Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

OSC Staff Notice: 51-722 - Report on a Review of Mining Issuers’ Management’s Discussion and Analysis and Guidance

OSC Staff Notice: 51-722 - Report on a Review of Mining Issuers’ Management’s Discussion and Analysis and Guidance

OSC Staff Notice 51-722

Report on a Review of Mining Issuers' Management's Discussion and Analysis and Guidance

Publication date: February 6, 2014

Part A -- Staff's Review of MD&A in the Mining Industry

1. EXECUTIVE SUMMARY

Management's Discussion and Analysis (MD&A) is a key disclosure document for all reporting issuers as it gives investors the ability to look at an issuer through the eyes of management. The MD&A must be transparent and clear to be informative.

The MD&A requirements are set out in National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102), specifically in Part 5 Management's Discussion and Analysis and in Form 51-102F1 Management's Discussion and Analysis (Form 51-102F1).

As a securities regulator, the Ontario Securities Commission (OSC) understands the challenges faced by small mining issuers in today's challenging market environment. Limited resources can make it difficult for small mining issuers to meet their regulatory obligations and comply with their reporting requirements.

Recognizing these challenges and the importance of smaller mining issuers in Ontario, staff of the OSC conducted a review (the Review) of the MD&A filed by mining issuers with a market capitalization of less than $100 million in an effort to understand the issues they face and to identify areas where regulatory guidance would assist the management of these companies in complying with their regulatory obligations. These issuers represent approximately 34% of the 1,105 reporting issuers for which the OSC is the principal regulator.

While the guidance provided in the Notice is specific to the mining issuers reviewed, the content of the Notice, including our disclosure examples, will benefit all issuers.

OSC Staff Notice 51-722 Report on a Review of Mining Issuers' Management's Discussion and Analysis and Guidance (the Notice):

• is meant to be an educational tool to assist issuers in complying with their MD&A disclosure obligations

• summarizes the results of the Review

• identifies areas for improvement

• provides concrete examples on how issuers can present their information in a relevant and meaningful manner

Our review focused on:

• venture issuer disclosure

• discussion of operations

• liquidity and capital resources disclosure

• disclosure of transactions between related parties

• disclosure of risk factors and uncertainties

• reporting on use of financing proceeds

SUMMARY OF RESULTS

- - - - - - - - - - - - - - - - - - - -

We identified specific areas for improvement:

• venture issuers without significant revenue from operations did not provide the breakdown of material components of exploration and evaluation (E&E) assets or expenditures

• issuers with exploration projects did not discuss and itemize their exploration expenditures

• issuers with a working capital deficiency provided very general discussion or no discussion about potential sources of financing and how they plan on continuing operations

• issuers did not appropriately disclose the identity of the party involved in the related party transaction

- - - - - - - - - - - - - - - - - - - -

2. INTRODUCTION

The MD&A is a summary written through the eyes of management which allows management to provide insights beyond the numbers found in the financial statements. As such, the MD&A should:

• provide a balanced discussion of an issuer's results, financial condition and future prospects -- openly discussing bad news as well as good news

• help current and prospective investors understand what is presented in the financial statements

• discuss trends and risks that have affected or are reasonably likely to affect the financial statements in the future

• provide information about the quality and potential variability of an issuer's earnings, cash flow and operations

The current market environment is making it very difficult for mining issuers to raise capital, with the smaller mining issuers being particularly affected. We also understand such an environment can make complying with reporting requirements quite challenging for smaller issuers due to the lack of resources. To assist smaller mining issuers to better understand certain MD&A requirements and to foster regulatory compliance we have developed the guidance and examples found in Part B -- Guide to MD&A Disclosure for Mining Issuers (Part B). We hope these examples will assist issuers to present clear, specific and relevant information about their financial condition and future prospects.

3. REVIEW RESULTS

A. Scope of Review

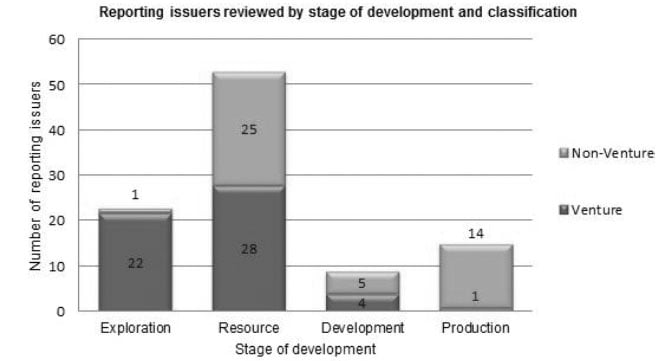

The OSC is the principal regulator for approximately 449 reporting issuers in the mining industry{1}, which is a very important sector in the capital markets in Ontario. These issuers have a combined market capitalization of $90.2{1} billion, representing 11% of Ontario's overall market capitalization. There are 374 Ontario mining issuers with a market capitalization of less than $100 million. In our ongoing compliance efforts, we have realized that many smaller mining issuers continue to struggle to provide complete and meaningful MD&A disclosure and generally need more guidance.

To understand the issues, we focused the Review on a sample of 100 Ontario mining issuers with a market capitalization of less than $100 million and focused on compliance with various aspects of the MD&A requirements in NI 51-102, including:

• venture issuer disclosure

• discussion of operations

• liquidity and capital resources disclosure

• disclosure of transactions between related parties

• disclosure of risk factors and uncertainties

• reporting on use of financing proceeds

B. Issuers Reviewed

Of the 100 Ontario mining issuers we reviewed, approximately 46% were non-venture issuers{2} and 54% were venture issuers{2}. Fifty-four percent of the issuers had a market capitalization of less than $25 million, with 28% having a market capitalization of less than $10 million. In terms of stage of development, the majority of issuers, 53%, were at the mineral resource stage, 23% were at the exploration stage and 24% were at the development or production stage.

C. Summary of Results

General

We found that many smaller mining issuers continue to struggle to provide complete and meaningful MD&A disclosure. The size of an issuer (as defined by market capitalization) was not a predictive factor as to whether an issuer met MD&A disclosure requirements. However, we note that issuers in the exploration stage generally need more guidance on appropriate entity-specific disclosure to be included in their MD&A than issuers in the development and production stages.

Venture Issuer Disclosure

Providing a breakdown of the material components of E&E, a presentation of E&E assets or expenditures on a property-by-property basis, general and administrative (G&A) expenses and other material costs incurred, helps investors understand the nature of the work being performed, how money is being spent and helps them evaluate the impact the expenses have in moving the exploration or developments of properties forward.

For venture issuers without significant revenue from operations, our Review found:

• 37% did not provide the breakdown of material components of E&E

• 20% presented the E&E on a property-by-property basis in their MD&A but failed to provide a further breakdown by material components

• 39% did not include a breakdown of material components of G&A expenses

Discussion of Operations

Issuers without producing mines - Beyond just the description of a project, it is important that investors receive essential information about an issuer's material mineral projects: work completed and expenses incurred during the period, current (and future) project plans and budgets. Providing this information will help investors follow and understand the progress of a project and measure how it is performing. It will also help investors connect the dots between initial plans and budgets and the time and costs required to take the project to the next stage.

Issuers with producing mines - The MD&A may be the principal document to inform shareholders and potential investors about the production and operations of a project. It is important that in the MD&A, issuers provide information on: production figures, production activities and milestones, operating and production costs, sales and revenue, explanations of any substantial changes to production and operation information, new developments and the impact each of these have on mineral resources and reserves.

