Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

CSA Multilateral Staff Notice 58-309 Staff Review of Women on Boards and in Executive Officer Positions- Compliance with NI 58-101 Disclosure of Corporate Governance Practices

CSA Multilateral Staff Notice 58-309 Staff Review of Women on Boards and in Executive Officer Positions- Compliance with NI 58-101 Disclosure of Corporate Governance Practices

CSA Multilateral Staff Notice 58-309

Staff Review of Women on Boards and in Executive Officer Positions –

Compliance with NI 58-101 Disclosure of Corporate Governance Practices

Date: October 5, 2017

Table of Contents

|

1. Executive Summary |

|

|

2. Background |

|

|

3. Three Year Review |

|

|

4. Findings |

|

|

5. Disclosure Deficiencies |

|

|

6. Conclusion and Questions |

|

|

Appendix A: Summary of Form 58-101F1 Corporate Governance Disclosure related to the WB/EP Rules |

1. Executive Summary

This staff notice (Staff Notice) reports the findings of staff of the securities regulatory authorities in Alberta, Manitoba, New Brunswick, Newfoundland and Labrador, Northwest Territories, Nova Scotia, Nunavut, Ontario, Québec, Saskatchewan and Yukon (Participating Jurisdictions or we) of our recent review of disclosure regarding women on boards and in executive officer positions as prescribed in National Instrument 58-101 Disclosure of Corporate Governance Practices (NI 58-101) (the WB/EP Rules). This Staff Notice reports the findings based on a review sample of 660 issuers that had year-ends between December 31, 2016 and March 31, 2017 (Year 3 or 2017 or current year).

This is the third consecutive annual review of this nature that we{1} have conducted. The findings from our first two annual reviews are set out in:

• CSA Multilateral Staff Notice 58-307 Staff Review of Women on Boards and in Executive Officer Positions -- Compliance with NI 58-101 Disclosure of Corporate Governance Practices published on September 28, 2015, which summarized our findings after reviewing the corporate governance disclosure of 722 issuers (Year 1 or 2015), and

• CSA Multilateral Staff Notice 58-308 Staff Review of Women on Boards and in Executive Officer Positions -- Compliance with NI 58-101 Disclosure of Corporate Governance Practices published on September 28, 2016, which summarized our findings after reviewing the corporate governance disclosure of 677 issuers (Year 2 or 2016).

This Staff Notice highlights the trends we have observed in the three reviews as well as certain compliance findings.

Key findings and observed trends at a glance

The table below provides a snapshot of the key findings from our reviews:

Findings

Year 1

Year 2

Year 3

Board Representation

Total board seats occupied by women

11%

12%

14%

Issuers with at least one woman on their board

49%

55%

61%

Issuers with three or more women on their board

8%

10%

11%

Board seats occupied by women for issuers with over $1 billion market capitalization

16%

18%

20%

Board seats occupied by women for issuers with over $10 billion market capitalization

21%

23%

24%

Board vacancies filled by women

_____

_____

26%{2}

Executive Officers

Issuers with at least one woman in executive officer positions

60%

59%

62%

Policies

Issuers that adopted a policy relating to the representation of women on their board

15%

21%

35%

Targets

Issuers that adopted targets for the representation of women on their board

7%

9%

11%

Issuers that adopted targets for the representation of women in executive officer positions

2%

2%

3%

Identification and Nominating Process

Issuers that considered the representation of women on their boards as part of the director identification and selection process

60%

66%

65%

Issuers that considered the representation of women in executive officer appointments

53%

58%

58%

Term Limits

Issuers that adopted director term limits

19%

20%

21%

{2} Board vacancies filled by women were not included in our reporting in Year 1 and Year 2.

Compliance findings

In our review, we noted the following:

Topic

Findings

Representation of women

•

97% of issuers disclosed the number or percentage of women on their boards.

•

94% of issuers disclosed the number or percentage of women in executive officer positions.

Policies

•

99% of issuers disclosed whether they had adopted a policy relating to the identification and nomination of women directors.

•

Of the issuers that disclosed that they had not adopted such a policy, 94% disclosed why they had not done so.

Targets

•

96% of issuers disclosed whether they had set targets for the representation of women on their boards.

•

95% of issuers disclosed whether they had set targets for the representation of women in executive officer positions.

•

Where no such targets were set, 94% of issuers disclosed that fact and why they had not done so in connection with the representation of women on their board, while 93% did so in connection with the representation of women in executive officer positions.

Director term limits

•

98% of issuers disclosed whether they had adopted director term limits, other mechanisms of board renewal or both.

•

Of issuers that had not adopted these measures, 97% disclosed their reasons for not doing so.

While a qualitative assessment of disclosure was not the focus of our review, we noted instances where disclosure required by the WB/EP Rules was vague or boilerplate in nature. We have identified areas for improvement in section 5 Disclosure Deficiencies of this Staff Notice.

2. Background

Disclosure requirements

On December 31, 2014, the Participating Jurisdictions{3} implemented the WB/EP Rules, which require that, on an annual basis, a non-venture issuer disclose:

• the number and percentage of women on its board of directors (board) and in executive officer positions;

• whether it has a written policy relating to the identification and nomination of women directors;

• whether it has targets for the number or percentage of women on its board and in executive officer positions;

• if it considers the representation of women in its director identification and selection processes and in its executive officer appointments; and

• whether it has director term limits or other mechanisms of board renewal.

