Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

Notice and Request for Comments: Proposed Amendments to NI 54-101 Communication with Beneficial Owners of Securities of a Reporting Issuer and Companion Policy 54-101CP Communication with Beneficial Owners of Securities of a Reporting Issuer

Notice and Request for Comments: Proposed Amendments to NI 54-101 Communication with Beneficial Owners of Securities of a Reporting Issuer and Companion Policy 54-101CP Communication with Beneficial Owners of Securities of a Reporting Issuer

NOTICE AND REQUEST FOR COMMENTS

PROPOSED AMENDMENTS TO

NATIONAL INSTRUMENT 54-101

COMMUNICATION WITH BENEFICIAL OWNERS OF SECURITIES OF A REPORTING ISSUER

AND

COMPANION POLICY 54-101CP COMMUNICATION WITH BENEFICIAL OWNERS

OF SECURITIES OF A REPORTING ISSUER

PROPOSED AMENDMENTS TO

NATIONAL INSTRUMENT 51-102 CONTINUOUS DISCLOSURE OBLIGATIONS

AND

COMPANION POLICY 51-102CP CONTINUOUS DISCLOSURE OBLIGATIONS

June 17, 2011

1. Introduction

We, the members of the Canadian Securities Administrators (the CSA), are publishing for a 60-day comment period revised versions of proposals (the Proposals) intended to improve the process by which reporting issuers send proxy-related materials to and solicit voting instructions from registered holders and beneficial owners of their securities (the Shareholder Voting Communication Process).

Specifically, we are publishing the following materials (the Revised Materials):

• a revised proposed amendment instrument to National Instrument 54-101 Communication with Beneficial Owners of Securities of a Reporting Issuer and the related forms (NI 54-101);

• a revised proposed amendment instrument to National Instrument 51-102 Continuous Disclosure Obligations and Form 51-102F5 Information Circular (Form 51-102F5) (collectively, NI 51-102); and

• revised proposed changes to:

• Companion Policy 54-101CP Communication with Beneficial Owners of Securities of a Reporting Issuer (54-101CP); and

• Companion Policy 51-102CP Continuous Disclosure Obligations (51-102CP).

The original versions of the above materials (the Original Materials) were first published on April 9, 2010. We received 27 comment letters. A summary of the comments we received and our responses to those comments are included in Schedule A.

The Original Materials also included proposed amendments to National Policy 11-201 Delivery of Documents by Electronic Means (NP 11-201). We are not publishing revised amendments to NP 11-201 at this time. An amended and restated version of NP 11-201 201 (Proposed New NP 11-201) was published for comment on April 29, 2011. We will consider at a later date what, if any, additional changes to Proposed New NP 11-201 should be made in connection with the Proposals.

The Revised Materials are contained in the following Schedules to this Notice. Certain jurisdictions may include additional local information in Annex I.

|

Schedule A:

|

Summary of Comments

|

|

|

|

|

Schedule B:

|

Revised Proposed Amendment Instrument to NI 54-101 and Blackline to the Original Materials

|

|

|

|

|

Schedule C:

|

Revised Proposed Changes to 54-101CP

|

|

|

|

|

Schedule D:

|

Revised Proposed Amendment Instrument to NI 51-102 and Blackline to the Original Materials

|

|

|

|

|

Schedule E:

|

Revised Proposed Changes to 51-102CP

|

|

|

|

|

Annex I:

|

Local Information

|

The Revised Materials will also be available on websites of CSA jurisdictions, including:

www.lautorite.qc.ca

www.albertasecurities.com

www.bcsc.bc.ca

www.gov.ns.ca/nssc

www.nbsc-cvmnb.ca

www.osc.gov.on.ca

www.sfsc.gov.sk.ca

www.msc.gov.mb.ca

For more information on the comment process, see below under "How to provide your comments on the Revised Materials".

2. Substance and purpose of the Proposals and the Revised Materials

The most significant features of the Proposals are as follows:

• providing reporting issuers with a new "notice-and-access" mechanism to send proxy-related materials to registered holders and beneficial owners of securities, collectively shareholders;

• simplifying the process by which beneficial owners are appointed as proxy holders in order to attend and vote at shareholder meetings; and

• requiring reporting issuers to provide enhanced disclosure regarding the beneficial owner voting process.

The Revised Materials contain proposed changes affecting these three features of the Proposals, which we describe below. We also briefly describe additional changes to other aspects of the Original Materials.

(a) Changes to notice-and-access (proposed sections 2.7.1 to 2.7.6 of NI 54-101; proposed sections 9.1.1 to 9.1.6 of NI 51-102)

Under notice-and-access, a reporting issuer would be permitted to deliver proxy-related materials by sending a notice package to shareholders containing the following:

• a notice to shareholders informing them that proxy-related materials have been filed on SEDAR and posted on another non-SEDAR website and explaining how to access them; and

• the relevant voting document (a proxy, Form 54-101F6 or Form 54-101F7, as applicable).

The notice package would not contain the information circular. Instead, the information circular would be filed on SEDAR and also posted on a non-SEDAR website. A shareholder could request that a paper copy of the information circular be mailed to the shareholder free of charge.

We continue to take the view that properly designed notice-and-access procedures can enhance the Shareholder Voting Communication Process as well as increase the overall efficiencies of the system. We now propose several changes to our original proposal in response to the comments we received, as well as our ongoing examination of the Shareholder Voting Communication Process.

(i) Reporting issuers other than investment funds can use notice-and-access for all meetings

The original notice-and-access proposal would not have permitted reporting issuers to use notice-and-access for "special meetings" as defined in NI 54-101. We now propose that notice-and-access be permitted for all meetings of reporting issuers that are not investment funds. See proposed section 2.7.1 of NI 54-101 and proposed section 9.1.1 of NI 51-102.

This proposed change is intended to address concerns that restricting notice-and-access to meetings that are not special meetings:

• adds an additional layer of complexity to the voting process and may cause shareholder confusion;

• implies that "routine" annual matters such as director elections and auditor appointments are not important; and

• limits the potential efficiencies that can be realized by notice-and-access.