Our Review found that:

• 70% of issuers without a producing mine provided limited disclosure about the plans or milestones for significant exploration and development projects, including anticipated costs to take the projects to the next stage of the project plan

• 44% of issuers with exploration projects did not discuss and itemize their exploration expenditures

Liquidity and Capital Resources

To better assess whether an issuer has sufficient funds to meet its business plans in the short-term and long-term, investors require meaningful information about an issuer's liquidity and ability to generate the cash needed to maintain operations. The MD&A provides an issuer with the opportunity to provide insight beyond the numbers and discuss material cash requirements, historical sources and uses of cash, material trends and uncertainties, and to explain and quantify working capital needs and how these needs relate to future business plans or milestones.

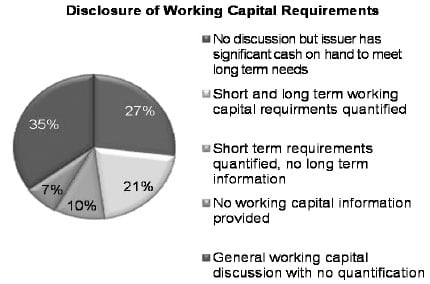

Of the 100 mining issuers reviewed:

• 27% clearly had significant current cash resources to meet their business needs

• 21% included a quantified discussion of how they intend to address in the short and long term their working capital requirements

• 52% provided either no disclosure or limited disclosure of their working capital requirements. This makes it difficult for a reader to assess whether the issuer has sufficient funds available to meet the issuer's business needs for the following 12 months

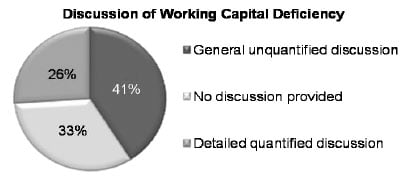

For issuers with a working capital deficiency:

• 26% included a detailed quantified plan of how they will meet their obligations as they come due and how they plan to rectify the deficiency

• 74% provided no discussion or a very general discussion about needing to access the capital markets in the future

Transactions Between Related Parties

Related party transactions (RPT) often play a significant role in the operations of businesses as they grow and can vary in complexity. We are aware that many smaller issuers leverage their business relationships to advance their projects in a cost controlled fashion by entering into related party contracts or transactions. It is critical that issuers are transparent to their shareholders about these transactions in the MD&A, so investors can better understand the business purpose and value of these transactions.

We note that:

• 95% of the issuers had some form of RPT disclosed in both their financial statements and their MD&A

• 48% of the issuers did not appropriately disclose the identity of the related party involved in the transaction. Most commonly, the relationship was disclosed but the actual party involved in the transaction was not named

• 14% of the issuers reviewed did not quantify the RPT

Risk Factors and Uncertainties

Company risks can impact an investor's investment decision, so it is important that issuers provide specifics about the risks impacting an issuer's business. Where possible, issuers should quantify the risks and when listing or ranking potential risks, be clear about their severity and significance. To make the information more meaningful, issuers should update their risk disclosures when circumstances change.

All issuers reviewed included some form of risk disclosure.

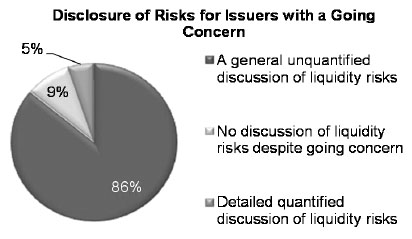

For issuers with a going concern risk:

• 9% provided no discussion of their liquidity risks despite having going concern issues

• 86% provided a generic, unquantified discussion of liquidity risks

Use of Financing Proceeds

Our Review identified only four issuers that raised capital through a prospectus offering in the past fiscal year:

• two issuers included a tabular comparison without any explanations of the changes

• two issuers did not include any disclosure relating to how the proceeds were used

SUMMARY

- - - - - - - - - - - - - - - - - - - -

As a result of our Review, we identified specific areas where our issuers would benefit from some additional guidance. Using the guidance in Part B will assist issuers in preparing their MD&A. An accurate MD&A and a complete continuous disclosure (CD) record will help ensure the process for obtaining a prospectus receipt is not delayed. We will continue to monitor MD&A filed by Ontario mining issuers as part of our ongoing CD review program.

- - - - - - - - - - - - - - - - - - - -

Part B -- Guide to MD&A Disclosure for Mining Issuers

1. MD&A GUIDANCE FOR MINING ISSUERS

To assist mining issuers in complying with the disclosure requirements in both NI 51-102 and Form 51-102F1, we have set out guidance for the sections where we noted areas where disclosure could be improved. When referring to this guidance be aware that you do not need to disclose information that is not material or not relevant to your business. While the guidance in section A Venture Issuer Disclosure applies specifically to venture issuers, non-venture issuers may find the information useful in preparing their MD&A. The examples provided below are for illustrative purposes only and readers are reminded that these examples are only one of many possible approaches management could take to present the information. Management must consider the particular elements of the issuer's business and ensure that all material information relating to the business is reflected in the MD&A.

A. Venture Issuer Disclosure

Disclosure requirement

Section 5.3 of NI 51-102 requires a venture issuer that has not had significant revenue from operations in either of its last two financial years to disclose in its MD&A on a comparative basis, a breakdown of material components of:

• E&E assets or expenditures

• G&A expenses

• other material costs

Further, the E&E assets or expenditures must be presented on a property-by-property basis.

Commentary

A breakdown of costs incurred helps investors understand the nature of the work that was performed and how an issuer is spending money. Further, a presentation of E&E assets or expenditures on a property-by-property basis helps investors evaluate the impact those expenditures have in moving the exploration or development of those properties forward.

Many issuers included disclosure similar to Example 1.

Example 1 -- boilerplate disclosure

|

|

Property A |

Property B |

Other |

Total |

|

|

||||

|

Balance, as at December 31, 2011 |

$3,300,000 |

$1,075,000 |

$200,000 |

$4,575,000 |

|

|

||||

|

Additions |

1,812,910 |

180,620 |

36,520 |

2,030,050 |

|

|

||||

|

Impairments |

- |

- |

(35,000) |

(35,000) |

|

|

||||

|

Balance, as at December 31, 2012 |

5,112,910 |

1,255,620 |

201,520 |

6,570,050 |

|

|

||||

|

Additions |

825.220 |

469,840 |

46,120 |

1,341,180 |

|

|

||||

|

Impairments |

- |

(1,725,460) |

- |

(1,725,460) |

|

|

||||

|

Balance, as at December 31, 2013 |

$5,938,130 |

- |

$247,640 |

$6,185,770 |

Example 1 is an example of disclosure frequently found during our Review where the issuer disclosed its exploration expenditures on a property-by-property basis without giving a breakdown by material components. While an investor will get a sense as to which property or project the issuer has moved forward, the fact that $825,220 was expended on property A during the year ended December 31, 2013 does not allow an investor to understand where and how the money was spent.

Examples 2a and 2b illustrate how an issuer can meet the requirements under section 5.3 of NI 51-102. These are detailed examples. Each issuer should assess the particulars of their business as the level of detail in these examples may not be material to every business.

