LCH Clearing Members are eligible to clear emissions contracts subject to approval.{5}

3.4 Nodal Clearing

The LCH Nodal service clears cash-settled OTC power and natural gas futures for participants of the Nodal Exchange.

Nodal Exchange is an independent electronic commodities exchange dedicated to offering locational forward trading products and services to participants in the organized North American power markets. Locational trading is used for the management of capacity constraint risk.

Nodal Exchange is a commodities exchange, covering the trading of on-peak and off-peak power contracts at significant hubs, zones and nodes in the organized North American electric markets. Currently, this is available in six market locations -- PJM Interconnection (PJM), New York Independent System Operator (NYISO), Independent System Operator of New England (ISO-NE), Midwest Independent System Operator (MISO), Electric Reliability Council of Texas (ERCOT) and California Independent System Operator (CAISO) -- and plans to expand to cover additional geographies.

The LCH Nodal service provides independent multilateral netting and clearing for the global OTC power and gas markets. The basic premise of the LCH Nodal service OTC power and gas clearing solution is to give the end user the option to use a screen-traded nodal auction market or a broker-matched trade submission facility to capitalize on a single pool of open interest.

The cleared OTC futures offered by the LCH Nodal service are cash-settled OTC futures contracts only and are not physically delivered. The LCH Nodal service does not currently cover options contracts and there is no provision for allocation or give-ups.

The LCH Nodal service allows for OTC futures contracts that have been concluded either bilaterally or through a broker matched trade submission facility to be registered for clearing. Trades executed or registered through Nodal Trading System in accordance with Nodal Exchange Rules are designated as "Nodal Transactions" and eligible for registration.

Clearing Members can set position limits in contracts on 1,800 hubs, zones and nodes on the Nodal Exchange. Trade sizes can be as little as 1 MW increments.

LCH calculates Initial Margin for Nodal Exchange transactions using a historical simulation Value-at-Risk ("VaR") methodology. A Clearing Member's portfolio is first revalued using historical returns, then the standard deviation of the portfolio profits and losses ("P&L") is used together with other parameters to estimate the portfolio VaR.

PART II -- APPLICATION OF APPROVAL CRITERIA TO CLEARING AGENCY

1. Governance

1.1 The governance structure and governance arrangements of the clearing agency ensures:

(a) effective oversight of the clearing agency;

The activities and operations of LCH are directed and overseen by its Board. The Board of LCH is comprised of nine individuals, is chaired by an independent non-executive LCH Board member, and includes three other independent non-executive directors, four other non-executive directors who are user representatives and one executive director. Fourty-Four percent of the LCH Board consists of independent members.

LCH Group's Articles of Association state the following in respect of "independent directors":

The Nomination Committee shall be entitled by notice in writing to the Company to nominate candidates to be "Independent Directors". The Board acting by simple majority shall appoint, if thought fit for appointment, persons nominated as Independent Directors (such persons shall be referred to for all purposes as the "Independent Directors"). A director appointed in this way may hold office only until dissolution of the next annual general meeting following his appointment unless he is elected by the Company by ordinary resolution at that meeting.

The Board shall consider, in determining whether a person is fit for appointment as an Independent Director, whether such person is independent in character and judgement and whether there are relationships or circumstances which are likely to affect, or could appear to affect, such person's judgement, including if such person:

• has been an employee of the Company or its Group within the last five years;

• has received or receives additional remuneration from the Company or its Group apart from a director's fee, participates in any share option or a performance-related pay scheme of the Company or its Group, or is a member of a pension scheme of the Company or its Group;

• has close family ties with any of the Company's or its Group's advisers, directors or senior employees;

• represents a significant shareholder; or

• has served on the Board for more than nine years from the date of his first election.

The Board shall state its reasons in the resolution of the directors appointing the Independent Director if it determines that a person nominated as an Independent Director is independent notwithstanding the existence of relationships or circumstances which may appear relevant to its determination including those listed in the articles.

Governance arrangements are clearly specified and information regarding them is publicly available in the annual report of the LCH Group.

The LCH Board supports the highest standards in corporate governance and, wherever possible, adopts the provisions of the Financial Reporting Council's UK Corporate Governance Code, which sets out principles of good governance for listed companies.

The LCH Board meets at least quarterly throughout the year. It has full and effective oversight of LCH and monitors the senior management through review of and discussions about information provided to it by senior management, as well as reports from internal and external audits.

LCH's Board is accountable to its shareholders. Non-executive directors of the LCH Board are drawn from the membership of the LCH Group Board. LCH Group Board membership includes representatives of users of the services of operating subsidiaries with a variety of complementary skills, product knowledge and industry experience and ensures that LCH Board and customer interests are closely aligned.

The above structure will change once the LSE-LCH Group merger has been finalized. This is not due to occur until Q2 2013 at the earliest. At that stage, LCH will be in a position to confirm the revised LCH Board structure.