In the event that a non-venture issuer does not have a written policy relating to the identification and nomination of women directors; does not have targets for the number or percentage of women on its board and in executive officer positions; does not consider the representation of women in its director identification and selection processes and in its executive officer appointments; or does not have director term limits or other mechanisms of board renewal, the WB/EP Rules require the issuer to explain why not.

The WB/EP Rules are intended to increase transparency for investors and other stakeholders regarding the representation of women on boards and in executive officer positions, and the approach that specific issuers take in respect of such representation. This transparency is intended to assist investors when making investment and voting decisions.

Refer to Appendix A, which includes a summary of the disclosure requirements of Form 58-101F1 Corporate Governance Disclosure of NI 58-101 (Form 58-101F1) related to the WB/EP Rules.

3. Three Year Review

This is the third consecutive annual issue-oriented review of disclosure provided under the WB/EP Rules.

Sample

As of May 31, 2017, approximately 1,500 issuers were listed on the Toronto Stock Exchange (TSX), of which 788 were subject to NI 58-101.{4} Of these issuers, we reviewed the disclosure of the 660 issuers that had year-ends between December 31, 2016 and March 31, 2017, and filed information circulars or annual information forms by July 31, 2017.{5} To remain consistent with the scope of the reviews we conducted in Year 2 and in Year 1, we did not review the disclosure of issuers with year-ends outside of the December 31 to March 31 time frame. Because of this, our findings, and the comparisons between the current year, Year 2 and Year 1, provide only a partial picture. In particular, the larger Canadian banks, which are part of an industry that has generally been an early adopter of diversity initiatives, are not captured in our reviews.{6}

The issuers in the current year, Year 2 and Year 1 samples vary for several reasons including:

• issuers being delisted from the TSX;

• issuers' listings of securities being moved to the TSX-V;

• corporate reorganizations resulting in issuers no longer being listed on the TSX; and

• issuers filing information circulars after July 31, 2017.

These sample differences could have impacted our comparisons of findings between the current year, Year 2 and Year 1.

Once all issuers have filed their corporate governance disclosure required by the WB/EP Rules for three consecutive years, we intend to publish the data to complete the three year review.

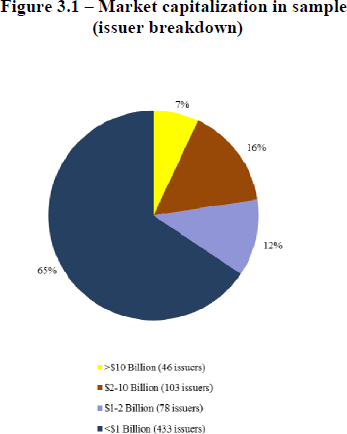

Market capitalization and industries in current sample

The market capitalization of the majority of the issuers in the sample was less than $1 billion (65%) as detailed in Figure 3.1 below. 40% of issuers in the sample had a market capitalization of less than $250 million.

Just over 40% of the issuers were in either the mining or oil and gas industries, with each of the remaining industries constituting between 4% to 13% of issuers as noted in Figure 3.2 below. Of the issuers in the mining and oil and gas industries, 77% and 65%, respectively, had a market capitalization of less than $1 billion.

The relationship between issuer size as measured by market capitalization and the adoption by issuers of initiatives to increase the representation of women on their boards and/or in executive officer positions has been consistent over the last three years.

Figure 3.1 -- Market capitalization in sample (issuer breakdown)

Figure 3.2 -- Industries in sample

4. Findings

The following section summarizes our findings in each of the five key areas:

A. Number of women on the board and in executive officer positions

B. Policies regarding the representation of women on the board

C. Issuer's targets regarding the representation of women on the board and in executive officer positions

D. Consideration of the representation of women in the director identification and selection process and consideration of the representation of women in executive officer appointments

E. Director term limits and other mechanisms of board renewal

A. Number of women on the board and in executive officer positions{7}

Issuers must provide both the number and percentage of women on their board and in executive officer positions each year

The number or percentage of women on their boards was disclosed by 97% of issuers in the sample and the number or percentage of women in executive officer positions was disclosed by 94% of issuers. Although this is an increase in disclosure over Year 2 and Year 1, we remind issuers that they must disclose both the number and percentage for the representation of women on their boards and in executive officer positions each year.{8}

(i) Board

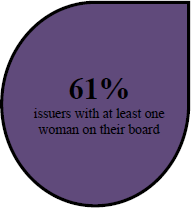

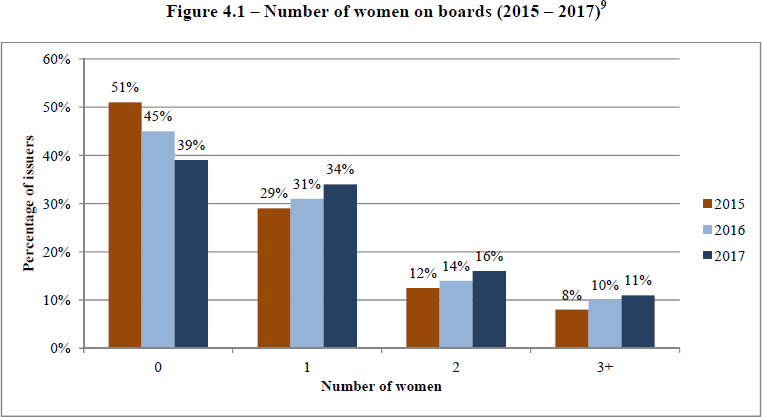

Figure 4.1 illustrates that 61% of issuers had at least one woman on their board, which represents a 6% increase over Year 2 and a 12% increase over Year 1. Further, the number of issuers with one, two, three or more women on their boards has increased each year over the three years covered by our reviews.