The proposed change also excludes investment funds from using notice-and-access. We did not explicitly request comment on, nor did we receive any comments that specifically addressed, the issue of whether investment fund reporting issuers should also be permitted to use notice-and-access for meetings. We would like to consider further and seek feedback on the appropriate form and content of notice for meetings involving investment funds, particularly those involving fundamental changes to an investment fund.

We also propose additional companion policy guidance on factors that reporting issuers should take into account when deciding when and how to use notice-and-access. Factors include:

• the nature of the meeting business; and

• whether notice-and-access resulted in material declines in shareholder voting rates where it was used for prior meetings.

(ii) Reporting issuers must provide advance notice of their first use of notice-and-access and disclosure and provide information regarding use of notice-and-access in the notification of meeting and record dates

The original notice-and-access proposal would have permitted a reporting issuer to use notice-and-access without giving shareholders any prior notification. This raises concerns that a shareholder who receives a notice package for the first time would be confused about what he or she is being sent.

We now propose that prior to using notice-and-access for the first time, a reporting issuer must provide advance notice that it intends to do so three to six months before the meeting. The issuer must issue a news release and post information regarding notice-and-access on a website that is not SEDAR. See proposed section 2.7.2 of NI 54-101 and proposed section 9.1.2 of NI 51-102.

We also no longer propose to require that each time a reporting issuer uses notice-and-access it issue a news release disclosing that fact at least 30 days before the meeting. We now propose that the reporting issuer state its intention to use notice-and-access in the notification of meeting and record dates required by section 2.2 of NI 54-101.

In addition, we provide companion policy guidance encouraging issuers to consider what additional methods of advance notice are appropriate, such as a mailing in advance of the meeting.

(iii) Reporting issuers must provide explanatory material regarding notice-and-access in the notice package

The original notice-and-access proposal did not require that any explanatory material regarding notice-and-access be included in the notice package. We now think that shareholders who receive a notice package always should have basic information about notice-and-access as part of the notice package.

We now propose that a reporting issuer must include a plain-language explanation of notice-and-access in the notice package that is sent to shareholders. The reporting issuer must also post the explanation on the website where the full set of proxy materials is posted. See proposed subparagraph 2.7.1(1)(a)(ii) of NI 54-101, and proposed subparagraph 9.1.1(1)(a)(ii) of NI 51-102.

(iv) Reporting issuers cannot include additional material in the notice package other than explanatory material regarding notice-and-access

The original notice-and-access proposal would have permitted reporting issuers to include additional material regarding the meeting (but not an information circular) in the notice package. We now propose to restrict a reporting issuer from including such additional material in the notice package unless a copy of the information circular is also included. We are concerned that provision of such additional material without an information circular encourages shareholders to only read the additional material without referring to the information circular.

(v) Inclusion of paper copies of the information circular with the notice package pursuant to standing instructions

The original notice-and-access proposal did not explicitly address whether it was permissible for a shareholder to provide annual or standing instructions to receive a paper copy of the information circular where a reporting issuer uses notice-and-access. Under the original proposal, the only specified method by which a shareholder could obtain a paper copy of the information circular was to contact the reporting issuer (or the reporting issuer's service provider) to request a paper copy after the notice package had been sent out.

We now think that shareholders should be able to request that a paper copy of the information circular be automatically included with the notice package. Having the information circular automatically included, as opposed to having to wait until the notice package has been sent out, is more user-friendly to shareholders.{1} Standing instructions also provide reporting issuers with information that can assist them in planning print volumes.

We therefore propose that reporting issuers be permitted to obtain standing instructions from registered holders, and intermediaries be permitted to obtain standing instructions from beneficial owners. Where a reporting issuer or intermediary obtains such instructions, they must comply with these instructions. We also impose obligations on reporting issuers and intermediaries to facilitate compliance with these standing instructions once they have been obtained. See proposed section 2.7.6 of NI 54-101 and proposed section 9.1.5 of NI 51-102.

(vi) Inclusion of paper copies of the information circular with the notice package where annual financial statements and MD&A are requested and sent as part of proxy-related materials

Section 4.6 of NI 51-102 establishes an annual request form mechanism for shareholders to request copies of a reporting issuer's annual financial statements and annual MD&A for the following year. These documents are generally found in an annual report, so for ease of reference, we will use the term annual report to refer to those documents.

If a reporting issuer does not send the annual report to all shareholders, the reporting issuer must send the annual request form to its shareholders to enable shareholders to request the annual report for the following financial year. In practice, service providers have integrated the annual request form mechanism with the Shareholder Communication Voting Process by:

• incorporating the annual request form into the proxy or the voting instruction form sent as part of proxy-related materials to shareholders. This avoids a separate mailing of the request form; and

• where the annual report has been requested, automatically inserting the annual report into the proxy-related materials sent to the relevant shareholders. This avoids a separate mailing of the annual report.

We also encourage reporting issuers to send their audited annual financial statements or annual report at the same time as other proxy-related materials. See section 7.2 of 54-101CP.

We have received feedback from Broadridge Investor Communications Corporation, the primary intermediary service provider, that in order to facilitate the efficient integration of the annual request form mechanism with the Shareholder Communication Voting Process, annual instructions to receive the annual report should also constitute instructions to include a paper copy of the information circular where the reporting issuer uses notice-and-access. Conversely, standing instructions to receive paper copies of the information circular as part of the notice package should also constitute instructions to include the annual report as part of the notice package.

If the instructions were not integrated in the above fashion, service providers would need to modify the existing infrastructure to accommodate four types of notice packages:

• notice package without paper copy of information circular and annual report;

• notice package with paper copy of information circular;

• notice package with paper copy of annual report; and

• notice packages with paper copy of information circular and annual report.

In contrast, integrating the instructions as requested would reduce the types of notice packages to two:

• notice package without paper copy of information circular and annual report;

• notice package with paper copy of information circular and annual report.

Having two types of notice packages would be simpler to design, implement and maintain.

We do not have any concerns with automatically including a paper information circular with the notice package for those shareholders who have requested to receive the annual report, and therefore propose that section 4.6 of NI 51-102 be amended so that paper copies of the information circular will be included with the notice package where the annual report is requested and sent as part of proxy-related materials.

