Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

CSA Staff Notice 43-309 - Review of Website Investor Presentations by Mining Issuers

CSA Staff Notice 43-309 - Review of Website Investor Presentations by Mining Issuers

CSA Staff Notice 43-309

Review of Website Investor Presentations by Mining Issuers

CSA Staff Notice 43-309 Review of Website Investor Presentations by Mining Issuers

April 9, 2015

1. Introduction

This notice summarizes the findings of a review (the Review) of investor presentations on mining issuers' websites, conducted by staff of the British Columbia Securities Commission (BCSC), the Ontario Securities Commission (OSC), and the Autorité des marchés financiers (AMF) (collectively, the Principal Mining Jurisdictions or we). We also provide practical information to assist mining issuers in designing investor presentations and websites that meet their disclosure obligations.

The Review assessed investor presentations' compliance with the requirements of National Instrument 43-101 Standards of Disclosure for Mineral Projects (NI 43-101). In addition, we reviewed the forward looking information (FLI) against the requirements of Part 4A of National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102).

We expect mining issuers to use this notice as a self-assessment tool to strengthen their compliance with securities laws, in particular NI 43-101 and FLI disclosure requirements.

2. Summary of Results

2.1 Key Findings

The results of our review highlight the need for mining issuers to improve their disclosure in order to comply with the following requirements of NI 43-101:

• Naming the qualified person (QP): review of technical information by a QP directly improves compliance with requirements

• Preliminary economic assessments (PEA): providing required cautionary statements ensures proper understanding of the PEA results' limitations

• Mineral resources and mineral reserves: a clear statement whether mineral resources include or exclude mineral reserves is essential to avoid misleading disclosure

• Exploration targets: potential quantity and grade must be expressed as a range and be accompanied by the required statements outlining the target limitations

• Historical estimates: disclosure must include source, date, reliability, key assumptions and be accompanied by the required cautionary statements.

2.2 Overall Assessment

In general we found there is room for improvement for mining issuers to comply with disclosure requirements.

Some issuers use terms and statements that could be interpreted as overly promotional or misleading, potentially resulting in a misrepresentation. Terms such as "world-class", "spectacular", "production ready", or "ore" may be used inappropriately in certain circumstances. Misuse of such terms was more commonly seen with exploration or mineral resource stage issuers.

Issuers at the mineral resource stage or earlier sometimes disclose anticipated economic outcomes for their mineral project such as production rate, capital and operating costs, or mine life suggesting that their project is at a more advanced stage of development than is supported by the existing technical report. Such disclosure may trigger the filing of a technical report to support the economic projections.

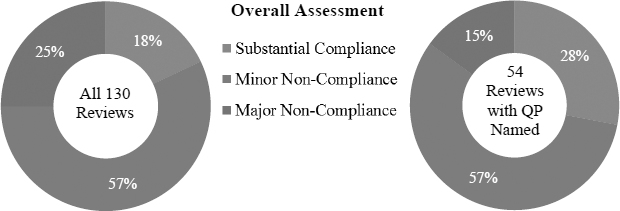

Based on an overall assessment of 130 investor presentations for compliance with NI 43-101 and FLI requirements, as well as whether the information was balanced and not overly promotional, we assigned a rating to each of the investor presentations as "substantial compliance", "minor non-compliance", or "major non-compliance".

Of the 130 investor presentations, 54 presentations provided the name of the QP that approved the disclosure, and stated that QP's relationship to the issuer, as required by section 3.1 of NI 43-101. Those 54 presentations were rated as having substantial compliance or minor non-compliance 85% of the time, a significant improvement over the full population of presentations.

As demonstrated in the following pie charts, the rating and overall compliance with NI 43-101 disclosure requirements increased significantly among investor presentations reviewed by a QP. We saw improvement in disclosure of exploration targets, mineral resources and mineral reserves, historical estimates and exploration information. No improvement was noted with disclosure of economic studies. Issuers are reminded of the requirement to name the QP responsible for approving the disclosure to ensure that the information complies with NI 43-101.