Figure 4.1 -- Number of women on boards (2015 -- 2017){9}

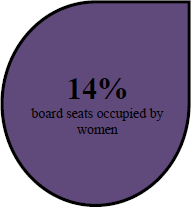

The overall percentage of board seats occupied by women was 14% compared to 12% in Year 2 and 11% in Year 1. Of the issuers in the sample, 15% added one or more women to their boards in the current year, compared to 10% in Year 2{10} and 15% in Year 1.{11}

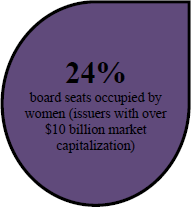

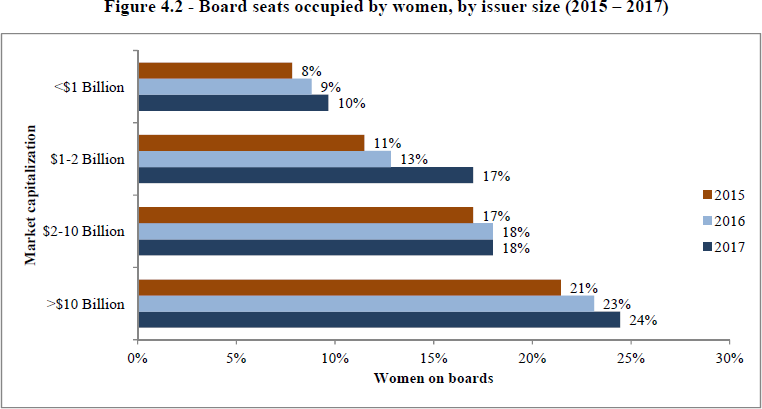

Similar to Year 2, the number of women on boards increased with the size of the issuer. Figure 4.2 shows that the number of board seats occupied by women has increased in all categories of issuer sizes over the three years covered by our review. In the case of issuers with a market capitalization of greater than $10 billion, 24% of board seats are now held by women.

Figure 4.2 -- Board seats occupied by women, by issuer size (2015 -- 2017)

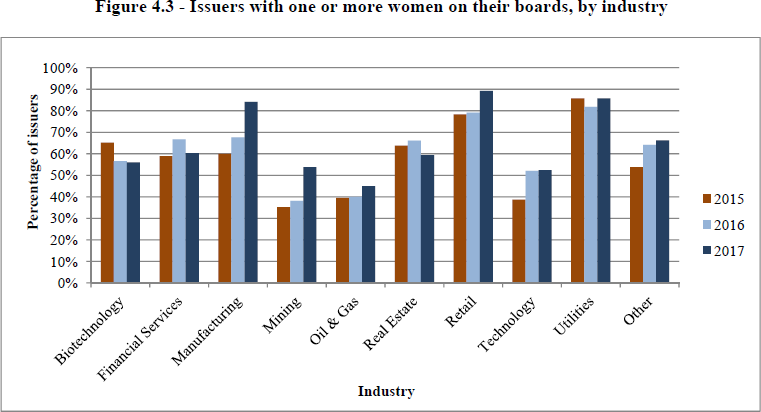

The number of women on boards varied significantly by industry. As noted in Figure 4.3, the retail industry had the greatest percentage of issuers with one or more women on their boards (89%), followed by the utilities industry (86%) and the manufacturing industry (84%), compared to 79%, 82% and 68% respectively in Year 2 and 78%, 86% and 60% respectively in Year 1. The retail and manufacturing industries both reported double digit increases over Year 2 and Year 1 in the percentage of issuers with one or more women on their boards.

Mining issuers also reported double digit increases over Year 2 and Year 1 in the percentage of issuers with one or more women on their boards. Although there was an increase in the percentage of mining, oil and gas and technology issuers with one or more women on their boards, consistent with Year 2 and Year 1, these industries had the lowest percentages of issuers with one or more women on their boards. Specifically, of issuers in the mining and oil and gas industries, 54% and 45% respectively reported that they had one or more women on their boards, increasing from the 38% and 40% reported in Year 2 and from the 35% and 40% reported in Year 1. In the technology industry, 52% of issuers reported that they had one or more women on their boards, which is consistent with the percentage in Year 2. In Year 1, 39% of issuers in the technology industry reported that they had one or more women on their boards.