However, we are not proposing at this time to explicitly prescribe the converse, i.e., the automatic inclusion of an annual report with the notice package where a paper information circular is included pursuant to standing instructions. While we acknowledge that having two types of notice packages would be simpler to design, implement and maintain, we would appreciate additional input from stakeholders before proposing such a change. Is it reasonable to infer that a shareholder who wishes to receive a paper copy of the information circular would also wish to receive the annual report?

(vii) Stratification

The original notice-and-access proposal contemplated that a reporting issuer could choose to send a notice package to some shareholders, and send a standard package (which would contain the notice of meeting, voting document and information circular) to others.

We now propose that where a reporting issuer uses notice-and-access, it must send the same basic notice package containing the required notice, the voting document, and the explanation of notice-and-access to all shareholders. However, the notice package for those shareholders who have provided standing instructions and who have provided annual instructions (as discussed above) would also include the paper copy of the information circular.

We refer to the process of including a paper copy of the information circular in the notice package as "stratification", and have added a new definition in subsection 1(1) of NI 54-101 and subsection 1.1(1) of NI 51-102.

We do not propose at this time to prescribe other criteria for when stratification can be used by a reporting issuer. We would require reporting issuers to disclose whether they are using stratification, and what criteria they are applying to determine which shareholders will receive a paper copy of the information circular. However, we are proposing companion policy guidance that states our expectation that a reporting issuer that uses stratification for purposes other than complying with shareholder instructions would do so in order to enhance effective communication, and not to disenfranchise shareholders.{2} The guidance also explains that we would not mandate the provision of stratification by reporting issuers or intermediaries, other than in order to comply with standing instructions or annual requests for paper copies of information circulars that they may have chosen to obtain from registered holders or beneficial owners. We expect any additional stratification criteria will evolve through market demand and practice, and we will monitor developments in this area.

(viii) The proposed exemption for delivery of proxy-related materials using US notice-and-access is available only to SEC issuers with a limited Canadian presence

The original notice-and-access proposal would have exempted reporting issuers who are SEC issuers from the obligation to deliver proxy-related materials to beneficial owners under NI 54-101 where they use the notice-and-access process prescribed by the SEC (U.S. notice-and-access). A similar exemption was proposed in respect of registered holders. We propose to amend the exemption to clarify that it is available only to SEC issuers with a limited Canadian presence. We also are exempting intermediaries who deliver proxy-related materials on behalf of the issuer using U.S. notice-and-access from their obligations under NI 54-101. See section 9.1.1 of NI 54-101 and section 9.1.6 of NI 51-102.

(ix) Methods for sending notice package

The original notice-and-access proposal contemplated that issuers would deliver the notice package either using:

• prepaid mail, courier or the equivalent; or

• any other method previously consented to by the shareholder.

We now propose to remove the reference to "any other method previously consented to by the shareholder", as it was not clear what such methods would be and how in practice they could be used to send the notice package. The revised provisions now only refer to sending the notice package by prepaid mail, courier or the equivalent. See paragraph 7.1(1)(b) of NI 54-101 and paragraph 9.1.1(1)(c) NI 51-102.

However, a reporting issuer's decision to use notice-and-access would not preclude a shareholder from also being sent proxy-related materials using an alternate method to which the shareholder previously has consented. See section 2.7.5 of NI 54-101 and section 9.14 of NI 51-102. For example, our understanding is that one or more service providers acting on behalf of reporting issuers or intermediaries have previously obtained consents from shareholders for proxy-related materials to be sent by email (with links to the materials included in the body of the email). This delivery method would still be available to issuers and intermediaries even if notice-and-access is used.

(x) Specific times by which a reporting issuer must provide materials for forwarding to proximate intermediaries

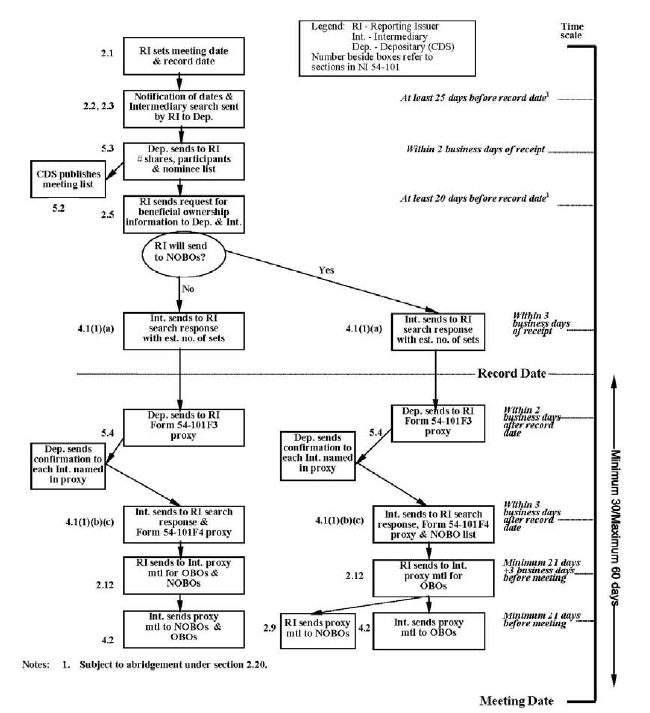

The original notice-and-access proposal did not mandate specific times by which a reporting issuer would have to provide the documents for the notice package to proximate intermediaries for forwarding. We now propose specific timelines: three business days before the 30th day before the date fixed for the meeting where materials are sent by first class mail, courier or the equivalent, and four business days before the 30th day in the case of other types of prepaid mail. See subsection 2.12(3) of NI 54-101.

We provide guidance in 54-101CP that "first class mail" is the equivalent of Canada Post Lettermail.

(xi) Methods and timing for fulfilling request for paper information circulars

We propose that there be two different sets of fulfillment requirements for requests received prior to the date of the meeting, and on or after the date of the meeting. Where the request is received prior to the date of the meeting, the paper information circular must be sent by first class mail, courier or the equivalent within three business days. Where the request is received on or after the date of the meeting, and within one year of the information circular being filed, the paper information circular must be sent by prepaid mail, courier or the equivalent within 10 calendar days. Requests for a paper copy of the information circular do not need to be fulfilled more than one year after the date of the applicable meeting. See paragraph 2.7.1(1)(f) of NI 54-101.