Example 2a -- entity-specific disclosure (E&E capitalized)

|

|

Property A |

Property B |

Other |

Total |

Total |

||||

|

|

|||||||||

|

|

December 31, 2013 |

December 31, 2012 |

December 31, 2013 |

December 31, 2012 |

December 31, 2013 |

December 31, 2012 |

December 31, 2013 |

December 31, 2012 |

|

|

|

|||||||||

|

Acquisition costs |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

|

|

|

|||||||||

|

Balance, beginning of period |

300,000 |

300,000 |

80,000 |

75,000 |

65,000 |

75,000 |

445,000 |

450,000 |

|

|

|

|||||||||

|

Incurred during period |

50,000 |

- |

- |

5,000 |

15,000 |

- |

65,000 |

5,000 |

|

|

|

|||||||||

|

Mineral properties abandoned |

- |

- |

(80,000) |

- |

- |

(10,000) |

(80,000) |

(10,000) |

|

|

|

|||||||||

|

Balance, endof period of period |

350,000 |

300,000 |

- |

80,000 |

80,000 |

65,000 |

430,000 |

445,000 |

|

|

|

|||||||||

|

Exploration Expenditures |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

|

|

|

|||||||||

|

Balance, beginning of period |

4,812,910 |

3,000,000 |

1,175,620 |

1,000,000 |

136,520 |

125,000 |

6,125,053 |

4,125,000 |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Assays and geochemistry |

41,050 |

145,730 |

27,390 |

- |

5,880 |

2,990 |

74,320 |

148,720 |

|

|

|

|||||||||

|

Camp costs |

25,550 |

57,400 |

5,410 |

- |

- |

- |

30,960 |

57,400 |

|

|

|

|||||||||

|

Consulting |

15,490 |

6,400 |

7,650 |

28,880 |

- |

13,680 |

23,140 |

48,960 |

|

|

|

|||||||||

|

Drilling |

466,820 |

1,248,500 |

330,390 |

- |

- |

- |

797,210 |

1,248,500 |

|

|

|

|||||||||

|

Geology |

38,690 |

19,400 |

17,420 |

- |

12,770 |

6,750 |

68,880 |

26,150 |

|

|

|

|||||||||

|

Geophysics |

25,990 |

42,200 |

- |

92,480 |

- |

- |

25,990 |

134,680 |

|

|

|

|||||||||

|

Travel and lodging |

77,260 |

124,880 |

36,120 |

21,660 |

4,990 |

9,600 |

118,370 |

156,140 |

|

|

|

|||||||||

|

Salaries and labour |

84,370 |

168,400 |

45,460 |

32,600 |

7,480 |

3,500 |

137,310 |

204,500 |

|

|

|

|||||||||

|

Total exploration expenditures |

775,220 |

1,812,910 |

469,840 |

175,620 |

31,120 |

36,520 |

1,276,180 |

2,025,050 |

|

|

|

|||||||||

|

Mineral properties abandoned |

- |

- |

(1,645,460) |

- |

- |

(25,000) |

(1,645,460) |

(25,000) |

|

|

|

|||||||||

|

Balance, end of period |

5,588,130 |

4,812,910 |

- |

1,175,620 |

167,640 |

136,520 |

5,755,770 |

6,125,053 |

|

|

|

|||||||||

|

Cumulative mineral property costs |

5,938,130 |

5,112,910 |

- |

1,255,620 |

247,640 |

201,520 |

6,185,770 |

6,570,050 |

|

Example 2a shows that the issuer has disclosed its E&E expenditures by material components and has provided the information for both of its material properties. The issuer has aggregated E&E for other non-material projects / properties in a separate column under "Other". The disclosure is also provided on a comparative basis. While the requirements in section 5.3 of NI 51-102 do not specifically require a qualitative discussion of the expenditures, staff is of the view that a discussion of the issuer's E&E assets or expenditures and G&A expenses should be included as part of the issuer's analysis of its operations under item 1.4 of Form 51-102F1. For example, we would expect a qualitative discussion on the increase in E&E on Property B in the year ended December 31, 2013, including drilling results and reasons supporting the decision to abandon the property. We would also expect a qualitative discussion about E&E on Property A decreasing during the year ended December 31, 2013 (e.g. the issuer is focusing on its main property due to budget constraints).

The information included in example 2a discloses "cumulative property costs" which allows an investor to reconcile the information included in the MD&A and the amount shown on the face of the statement of financial position under "property costs".

Example 2a assumes that the issuer's accounting policy is to capitalize E&E expenditures. Example 2b illustrates how an issuer that expenses its expenditures would present the information.

Example 2b -- entity-specific disclosure (E&E expensed)

|

|

Property A |

Property B |

Other |

Total |

Total |

||||

|

|

|||||||||

|

|

December 31, 2013 |

December 31, 2012 |

December 31, 2013 |

December 31, 2012 |

December 31, 2013 |

December 31, 2012 |

December 31, 2013 |

December 31, 2012 |

|

|

|

|||||||||

|

Exploration Expenditures |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

_____ |

|

|

|

|||||||||

|

Assays and geochemistry |

41,050 |

145,730 |

27,390 |

- |

5,880 |

2,990 |

74,320 |

148,720 |

|

|

|

|||||||||

|

Camp costs |

25,550 |

57,400 |

5,410 |

- |

- |

- |

30,960 |

57,400 |

|

|

|

|||||||||

|

Consulting |

15,490 |

6,400 |

7,650 |

28,880 |

- |

13,680 |

23,140 |

48,960 |

|

|

|

|||||||||

|

Drilling |

466,820 |

1,248,500 |

330,390 |

- |

- |

- |

797,210 |

1,248,500 |

|

|

|

|||||||||

|

Geology |

38,690 |

19,400 |

17,420 |

- |

12,770 |

6,750 |

68,880 |

26,150 |

|

|

|

|||||||||

|

Geophysics |

25,990 |

42,200 |

- |

92,480 |

- |

- |

25,990 |

134,680 |

|

|

|

|||||||||

|

Travel and lodging |

77,260 |

124,880 |

36,120 |

21,660 |

4,990 |

9,600 |

118,370 |

156,140 |

|

|

|

|||||||||

|

Salaries and labour |

84,370 |

168,400 |

45,460 |

32,600 |

7,480 |

3,500 |

137,310 |

204,500 |

|

|

|

|||||||||

|

Total exploration expenditures |

775,220 |

1,812,910 |

469,840 |

175,620 |

31,120 |

36,520 |

1,276,180 |

2,025,050 |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Cumulative E&E since inception |

5,588,130 |

4,812,910 |

- |

1,175,620 |

167,640 |

136,520 |

5,755,770 |

6,125,053 |

|

REMINDER

- - - - - - - - - - - - - - - - - - - -

Venture issuers without significant revenues must:

• disclose a breakdown of the material components of E&E assets or expenditures, G&A expenses, and other material costs on a comparative basis

• present E&E assets or expenditures on a property-by-property basis

• include a qualitative discussion of those expenditures

- - - - - - - - - - - - - - - - - - - -

B. Discussion of Operations -- Issuers without producing mines

Disclosure requirement

Item 1.4 of Form 51-102F1 requires issuers to analyze their operations for the most recently completed period. The nature of the discussion should vary depending on the maturity of an issuer's operations. For example, Item 1.4 (d) of Form 51-102F1 requires issuers that have significant projects that have not yet generated revenue to describe each project including (a) the issuer's plan for each of its significant projects, (b) the status of each project relative to that plan, (c) expenditures made and (d) how the expenditures made relate to anticipated timing and costs to take the project to the next stage of the project plan.

Commentary

The annual MD&A for a mining issuer that is not at the production stage should provide the investor with information essential to understanding the issuer's material mineral projects. This would be more important for a venture issuer who chooses not to file an Annual Information Form{3} (AIF), and for issuers with early-stage exploration projects that may not have yet filed a technical report{4} on their projects. In these circumstances, the annual MD&A may be the only continuous disclosure document where management can summarize the project for investors and the interim MD&A allows that information to be updated.