(b) the clearing agency's activities are in keeping with its public interest mandate;

LCH's stated corporate objectives are to (i) reduce risk and safeguard the financial infrastructure in the markets LCH serves, (ii) deliver market leading and cost-effective clearing services, and (iii) be the leading multi-asset clearing house, independently serving diverse markets around the world. LCH's governance structure is designed to ensure that LCH meets these corporate objectives. The LCH Board retains the responsibility to ensure that LCH meets these objectives.

(c) fair, meaningful and diverse representation on the governing body (Board) and any committees of the Board, including a reasonable proportion of independent directors;

See the response to (a) above.

LCH maintains Audit and Risk Committees. The Audit Committee is an independent committee which, under its terms of reference, must comprise no fewer than four non-executive directors of LCH{6}, as discussed in subsection 1.1(a) above. The Risk Committee is independent from any direct influence by the management of LCH and maintains a Clearing Member and end-client representation composition. The Risk Committee is chaired by an independent non-executive director. The Audit Committee has responsibility for review of financial statements, oversight of internal and external auditors, regulatory compliance and the internal control environment. The Risk Committee oversees membership criteria, risk policies (including adequacy of the Default Fund and operational risk controls). While the Risk Committee is charged with reviewing current, and determining new, risk policies, the LCH Chief Executive Officer retains responsibility for default declaration and default handling, in order to ensure speed of action and the avoidance of potential conflicts of interest.

Day-to-day operations of LCH are the responsibility of LCH's chief executive and other senior management. Their decisions are exercised with an appropriate degree of independence from the LCH Board.

See also (b) above.

(d) a proper balance among the interests of the owners and the different entities seeking access (participants) to the clearing, settlement and depository services and facilities (settlement services) of the clearing agency;

Membership applications are subject to the Risk Committee approved criteria and approvals or rejections are made under the delegated authority of the Risk Committee. The Risk Committee is comprised of up to nine LCH executives, two participants from the interest rate swaps market, two representatives with specialist risk, related audit and/or regulatory experience, and two buy-side participants. The external Risk Committee members attend in their capacity as risk experts and do not represent their employer.

Membership criteria are set out in the clearing house procedures. Membership criteria must be met in order for an applicant to be considered for Clearing Member status. These requirements are without prejudice to the provisions of the Clearing Membership Agreement which must be executed by the applicant, and must equally be met by Clearing Members.

(e) the clearing agency has policies and procedures to appropriately identify and manage conflicts of interest;

The Risk Committee and Audit Committee have procedures in place to manage potential conflicts of interest or conflicts of interest when they arise.

Both the Risk Committee and Audit Committee are governed by Terms of Reference.

Under powers formally delegated by the LCH Board, the Chief Executive of LCH has responsibility for establishing, maintaining and implementing the risk management framework (embracing principles, policies, methodologies, systems, internal controls, processes, procedures and people) in line with the Group Board's approved appetite for risk (the extent and categories of risk which the Group Board regards as acceptable for the group to bear). This explicit delegation of powers, which otherwise might anyway have been assumed to be exercised by the executive, is considered necessary formally to preserve the independence of risk management, to avoid conflicts of interest if the LCH Board or Risk Committee was involved in the decision-making and to ensure a timely response to situations which can develop and deteriorate rapidly

Matters concerning significant risks faced by the Group's operating subsidiaries are addressed by a Risk Committee of the relevant subsidiary board or, in the case of operational risk matters, by the Audit Committee of the relevant subsidiary.

The Chairman of the Risk Committee of each subsidiary reports to the Board on the discussions, decisions and recommendations of the committee in order for the Board to understand the business implications and where necessary to formally ratify these decisions and recommendations. Under powers formally delegated by the Board, the Chief Executive of each subsidiary has responsibility for all risk decisions taken within the framework of agreed risk policies. All changes to risk policy require thorough review by the Risk Committees and either their approval or recommendation for Board approval.

Conflicts of interest are monitored closely. First, conflicts of interest for every director are investigated at the time of appointment, considered and approved by the LCH Board and reviewed annually. Second, conflicts of interest for every director are also addressed at every LCH Board meeting in relation to the agenda items and the sensitivity of projects arising in the course of LCH Board business.

(f) each director or officer of the clearing agency, and each person or company that owns or controls, directly or indirectly, more than 10 percent of the clearing agency is a fit and proper person; and

Each LCH Board member has extensive experience, knowledge and skills necessary to operate LCH's clearing facility. The LCH Board meets at least quarterly throughout the year. It has full and effective oversight of LCH and monitors the senior management through review of and discussions about information provided to it by senior management, as well as reports from internal and external audits.

As at end of December 2012, there is no single shareholder with a holding of 10% or more of LCH's issued and outstanding shares. There is currently no legal or regulatory restriction in respect of a shareholding of greater than 10%.

(g) there are appropriate qualifications, limitation of liability and indemnity provisions for directors and officers of the clearing agency.