Figure 4.3 -- Issuers with one or more women on their boards, by industry

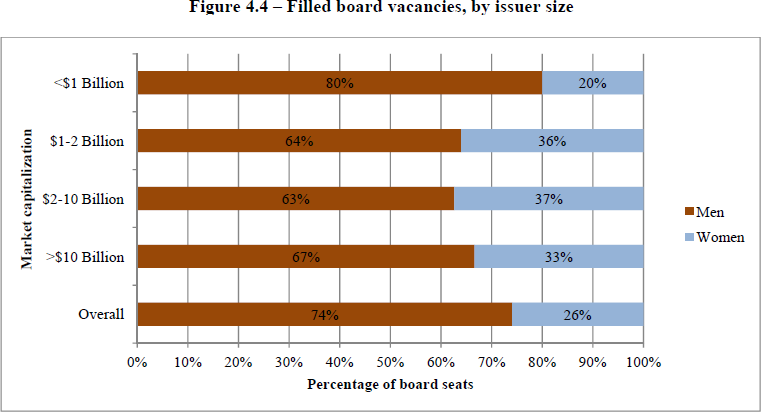

As part of our year-over-year analysis, we also looked at each issuer to determine whether it filled any board vacancies during the year and, if so, the percentage of those positions that were filled by women. In our sample, 674 board seats were vacated during the year and 505 of those seats were filled. As noted in Figure 4.4, of these filled vacancies, 26% (131 seats) were filled by women and 74% (374 seats) were filled by men.

Figure 4.4 -- Filled board vacancies, by issuer size

(ii) Executive officers

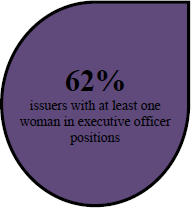

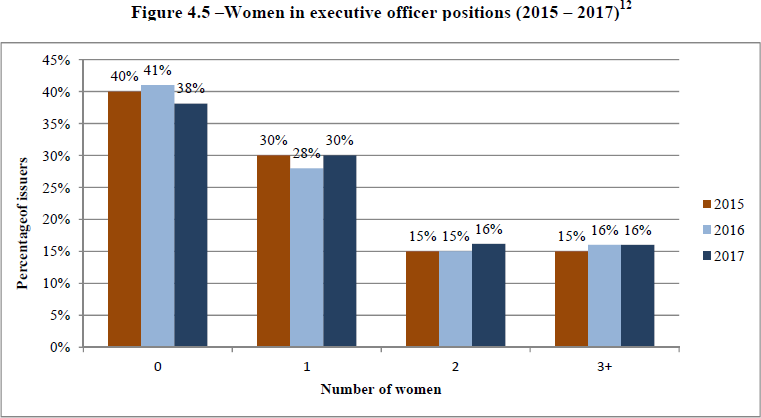

Figure 4.5 illustrates that 62% of issuers that disclosed executive officer information had at least one woman in an executive officer position, which remained relatively consistent with the 59% reported in Year 2 and 60% reported in Year 1. The percentages for those issuers that had two women in executive officer positions as well as those that had three or more in such positions were also relatively consistent over the three years that were reviewed.

Figure 4.5 --Women in executive officer positions (2015 -- 2017){12}

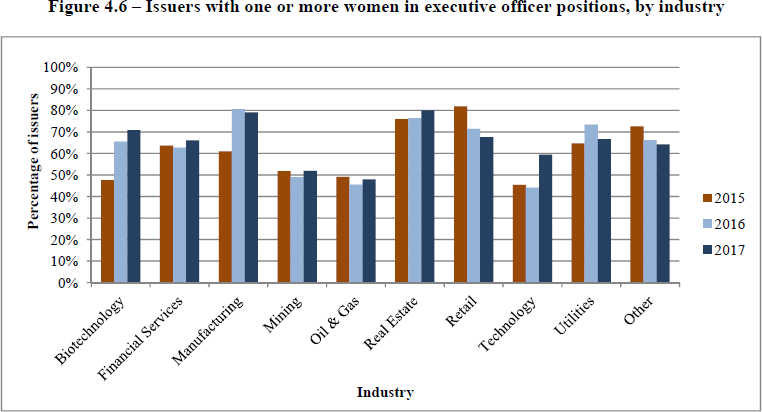

As illustrated in Figure 4.6, the real estate and manufacturing industries had the highest percentage of issuers with one or more women in executive officer positions, whereas the mining and oil and gas industries had the lowest percentage of issuers with one or more women holding such positions. Specifically, 80% and 79% of issuers in the real estate and manufacturing industries that disclosed executive officer information had one or more women in executive officer positions, as compared to 76% and 81% respectively in Year 2, and 76% and 61% respectively in Year 1. Of issuers in the mining and oil and gas industries, 52% and 48% of issuers respectively had one or more women in executive officer positions compared to 49% and 46% in Year 2 and 52% and 49% in Year 1.

Figure 4.6 further illustrates that while there have been double digit increases since Year 1 in the percentage of issuers in the manufacturing industry with one or more women in executive officer positions, there has been a decrease in the percentage of issuers with one or more women in executive officer positions in certain industries, such as the retail industry.

Figure 4.6 -- Issuers with one or more women in executive officer positions, by industry

B. Policies regarding the representation of women on the board{13}

Disclosure about a written policy, if adopted, must describe how it relates to the identification of women directors

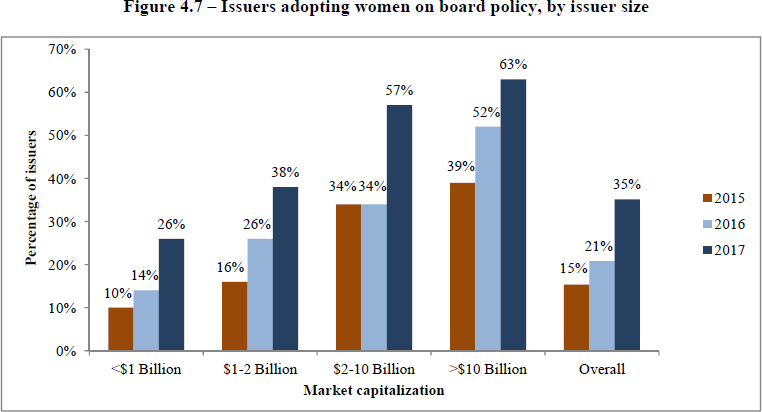

Of the issuers in the sample, 99% disclosed whether they had adopted a policy relating to the identification and nomination of women directors. Of the issuers that disclosed that they had not adopted such a policy, 94% disclosed why they had not done so.{14}