To meet the requirements under Item 1.4 (d) of Form 51-102F1, issuers must include disclosure about the following items, on a property-by-property basis:

• description of the project

• work completed and expenditures made during the period

• current status -- project plans and budgets

• explanation of how expenditures relate to anticipated timing and cost to take the project to the next stage of the project plan

We describe each of these items in further details on the following page.

- - - - - - - - - - - - - - - - - - - -

Description of the project

• What are you looking for?

• Where are you looking?

- - - - - - - - - - - - - - - - - - - -

The project description in the annual MD&A should provide investors with enough information to follow progress on the project as reported by the issuer in subsequent disclosures such as interim MD&A and news releases. That description should include the following information:

• location of the property

• property ownership, and the issuer's ongoing obligations to maintain its interest

• type of commodities

• geological setting -- a brief description of the geology and known mineral occurrences

• exploration work to date -- the work done and a summary of significant results

• any mineral resources or mineral reserves outlined on the property

• information required by Part 3 of National Instrument 43-101 Standards of Disclosure for Mineral Properties (NI 43-101). If this information is summarized in the MD&A, it can be referred to in later filings to comply with disclosure requirements of NI 43-101 as per section 3.5 of NI 43-101

• name of the qualified person for the technical information

If the issuer has filed an AIF or technical report with this information, a reference to that filing should be included.

Issuers do not need to repeat the history of a project in every MD&A. We noted many instances where issuers were merely repeating the information previously disclosed in an earlier MD&A without including information about the current period. While issuers without a current AIF may want to include more historical information to provide background information about their projects, the majority of the discussion should focus on what happened in the current year or interim period.

- - - - - - - - - - - - - - - - - - - -

Work completed and expenditures made during the period

• What have you done?

• What did it cost you?

- - - - - - - - - - - - - - - - - - - -

In this section, the issuer should provide information on the progress of the project to date. Repeating information found in the financial statements without explaining significant changes does not provide meaningful insight to an investor.

We note nearly half of issuers reviewed did not provide an itemized breakdown of historical and current period exploration expenditures on a property-by-property basis. As discussed in Section A, venture issuers without significant revenue are required to include the disclosure in section 5.3 of NI 51-102. However, for non-venture issuers that have significant projects not yet generating revenue, an itemized breakdown helps investors understand how the issuer performed during the period covered by the MD&A.

In the absence of significant revenues, the disclosure of itemized expenditures will help an issuer:

• explain the operations of the issuer and describe where progress has been made on the different projects / properties

• identify important trends and risks that have affected the financial statements (e.g. changes in the amount or type of exploration expenditures)

• provide information about the potential variability of the issuer's profit or loss and cash flow

Further, staff believe that answering the following questions in the MD&A provides useful disclosure to investors:

• What new exploration work (e.g. geophysical or geochemical surveys, mapping, sampling, or drilling) has the issuer done on the project?

• How much was spent on the work completed and is the amount substantially different from budgets disclosed in previous filings and offering documents?

- - - - - - - - - - - - - - - - - - - -

Current status -- Project plans and budgets

• What did the work accomplish?

• What are you planning next?

• How will you pay for it?

- - - - - - - - - - - - - - - - - - - -

While issuers generally describe their significant projects and the work that has been completed during the period, MD&A would be improved by identifying how the accomplishments relate to the issuer's plans or next steps. For example:

• Is further work planned or has the issuer reached a decision on whether to advance the project further?

• What exploration or development milestones have been reached (for example, have all targets been tested or has a mineral resource been outlined)?

• Has the issuer met the requirements of an option or joint-venture agreement?

Issuers generally include some information about their plan for a significant project but the information is often vague and not meaningful. Issuers need to better explain the relationships or "connect the dots" between the current status of a project, their plan for the project, what they will spend on the project and when those expenditures will take place. This discussion is even more important when an issuer has liquidity or going concern issues so investors can understand the issuer's ability to meet cash requirements. The issuer must also discuss if sufficient resources are available to meet the projected capital commitments and, if not, disclose the expected source(s) of funds to meet those commitments. Further information on "liquidity and capital resources" can be found in Section D.

Investors are interested in understanding what the next phase of exploration or development is for the project by getting answers to questions such as:

• Is the issuer continuing to advance the project?

• Will the issuer be in a position to report a mineral resource estimate, and if so, when?

Example 3 is an example of disclosure commonly provided where an issuer fails to comply with the requirement. The disclosure is vague and lacks the details and quantification that would make it meaningful.

Example 3 -- boilerplate example

In 2013, the Company continued its exploration efforts on the XYZ Lake property including additional drilling on the Fire Zone which continued to intersect significant zone of mineralization. In addition, geophysical surveys identified several targets for testing which may represent zones of mineralization similar to the Fire Zone.

In 2014, the Company expects to continue its drilling efforts to outline the Fire Zone mineralization and also drill test the geophysical targets. The Company anticipates it will be in a position to disclose an initial mineral resource estimate on the XYZ Lake property in 2014.

The following example illustrates better disclosure on how issuers can discuss their plans and expected expenditures for their projects.

Example 4 -- entity-specific example

In 2013, the Company spent $873,100 on exploration expenses on the XYZ Lake property which consisted mainly of two phases of diamond drilling on the Fire Zone (totaling 25 holes for 4,820 metres) which were completed in February, 2013 and September, 2013. This drilling continued to outline significant zones of mineralization, the results of which were reported by the Company in news releases on May 30, 2013, June 24, 2013 and November 29, 2013. In addition, an airborne geophysical survey (703 line km) was completed in the summer which identified several targets for testing which may represent zones of mineralization similar to the Fire Zone.

In early 2014, the Company expects to spend approximately $800,000 conducting additional diamond drilling on the Fire Zone as well as follow-up drill testing of the high priority geophysical targets. It is expected that both drilling programs will consist of approximately 20 drill holes totaling about 5,000 metres. By the third quarter of 2014, the Company anticipates it will have completed a sufficient amount for drilling in order to commission an initial independent NI 43-101 mineral resource estimate on the Fire Zone which is expected to be disclosed by the end of 2014.

Example 5 is an example that provides limited information to investors.

Example 5 -- boilerplate example

Due to the challenging economic environment, the Company does not plan to spend any funds on the ABC property until market conditions improve.

Example 6 clarifies what was spent in the current year as well as the issuer's future plans. Depending on the circumstances, the disclosure does not always need to be extensive to meet the requirements.

Example 6 -- entity-specific example

In May, 2013 the Company spent $133,750 on exploration expenses related to the ABC property which consisted of an airborne geophysical survey (525 line km) to identify additional targets for drill testing. Four high priority targets were identified which may represent zones of mineralization similar to the Hill Zone discovered in the summer of 2012.

Due to the challenging economic environment, the Company does not plan to spend any additional funds on the ABC property until market conditions improve.

Example 7 illustrates how issuers can summarize and link the work completed on a specific project / property, the plans for that project / property, the status of the project relative to those plans and how the expenditures made relate to anticipated timing and costs to take the project to the next stage of the project plan.