See 1.1(a) and 1.1(b) above.

The Chief Executive Officer and senior management of LCH have responsibility for the day-to-day operations of LCH. Their decisions are exercised with an appropriate degree of independence from the LCH Board. See also paragraph 1.1(d) above on the Risk and Audit Committee structure.

LCH's Directors and Officers insurance is in place.

2. Fees

2.1 All fees imposed by the clearing agency are equitably allocated. The fees do not have the effect of creating unreasonable barriers to access.

LCH has in place procedures to control its costs of operation; regular analysis and benchmarking on charges are undertaken. Over the past three years, competition has led to significant fee reductions. In terms of fees, there are many different fee-structures within LCH, fee-structures are transparent and available on the LCH website.

LCH is entitled to levy fees in respect of such matters and at such rates as may from time to time be prescribed. Fees shall be payable by Clearing Members, as may be prescribed by LCH Procedures.

A minimum monthly charge per Clearing Member of €5,000 is applied across all LCH activity in RepoClear, the total registration fees chargeable to a Clearing Member are detailed in the fee schedule on LCH's website. There are no transaction fees per se for SwapClear. Clearing Members pay a fixed annual clearing fee to participate in the SwapClear service. Smaller Clearing Members may from time to time incur a transaction fee if certain thresholds are exceeded.

LCH's EnClear service fees are calculated on a per lot basis depending upon the contract. The fee schedule for EnClear can be found on LCH's website.

The fee schedule for Nodal is detailed on LCH's website.

2.2 The process for setting fees is fair and appropriate, and the fee model is transparent.

See 2.1 above.

Fees are determined at the LCH Group Board level. Clearing fee income and associated rebates, together with other fee income, is recognized on a transaction by transaction basis in accordance with the Group's fee scales. The Group does not operate an ex-ante rebate scheme. Any changes made to the fees and charges payable shall take effect, as prescribed by the LCH Procedures. Fees are notified to the regulators prior to taking effect.

3. Access

3.1 The clearing agency has appropriate written standards for access to its services.

By virtue of the membership agreement that Clearing Members sign with LCH, Clearing Members are subject to the rules made by LCH in the conduct of their business.

The rules and procedures are publicly available on the LCH website and the governing laws and regulations are available on relevant websites.

LCH has clear internal procedures for access to its services. These are consistent with the LCH rules and procedures publicly available.

The Rules of LCH are published and amended from time to time to accurately reflect the services provided. LCH notifies the FSA and Clearing Members of new rules and rule changes in line with FSMA. LCH notifies the FSA and CFTC of the Rules of LCH where applicable and publishes them upon approval. LCH notifies both the FSA and CFTC of Default Fund Rules 14 days prior to publication.

3.2 The access standards and the process for obtaining, limiting and denying access are fair and transparent. A clearing agency keeps records of

(a) each grant of access including, for each participant, the reasons for granting such access, and

In considering a new Clearing Member application, LCH conducts thorough reviews into the organization concerned. Potential Clearing Members must meet the basic requirement to be considered for membership, which is a minimum net capital requirement of £5million{7} The minimum contribution for the four clearing services set out in this application are defined in LCH's Default Fund Rules. Appropriate banking arrangements must be put in place, and the organization must have appropriate systems to cope with their clearing activities.

Members are now subject to an internal credit rating. The final rating is determined by the Risk Executive's interpretation of:

• Market Implied Ratings / Credit Edge

• Financial Resources

• Operational capability

• Support -- (where an explicit statement of support is provided froma higher rated entity).

With respect to becoming an EnClear Member, the Clearing Member must either be, or have applied to become, a RepoClear Clearing Member, a SCM, an EquityClear Clearing Member, a Clearing Member of the relevant exchange(s), an LCH EnClear OTC Clearing Member or a Special Clearing Member. Clearing Member status may be granted on a conditional basis before any Clearing House requirements have been fully met or before related exchange clearing membership(s) requirements are met, but cannot be operational until such requirements are satisfied.

A Clearing Member will need to satisfy the criteria for membership set out in section 1 of the LCH Procedures. The minimum membership criteria also act as a default protection mechanism for LCH by ensuring that all Clearing Members are of sufficient financial resource and operational standing.

In considering an organization for membership, analysis is conducted on the following areas:

• Legal formation and history of incorporation, including subsequent mergers & acquisitions;

• The corporate organization (subsidiaries, branches, sister companies, representation offices) indicating whether or not the counterparty subcontracts its activity;

• Regulation -- level and quality of regulation across different jurisdictions;

• Ownership;

• History of markets and clients cleared and current clearing member status.

The above process is fully documented.

A formal process is in place for appeals for Clearing Members and or certain other circumstances. This process is set out in the LCH Procedures.

(b) each denial or limitation of access, including the reasons for denying or limiting access to an applicant.