Figure 4.7 illustrates that 35% of issuers disclosed they had adopted a policy relating to the identification and nomination of women directors, representing a significant increase over 21% in Year 2 and 15% in Year 1.{15} Issuers with a market capitalization of greater than $1 billion were more likely to have adopted a policy than issuers with a market capitalization of less than $1 billion. Further, 26% of issuers with a market capitalization of less than $1 billion disclosed that they had adopted a policy relating to the identification and nomination of women directors compared to 14% in Year 2 and 10% in Year 1.

We noted that 53% of issuers disclosed that they did not adopt a policy relating to the identification and nomination of women directors, compared to 59% in Year 2 and 65% in Year 1. Approximately 11% of issuers had broader diversity policies that encompassed a range of characteristics such as: age, ethnicity, race, religion and sexual orientation. However, these policies did not have specific provisions relating to the identification and nomination of women directors.

Figure 4.7 -- Issuers adopting women on board policy, by issuer size

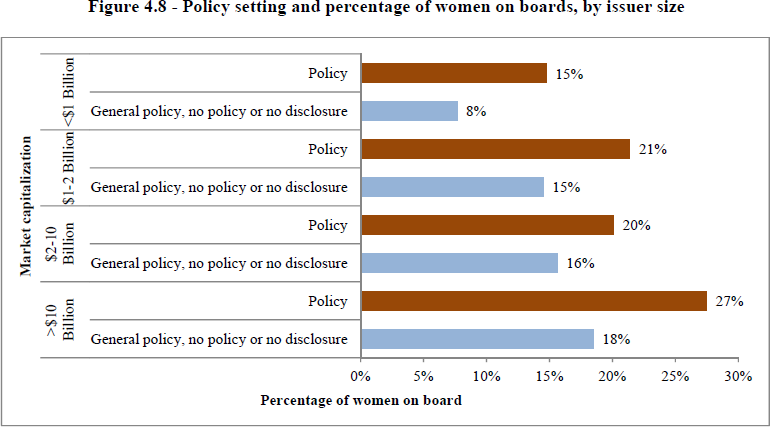

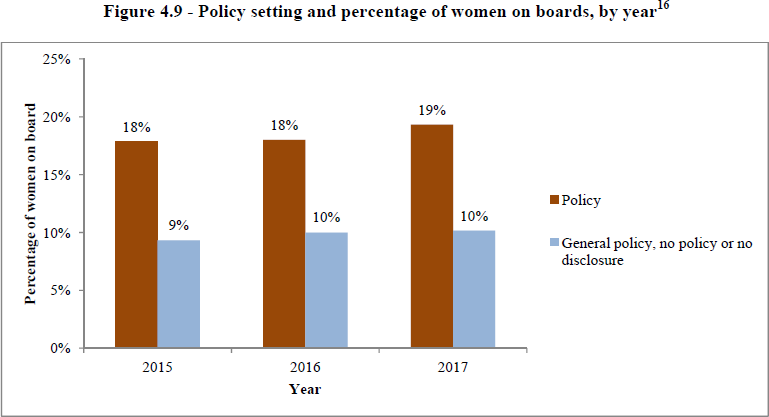

Figures 4.8 and 4.9 illustrate that regardless of issuer size, those issuers that had adopted a policy relating to the representation of women on their boards had a higher percentage of women on their boards compared to issuers without such a policy. The 232 issuers that had adopted a policy relating to the representation of women on their boards had an average of 19% of women on their boards compared to issuers with no such policy, which had an average of 10% of women on their boards. The relationship between the adoption of a policy and the higher representation of women on an issuer's board has been consistent over the last three years. In Year 2 and Year 1, issuers with a policy relating to the representation of women on their boards had an average of 18% of women on their boards compared to issuers with no such policy, which averaged 10% in Year 2 and 9% in Year 1.

Figure 4.8 -- Policy setting and percentage of women on boards, by issuer size

Figure 4.9 -- Policy setting and percentage of women on boards, by year{16}

C. Issuer's targets regarding the representation of women on the board and in executive officer positions{17}

Of the issuers sampled, 96% disclosed whether they had set targets for the representation of women on their boards, while 95% disclosed whether they did so for the representation of women in executive officer positions. Where no such targets were set, 94% of issuers disclosed that fact and why they had not done so in connection with the representation of women on their board, while 93% did so in connection with the representation of women in executive officer positions.{18}

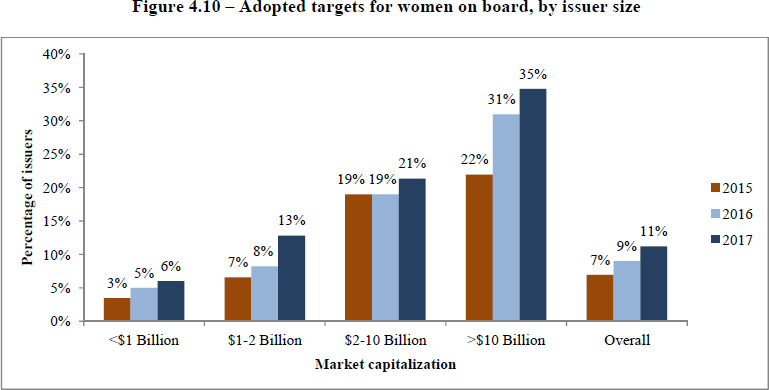

As outlined in Figure 4.10, targets for the representation of women on their boards were set by 11% of issuers, representing an increase from 9% in Year 2 and 7% in Year 1. Issuers set various types of targets such as:

• percentage or number of female board members; and

• percentage or number of female independent directors.