Example 7 -- entity-specific example

|

Property |

Summary of Completed Activities (Jan 1, 2013 -- Dec 31, 2013) |

Expenditures (Year ended Dec 31, 2013) |

Plans for the Project for 2014 |

Planned Expenditures for 2014 |

||

|

|

||||||

|

A |

• |

January to March 2013 -- the Company completed 10 diamond drill holes (3,115 metres) testing for extensions of the Main Zone discovered in 2012. Five of these holes successfully intersected mineralization with similar gold grades and widths as observed in the Main Zone. These holes have traced the Main Zone for approximately 550 metres along strike and to a depth of 250 metres. One hole (A13-08) identified a new and potentially significant gold-bearing zone associated with a strong albite alteration. |

$ 775,220 (total for the year) |

• |

Conduct in-fill diamond drilling (approximately 15 holes totalling 4,500 metres) to provide sufficient data to support an initial NI 43-101 mineral resource estimate to be completed in Q3 or Q4 of 2014. |

$ 750,000 |

|

|

||||||

|

|

• |

Several of the 2013 drill holes were followed-up by downhole IP surveys which will be used to guide further exploration. |

|

|

|

|

|

|

||||||

|

|

• |

August 2013 -- additional geological mapping and structural analysis was undertaken to better understand the complex nature of the Main Zone mineralization. |

|

|

|

$ 30,000 |

|

|

||||||

|

|

• |

October to December 2013 -- the Company compiled and assessed the exploration results obtained over the previous two drilling campaigns (25 drill holes totalling 11,440 metres) along with the geological, structural and geophysical data to assist with planning the next phase of work. |

|

• |

Undertake initial metallurgical test work to determine potential gold recovery rates and processing method options. |

$ 70,000 |

|

|

||||||

|

|

|

|

|

• |

Initial mineral resource estimate and independent NI 43-101 technical report. |

|

|

|

||||||

|

B |

• |

June to September 2013 -- the Company completed 15 diamond drill holes (2,750 metres) testing the most significant anomalies identified during the 2012 airborne VTEM electromagnetic and magnetic survey. Two holes (B13-04 and B13-12) intersected weakly mineralized zones associated with quartz veining which returned values ranging from 1-2 g/t gold over 1.5 metres. Although a number of other drill holes intersected several significant zones of sulphide mineralization and associated alteration, the assay results for these zones were disappointing. |

$ 469,840 (total for the year) |

• |

No further work is planned on the property and management has decided to return the property to the vendor. |

- |

|

|

||||||

|

Other |

• |

Fall 2013 -- the Company completed several prospecting and soil geochemistry programs on non-material properties. |

$ 31,120 (total for the year) |

• |

Further work to be determined. |

- |

It is important to note that information included in the columns "Plans for the Project for 2014" and "Planned Expenditures for 2014" would be forward-looking information (FLI) subject to securities requirements.{5}

REMINDER

- - - - - - - - - - - - - - - - - - - -

Issuers with significant projects that have not yet generated revenue must disclose useful information for each material property or project that is not at the development or production stage including:

• description of the project

• work completed and expenditures made during the period

• current status of the project plans and budgets

• how expenditures relate to anticipated timing and cost to take the project to the next stage of the project plan

- - - - - - - - - - - - - - - - - - - -

C. Discussion of Operations -- Issuers with producing mines

Disclosure requirement

Item 1.4 of Form 51-102F1 requires issuers to analyze their operations for the most recently completed period. As mentioned in Section B, the discussion should vary with the stage of development of an issuer's operations.

Commentary

When a mining issuer has mineral properties in production, it is likely those properties are material to the issuer's affairs. The MD&A may be the principal document to inform shareholders and potential investors about production figures, operating costs, new developments and the impact each of these has on mineral resources and mineral reserves. In addition to the general information applicable to mineral exploration properties, issuers with mines in production should inform the reader about the production activities.

To meet the requirements under Item 1.4 (e) of Form 51-102F1, issuers must include useful disclosure about the following items, on a property-by-property basis:

• development and production milestones

• mineral resources and mineral reserves

• operating and production information

Each of these items is described in further detail below.

Development and Production Milestones

Item 1.4(e) of Form 51-102F1 requires an issuer to discuss development milestones, which could include any of the following:

• mineral resource or mineral reserve estimates

• results of pre-feasibility or feasibility studies

• exploration discoveries

• mineral resource or mineral reserve losses (for example, through ground failures)

• production decisions, expansion plans, or development of new resource zones

• expansions or changes to a processing plant

• name of the qualified person for the technical information

An issuer must also state whether there is a technical report supporting the disclosure of a mineral reserve, whether the technical report is the basis for any milestone and whether it forms the basis for a production decision. If the issuer has gone into production without a mineral reserve estimate based on at least a pre-feasibility study, the MD&A must disclose this information.

Mineral Resources and Mineral Reserves

Changes to a project's mineral resource base will usually be material information. In the MD&A, the issuer should:

• present the results of mine-area exploration programs and show their effect on mineral resource and mineral reserve estimates

• describe changes to mine plans, cut-off grades, process flow sheets, offtake or sales agreements or commodity prices, and their effect on mineral resource and mineral reserve estimates

Operating and Production Information

Both the annual and the interim MD&A should describe the results of operations including mine production, sales volume, and operating revenue. Some basic requirements for discussing an operating mine's results would include:

• mine production for the period

• mill throughput and head grades

• mill recovery and production of the mine's saleable commodities (for example, gold in doré or base metal in concentrate)

• operating cost, calculated using a recognized formula (e.g. all-in sustaining cash cost)

When production figures or operating costs change substantially from one interim period to the next or year to year, the MD&A should explain the reasons behind the change. The MD&A should describe:

• changes to mine plans, abandonment of uneconomic or inaccessible zones or accelerated production from parts of the mineral reserve

• development programs, particularly where those programs require the issuer to curtail production temporarily

• modifications to processes that affect production rates, mill throughput, head grade or recoveries

The MD&A should discuss the outlook for the operation for the forthcoming period (next year, in annual MD&A; next quarter, in interim MD&A):

• discuss any plans for significant capital expenditures, such as underground development, changes to plant capacity, or renewal of the mining fleet

• provide an outlook for expected production and operating costs

In example 8, the issuer does not include sufficient information to meet the requirements of item 1.4(e) of Form 51-102F1. While the issuer discloses the mine production for the period, the issuer does not state the gold grades, only that they improved, and does not explain why they changed. Further, there are no explanations about variances in production costs. We also note that the issuer does not explain the reasons leading to an impairment at Small Gold Mine. Finally, while the issuer includes an outlook, the information lacks sufficient details to be useful.

Example 8 -- boilerplate example

Main Gold Mine

Total ore mined in the quarter ended June 30, 2013 was 102,200 tonnes at improved gold grades compared to last quarter's figures due to improvements made at the end of 2012. These improvements reduced the cash cost per ounce{6} to US$1,088 in the current quarter and the Company sold its increased gold production at an average price of US$1,404. Operations continued to focus on the Upper Vein.

Small Gold Mine

Higher than expected costs at Small Gold Mine resulted in an impairment charge of $10,345,956.

Outlook to September 30, 2013

• Continue to explore and develop Main Gold Mine.

• Make improvements at Small Gold Mine.

• Obtain the required permits for other projects.

While example 9 is a simplified version of what an issuer would include in its MD&A, it illustrates how an issuer can provide meaningful information to investors by complying with the requirements. In this example, the issuer includes a comparative discussion of mine results with information about mine production for the period and reasons for the improvements, including figures for all-in sustaining cash costs. Operating decisions concerning Small Gold Mine are also described, including reasons leading to an impairment charge and its impact on the financial statements. Finally, plans for the issuer's two mines include specific information about what an investor can expect for the next interim period.