Under Section 1.2 of LCH's Clearing House Procedures, the denial of access or limitation of access, including the reasons for denying or limiting access to a Clearing Member is documented and transparent. LCH may, in its sole discretion, refuse an application for membership where it considers it appropriate to do so in accordance with its internal risk management policies and procedures as amended from time to time. LCH may, at any time, impose additional conditions relative to continued Clearing Member status, and at any time vary or withdraw any such conditions. These conditions may include, but are not limited to, a requirement to deposit additional security in cash or collateral as determined by LCH.

4. Rules and Rulemaking

4.1 The clearing agency's rules are designed to govern all aspects of the settlement services offered by the clearing agency, and

(a) are not inconsistent with securities legislation,

LCH has obtained legal opinions on both Canadian federal and Ontario law to ensure that its arrangements are consistent with local law. From these opinions LCH has taken comfort that its rules are consistent with Canadian federal and Ontario law.

LCH is required under the FSMA to have procedures and arrangements in place to enforce its rules. In practice, as the majority of the rules, as laid out in the LCH Regulations including its Procedures, are in relation to the daily compliance with financial obligations, the daily or monthly compliance with delivery obligations, and the quarterly re-calculation of the Default Fund contributions, therefore, enforcement is routine and essentially automated. As a leading independent CCP, LCH does not have conduct of business rules of the kind established by the exchanges whose contracts it clears or the regulators of its Clearing Member firms. FSMA Regulations 2001, Paragraph 23 requires a Recognized Clearing House to have effective arrangements for the investigation and resolution of complaints arising in connection with the performance of, or failure to perform, any of its regulatory functions, including arrangements for the investigation of a complaint by a person independent of the clearing house. To date, LCH has not had need of such a formal procedure to date, and has not had to deal with any such complaint.

(b) do not permit unreasonable discrimination among participants, and

Because non-compliance with most rules is so visible -- and would constitute an act of default under LCH's Default Rules -- compliance can be said to be mandatory. In the case of financial resource requirements, LCH CRO staff check compliance; their work being independent of the requirement on Clearing Members to inform LCH if they fall below the lowest amount.

LCH has no published list of disciplinary actions. LCH's rules do not discriminate among Clearing Members as they apply equally to all Clearing Members.

(c) do not impose any burden on competition that is not necessary or appropriate.

Clearing Members have the right to apply for approval to clear one or more of the markets cleared by LCH, subject to meeting the requirements of LCH in respect of each such market and not imposing unnecessary or inappropriate burdens on competition.

4.2 The clearing agency's rules and the process for adopting new rules or amending existing rules should be transparent to participants and the general public.

LCH Rules are transparent and available to the public. LCH Rules are maintained on the LCH website.

The Rules of LCH are published and amended from time to time to accurately reflect the services provided. LCH notifies the FSA and Clearing Members of new rules and rule changes in line with FSMA. LCH also notifies the CFTC of changes to the Rules of LCH where applicable and publishes them upon approval. Under the European Market Infrastructure Regulation (EMIR), LCH will be required to publicly consult on rule changes.

4.3 The clearing agency monitors participant activities to ensure compliance with the rules.

LCH monitors Clearing Member activities to ensure compliance with the rules by conducting a risk-based review which incorporates both a qualitative and quantitative assessment: qualitative in terms of due diligence reviews and visits and quantitative tools that include credit ratings and more sensitive market indicators such as implied ratings and expected default frequency. The process draws together data from a number of sources to give an overall impression of the counterparty risk associated with the Clearing Member.

Clearing Members can be subject to due diligence visits by LCH, the purpose of this assessments is to discuss ongoing corporate structure and strategy; the scope of the Clearing Member's business generally and clearing activities specifically; financials; regulation; operational processes; banking facilities, and risk management (of clients and any proprietary business, margining, credit management policy, stress testing, etc.). The analysis looks at exposure to LCH, such as details of current and historical margins, collateral held, market concentrations and stress testing results, T-Ratio Analysis, future plans and other exposures (e.g., as a treasury investment counterparty, PPS Bank).

For delivery failures in the case of LCH's RepoClear, LCH Regulation 59(c) establishes that if a Clearing Member persistently fails to deliver securities to LCH, LCH shall be entitled to terminate membership of the firm in question, on written notice, requiring liquidation or transfer of open contracts. LCH has not had to apply Regulation 59(c).

In the case of LCH's SwapClear, a failure to delivery will be deemed a failed delivery on Delivery Day +1. Buying-in will occur at 11:00hrs on the Delivery Day +1.

In respect of EnClear, buying-in will be executed in respect of a failure by the Selling Clearing Member to make a Transfer Request that results in the receipt of the necessary Instruments into the Holding Account of LCH.

See also section 4.1(b) above.

4.4 The rules set out appropriate sanctions in the event of non-compliance by participants.

See above 4.1(b) and 4.3 above.