Certain issuers also set staggered targets that extended over a period of years. Of issuers that set targets relating to the percentage of women on their boards, 90% set a target of 25% or greater.

Of issuers that adopted targets for the representation of women on their boards, 86% provided disclosure regarding their progress in achieving their targets. Of issuers with board targets, 57% had already achieved their stated target.

Figure 4.10 also illustrates the relationship between the market capitalization of issuers and the setting of targets for the representation of women on boards. Approximately one third of issuers with a market capitalization of greater than $10 billion adopted such targets compared to 6% of issuers with a market capitalization of less than $1 billion.

A variety of reasons were disclosed by issuers for not adopting targets for the representation of women on their boards and issuers often cited multiple reasons. The most common reasons cited include:

If the issuer has adopted a target, it must disclose the annual and cumulative progress in achieving the target

•

candidates are selected based on merit (64%);

•

targets would not be effective or are arbitrary (12%);

•

targets are unduly restrictive (11%);

•

the issuer wants to select candidates from the broadest talent pool (11%); and

•

it would not be in the issuer's or shareholders' best interest (10%).

Formal targets for the representation of women in executive officer positions were set by 3% of issuers compared to 2% of issuers in Year 2 and Year 1.

Figure 4.10 -- Adopted targets for women on board, by issuer size

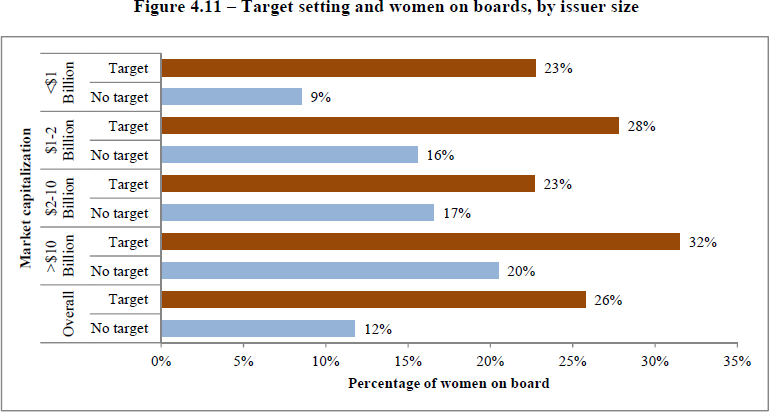

As illustrated in Figure 4.11, regardless of market capitalization, there was a higher representation of women on the boards of issuers that had adopted board targets, compared to issuers without targets. Issuers that had adopted board targets had an average of 26% of female representation on their boards, compared to issuers without targets that had an average of 12% of female representation on their boards. However, we also noted that the representation of women on boards of issuers that had not adopted targets increased from Year 2, except for issuers with a market capitalization of greater than $10 billion.

Figure 4.11 -- Target setting and women on boards, by issuer size

D. Consideration of the representation of women in the director identification and selection process{19} and consideration of the representation of women in executive officer appointments{20}

If the issuer considers the representation of women, it must disclose how it is considered

Of the issuers in the sample, 87% disclosed whether they considered the level of representation of women on their boards, while 84% disclosed whether they considered the level of representation of women in executive officer positions. 37% of issuers that disclosed they consider the representation of women provided disclosure as to how it was considered for their boards, while 34% of issuers did so for their executive officer positions. Where the level of representation of women on their boards or in their executive officer positions was not considered, 99% of issuers disclosed the reasons for not doing so for their boards, while 96% did so for their executive officer positions.{21}

In our sample, 65% of issuers disclosed that they considered the representation of women on their boards as part of their director identification and nominating process compared to 66% in Year 2 and 60% in Year 1. For executive officer appointments, 58% of issuers disclosed that they considered the representation of women when making such appointments in both the current year and Year 2, compared to 53% of issuers in Year 1.

Similar to Year 2 and Year 1, the most common explanation provided by issuers that did not consider the representation of women in their board appointments (83%) or in their executive officer positions (80%) was that their selection was based on merit.

We continue to observe issuers simply disclosing that they consider the representation of women for both their board and executive officer positions without further elaboration. More clarification and detail of how they do so is necessary for the disclosure to be meaningful.