(xii) Other changes to the notice-and-access proposal

We are also making the following additional changes to the notice-and-access proposal:

• The information circular and other documents in the notice package must be filed on SEDAR and posted on a non-SEDAR website on or before the day that the reporting issuer sends the notice package (paragraph 2.7.1(1)(d) of NI 54-101). The original proposal that the posting had to occur on the same day as the sending of the notice package meant that reporting issuers potentially would have to choose between mailing the annual financial statements and annual MD&A with the notice package, and incorporating by reference the information circular in the AIF.

• We have modified the provisions that restrict information gathering by reporting issuers who receive requests for paper copies of information circulars or via the non-SEDAR website so that the prohibitions address intentional information gathering by the reporting issuer (section 2.7.3 of NI 54-101). Intentional information gathering can be contrasted with situations where information is volunteered by a requester, or where certain website functionality could be, but is not used, to identify a shareholder who accesses the non-SEDAR website.

(b) Simplification of beneficial owner proxy appointment process (sections 2.18 and 4.5 of NI 54-101)

(i) Authority to act for and on behalf of the beneficial owner in respect of all matters that may come before the meeting

The Original Materials proposed the repeal of the provisions relating to legal proxies, and replaced them with a provision that requires intermediaries and management as applicable to appoint a beneficial owner (or another person designated by the beneficial owner) as proxy holder to attend and vote at the meeting, if requested by the beneficial owner. However, there was no explicit requirement that an intermediary or reporting issuer management give discretionary authority to a beneficial owner to vote on all matters that would come before the meeting. The lack of an explicit requirement would permit an intermediary or management to limit the scope of voting authority to only those matters identified in the voting instruction form, and therefore potentially prevent the beneficial owner from voting on important matters that might come before the meeting but that were not set out in the voting instruction form.

We therefore propose that unless a beneficial owner has instructed otherwise, where an intermediary appoints a beneficial owner or a nominee of the beneficial owner as a proxy holder, the beneficial owner or nominee also must be given authority to attend, vote and otherwise act for and on behalf of the intermediary (or the issuer's management, where the reporting issuer is sending proxy-related materials directly to NOBOs) in respect of all matters that may come before the applicable meeting and at any adjournment or continuance.

We also propose consequential changes to the instructions regarding attending and voting at a meeting in Form 54-101F6 and Form 54-101F7.

(ii) Deposit of proxy prior to proxy cut-off

The Original Materials proposed to require an intermediary (or if applicable the reporting issuer) to deposit any proxy appointing a beneficial owner as a proxy holder within any time specified under corporate law for the deposit of proxies (a proxy cut-off). We propose to modify this requirement so that it applies only where the intermediary or reporting issuer (as the case may be) obtains the instructions from the beneficial owner to appoint it as proxy holder at least one business day before the proxy cut-off.

(c) Enhanced disclosure of voting process (subsection 2.2(2) of NI 54-101)

We propose to add a requirement that the notification of meeting and record dates under subsection 2.2(2) of NI 54-101 also include disclosure regarding the reporting issuer's use of notice-and-access, whether it is sending proxy-related materials directly to NOBOs, and whether it intends to pay for delivery of proxy-related materials directly to OBOs. We think that including this information in the notification will enhance the transparency of the voting process. This requirement is in addition to the requirement to disclose the above information in the information circular if applicable.

(d) Other changes to NI 54-101

We propose several other changes in respect of the amendments to NI 54-101:

• Subsection 2.5(4): We propose that a reporting issuer or person or company retained by the reporting issuer may request beneficial ownership information for the purpose of obtaining a NOBO list, if the intermediary to whom the request is being made reasonably believes that the person or company making the request has the technological capacity to receive the NOBO list. We think this change balances the concern with opening up the entire process of obtaining beneficial ownership information with streamlining the process for obtaining NOBO lists. It also enables the entity in the best position to assess a requester's technological capacity to receive the NOBO list to make that assessment.

• Removal of proposed changes to processing times in section 2.12: We no longer propose to have a single three-day processing time for proxy-related materials sent indirectly by prepaid mail. We are retaining the existing provision, which requires an additional day for processing proxy-related materials that are not sent by first class mail.

• Subsections 2.18(5) and 5.4(4): We propose to clarify that the confirmation provided to the intermediary must identify the specific meeting to which the confirmation applies, but is not required to specify each proxy appointment.

• Subsection 2.20(a.1) of NI 54-101: We propose to clarify that where a reporting issuer uses notice and access, a reporting issuer can abridge the record date for notice to not less than 30 days before the meeting date, and the sending of the notification of meeting and record dates under section 2.2 to not less than 30 days before the date of the meeting. This is to enable shareholders to have sufficient time to request and receive a paper copy of the information circular in advance of the meeting, if they wish to receive one.

• Removal of certain proposed record keeping requirements: We are removing the proposed requirements for issuers and intermediaries to retain a record of each Form 54-101F6 or Form 54-101F7 sent and the date and time of any voting instructions, including proxy appointment instructions, at this time. We will consider the broader issue of record-keeping generally in the proxy voting system at another time.

• Form 54-101F2 Request for Beneficial Ownership Information: We propose to amend the form to require the reporting issuer to state whether it is using notice-and-access, and any stratification criteria being used.

3. Other possible reforms to the proxy voting process

We received a number of comments on possible reforms to the proxy voting process which are set out and discussed in Appendix A. We thank all the commentators for their feedback. We are not at this stage publishing any specific regulatory proposals, other than the Proposals, in response to the comments we received. However, we continue to assess the proxy voting process, and may publish additional materials for consultation at a later date. We note that the proxy voting system is complex, and changes intended to improve one part of the system can cause "ripple effects" on other parts. Any proposed reforms must be carefully designed in order to minimize the likelihood of unintended consequences.

4. How to provide your comments on the Revised Materials

You must submit your comments in writing by August 16, 2011. If you are sending your comments by email, you should also send an electronic file containing the submissions in Microsoft Word.