5. Due Process

5.1 For any decision made by the clearing agency that affects an applicant or a participant, including a decision in relation to access, the clearing agency ensures that:

(a) an applicant or a participant is given an opportunity to be heard or make representations; and

Full LCH appeals procedure can be found on LCH's website. A brief overview of the process is set out below.

A Clearing Member or, in certain cases, a RepoClear Dealer or SD or other non-member, may appeal against a decision of LCH.

A Clearing Member may appeal against any of the following decisions made by LCH:

• A decision that the Clearing Member does not meet the criteria for extension of its clearing relationship with LCH;

• A decision by LCH to rescind that Clearing Member's eligibility to have contracts of a certain category or categories registered in its name;

• A decision by LCH to terminate that Clearing Member's Clearing Membership Agreement other than when such decision occurs in connection with the operation by LCH of its Default Rules and Procedures.

Appeals must be made lodging an appeal via an appeal form to the Company Secretary, who shall acknowledge receipt within 7 days. Further information may be requested.

There are several steps by which an appeal can proceed, namely, the appeal can be submitted by the Company Secretary to the Appeal Committee, or to an Appeal Tribunal in the event that a notice of further appeal is made.

(b) the clearing agency keeps a record of, gives reasons for, and provides for appeals or reviews of, its decisions.

LCH keeps a record of, and gives reasons for, its decisions that affect an applicant or Clearing Member, including a decision relating to access. Additionally, LCH provides for appeals or reviews of its decisions. A Clearing Member who is aggrieved by any action taken by LCH or decision of LCH (other than any decision set out in 11.2 of Clearing House Procedures), or any decision taken under Regulation 26 in or under or in connection with LCH's powers under the Default Rules and Procedures may, no later than 14 days after the date of the decision or action, request a review of such action or decision by the Chief Executive of LCH.

6. Risk Management

6.1 The clearing agency's settlement services are designed to minimize systemic risk.

As a CCP, LCH is responsible for the performance of all registered contracts through to their final settlement. In the case of all swap contracts, that final settlement takes the form of a cash payment from one Clearing Member to another -- that last payment bringing to an end the chain of periodic payments initiated after registration and made on the basis of settlement to latest market prices. All such cash payments are made through LCH's PPS, which is an assured payments arrangement operated by LCH and twelve banks in the U.K. and seven banks in the U.S. that act as bankers to LCH's Clearing Members. LCH currently has no PPS arrangements in Canada.

LCH has a rigorous intra-day margining policy and monitors the creditworthiness and market exposure of each Clearing Member on an ongoing basis. (For further information please refer to section 6.3(1)).

Before the SwapClear Restrike project (referred to previously), LCH maintained a single default fund comprised of contributions from Clearing Members across all markets cleared by LCH. Technically, this consisted of four default funds, each with a predetermined maximum fund size: the Exchange Fund (£310 million); the EquityClear Fund (£100 million); the RepoClear Fund (£105 million); and the SwapClear Fund (£125 million). Contributions to each fund were called from all Clearing Members authorized to clear the relevant products, and were pro-rated on the basis of initial margin, except for the Exchange Fund, which also considered the share of cleared volume when calculating contributions. Notwithstanding the distinction between funds, in the event of a default the funds acted as one default fund; that is, the aggregate amount was available for losses incurred as a result of a default in any market.

In May 2012, LCH segregated the SwapClear Default Fund under a "Limited Recourse" structure. The new Default Fund size is set with a floor of £1 billion and a cap of £5 billion. For each Clearing Member the stress test losses over initial margin will be evaluated based on the exposures across each Clearing Member's House accounts plus the exposures of their clients.

SwapClear Contributions are risk weighted, with each SCM being required to contribute a minimum of £10 million. The segregation of the SwapClear Fund means that, in the event of a default of a SCM, LCH will not have recourse to contributions of non-SCMs. Equally, LCH will not have recourse to contributions of SCMs in the event of a default of a non-SCM(s). Contributions of the defaulter itself will be available across services.

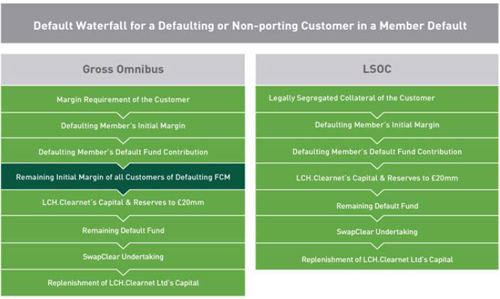

In the event that the default of a SCM exhausts all of the resources available to LCH in relation to that default (the "SwapClear Waterfall"), the SwapClear Service will close. In contrast to the current arrangements the SwapClear Waterfall is limited recourse in that (i) it does not extend to the general capital of LCH, and (ii) SCMs are not obliged to make additional payments to make good any shortfall to LCH. Ontario resident SCMs are, and will continue to be, subject to the Gross Omnibus Default Waterfall shown below.

All SCMs will be obliged to provide additional unfunded Default Fund contributions limited to one such payment per SCM default up to a maximum of three defaults in six months.