Example 9 -- entity-specific example

Main Gold Mine

Total ore mined in the quarter ended June 30, 2013 was 102,200 tonnes at 6.47 g/t gold. The tonnage and grade is 36% and 11% above last quarter's figures, respectively, driven by productivity improvements at the mine and at the mill. The increased mining rate is attributable to a larger mechanized mining fleet suitably fitted to the mining method and improved underground infrastructure. The mill attained an average daily production rate of 920 tonnes at 94% gold recovery with improved performance attributable to the mill expansion completed at the end of 2012 with installation of a ball mill with twice the previous capacity. These improvements contributed to a significant year-over-year reduction in all-in sustaining cost per ounce of US$1,088 in the current quarter from US$1,242 last year. The Main Gold Mine sold a total of 14,686 ounces of gold at an average price of US$1,404 in the quarter compared to gold sales of 12,109 ounces at an average price of US$1,612 in the comparable period last year. Total capital development of underground workings during the quarter is 422 meters. Operations are focusing on the continued development of the Upper Vein which was identified by drilling in early 2012.

Small Gold Mine

Higher than expected costs at Small Gold Mine, that are now forecast to continue, prompted management to assess indicators of impairment related to the project and its associated assets. Management used a discounted cash flow model to calculate the recoverable amount. This resulted in an impairment charge of $10,345,956 to Small Gold Mine and its associated assets with $2,846,000 allocated to property, plant and equipment, and $7,499,956 to deferred development expenditure. Management is implementing several cost cutting measures related to mining and personnel to address the higher costs.

Outlook to September 30, 2013

• Continue to explore and develop the Upper Vein at Main Gold Mine.

• Implement cost cutting measures at Small Gold Mine while continuing to review and assess its continued viability.

• Work with local and federal governments to obtain the required permits to advance the Company's other gold projects.

REMINDER

- - - - - - - - - - - - - - - - - - - -

Issuers with producing mines or mines under development must include useful disclosure on a property -by-property basis about:

• development and production milestones

• mineral resources and mineral reserves

• operating and production information

- - - - - - - - - - - - - - - - - - - -

D. Liquidity and Capital Resources

Disclosure requirement

The MD&A should include a meaningful discussion of an issuer's liquidity including its ability to generate sufficient amounts of cash in the short and long term to maintain its operations. Items 1.6 and 1.7 of Form 51-102F1 require an issuer to disclose, among other things:

• its ability to meet planned growth or fund development activities

• its working capital requirements

• its capital expenditures, including an analysis of expenditures not yet committed but required to meet planned growth or to fund development activities

If an issuer has or expects to have a working capital deficiency, the issuer must discuss its ability in both the short and long term to meet its obligations as they come due. The issuer must also discuss how it plans to remedy the working capital deficiency.

Commentary

Meaningful analysis in an issuer's MD&A of material cash requirements, historical sources and uses of cash as well as material trends and uncertainties is important so investors can understand the issuer's ability to generate cash and meet cash requirements. A good analysis of liquidity position involves a meaningful discussion of cash flows from operations, investing, and financing, beyond stating balances from the financial statements. In particular, a detailed liquidity discussion is especially important for smaller non-producing issuers given the constant demands for financing to meet project milestones. The disclosure should explain why management believes it has sufficient resources. Issuers can improve their discussion of working capital requirements by better explaining and quantifying their working capital needs and how their working capital needs relate to their plan for the next fiscal year or up to the next business milestone. Having working capital in excess of last year's expenditures is not sufficient for investors to understand why the issuer has sufficient financial resources if the plan/outlook isn't also disclosed.

Rather than repeating items that are reported in the statement of cash flows, an issuer should concentrate on disclosing the primary drivers of cash flows and the reasons for material changes in major sub-items underlying the line items reported in the financial statements. Issuers should also consider whether they need to provide enhanced disclosures about significant debt instruments, guarantees, and covenants.

Without providing further details, including quantification, example 10 does not allow an investor to assess whether or not the issuer's statement that it has sufficient liquidity to meet its current working capital requirements and fund its development activities is reasonable.

Example 10 -- boilerplate example

Management believes that the funds currently on hand are sufficient to meet the Company's short-term obligations.

Example 11 -- entity-specific example

The Company's working capital requirements for the past year are discussed in detail in the Discussion of Operations section. Fixed costs to maintain operations, pay taxes and royalties and upkeep are about $60,000 per annum. Corporate and general costs to maintain the requirements of a listed company have been about $95,000 in both 2013 and 2012. Therefore, minimum working capital requirements are estimated at $155,000 per year.

Estimated Working Capital Requirements 2014

|

Complete preliminary economic assessment (PEA) |

$ |

300,000 |

|

|

||

|

Corporate & general |

$ |

155,000 |

|

|

||

|

Convertible note repayment |

$ |

<<1,200,000>> |

|

|

||

|

Total |

$ |

1,655,000 |

As at December 31, 2013, the Company's cash and cash equivalents were $684,000. The Company has access to sufficient funds to meet its current overhead requirements. The Company also has sufficient cash to fund the PEA. The resulting PEA report will provide the basis of a decision to advance development, finance further exploration or consider other options. The Company does not currently have sufficient resources to repay the convertible notes in December 2014. The Company plans to complete an offering of new debt securities in the fall to fund the repayment.

Example 11 clearly illustrates the issuer's current financial position. Clear entity-specific disclosure is important so that investors can understand any anticipated funding shortfalls and financing resources available to meet spending commitments and continue key projects. It is important to focus on realistic solutions and providing an analysis that will let investors know how the issuer will carry on its business.

Disclosure is helpful, even when exploration has been put on hold. A complete discussion of the issuer's financial obligations and discretionary expenses helps an investor better understand how an issuer is meeting its obligations during a time when exploration is on hold. This is an opportunity for an issuer to explain to investors how it is controlling its costs, the minimum amount of funds it needs to get through the next period and how the issuer expects to finance it.

It is also important that the discussion in the liquidity section ties to the operating plan. In our Review, we noted instances where there was disclosure of a plan to spend significant amounts to develop a property. In some of these instances the liquidity section only discussed current working capital requirements which was inconsistent with the discussion of operations, and the plans to develop the property. The liquidity section should be a complete discussion including cash requirements for both operating and capital requirements planned for in the coming year. Obligations for payments with respect to flow through shares should also be included when discussing cash requirements. Example 12 shows how an issuer may want to provide an update of their obligations relating to flow-through shares.

Example 12 -- entity-specific example

In January, the Company issued $3.5 million of flow-through shares. In addition to the amounts disclosed in the contractual obligations table, the Company is committed to spend $3.5 million in Canadian exploration expenses. As of March 31 the Company had spent $0.7 million in Canadian exploration expenses, the remaining balance of $2.8 million must be spent by December 31, 2014.

When disclosing capital requirements it is important that all obligations are discussed so that investors can understand what is required for the issuer to continue operating its business. Many issuers simply provide the contractual obligations table required by item 1.6 of Form 51-102F1 but neglect to provide a discussion of these obligations.

REMINDER

- - - - - - - - - - - - - - - - - - - -

To be meaningful, the discussion of liquidity and capital resources must address in detail all future cash requirements of an operating and capital nature and how they will be funded. Simply disclosing that management believes it has sufficient resources to fund currently planned exploration or development is not sufficient.

- - - - - - - - - - - - - - - - - - - -

E. Transactions between Related Parties

Disclosure requirement

For issuers that enter into transactions between related parties, Item 1.9 of Form 51-102F1 requires the relationship be discussed and the related person or entity be identified in the MD&A. In addition to identifying the related party, the issuer must discuss the business purpose of the transaction, the recorded amount of the transaction and how it was measured. If there are any ongoing commitments related to the transaction, these must also be disclosed.