Please address your comments to all of the CSA member commissions as follows:

British Columbia Securities Commission

Alberta Securities Commission

Saskatchewan Financial Services Commission -- Securities Division

Manitoba Securities Commission

Ontario Securities Commission

Autorité des marchés financiers

New Brunswick Securities Commission

Registrar of Securities, Prince Edward Island

Nova Scotia Securities Commission

Superintendent of Securities, Northwest Territories

Superintendent of Securities, Yukon Territory

Superintendent of Securities, Nunavut

Please send you comments only to the addresses below. Your comments will be forwarded to the remaining CSA jurisdictions.

John Stevenson

Secretary

Ontario Securities Commission

20 Queen Street West

19th Floor, Box 55

Toronto, Ontario M5H 3S8

Fax: 416-593-2318

Email: [email protected]

Anne-Marie Beaudoin

Corporate Secretary

Autorité des marchés financiers

800, square Victoria, 22e étage

C.P. 246, tour de la Bourse

Montréal, Québec H4Z 1G3

Fax: 514-864-6381

E-mail: [email protected]

Please note that all comments received during the comment period will be made publicly available. We cannot keep submissions confidential because securities legislation in certain provinces requires publication of a summary of the written comments received during the comment period.

We will post all comments received during the comment period to the OSC website at www.osc.gov.on.ca to improve the transparency of the policy-making process.

Questions

Please refer your questions to any of the following:

|

Winnie Sanjoto

|

Lucie J. Roy

|

|

Senior Legal Counsel

|

Senior Policy Advisor

|

|

Corporate Finance Branch

|

Policy and Regulation Department

|

|

Ontario Securities Commission

|

Autorité des marchés financiers

|

|

416-593-8119

|

514-395-0337 poste 4464

|

|

|

|

|

Nazma Lee

|

Donna Gouthro

|

|

Senior Legal Counsel

|

Financial Analyst

|

|

Legal Services, Corporate Finance Division

|

Nova Scotia Securities Commission

|

|

British Columbia Securities Commission

|

902-424-7077

|

|

604-899-6867

|

|

|

Toll-free (across Canada): 800-373-6393

|

|

|

|

|

|

|

|

|

Celeste Evancio

|

|

|

Legal Counsel

|

|

|

Corporate Finance

|

|

|

Alberta Securities Commission

|

|

|

403-355-3885

|

|

|

|

|

{1} We note that data from the U.S. suggests that where retail beneficial owners receive full packages of materials as a result of standing instructions, their rate of vote return is extremely high. 60% of beneficial owner accounts that received full packages as a result of standing instructions voted, as compared to approximately 19% of beneficial owner accounts where notice-and-access was not used. See "Notice and Access: Statistical Overview of Use with Beneficial Shareholders As of December 31, 2010." Slides available at http://www.broadridge.com/notice-and-access/index.asp.

{2} One example of how stratification could enhance communication is where a reporting issuer wishes to send proxy-related materials to all its beneficial owners, including those who have declined to receive materials (declining beneficial owners). These declining beneficial owners could be sent a notice package only, while the reporting issuer would send other beneficial owners who wished to receive all materials the notice package and the information circular. All beneficial owners thus would receive the documentation necessary to vote, but those declining to receive materials would not receive a paper copy of the information circular unless they requested it.

SCHEDULE A

SUMMARY OF COMMENTS AND RESPONSES

We received comment letters from the following:

British Columbia Investment Management Corporation

Broadridge Investor Communication Solutions Canada

Canadian Bankers Association

Canadian Coalition for Good Governance

Canadian Foundation for Advancement of Investors Rights

Canadian Oil Sands

Canadian Society of Corporate Secretaries

Computershare Trust Company of Canada

Davies Ward Phillips & Vineberg LLP

GG Consulting

Hermes Equity Ownership Services Limited

Investment Industry Association of Canada

Kempenfelt House Consulting Inc.

Kenmar Associates

Kingsdale Shareholder Services

Laurel Hill Advisory Group

Manitoba Telecom Services Inc.

Manulife Financial Corporation

Mouvement d'Education et de Défense des Actionnaires

Ontario Bar Association

Pension Investment Association of Canada

RBC Dominion Securities

Scotia Capital Inc.

Securities Transfer Association of Canada

Shareholder Association for Research and Education

TMX Group Inc.

TransCanada Corporation

A. Comments on the Original Materials

|

# |

Issue/Comment |

Response |

|

|

||

|

Notice-and-Access |

||

|

|

||

|

1. |

Whether notice-and-access generally is a positive development, particularly for retail investors |

|

|

|

||

|

|

The majority of comments, including comments from reporting issuers, institutional shareholders, intermediaries and service providers, were generally supportive of notice-and-access as being a positive step toward encouraging proxy voting and making the system more efficient. A transfer agent group noted that in its view, the main cause for a decrease of retail voting in the U.S. was the absence of the voting instruction form from the notice package. Several comment letters, however, recommended improvements be made to the proposed notice-and-access procedures, particularly a greater focus on shareholder education regarding notice-and-access. |

We continue to think that permitting issuers to use notice-and-access to send proxy-related materials can improve the beneficial owner communication process. |

|

|

||

|

|

We received several comments from groups with a shareholder focus that did not support notice-and-access. Two commentators were very concerned that notice-and-access would be an obstacle to informed voting by requiring beneficial owners to take additional steps to access the information circular. One of the commentators stated that fundamental changes needed to be made to the procedures, and said that the proposal as currently designed should not be adopted. |

We are, however, proposing several changes to the notice-and-access procedures we originally proposed in order to address concerns that notice-and-access will be an obstacle to voting, particularly by retail shareholders. |

|

|

||

|

|

We received one comment that was neither in favour of nor opposed to notice-and-access, but that recommended that the CSA should monitor the effect of notice-and-access on the participation of Canadian retail shareholders, with the aim of holding voting participation rates at 2010 levels or increasing them. |

We now propose that reporting issuers who use notice-and-access must provide advance notification before they use notice-and-access for the first time; and explanatory material on notice-and-access must be included in the notice package along with the notice and voting instruction form. |

|

|

||

|

|

|

We also propose to permit registered holders and beneficial owners to provide standing instructions on whether they wish to receive paper copies of information circulars in all instances where a reporting issuer is using notice-and-access. |

|

|

||

|

2. |

Whether notice-and-access should be available for special meetings under NI 54-101 |

|

|

|

||

|

|

Only one comment supported restricting notice-and-access to meetings that are not special meetings under NI 54-101 and to only extend it to all meetings until the impact of notice-and-access on voting participation rates had been demonstrated. |