In August 2012, LCH segregated the RepoClear Default Fund, and the maximum size of the default fund, based on the stress tests applied to current positions of RepoClear members, is set at €620 million with a cap of €1,500 million.{8} LCH further proposes to implement an enhanced RepoClear Default Fund and related Default Management process. Discussions are in progress with LCH's Product Advisory Group and RepoClear Default Fund Design Group. Phase II of this process is developing the Service Closure component ("living will") of the Default Fund, and a formalized Default Management process. Implementation is scheduled for the first half of 2013.

Notwithstanding the separation of the default funds, a defaulting Clearing Member's contribution to any default fund will be available to cover a loss arising from any clearing service.{9} By contrast, surviving Clearing Members' contributions to a particular default fund will be available only to cover losses arising from the clearing service(s) relevant to that default fund.

In November 2012, LCH SwapClear moved to a Legal Segregation with Operational Commingling (LSOC) model which restricts a DCO from utilizing the assets of one customer to meet the obligations of another customer or FCM in the event of a default (as depicted above).

6.2 The clearing agency has appropriate risk management policies and procedures and internal controls in place.

LCH recognizes that the management of counterparty and market risk associated with its CCP role, maintenance of adequate capacity and security with respect to its automated (IT) systems and the establishment, testing, evaluation and modification of, and back-up plans with respect to, such systems is integral to the achievement of its objective of providing secure and efficient clearing services to Clearing Members.

The most obvious risk managed by LCH is that of a clearing member no longer meeting, or being able to meet, its financial obligations to the clearing organisation. As the contractual CCP to all Clearing Members, LCH is legally obliged to assume the open, registered positions of the defaulting Clearing Member and to ensure their settlement or transfer. In so doing, LCH protects the non-defaulting Clearing Members, their clients, and the markets from de-stabilizing and contagious consequences. It has become standard practice to describe this central role as one of protecting against systemic risk. LCH has detailed policies and procedures across all services and product lines, and specific market margin policies for the Fixed Income, SwapClear, EnClear and LCH Nodal services, among others.

LCH SwapClear's primary goal after the default of a Clearing Member is to reduce the risk of the outstanding positions. Upon a default, LCH SwapClear immediately facilitates the porting of non-defaulting clients to solvent Clearing Members. LCH SwapClear then begins hedging the portfolio via its DMG.

The DMG meets periodically throughout the year and participates in our default fire drills to ensure preparedness in the event of a default. Once the risk of the portfolio is substantially reduced by the DMG, LCH's SwapClear has the ability to split the defaulter's portfolio by currency and then (at the discretion of the DMG) into small sub-portfolios within that currency. The DMG then conducts an auction for each portfolio. The ability to operationally receive and price an auctioned portfolio is one of the criteria validated by LCH SwapClear prior to granting membership. Further, the operational capabilities of each Clearing Member during a default are tested regularly via our fire drill.

For losses greater than the financial resources of the defaulter, the funded Default Fund contributions of the LCH SwapClear Clearing Members will be attributed into tranches based upon bidding behaviour in the auction:

• Tranche 1 -- Non Bidders;

• Tranche 2 -- Auction Bidders (not winner);

• Tranche 3 -- Auction Winner (plus those with same bid as winner).

As described above, in order to control the default risks that it manages, LCH sets minimum capital requirements for Clearing Members, and monitors compliance with those requirements and the general financial health of its Clearing Members; establishes margining policies of various kinds, together with monitoring and limits on exposures relative to capital; and maintains a Default Fund and related default cover as a precaution against any situation in which a defaulter's initial margin is insufficient to cover the cost to LCH of managing a default.

All SCMs will continue to demonstrate operational capability during a default scenario. All SCMs will be entitled to outsource default management responsibilities to a third party on a case by case basis and on the proviso that certain outsourcing conditions are met and subject always to the discretion of LCH.

In respect of the SwapClear service, LCH relies on non-defaulting SCMs to supply impartial expertise through the DMG and to bid for the portfolio of a defaulting SCM. LCH is committed to ensure that its post-default backing is of appropriate size. Current assessment of the appropriate size of the Default Fund is based on a scenario-based stress testing approach using historical and theoretical scenarios. They include: 1987 Stock Market crash; Long Term Capital Management default; 1992 Sterling ERM exit; 1994 Bond Market collapse; 2008 Lehman Brothers default; 1991 Gulf War; and Hurricane Katrina.

There are other historical scenarios as well as individual product and theoretical scenarios aimed at assuring that LCH's stress testing across the broad range of products offered is not overly reliant on history. The models assess the adequacy of initial margin requirements across the entire membership of LCH, looking at house and client accounts separately, on the basis of a series of extreme price movements in all contracts. The tests are run on a daily basis and the results assessed alongside other risk measures and ratios. The emphasis has been on whether the Default Fund is adequate in size to enable LCH to cope with (i) the default of the largest Clearing Member exposure and five small Clearing Members in the very extreme conditions replicated in the model, or (ii) the simultaneous default of the second and third largest Clearing Member under the same extreme conditions. LCH is committed to continuance of the testing and to taking action in relation to any findings that suggest that the Default Fund would be insufficient to cover these events. Results are assessed daily by the Risk Department{10} and on a quarterly basis by the Risk Committee which reports on adequacy to the LCH Board.