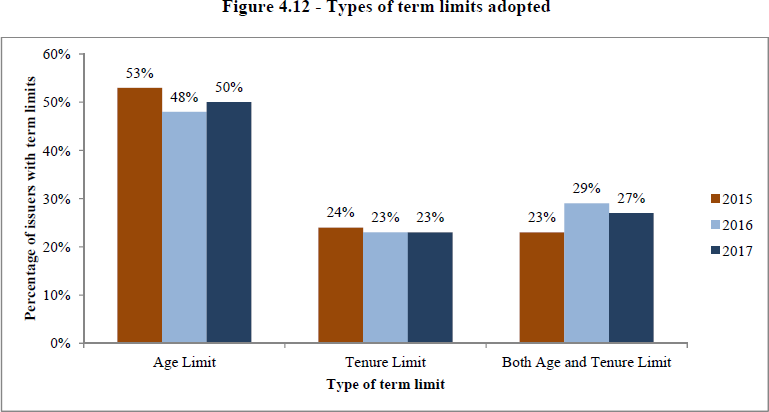

E. Director term limits and other mechanisms of board renewal{22}

If an issuer discloses that it has mechanisms for board renewal, it must describe them including how those mechanisms contribute to board renewal

Of the issuers sampled, 98% disclosed whether they had adopted director term limits, other mechanisms of board renewal or both. Of issuers that had not adopted these measures, 97% disclosed their reasons for not doing so.{23} The most common reason disclosed was that director terms limits may negatively impact the continuity and experience on the board.

In our sample, 21% of issuers disclosed that they had adopted director term limits, compared to 20% in Year 2 and 19% in Year 1. As illustrated by Figure 4.12, issuers adopted different forms of director term limits, with:

• 50% adopting age limits,

• 23% adopting tenure limits, and

• 27% adopting both age and tenure limits.

In addition, many issuers continued to point out that they had other mechanisms of board renewal that they had adopted, but they did not adequately describe them. Many of these issuers disclosed that they conduct regular assessments of their boards and committees for effectiveness and contribution (as required under Item 9 of Form 58-101F1); however, they often did not explain how those assessments contribute to board renewal. An example would be disclosing that a negative assessment could contribute to board renewal by creating a vacancy.

Figure 4.12 -- Types of term limits adopted

5. Disclosure Deficiencies

In our review, we noted disclosure deficiencies in five areas, where the disclosure was often vague or boilerplate in nature, or was not provided at all. We draw issuers' attention to the following disclosure requirements, where these deficiencies were noted:

• Disclosure of both the number and percentage of women on the issuer's board and in its executive officer positions each year.

• If the issuer discloses that it has adopted a written policy regarding the representation of women on its board, a description of that policy, including a clear explanation of how the policy applies to the identification of women directors.

• If the issuer discloses that it has adopted targets regarding the representation of women on its board and in its executive officer positions, annual and cumulative progress in achieving the targets.

• If the issuer discloses that it considers the representation of women in the director identification and selection process and/or when making executive officer appointments, a description of how it does so.

• If the issuer discloses that it has adopted term limits or other mechanisms of board renewal, a description of those limits or other mechanisms and how they contribute to board renewal.

Issuers must provide the disclosure required by the WB/EP Rules. Failure to comply with these requirements could result in regulatory action. We will continue to monitor issuers' corporate governance disclosure related to the representation of women on boards and in executive officer positions.

6. Conclusion and Questions

This Staff Notice reports the findings of our third review of corporate governance disclosure required by the WB/EP Rules. It also compares the findings of this review with the reviews we conducted in Year 2 and Year 1. The WB/EP Rules are intended to provide transparency to assist investors when making voting and investment decisions. This objective is most effectively achieved if the disclosure provides a clear description of the corporate governance practices that an issuer has adopted in relation to women on boards and in executive officer positions, or the reasons for not adopting such practices, as the case may be.

Please refer your questions to any of the following:

Ontario Securities CommissionJo-Anne MatearManager, Corporate Finance416-593-2323Sandra HeldmanSenior Accountant, Corporate Finance416-593-2355Rick WhilerSenior Accountant, Corporate Finance416-593-8127Katie DeBartoloAccountant, Corporate Finance416-593-2166Alberta Securities CommissionKari HornGeneral Counsel403-297-4698Alison TrollopeDirector, Communications & Investor Education403-297-2664Cheryl McGillivrayManager, Corporate Finance403-297-3307Financial and Consumer Affairs Authority of SaskatchewanTony HerdzikDeputy Director, Corporate Finance / Securities306-787-5849The Manitoba Securities CommissionWayne BridgemanDeputy Director, Corporate FinanceSecurities Division204-945-4905Toll-free: 1-800-655-5244 (MB only)Autorité des marchés financiersMartin LatulippeDirector, Continuous Disclosure514-395-0337, ext. 4331Toll-free: 1-877-525-0337, ext. 4331Nadine GamelinSenior Analyst, Continuous Disclosure514-395-0337, ext. 4417Toll-free: 1-877-525-0337, ext. 4417Diana D'AmataSenior Regulatory Advisor, Continuous Disclosure514 395-0337, ext. 4386Toll-free: 1-877-525-0337, ext. 4386Financial and Consumer Services Commission (New Brunswick)Ella-Jane LoomisSenior Legal Counsel, Securities506-658-2602Nova Scotia Securities CommissionHeidi SchedlerSenior Enforcement Counsel902-424-7810Toll-free: 1-855-424-2499

{1} The Alberta Securities Commission did not participate in the 2015 and 2016 reviews as the WB/EP Rules had not yet been adopted in Alberta. The British Columbia Securities Commission has not adopted the WB/EP Rules. However, Alberta-based and BC-based TSX-listed issuers were included in the respective samples.