2.3 Actions Taken

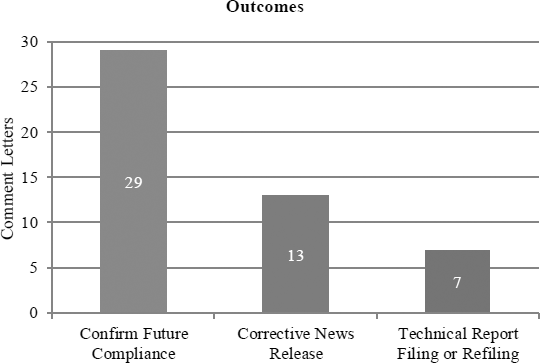

Of the 130 investor presentations reviewed, we sent letters to 49 mining issuers requiring them to amend their investor presentations and correct the non-compliant disclosure. As shown in the bar graph below, this resulted in a range of outcomes from mining issuers confirming future compliance with the requirements, to issuing a corrective news release, to filing or refiling a technical report.

The majority of the corrective news releases and technical report filings or refilings resulted from non-compliant disclosure of economic studies, PEAs, mineral resources, mineral reserves, exploration targets, historical estimates, or overly promotional language.

3. Purpose and Objective

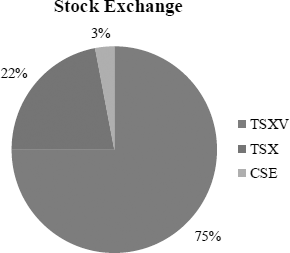

Mining issuers make up approximately 43% (1,600) of the total number of reporting issuers overseen by CSA jurisdictions{1}. Approximately 94% of all mining issuers listed on the Toronto Stock Exchange (TSX), TSX Venture Exchange (TSXV), and the Canadian Stock Exchange (CSE) are regulated by the BCSC, OSC or AMF which maintain a staff of specialized mining professionals to review disclosure by mining issuers based in their respective jurisdictions.

Investor presentations and other forms of investor relations materials contained on mining issuers' websites provide a powerful tool for communication. Information found on issuer websites is captured by the definition of "written disclosure" in NI 43-101 and disclosure requirements apply.

We often observe non-compliance with disclosure on mining issuers' websites such as investor presentations, fact sheets, media articles, and links to third party content. Our Review was intended to provide data and analysis to better understand the nature, extent and compliance of the disclosure in investor presentations in order to better assist mining issuers and their investor relations personnel to improve their disclosure to investors.

4. Profile of Issuers Reviewed

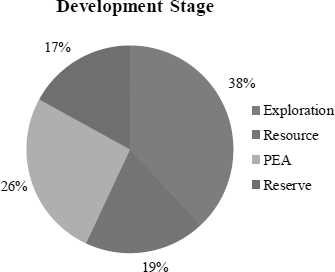

Approximately 88% of all mining issuers listed on the TSX, TSXV, and the CSE are at the pre-production stage. Our review focused on a sample of 130 mining issuers at the pre-production stage from the Principal Mining Jurisdictions with investor presentations dated between December 2013 and October 2014. The following pie charts provide details of the profile of the mining issuers reviewed in our sample including stock exchange listing, development stage, project location, and main commodity.