Commentary

RPTs often play a significant role in the operations of businesses as they grow. These transactions can vary from simple contracts for key management personnel to complex financing agreements. While RPTs may provide the issuer with benefits that are not available from other arms-length parties or to other issuers on the same terms, disclosure needs to insure there is transparency around these transactions so readers of the MD&A understand the business purpose of these transactions. In addition, the measurement basis used is important disclosure so the value of the transaction can be evaluated. Example 13 illustrates the type of RPT disclosure we frequently saw in our Review.

Example 13 -- boilerplate example

During the year, the Company paid $148,541 for services to a firm in which a director is a partner.

Example 13 lacks detail as it does not explain the services provided, how they were valued or the business reason for entering into the transaction. In addition, a reader cannot tell from this statement which director was involved in the RPT. It is not sufficient to disclose that "the Company paid for services to a firm related to one of the directors"; rather one must clearly identify the specific person or entity.

Example 14 shows how the disclosure in example 13 could be improved to meet the requirements in item 1.9 of Form 51-102F1. In example 14, the name of the related party is included, the business purpose of the transaction is discussed and how the transaction was valued is described.

Example 14 -- entity-specific example

During the year, the Company paid professional fees of $148,541 to Best Miner LLP, a law firm of which Joe Prospector, a director of the Board, is a partner. These services were incurred in the normal course of operations for general corporate matters, attendance at committee and board meetings, as well as evaluating business opportunities. All services were made on terms equivalent to those that prevail with arm's length transactions.

Example 15 is another instance of boilerplate disclosure relating to a RPT transaction.

Example 15 -- boilerplate example

During the year, the Company paid $200,000 of interest on a loan payable to a majority shareholder.

Example 16 shows both the business purpose and the amount of the transaction.

Example 16 -- entity-specific example

During the year, the Company paid $200,000 in interest on a loan of $2,000,000 received from the CEO, who is a majority shareholder. The unsecured loan bears interest at 10% per annum and matures in five years with an option by the Company to extinguish the debt at any time without penalty. The transaction was recorded in the Company's financial statements at the exchange amount. The Company entered into this related party transaction because alternate sources of financing were unavailable due to the Company's limited operating history, lack of collateral and limited access to public financing due to current global financial conditions.

For mining issuers, it is not uncommon for the acquisition of a property to come from a related party. Example 17 is an example of boilerplate disclosure relating to the acquisition of such a property.

Example 17 -- boilerplate example

In March 2013, the Company closed an acquisition of the Golden Mine property with Mr. Striker, a director of the Company. The company issued 500,000 shares to Mr. Striker for a 100% interest in the property, subject to a 1.5% net smelter return retained by Mr. Striker.

In addition to disclosing the nature and relationship of the related party, it is also important to disclose the business purpose of the transaction so that investors can evaluate these services and the business purpose of the related party transaction. The following example highlights how the issuer disclosed the purpose of the transaction.

Example 18 -- entity-specific example

In March 2013, the Company closed an acquisition of the Golden Mine property with Mr. Striker, a director of the Company. The transaction was approved by the board of directors with Mr. Striker abstaining from the vote. The Company issued 500,000 shares to Mr. Striker for a 100% interest in the property, subject to a 1.5% net smelter return retained by Mr. Striker. An independent valuation by ABC Consultants stated the transaction was within a range of fair values for a similar mineral property. The transaction gives the company a large land position near the Brilliant Mine discovery of DEF Minerals Limited.

REMINDER

- - - - - - - - - - - - - - - - - - - -

By virtue of their nature, transactions between related parties lack the independence inherent in arm's length transactions. Investors need to understand who are the specific parties involved, the business purpose and economic substance of RPTs, so they can understand the rationale for transactions and impact on the business.

- - - - - - - - - - - - - - - - - - - -

F. Risk Factors and Uncertainties

Disclosure requirement

To comply with item 1.4(g) of Form 51-102F1, the MD&A must include a discussion of risk factors and uncertainties the issuer believes will materially affect its future financial performance. This discussion should include entity specific information about risks that may affect or have affected the issuer and that would be most likely to influence an investor's decision to purchase its securities, risks that affect the issuer's financial statements or risks that are reasonably likely to affect them in the future. Where possible, the impact of the risk should be quantified.

Commentary

Investors need to understand the entity specific risks and how those risks may impact the issuer and its business, both of which may affect an investment decision or the value of its investment should the risks be realized. To avoid boilerplate disclosure, reporting issuers should be more specific on the potential consequences of risks to the company.

We noted that issuers often conclude an individual risk discussion by saying that if the risk was realized it "could have a material adverse impact on the Company", without stating what that specifically may be.

• Would it affect revenues, cash flows, costs?

• Would the impact potentially be isolated such that it could be managed swiftly or would it have a sweeping pervasive effect that could endanger the Company's solvency/viability, or would its effect lie somewhere in between?

• For how long can the issuer rely on existing sources of liquidity before additional financing is needed?

These risks should be quantified when possible.

When reviewing the MD&A, it is often difficult based on the disclosure provided to determine which are the most immediate or most serious risks to the issuer. The AIF requires issuers to disclose the risks in order of seriousness from the most serious to the least serious. Form 51-102F1 does not have a similar instruction but rather directs issuers to focus the MD&A on material information. We have found many issuers include a lengthy list of risks without any indication of the level of exposure or significance of the risks. When presented this way, key risk information may become lost amid less relevant information.

In addition to providing a detailed and quantified description of potential risks, to provide meaningful risk disclosures to investors, issuers should update their risk disclosures when circumstances change. It appears from our Review, that there is little to no updating of risk disclosures year over year or from annual to subsequent interim periods. Issuers should consider enhancing processes to monitor for changes in risks to ensure their disclosures are comprehensive and reflect current circumstances. A statement in the MD&A that the risks remain unchanged or a summary of the changes since the previous disclosures would help investors focus on new information. Issuers should also consider disclosing anticipated future changes in risk exposure.

Risk disclosure needs to be specific. As seen in the boilerplate example below, knowing that an issuer faces normal risks inherent to the mining industry does not inform investors of the issuer's specific operations.

Example 19 -- boilerplate example

The Company's operations are located in Foreign Country X. The company is subject to the political risks and economic considerations of operating in Foreign Country X.

Knowing the specific risks an issuer faces helps a reader of the MD&A understand and evaluate the risk. The disclosure in example 19 is boilerplate and could apply to many issuers operating in foreign countries. By contrast, the disclosure in example 20 shows how the impact of the foreign operations could specifically impact the issuer.

Example 20 -- entity-specific example

The Company's principal property is located in Region Y of Foreign Country X. Consequently, the Company is subject to certain risks associated with foreign ownership, including currency, inflation, political and property title risk. On January 13, 2013, a coup was initiated by members of the Region Y army, creating uncertainty within the area where the company operates. Currently, operations are continuing but travel and access to the property may be curtailed due to political instability or risks to personnel which may result in project delays. The Company is closely monitoring the situation and management will continue to provide updates.

REMINDER

- - - - - - - - - - - - - - - - - - - -

To be meaningful to investors, risk disclosure needs to be entity-specific and updated regularly.

- - - - - - - - - - - - - - - - - - - -

G. Use of Financing Proceeds

Disclosure requirement

Item 1.4(i) of Form 51-102F1 requires issuers that have raised capital in a prospectus offering to compare, in tabular form, any changes in the use of proceeds and to explain the impact of the changes on the issuer's ability to achieve its business objectives and milestones.