We agree with the large majority of comments that notice-and-access should be available for all meetings, not just special meetings. We therefore propose to eliminate this restriction. In addition, we also propose additional companion policy guidance on what factors reporting issuers should consider when deciding whether to use notice-and-access. |

|

|

||

|

|

All other comments disagreed with restricting notice-and-access to meetings that are not special meetings. |

|

|

|

||

|

|

The comments expressed the following concerns regarding the proposed restriction: |

|

|

|

||

|

|

(a) it would add an additional layer of complexity to an already complex system; |

|

|

|

||

|

|

(b) the distinction between special and non-special meetings is not meaningful in many cases, as controversial matters are often voted on at non-special meetings (e.g., the case of proxy contests); |

|

|

|

||

|

|

(c) it could perpetuate a view that the election of directors and (re)appointment of auditors require less attention; |

|

|

|

||

|

|

(d) it would significantly reduce the number of meetings for which notice-and-access could be used, thus significantly reducing the efficiency gains for the beneficial owner communication process. |

|

|

|

||

|

3. |

Whether there should be a prescribed form of notice |

|

|

|

||

|

|

Comments were divided on this issue. |

Regardless of whether commentators supported a prescribed or standardized form, all commentators appeared to agree that the notice should contain basic information about the matters to be voted on, and that investor confusion should be minimized. |

|

|

||

|

|

Those who supported a prescribed or standardized form of notice expressed concern that lack of specific requirements could create inconsistency between proxy-related materials and result in shareholder confusion. |

With the above objectives in mind, we have revised the proposal to specify that the notice must only state certain information. With respect to matters being voted on at the meeting, the notice must only state each matter or group of related matters to be voted on as identified in the form of proxy. This will facilitate consistency between the notice and other proxy-related materials, as well as standardization of the notice among issuers, both of which are intended to minimize investor confusion. We also propose companion policy guidance that states our expectations that reporting issuers draft the items to be voted on in the proxy in a clear and user-friendly manner. |

|

|

||

|

|

Those who did not think that a prescribed or standardized form was necessary noted that as long as the basic information about matters to be voted on was provided, it would be appropriate to provide additional information. |

|

|

|

||

|

4. |

Whether additional information (that is not an information circular) can be provided with the notice |

|

|

|

||

|

|

Comments were divided on this issue. Most commentators shared a concern that additional materials could be confusing and in some cases, intentionally or unintentionally inaccurate or misleading. One comment suggested mandating a plain language summary of the notice with all relevant voting information. Another comment suggested prescribing rules regarding the type, tone, content and purpose of additional materials. One comment also proposed requiring any additional materials to be provided to all investors, regardless of how the materials were delivered. |

We think that permitting additional materials to be included in the notice-and-access package without any prescribed rules around type, tone, content and purpose could contribute to investor confusion. Furthermore, we are concerned that providing such additional materials without the information circular encourages shareholders not to review the information circular. We therefore propose to prohibit additional material from being included in the notice-and-access package without an information circular also being included. |

|

|

||

|

5. |

Whether notice-and-access can be used only in respect of some beneficial owners |

|

|

|

||

|

|

Comments were divided on this issue. Some comments expressed concern that selective use of notice-and-access would be confusing to shareholders, and in some cases could be used to manipulate voting outcomes by reporting issuers. Other comments viewed selective use of notice-and-access as being consistent with effective communication with shareholders while maximizing cost efficiencies in the communication process. |

In order to minimize the complexity of the system and investor confusion, we propose that an issuer that uses notice-and-access under NI 54-101must use it in respect of all its beneficial owners (subject to any alternate delivery methods such as e-mail delivery to which the shareholder has consented or may consent). However, the issuer can choose to include a paper copy of the information circular in the notice package that is delivered to a subset of its shareholders. We have added a definition of "stratification" to describe these procedures. |

|

|

||

|

|

One comment noted that there is a distinction to be made between selective use of notice-and-access, and "stratification". Stratification refers to procedures whereby an issuer that uses notice-and-access includes paper copies of the information circular in the notice package sent to a subset of beneficial owners. |

We think that stratification as part of notice-and-access can be consistent with effective communication while maximizing cost efficiencies in the communication process. However, in order to increase transparency, we propose to require that stratification criteria be disclosed in the notification of meeting and record dates required by s. 2.2 of NI 54-101, the notice-and-access explanation required by s. 2.7.1(1)(a)(ii), and the information circular. We also propose companion policy guidance that states our expectation that a reporting issuer will use stratification in order to enhance effective communication, and not to disenfranchise shareholders. |

|

|

||

|

6. |

Costs and benefits of notice-and-access |

|

|

|

||

|

|

Comments were divided on whether notice-and-access would result in cost savings to the Shareholder Voting Communication Process. Some commentators were of the view that notice-and-access would result in significant cost savings, while others were of the view that it would depend on the particular circumstances of the issuer. One commentator noted that notice-and-access also had costs associated with building and maintaining the infrastructure, lost economies of scale in printing and mailing materials and cost transfers to investors to access and print materials. In addition, several comments expressed concern that potential cost savings of notice-and-access would not be passed on to issuers absent regulatory intervention on fees charged by service providers. |

Based on the comments, it appears that the potential for costs savings will depend on a number of factors. For example, one issuer provided an estimate of $75,000 to $500,000 in savings (depending on the type of meeting), while another estimated savings of $500,000 to $700,000. |

|

|

||

|

|

An intermediary service provider noted that on a proportional basis, the opportunity for significant cost savings for issuers in Canada is likely to be less than that seen in the U.S. Issuers in Canada have already received cost savings due to regulatory changes. In particular, reporting issuers are not required to send annual financial statements and annual MD&A to all registered holders and beneficial owners if they use the annual request form mechanism in NI 51-102. |