5. NI 43-101 Compliance

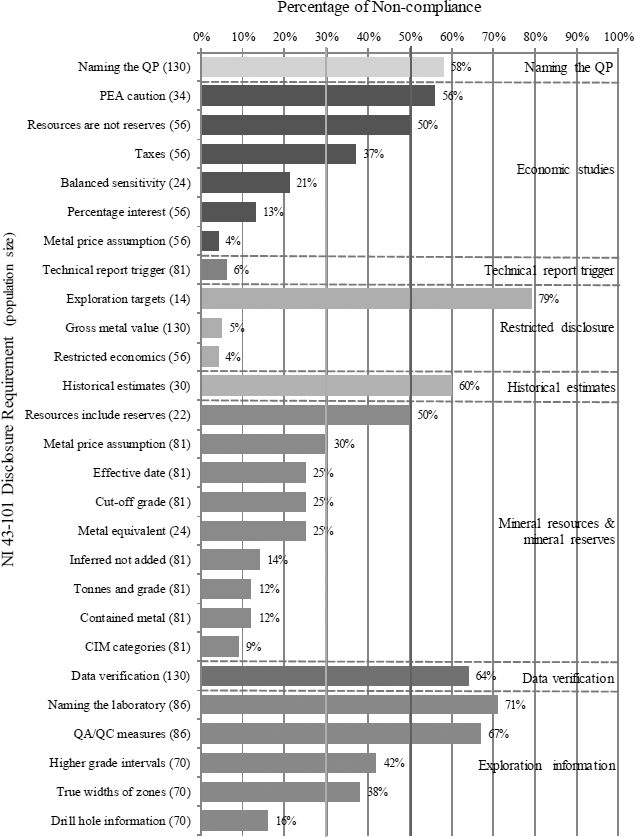

The results of our Review are presented according to the following thresholds of non-compliance: High Level of Non-Compliance (greater than 50% of investor presentations reviewed) and Areas for Additional Improvement (between 30% and 50% of investor presentations reviewed). When discussing the Review findings the number of investor presentations that included the particular disclosure is provided followed by the percentage of presentations that did not comply with NI 43-101 requirements. After each Review finding, staff commentary is provided on specific disclosure requirements and reminders for mining issuers. See Appendix A for an overall summary of the 130 investor presentation Review and Appendix B for details of the Review measures and references to the applicable NI 43-101 requirements.

5.1 High Level of Non-Compliance

A. Naming the QP

Of the 130 investor presentations reviewed we found that only 54 provided the QP's name and their relationship to the issuer resulting in 58% non-compliance.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• The foundation of NI 43-101 is that scientific or technical information is prepared or approved by a QP and the document containing this disclosure provides the name and relationship to the issuer of the QP. We remind issuers that including the name of the QP and their relationship to the issuer is required for all documents containing scientific or technical disclosure, including websites and investor relations materials.

• As shown by the results of this Review, the QP plays an important role in disclosure compliance. While the issuer is responsible for its own disclosure, it must ensure that the technical information is consistent with the information provided by the QP. Having the QP review and approve the disclosure (such as the investor presentation, website, etc.) has shown improved compliance with NI 43-101.

- - - - - - - - - - - - - - - - - - - -

B. PEA cautionary statements

We observed that 34 of the investor presentations included financial results from a PEA level economic analysis and found that 56% lacked the required cautionary statements that the study included inferred mineral resources and the financial results of the PEA may not be realized.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• We caution issuers to ensure that disclosure of the results of a PEA provide appropriate cautionary statements for the public to understand the limitations of the results of the PEA. Disclosure of a PEA that include inferred mineral resources must state with equal prominence that, "the preliminary economic assessment is preliminary in nature, it includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the preliminary economic assessment will be realized".

- - - - - - - - - - - - - - - - - - - -

C. Caution that mineral resources are not mineral reserves

We noted that 56 of the investor presentations included financial results of an economic analysis of mineral resources, 34 of which were results of a PEA level study. Of the 56 instances, 50% did not include the required statement cautioning the public that economic viability of the mineral resources has not been demonstrated by the economic analysis.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• Any disclosure implying that a PEA has demonstrated economic or technical viability is contrary to the definition of a PEA. In this context, disclosure of results of an economic analysis of mineral resources must include an equally prominent statement that, "mineral resources that are not mineral reserves do not have demonstrated economic viability". This caution is required any time the disclosure includes the results of an economic analysis of mineral resources.

- - - - - - - - - - - - - - - - - - - -

D. Inclusion or exclusion of mineral reserves in mineral resources

We observed that 22 of the investor presentations disclosed both mineral resources and mineral reserves. For these presentations, it was not clear 50% of the time whether mineral resources included or excluded mineral reserves. This is important information in order to avoid double counting of the mineral resource estimate.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• When reporting both mineral resources and mineral reserves, a clear statement whether mineral resources include or exclude mineral reserves is required. As practices on this matter vary, it is essential to state which convention is being followed to avoid misleading disclosure. The CIM Estimation Best Practice Committee recommends that mineral resources should be reported separately and exclusive of mineral reserves.

- - - - - - - - - - - - - - - - - - - -

E. Exploration targets

We observed that only 14 of the investor presentations included disclosure of an exploration target, but this disclosure was non-compliant 79% of the time. This significant level of non-compliance is related to either failing to express the target as ranges or not including the required cautions, or both.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• Staff has significant concerns about the disclosure of exploration targets, which are not mineral resource estimates and cannot be used the way a mineral resource estimate would be. If a mining issuer chooses to disclose an exploration target, it must provide a reasonable basis for the target and also make the public aware of the target's limitations. Both the potential quantity and grade of the exploration target must be expressed as ranges and be accompanied by an equally prominent statement that, "the potential quantity and grade is conceptual in nature, there has been insufficient exploration to define a mineral resource" and that "it is uncertain if further exploration will result in the target being delineated as a mineral resource".