In putting in place these arrangements and procedures; LCH protects itself from attack under insolvency laws by virtue of Part VII of the U.K. Companies Act 1989 ("U.K. Companies Act"), as amended. Part VII provides, broadly, that procedures carried out pursuant to the default rules of an RCH take precedence over the rights of a liquidator or other insolvency office-holder.

The policies and controls relating to counterparty and market risk (including policies relative to money settlement and exposures to banks) fall under the responsibilities of the Risk Department of LCH. New policies designed by the Risk Department are submitted to the Risk Committee, which also reviews existing policies. The boundaries of responsibility are drawn at the frontier between policy and efficacy of policy (Risk Committee responsibility) and day-to-day risk management decisions and actions (Risk Department responsibility).

Internal Audit

The internal audit function conducted by LCH's Internal Audit department covers all aspects of LCH's activities, drawing on external audit expertise as appropriate. The unit, whose head reports to the Chief Administrative Officer, as well as the Chairman of the Audit Committee, has appropriate independence and its work is considered and reinforced by the Audit Committee of the LCH Board.

The review by Internal Audit of the Risk Department focuses on the testing of key policies and procedures relating to governance, internal risk framework, key risk indicators and monitoring and reporting to ensure the robustness of the framework. The detailed reviews are conducted utilizing external expertise where required. Internal Audit do to an extent place reliance upon the expertise of the management within the Risk Department, which in turn provides assurance to the LCH Board, senior management and external regulators (e.g., FSA), that LCH's operational risks are being managed in an effective, timely and appropriate manner.

6.3 Without limiting the generality of the foregoing, the clearing agency's services or functions are designed to achieve the following objectives:

1. Where the clearing agency acts as a central counterparty, it rigorously controls the risks it assumes.

Role of the Risk Department

LCH's Risk Department is underpinned by harmonized policies for all LCH services, thereby eliminating major differences in how risk is controlled. The aim of LCH's Clearing Member and position monitoring is to detect, as early as possible, events that may threaten the ability of a Clearing Member to continue to meet its obligations to LCH. The Risk Department of LCH monitors information on Clearing Members' creditworthiness and financial condition. The primary information considered by the Risk Department comprises: (i) financial reports and regulatory returns; (ii) external credit-ratings, market implied ratings and expected default frequency; and (iii) LCH's evaluation of its operational capability, business strategy and level of support from parent or sovereign. .

In this latter regard, the Risk Department will consider, in addition to financial reports and regulatory returns and external credit ratings, factors such as: (i) the Clearing Member's legal and ownership structure; (ii) if part of a holding company, the nature of the group business; (iii) the principal officers of the Clearing Member; (iv) operational issues that have been identified; (v) how the Clearing Member compares with its peers (e.g., markets cleared, net capital, external ratings); and (vi) the financial support available to the Clearing Member and whether the support is implicit or explicit, taking into account the systemic risk that may be posed by the Clearing Member.

In, deriving an internal credit score for Clearing members, a score attached to each of the quantitive factors is assigned a specific weight. The total score from these factors can be amended following further assessment of qualitative information regarding operational capability and business strategy to give a final score for each Clearing Member.. The Risk Department recommends the internal credit scores to the Executive Risk Committee{11} (ERCO), for approval or further review. The internal credit score influences the Risk Department's response to specific risks identified by the Daily Risk Monitoring and determines the frequency with which the Risk Department will conduct future assessments of the Clearing Member.

LCH pays particular attention to positions that are large in relation either to a Clearing Member's financial resources or to open interest in a particular contract and that would challenge LCH's holding periods and close-out assumptions. In relation to futures business the position monitoring looks at house and client accounts separately and in the aggregate. The basic assessment is undertaken daily on the basis of end-of-day positions. However, LCH has full intra-day risk assessment capability for both its futures and non-futures business (including OTC derivatives and cash equities) and performs routine intra-day monitoring of valuation losses and re-calculated initial margin requirements, including new business. If monitoring gives rise to concerns about the size of positions in a Clearing Member's client account (which at LCH may be an omnibus account or for certain cleared business LSOC (see section 6.1 or full segregated), further information is sought from the Clearing Member, notably about the concentration of individual client positions. Although LCH does not routinely collect information on individual client positions, LCH may require Clearing Members to provide such information (refer to LCH Procedures 1.1.3).

Initial and Intraday Margin

A key monitoring ratio is that of initial margin to financial resources, whereby the level of initial margin is monitored and action can be takne if it exceeds a threshold in comparison to net capital. Thresholds are set in relation to internal credit scores.