We acknowledge concerns that the notice-and-access process not be overly complicated and expensive to design and maintain, and therefore have proposed a number of changes that are intended to streamline and standardize the procedures. With regard to the issue of service provider fees, we note that the use of notice-and-access is voluntary, and that it is up to each reporting issuer to assess whether fees charged in connection with notice-and-access will be sufficiently offset by the savings associated with printing and mailing. |

|

|

||

|

|

The same intermediary service provider also noted that it is unclear at this stage whether building and maintaining a notice-and-access system is justified given the potential number of corporations that may use the proposed notice-and-access procedures. It also noted that notice-and-access as an additional option for distribution of proxy-related materials, can increase cost and complexity for participants in the Shareholder Voting Communication Process. |

|

|

|

||

|

7. |

Whether notice-and-access is adequately integrated with the process for requesting copies of financial statements and MD&A |

|

|

|

||

|

|

The comments received on this issue were divided, although a small majority took the view that the two processes could be better integrated. |

We have made the following changes in response to the comments: |

|

|

||

|

|

|

(a) We propose to permit proxy-related materials to be filed on or prior to the day the notice is sent. This will enable a reporting issuer to both incorporate by reference the information circular in its AIF (by filing the information circular prior to filing its AIF, annual financial statements and annual MD&A); and send a single set of proxy-related materials that includes the annual financial statements and annual MD&A. |

|

|

||

|

|

|

(b) We propose to amend NI 51-102 so that an annual request form used to request the annual financial statements and MD&A will also constitute a request for a paper copy of the information circular where the reporting issuer uses notice-and-access. |

|

|

||

|

|

|

(c) We propose to reduce the period that a reporting issuer is obligated to fulfil requests for annual or interim financial statements and annual or interim MD&A to one year from the date that the materials were filed, which is consistent with the proposed provision that a reporting issuer is only required to fulfil a request for a paper information circular one year from the date of the meeting to which it relates. |

|

|

||

|

8. |

Requirement that reporting issuer issue news release regarding use of notice-and-access |

|

|

|

||

|

|

The majority of comments questioned the utility of the news release requirement. One comment noted that the information required in the news release should be drafted to refer to both registered holders and beneficial owners. |

We propose several changes as to how shareholders learn about a reporting issuer's use of notice-and-access. First, we propose a new requirement that a reporting issuer provide advance notice three to six months before the first meeting where notice-and-access is used by issuing a news release and posting information on a website that is not SEDAR. Second, we propose that information regarding notice-and-access subsequently be disseminated in the notification of meeting required in s. 2.2(2) of NI 54-101. Finally, the information to be disclosed must be in respect of both registered holders and beneficial owners. |

|

|

||

|

9. |

Requirement that reporting issuer post "document with same information" on non-SEDAR website |

|

|

|

||

|

|

One comment noted that this requirement should be redrafted to require that the reporting issuer post the "information circular" on the non-SEDAR website. |

We are adopting the suggested change. |

|

|

||

|

10. |

Requirement that reporting issuer provide "information" to the intermediary |

|

|

|

||

|

|

One comment requested that this requirement be redrafted to clarify that the reporting issuer must provide the materials for forwarding, as the provision as currently drafted would require intermediaries to be responsible for producing the required notice. |

We are adopting the suggested change. |

|

|

||

|

11. |

Requirement that requests for paper copies of information circular be fulfilled within 3 business days |

|

|

|

||

|

|

One comment recommended that the requirement should only apply if a request is received at least 3 business days prior to the meeting. Another comment requested that guidance be provided on how to deal with last-minute requests. |

In our view, it is appropriate for any request for an information circular that is received on or before a meeting date to be fulfilled in a prompt manner. We therefore are not proposing to change the 3 business day fulfillment requirement. We also propose to require that first class mail, courier or the equivalent be used in those cases. However, we propose to permit requests received after the date of the meeting to be fulfilled within 10 calendar days and by prepaid mail other than first class mail, which is consistent with the new proposed fulfillment time frames for annual financial statements and annual MD&A. The new proposed mandatory notice-and-access explanation must contain information about when requests should be received in order for the requester to receive the paper copy in advance of any deadline for the submission of voting instructions and the date of the meeting. |

|

|

||

|

12. |

Requirement not to "obtain" information when fulfilling requests for paper copies |

|

|

|

||

|

|

One comment requested a change from the word "obtain" to "request". |

We have adopted the suggested change. |

|

|

||

|

13. |

Use of term "enable" in context of prohibition against identification of person accessing website where materials are posted |

|

|

|

||

|

|

One comment stated that the proposed prohibition against a reporting issuer using any means that would "enable" the reporting issuer to identify a person or company is too broad, and recommended that the provision be changed to read that the reporting issuer "must not collect" such information. |

We have adopted the suggested change. |

|

|

||

|

14. |

Reporting issuer must send notice and post materials on non-SEDAR website at least 30 days before the meeting and on same day that notice package is sent |

|

|

|

||

|

|

One comment stated that the 30-day period was too far in advance of the meeting, and that sending of the notice and posting of materials should be able to take place at least 21 days before the meeting. |

We are not adopting the suggestion regarding reducing the 30-day period as we continue to take the view that 30 days is an appropriate period to reasonably enable shareholders who receive the notice to request and obtain a paper copy of the information circular if they wish. |

|

|

||

|

|

One comment raised a concern that the requirement that the notice be sent out on the same day that the proxy-related materials are made publicly available through filing on SEDAR could result in reporting issuers having to choose between mailing the annual financial statements and annual MD&A with the notice, and incorporating disclosure from the information circular in the AIF. |

We have adopted the change suggested to permit the proxy-related materials to be filed on SEDAR on or before the day the notice package is sent. |

|

|

||

|

15. |

No specific time frame mandated for when intermediaries must receive notice materials for sending to beneficial owners |

|

|

|

||

|

|

One comment recommended that there be a specific time frame mandated for when intermediaries must receive notice materials where the reporting issuer is sending the materials indirectly to beneficial owners. |

We propose that the time frames now track the time frames that apply to standard mailings of proxy-related materials. See s. 2.12 of NI 54-101. |

|

|

||

|

16. |

No provision that permits beneficial owners to provide standing instructions to receive paper copy of information circular |

|

|

|

||

|

|

Two comments suggested that there should be provision for beneficial owners to give standing instructions that they wish to receive paper copies of information circulars in every case. One commentator noted that under the SEC notice-and-access rules, investors are permitted to give standing instructions to receive paper copies of meeting materials, and that statistics indicate that those investor who give these instructions tend to vote more often than the average retail investor. |