Commentary

In a prospectus offering an issuer must disclose the principle purposes for which the funds raised will be used. It is important that investors be updated on how the money raised has been spent as the funds raised for mining issuers are often earmarked for specific projects or stages of specific projects. This information allows investors to assess how an issuer is spending the proceeds raised in an offering document.

Answering the following questions in the MD&A provides useful disclosure to investors:

• How does the nature and amount of expenditures made by the issuer compare to the use of proceeds from previous financing?

• How do variances impact future operations?

• How will the variance affect the issuer's ability to achieve its business objective and milestones?

• Will the issuer require additional financing to meet its next milestone?

2. HOW TO AVOID BOILERPLATE DISCLOSURE

Good public disclosure and comprehensive MD&A will help investors understand your business and will assist issuers in complying with the requirements in NI 51-102 and Form 51-102F1. Considering the following questions may assist issuers in preparing a meaningful and useful MD&A.

Venture Issuer Disclosure

|

Areas |

Considerations |

||

|

|

|||

|

Additional disclosure for venture issuers without significant revenue |

• |

Is there a breakdown of material components of: |

|

|

|

|||

|

|

|

• |

E&E assets or expenditures? |

|

|

|||

|

|

|

• |

General and administrative expenses? |

|

|

|||

|

|

|

• |

Other material costs? |

|

|

|||

|

|

• |

Has the breakdown been provided for each of the last two financial years? |

|

|

|

|||

|

|

Note: Considered to be a material component of cost if the cost exceeds greater that 20% of total amount of class or $25,000 |

||

|

|

|||

|

Mining exploration and development issuers |

• |

Have E&E assets or expenditures been presented on a property-by-property basis? |

|

Discussion of Operations

|

Areas |

Considerations |

|||

|

|

||||

|

Exploration Projects |

• |

Has the following disclosure been made for each material project: |

||

|

|

||||

|

|

|

• |

A description of the project? |

|

|

|

||||

|

|

|

• |

Plans for the project? |

|

|

|

||||

|

|

|

• |

Status of the project relative to that plan? |

|

|

|

||||

|

|

|

• |

Expenditures made to date and how these relate to anticipated timing and costs to take the project to the next stage of the project plan? |

|

|

|

||||

|

Availability of capital resources |

• |

Are sufficient resources available to meet projected capital commitments? If not, is there disclosure about the expected source(s) of funds to meet those commitments? |

||

|

|

||||

|

|

|

Note: Refer to discussion on "liquidity and capital resources" |

||

|

|

||||

|

Variance in use of prospectus proceeds |

• |

If capital has been raised from a prospectus offering: |

||

|

|

||||

|

|

|

• |

Has any difference between the planned use of proceeds and their actual use, been explained? |

|

|

|

||||

|

|

|

• |

Has the issuer disclosed how these variances may impact the issuer's ability to take the project to the next stage of the project plan? |

|

|

|

||||

Liquidity and Capital Resources

|

Areas |

Considerations |

|||

|

|

||||

|

Ability to generate sufficient cash |

• |

Has the issuer analyzed its ability to generate sufficient cash, in the short term and the long term to: |

||

|

|

||||

|

|

|

|

• |

Address working capital requirements? |

|

|

||||

|

|

|

|

• |

Maintain properties and agreements in good standing? |

|

|

||||

|

|

|

|

• |

Meet spending commitments? |

|

|

||||

|

|

|

|

• |

Finance new opportunities? |

|

|

||||

|

Working capital requirements |

• |

Are the issuer's working capital requirements disclosed? |

||

|

|

||||

|

|

• |

If a working capital deficiency exists, or is expected, has the issuer discussed and analyzed its: |

||

|

|

||||

|

|

|

|

• |

Ability to meet obligations as they become due? |

|

|

||||

|

|

|

|

• |

Plans, if any, to remedy the deficiency? |

|

|

||||

|

Spending requirements |

• |

Is there disclosure and analysis about: |

||

|

|

||||

|

|

|

|

• |

Exploration and development expenditures required to maintain properties or agreements in good standing? |

|

|

||||

|

|

|

|

• |

Amount, nature and purpose of commitments? |

|

|

||||

|

|

|

|

• |

Expenditures that are not yet committed but are required to maintain the issuer's capacity or finance new opportunities? |

|

|

||||

|

Sources of financing |

• |

Have the expected sources of financing been identified? |

||

|

|

||||

|

|

• |

Has the issuer discussed known trends or expected fluctuations in capital resources, including changes in mix and relative cost of resources? |

||

|

|

||||

|

|

• |

Has the issuer discussed how difficulties in obtaining financing could affect the issuer including status of projects, financing operations and ability to continue as going concern? |

||

Transactions between Related Parties

|

Areas |

Considerations |

|||

|

|

||||

|

Disclosure of all RPTs |

• |

Are all transactions between related parties disclosed and discussed? |

||

|

|

||||

|

Identity and relationship of related party |

• |

Is there disclosure of: |

||

|

|

||||

|

|

|

|

• |

The name of the related party (not only the related party's position or relationship with the issuer)? |

|

|

||||

|

|

|

|

• |

The name of ultimate beneficiaries of the RPT, where the transaction is conducted through a corporate entity? |

|

|

||||

|

|

|

|

• |

The relationship between the issuer and the related party? |

|

|

||||

|

Business purpose and economic substance of transaction |

• |

Are the reasons for entering into the RPTs disclosed and explained? |

||

|

|

||||

|

|

|

|

• |

Are the economic benefits to the issuer from each RPT disclosed and explained? |

|

|

||||

|

|

|

|

• |

Is there disclosure of the consideration that was paid? |

|

|

||||

|

|

|

|

• |

Is there an explanation as to why the issuer acquired assets or services from a related party as opposed to an arm's length party? |

|

|

||||

|

|

|

|

• |

Is the discussion quantified where possible? |

|

|

||||

|

|

Note: Avoid generic descriptions such as "consulting" or "for services performed" |

|||

|

|

||||

|

Recorded amount of transaction and measurement basis used |

• |

Is the recorded amount of the transaction and the measurement basis used disclosed? |

||

|

|

||||

|

Ongoing or contractual or other commitments |

• |

Is there disclosure and discussion of ongoing contractual or other commitments arising out of RPTs? |

||

|

|

||||

|

Processes and procedures for identifying, evaluating and approving RPTs |

• |

Is there a description of management and board processes and procedures for identifying, evaluating and approving RPTs? |

||

Risk Factors Disclosure

|

Areas |

Considerations |

|

|

|

||

|

MD&A disclosure |

• |

Is there a discussion of important trends and risks that have affected the issuer's financial statements? |

|

|

||

|

|

• |

Is there a discussion of trends and risks that are reasonably likely to affect the issuer's financial statements in the future? |

|

|

||

|

|

• |

Is there a discussion of commitments, events, risks or uncertainties that the issuer reasonably believes will materially affect its future performance? |

|

|

||

|

|

Note: An issuer should not provide a "laundry list" of every conceivable risk |

|

|

|

||

|

Suggested risk management practices |

• |

Does the board have a full understanding of the risks facing the issuer and how those relate to the overall risk appetite of the issuer? |

|

|

||

|

|

• |

Does the board take appropriate steps to stay informed of key developments that could increase the issuer's risk exposure? |

|

|

||

|

|

• |

Is there a strategy in place to ensure that significant risks are identified and managed by the board and management? |

Part C -- Conclusion

1. CONCLUSION