- - - - - - - - - - - - - - - - - - - -

F. Historical estimates

Our Review observed that 30 of the investor presentations included disclosure of an historical estimate, but this disclosure was non-compliant 60% of the time.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• Disclosure of historical estimates continues to need improvement in order to comply with the requirements. Simply saying "not NI 43-101 compliant" does not meet that requirement. Issuers are reminded that the required information about the source, date, reliability, key assumptions and other factors must be provided each time the historical estimate is disclosed. In addition, an equally prominent statement is required alerting the public that, "a qualified person has not done sufficient work to classify the historical estimate as current mineral resources or mineral reserves" and "the issuer is not treating the historical estimate as current mineral resources or mineral reserves".

- - - - - - - - - - - - - - - - - - - -

G. Exploration information about quality assurance/quality control and naming the laboratory

We found that 86 of the investor presentations disclosed analytical or testing results, with 67% failing to disclose a summary of the quality assurance program and quality control measures applied and 71% failing to provide the name and location of the testing laboratory used.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• Issuers may be able to comply with the disclosure requirements concerning exploration information by including in the written disclosure a reference to the title and date of a document previously filed on SEDAR that contains the exploration information. This may include previously filed documents such as news releases and technical reports. As discussed below, relying on previously filed documents is acceptable to satisfy some of the disclosure requirements in Part 3 of NI 43-101.

- - - - - - - - - - - - - - - - - - - -

H. Data verification

Of the 130 investor presentations reviewed only 47 included any reference to a statement that the QP had verified the data resulting in 64% non-compliance.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• Data verification is the process of confirming that the data underlying the written disclosure has been properly generated, was accurately transcribed, and is suitable for the purpose that the data is used. NI 43-101 requires the issuer to include a statement regarding verification of the data by the QP in the document containing the written disclosure.

• As noted above with exploration information, disclosure regarding data verification may be made compliant by referencing the title and date of a document previously filed by the issuer that contains the required data verification statement information by the QP.

- - - - - - - - - - - - - - - - - - - -

5.2 Areas for Additional Improvement

A. Taxes in economic studies

We found that 56 of the investor presentations included financial results from economic studies (34 PEA level and 22 pre-feasibility or feasibility level). Of these 56 instances, 37% reported only pre-tax financial results or provided no information about the tax rate for the mineral project. Surprisingly, the level of pre-tax only financial results was higher for projects at a pre-feasibility or feasibility level than at a PEA level.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• Reporting only pre-tax financial results for an "advanced property", which includes results of a PEA, pre-feasibility or feasibility study does not provide complete and balanced information for investors to appropriately assess the financial results. In order to properly evaluate the potential viability of mineral resources in a PEA, or to demonstrate viability in a pre-feasibility or feasibility study, the cash flow model needs to include assumptions that have an economic impact such as taxes, royalties, and other government levies.

- - - - - - - - - - - - - - - - - - - -

B. Metal price assumptions used in mineral resources and mineral reserves

Eighty-one of the investor presentations disclosed mineral resources and 22 of these also disclosed mineral reserves. We found that 30% of the time no information was provided about the assumed metal price used for determining the mineral estimates.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• Metal or commodity price assumptions are key factors in establishing the cut-off grade for both mineral resources and mineral reserves and these assumptions can have a significant impact on the size of the mineral estimate. For this reason, it is important that the assumed metal or commodity price, and the cut-off grade, be clearly stated. Issuers are also reminded to provide the effective date of the reported estimate.

• Providing a complete table of current mineral resources and mineral reserves with all material assumptions in an appendix to the investor presentation may assist in providing the required information. Issuers may also be able to satisfy the requirement to disclose key assumptions by referencing the title and date of a document previously filed by the issuer that contains the required information. Nevertheless, if the assumed metal or commodity price is significantly below or above current prices, issuers should make sure the disclosure is not misleading by clearly stating the key assumptions.

- - - - - - - - - - - - - - - - - - - -

C. Drilling information regarding true widths and significantly higher grade intervals

We observed that 70 of the investor presentations included drilling results. Of these, 38% did not include information on true widths of mineralized zones and 42% did not provide results of significantly higher grade intervals enclosed in a lower grade intersection. This type of information is particularly important for early stage projects.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• When drilling results are reported, it is important that investors be provided with information about the nature and context of the results such as true width and higher grade intersections. Without this information the drilling results, especially at the exploration stage, may be potentially misleading.