{3} On December 31, 2014, the Participating Jurisdictions excluded the Alberta Securities Commission. The Alberta Securities Commission subsequently adopted the WB/EP Rules effective December 31, 2016.

{4} Issuers excluded from our review included: (i) approximately 650 exchange-traded funds or closed-end funds; (ii) issuers that moved the listing of their securities from the TSX Venture Exchange (TSX-V) to the TSX in 2017; and (iii) other issuers such as designated foreign issuers and SEC foreign issuers that are exempt from the requirements of NI 58-101.

{5} This approach is consistent with our Year 2 and Year 1 reviews.

{6} The six largest banks had an average of 35% of women on their boards based on their 2017 information circulars filed for their years ending October 31, 2016.

{7} Refer to Appendix A (Item 15 of Form 58-101F1).

{8} If an issuer discloses the number, but not the percentage, of its executive officers who are women, investors may not be able to readily determine the proportion of women in executive officer positions as the total number of the issuer's executive officers may not be disclosed.

{9} Based on 722 issuers in 2015, 677 issuers in 2016 and 660 issuers in 2017.

{10} Based on 613 issuers that we reviewed in Year 2.

{11} Based on 649 issuers that we reviewed in Year 1.

{12} Based on 598 issuers that provided the number of women in executive officer positions in 2015, 613 issuers in 2016, and 614 in 2017.

{13} Refer to Appendix A (Item 11 of Form 58-101F1).

{14} A qualitative assessment of the disclosure was not the focus of this review for all Participating Jurisdictions.

{15} While it was unclear from the disclosure whether the policies for a small number of these issuers were in written form, we have assumed this to be the case for the purposes of our review.

{16} The policy results in this figure are based on 232 issuers that had adopted a policy in 2017, 141 issuers in 2016 and 111 issuers in 2015.

{17} Refer to Appendix A (Item 14 of Form 58-101F1).

{18} A qualitative assessment of the disclosure was not the focus of this review for all Participating Jurisdictions.

{19} Refer to Appendix A (Item 12 of Form 58-101F1).

{20} Refer to Appendix A (Item 13 of Form 58-101F1).

{21} A qualitative assessment of the disclosure was not the focus of this review for all Participating Jurisdictions.

{22} Refer to Appendix A (Item 10 of Form 58-101F1).

{23} A qualitative assessment of the disclosure was not the focus of this review for all Participating Jurisdictions.

Appendix A: Summary of Form 58-101F1 Corporate Governance Disclosure related to the WB/EP Rules

|

Item 10. Director Term Limits and Other Mechanisms of Board Renewal |

Disclose whether or not the issuer has adopted term limits for the directors on its board or other mechanisms of board renewal and, if so, include a description of those director term limits or other mechanisms of board renewal. If the issuer has not adopted director term limits or other mechanisms of board renewal, disclose why it has not done so. |

|

|

|

||

|

Item 11. Policies Regarding the Representation of Women on the Board |

(a) Disclose whether the issuer has adopted a written policy relating to the identification and nomination of women directors. If the issuer has not adoptedsuch a policy, disclose why it has not done so. |

|

|

|

(b) If an issuer has adopted a policy referred to in (a), disclose the following in respect of the policy: |

|

|

|

|

(i) a short summary of its objectives and key provisions, |

|

|

|

(ii) the measures taken to ensure that the policy has been effectively implemented, |

|

|

|

(iii) annual and cumulative progress by the issuer in achieving the objectives of the policy, and |

|

|

|

(iv) whether and, if so, how the board or its nominating committee measures the effectiveness of the policy. |

|

|

||

|

Item 12. Consideration of the Representation of Women in the Director Identification and Selection Process |

Disclose whether and, if so, how the board or nominating committee considers the level of representation of women on the board in identifying and nominating candidates for election or reelection to the board. If the issuer does not consider the level of representation of women on the board in identifying and nominating candidates for election or re-election to the board, disclose the issuer's reasons for not doing so. |

|

|

|

||

|

Item 13. Consideration Given to the Representation of Women in Executive Officer Appointments |

Disclose whether and, if so, how the issuer considers the level of representation of women in executive officer positions when making executive officer appointments. If the issuer does not consider the level of representation of women in executive officer positions when making executive officer appointments, disclose the issuer's reasons for not doing so. |

|

|

|

||

|

Item 14. Issuer's Targets Regarding the Representation of Women on the Board and in Executive Officer Positions |

(a) For purposes of this Item, a "target" means a number or percentage, or a range of numbers or percentages, adopted by the issuer of women on the issuer's board or in executive officer positions of the issuer by a specific date. |

|

|

|

(b) Disclose whether the issuer has adopted a target regarding women on the issuer's board. If the issuer has not adopted a target, disclose why it has not done so. |

|

|

|

(c) Disclose whether the issuer has adopted a target regarding women in executive officer positions of the issuer. If the issuer has not adopted a target, disclose why it has not done so. |

|

|

|

(d) If the issuer has adopted a target referred to in either (b) or (c), disclose: |

|

|

|

|

(i) the target, and |

|

|

|

(ii) the annual and cumulative progress of the issuer in achieving the target. |

|

|

||

|

Item 15. Number of Women on the Board and in Executive Officer Positions |

(a) Disclose the number and proportion (in percentage terms) of directors on the issuer's board who are women. |

|

|

|

(b) Disclose the number and proportion (in percentage terms) of executive officers of the issuer, including all major subsidiaries of the issuer, who are women. |

|