LCH has a clear statement from the LCH Board on its Risk Appetite for initial margin that applies across all product lines; the Risk Management Department is expected to ensure that initial margin is sufficient to cover 99.7 percent of observed profits and losses over the assumed holding period of the contract(s). This Risk Appetite is backtested regularly and reported to the Risk Committee on at least a quarterly basis. LCH generates initial margin requirements for cleared swaps (SwapClear) using Probabilistic Approach to Interest-Rate Scenarios ("PAIRS").

Where LCH algorithms require the setting of margin rates, they are routinely reviewed for all major contracts (e.g., contracts with significant open interest are reviewed at least monthly). Additional reviews occur when a margin level is challenged or exceeded by price movements or when an unexpected event occurs between scheduled reviews (e.g., sudden news of a political or economic event). The primary focus in setting margin levels is on price history, close-to-close and intra-day range movements. Analysis based on price data is augmented by the implied volatility of related option contracts and assessment of imminent, known price-sensitive events. In the case of commodity contracts, observed seasonal patterns are also taken into account in setting margin levels. LCH has full authority to implement an increase in margin levels applicable to any or all of its Clearing Members under LCH Regulation 12. The levels of margin held and their appropriateness against observed profits and losses is reviewed daily for each Clearing Member and back testing results are reviewed at least monthly by the Risk Department.

LCH has an intra-day margin policy for all products that it clears, including exchange-traded futures and options on futures. The policy is based on full re-valuation and re-calculation of initial margin requirements in respect of all registered contracts, including contracts entered into on the day of the call. The intra-day margin policy provides for regular intra-day recalculations and the collection of additional margin liabilities above a de minimis level set for each Clearing Member in relation to its internal credit score.

Where additional funds are required, they are collected in cash through the PPS, discussed in Section 6.1 above, with the possibility of late calls for dollars in New York. Where surplus cover, in cash or non-cash collateral, is available, it is utilized by LCH to satisfy the call.

Intra-day calls must be confirmed by PPS banks no later than one hour after they are made. The PPS agreement establishes 14:00 London time as the latest time at which LCH may make a call in London and 21:00 London time as the latest time at which LCH may make a call in New York.

SwapClear

Initial margin is collected from each Clearing Member to cover potential losses in the event of a default under prevailing market conditions over a specified holding period and at a specified confidence level. LCH's SwapClear initial margin is calculated on the basis of a five-day holding period per member's house positions and seven-days for clients and is the aggregate worst case loss across all currencies over the historical period, using LCH's proprietary PAIRS margin methodology. PAIRS is a VaR model based on filtered historical simulation incorporating modified volatility scaling. The model uses five years (1250 days) of historical market data to simulate changes in portfolio value from which an estimate of potential loss is calculated. Portfolio positions are fully revalued in each scenario. PAIRS addresses the effects of volatility clustering in interest rate markets by implementing a modified volatility scaling methodology, whereby historical scenarios are explicitly scaled to reflect prevailing market conditions. Volatility scaling is applied based on an "Exponentially Weighted Moving Average" (EWMA) model with a decay factor of 0.97.

In addition to PAIRS initial margin, SwapClear applies margin add-ons covering Credit Risk, Liquidity Risk Sovereign Risk and Concentration Risk where a particular Clearing Member's inherent risk exposure is not captured within the PAIRS model.

In the case of any future expansion of contract types cleared as a registered DCO, LCH would look to use one of its established initial margining methods, with necessary adaptation, on the basis of an assessment of which most appropriately measures the risk of a new contract type to ensure consistency with its 99.7 percent Risk Appetite.

RepoClear

RepoClear uses an adaptation of London SPAN® (Standard Portfolio Analysis of Risk system) and the reviews of the appropriateness of the price assumptions about the different types of bonds are similar to those for comparable reviews of futures contracts.{12} As above, RepoClear applies margin add-ons covering Credit Risk, Wrong Way Risk, Sovereign Risk and Concentration Risk and Stress test losses.

EnClear

LCH's EnClear Service also uses London SPAN® that incorporates both futures and options, and calculates the net Initial Margin requirement. There are three major inputs to the London SPAN margin calculation -- Positions, Prices and Parameters (determined by LCH and reviewed on a continual basis). A change to any one of these will result in a change to the margin requirement.

LCH Nodal

For Nodal Exchange Margining Methodology, LCH calculates Initial Margin for Nodal Exchange transactions using a historical simulation VaR methodology. A Clearing Member's portfolio is first revalued using historical returns, then the standard deviation of the portfolio P&L is used together with other parameters to estimate the portfolio VaR.

LCH also calculates a minimum margin figure to ensure that a minimum level of margin is called. To calculate the minimum margin, the Minimum Margin Percentage (MP), a parameter set by LCH, is multiplied by the total gross portfolio value (the absolute value of the long positions plus the absolute value of the short positions).