• In some cases, including representative drill sections or other figures showing mineralized intervals may assist in providing the necessary information in investor presentations. Mining issuers may also be able to rely on a previously filed document that contains the required information.

- - - - - - - - - - - - - - - - - - - -

5.3 Technical Report Triggers

Technical reports are a key disclosure document under NI 43-101, supporting a mining issuer's disclosure about its material mineral properties. Our Review identified 81 investor presentations that disclosed mineral resources, mineral reserves, or results of a PEA. First time written disclosure of mineral resources, mineral reserves, or results of a PEA, or a change to any of these that constitutes a material change for the issuer triggers the filing of a technical report.

We noted that five of the 81 investor presentations (6%) disclosed financial results of an economic analysis (e.g. PEA or scoping study) that were not supported by a technical report.

Staff commentary

- - - - - - - - - - - - - - - - - - - -

• Notwithstanding the fact that our review showed a high level of compliance, we have determined that a highlight of this requirement is warranted based on the relative gravity of not complying with the technical report trigger.

• We have significant concerns when information provided on a mining issuer's website includes PEA disclosure that is not supported by the existing technical report. Disclosing economic projections in investor presentations, fact sheets, posted or linked third party reports, or any statements on the issuer's website may trigger the filing of a technical report to support the disclosure.

• Mining issuers are reminded that we consider that the issuer has disclosed the results of a PEA, or similar type of economic analysis, when the disclosure includes information such as forecast mine production rates that might contain capital costs to develop and sustain the mining operation, operating costs, and projected cash flows.

- - - - - - - - - - - - - - - - - - - -

6. FLI Compliance

The majority of investor presentations included FLI disclosure, often on slide two. We observed that 54% did not provide information required by paragraph 4A.3(c) of NI 51-102 concerning the material factors and assumptions used to develop the FLI. We expect that mining issuers will follow General Guidance (3) of Companion Policy 43-101CP indicating that FLI includes metal price assumptions used in mineral resource and mineral reserve estimates as well as other assumptions used in economic analysis and financial projections based on engineering studies.

7. Overly Promotional Terms and Potentially Misleading Information

During the course of the Review, we also assessed the investor presentations for terms and statements that may be overly promotional or misleading, potentially resulting in a misrepresentation{2} under securities legislation in a jurisdiction of Canada.

Terms which may be used inappropriately in certain circumstances include, "world-class", "spectacular and exceptional results", "production ready", "ore" in relation to mineral resources, and "management estimates". We noted that 38% of the investor presentations included statements that could be considered overly promotional or misleading, especially exploration stage and mineral resource stage issuers, by portraying their project to be at a more advanced stage of development.

8. Conclusions

We expect mining issuers to use this notice to strengthen their compliance with securities legislation and improve their disclosure to investors. Having the QP review technical disclosure in investor presentations and other website disclosure is an important step in improving compliance with NI 43-101.

We will continue the review of mining issuers' website disclosure as part of our overall continuous disclosure review program. When we identify material disclosure deficiencies, we will request that the issuer correct the deficiency by amending or removing the website disclosure and filing a clarifying or retracting news release. We may place the issuer on the reporting issuer default list and where the issuer fails to comply with the requests we may consider issuing a cease trade order until the issuer corrects the deficiency.

If an issuer is considering a prospectus offering, the review of the prospectus filing will likely be deferred if issues such as those noted above are present.

For further guidance on this issue, please see CSA Staff Notice 51-312 Harmonized Continuous Disclosure Review Program and CSA Notice 51-322 Reporting Issuer Defaults.

Questions

Please refer your questions to any of the following people:

{1} As at December 2014

{2} Misrepresentation as defined under securities legislation in each of the Canadian jurisdictions. Though the wording of the definition of "misrepresentation" differs slightly, in substance this definition is harmonized in all jurisdictions.

Appendix A

Results of 130 Investor Presentation Reviews

The following chart provides a summary of the 130 investor presentations reviewed and the percentage of non-compliance compared to particular disclosure requirements in NI 43-101. The non-compliance percentage is relative to the number of occurrences of the particular disclosure (population size). Disclosure requirements are grouped and colour-coded by type of disclosure, such as Economic studies.

Appendix B

Review Measures in Appendix A with Reference to Provisions of NI 43-101

Note: Review measures below are grouped and listed in the same order as the results in Appendix A.

|

Naming the QP |

s. 3.1 requires issuers to name the QP responsible for the technical disclosure and their relationship to the issuer |

|

|

|

|

Economic studies |

|

|

PEA caution |

ss. 2.3(3) requires disclosure of a PEA that includes inferred mineral resources provide the mandatory cautionary statements |

|

|

|

|

Resources are not reserves |

para. 3.4(e) requires a statement that mineral resources that are not mineral reserves do not have demonstrated economic viability if results of an economic analysis of mineral resources is provided |

|

|

|

|

Taxes |

Item 22(d) of Form 43-101F1 requires a summary of taxes applicable to the mineral project |

|

|

|

|

Balanced sensitivity |

s. 3.5 of 43-101CP states that disclosure must be factual, complete, and balanced and not present or omit information in a manner that is misleading -- such as an unbalanced sensitivity analysis |

|

|

|

|

Percentage interest |

s. 3.5 of 43-101CP states that disclosure must be factual, complete, and balanced and not present or omit information in a manner that is misleading -- such as not stating that the issuer only holds a minor percentage interest in a mineral project |

|

|

|

|

Metal price assumption |

Item 22(a) of Form 43-101F1 requires a clear statement of the principal assumptions used in an economic analysis -- such as assumed metal price |

|

|

|

|

Technical report trigger |

para. 4.2(1)(j) requires that first time written disclosure of mineral resources, mineral reserves or the results of a PEA, or a change to any of these that is a material change to the issuer, must be supported by a technical report |

|

|

|

|

Restricted disclosure |

|

|

Exploration targets |

ss. 2.3(2) permits disclosure of exploration targets expressed as ranges of potential quantity and grade and subject to the inclusion of mandatory cautionary statements and other information |

|

|

|

|

Gross metal value |

para. 2.3(1)(c) prohibits issuers from disclosing gross value of metal or mineral in a deposit or sampled interval |

|

|

|

|

Restricted economics |

para. 2.3(1)(b) prohibits the disclosure of economic analysis using inferred mineral resources (except as allowed in a PEA), historical estimates, or exploration targets |

|

|

|

|

Historical estimates |

s. 2.4 requires specific information and mandatory cautionary statements when disclosing historical estimates |

|

|

|

|

Mineral resources & mineral reserves |

|

|

Resources include reserves |

para. 2.2(b) requires a statement whether mineral reserves are included in mineral resources |

|

|

|

|

Metal price assumption |

para. 3.4(c) requires disclosure of key assumptions (such as assumed metal price) used to determine the mineral resources and mineral reserves |

|

|

|

|

Metal equivalent |

para. 2.3(1)(d) requires that disclosure of a metal equivalent grade also state the grade of each metal used to establish the metal equivalent grade |

|

|

|

|

Effective date |

para. 3.4(a) requires that the effective date of a mineral resource and mineral reserve be disclosed if the mineral estimate is reported |

|

|

|

|

Cut-off grade |

para. 3.4(c) requires disclosure of key assumptions (such as cutoff grade) used to determine the mineral resources and mineral reserves |

|

|

|

|

Inferred not added |

para. 2.2(c) prohibits the addition of inferred resources to other categories of mineral resources |

|

|

|

|

Tonnes and grade |

para. 3.4(b) requires the quantity and grade of each category of mineral resources and mineral reserves be disclosed |

|

|

|

|

Contained metal |

para. 2.2 (d) requires that disclosure of contained metal also state the grade and quantity for each category of mineral resources and mineral reserves |

|

|

|

|

CIM categories |

para. 2.2(a) requires the use of only accepted mineral resource and mineral reserve categories as prescribed by the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) |

|

|

|

|

Data verification |

s. 3.2 requires issuers to include a statement whether a QP has verified the data disclosed, how it was verified and reasons for any failure to verify |

|

|

|

|

Exploration information |

|

|

Name of laboratory |

para. 3.3(2)(f) requires disclosure of the name and location of the testing laboratory used and any relationship to the issuer |

|

|

|

|

QA/QC measures |

para. 3.3(1)(c) requires disclosure of a summary of the quality assurance program and quality control measures applied |

|

|

|

|

Higher grade intervals |

para. 3.3(2)(d) requires disclosure of any significantly higher grade intervals forming part of a lower grade intersection |

|

|

|

|

True widths of zones |

para. 3.3(2)(c) requires disclosure of true widths of mineralized zones, to the extent known |

|

|

|

|

Drill hole information |

para. 3.3(2)(b) requires disclosure of drilling information to include the location, azimuth and dip of the drill holes and the sample interval depth |