We are adopting this suggestion. We propose that reporting issuers be permitted to obtain standing instructions in respect of registered holders, and that intermediaries be permitted to obtain standing instructions in respect of beneficial owners. We considered proposing that reporting issuers be permitted to obtain standing instructions from beneficial owners, but were not able to envision how reporting issuers could implement a mechanism to obtain, maintain and execute such instructions given the current infrastructure whereby intermediaries are primarily responsible for collecting and maintaining beneficial owner shareholder communication data. We therefore are not proposing such a provision at this time. |

|

|

||

|

17. |

Reporting issuers who use notice-and-access are not required to pay for delivery to OBOs |

|

|

|

||

|

|

One comment stated that reporting issuers who use notice-and-access should be required to pay for delivery of the notice to OBOs. See also Issue/Comment 32, which relates to reporting issuers not being required to pay for delivery to OBOs generally. |

We are not adopting this suggestion. The notice-and-access proposal is not intended to address the general question of how the cost of delivering proxy-related materials to OBOs should be allocated. However, we strongly encourage those reporting issuers who use notice-and-access to pay for delivery of the notice package to OBOs. |

|

|

||

|

18. |

Integrating other delivery methods with notice-and-access (s. 2.7(2)(c) and 4.2(2)(c) of NI 54-101 in the Original Materials) |

|

|

|

||

|

|

One comment noted that it was unclear what other delivery methods are being contemplated and how they would be integrated into the beneficial owner communication process. |

We are removing the originally proposed sections that enumerate the permitted delivery methods for proxy-related materials as these provisions are no longer necessary. We also are removing the reference to delivery methods other than prepaid mail, courier or the equivalent for the notice package. |

|

|

||

|

19. |

Exemption for SEC issuers who use U.S. notice-and-access |

|

|

|

||

|

|

A comment identified several technical issues with the proposed exemption for SEC issuers, including how the exemption would interact with the obligations of intermediaries subject to obligations under NI 54-101, but who might not be subject to the U.S. notice-and-access rules. |

The proposed exemption is revised as follows: |

|

|

||

|

|

|

(a) We propose to eliminate the original condition that the SEC issuer obtain confirmation from each intermediary that it will "comply" with the U.S. notice-and-access rules, and replace it with a condition that the issuer arrange with each intermediary to send the materials using the U.S. notice-and-access procedures; |

|

|

||

|

|

|

(b) We narrow the application of the exemption to SEC issuers that have a limited Canadian presence; |

|

|

||

|

|

|

(c) We expand the exemption to apply to any intermediary that, at the request of an SEC issuer, uses U.S. notice-and-access procedures to deliver proxy-related materials to beneficial owners. |

|

|

||

|

20. |

No consequential amendments to Form 54-101F2 |

|

|

|

||

|

|

||

|

|

Two comments requested that the Form 54-101F2 Request for Beneficial Ownership Information be amended to reflect the changes proposed in NI 54-101 relating to notice-and-access and also require the issuer to indicate which method(s) of delivery were going to be used, i.e., direct delivery to NOBOs, indirect delivery to both types of beneficial owners, selective/complete use of N&A, etc. |

We are adopting this suggestion. We note that some of the information listed is already required to be provided in Form 54-01F2, i.e., Items 7.4 and 10 of Part 1 -- Reporting issuer Information. |

|

|

||

|

Repeal of legal proxy provisions and appointment of beneficial owner or its nominee as proxy holder |

||

|

|

||

|

21. |

Reporting issuer must provide confirmation in a format that is acceptable to the intermediary that reporting issuer will appoint the NOBO as proxy holder where NOBO has so requested |

|

|

|

||

|

|

One comment noted that the clause as drafted could result in multiple confirmation formats, and recommended that it not be at the sole discretion of the intermediary. Furthermore, the clause as drafted also could permit an intermediary to demand confirmation of every proxy appointment submitted on behalf of its clients. This could create logistical issues, especially on meetings for large reporting issuers during the height of meeting season. |

We removed the requirement that the confirmation be in a format acceptable to the intermediary. We also have added a new provision that clarifies that the confirmation does not need to specify every proxy appointment submitted, and that it is sufficient simply to identify the meeting to which the confirmation applies. |

|

|

||

|

22. |

Beneficial owner or nominee that is appointed as proxy holder does not have power of attorney to act as principal with authority to vote on all matters before the meeting |

|

|

|

||

|

|

Issuers should clearly outline in the information circular and on the form of proxy/VIF that the appointee will have authority to present matters to the meeting and to vote on all matters brought before the meeting. Furthermore, issuers should clearly state this fact in the voting instruction form/form of proxy and the information circular. |

We have added a provision that the appointee has full authority to present matters to the meeting and vote on all matters that are presented at the meeting, even if these matters are not set out in the VIF or the information circular. |

|

|

||

|

23. |

No specific mechanism outlined for appointing a beneficial owner to attend and vote at a meeting |

|

|

|

||

|

|

One comment requested that there should be a specific mechanism outlined in NI 54-101 for appointing a beneficial owner to attend and vote at a meeting. |

We are not adopting this change. However, as we noted in the notice accompanying the Original Materials, the appointee system has been developed and in place for some time, and we are adding a discussion of it in the companion policy. |

|

|

||

|

24. |

Obligation to deposit proxy by proxy cut-off |

|

|

|

||

|

|

A comment requested that the requirement to deposit the proxy by the proxy cut-off pursuant to voting instructions from a beneficial owner only apply where the voting instructions were received at least one business day prior to the proxy cut-off. |

We are adopting this suggestion. However, we propose companion policy guidance that we expect that reporting issuers and intermediaries will make best efforts to deposit the proxy even if the instructions are obtained less than one business day before the proxy cut-off. |

|

|

||

|

Enhanced disclosure of proxy voting process in information circular |

||

|

|

||

|

25. |

Requirement to disclose where notice-and-access used only for some beneficial owners |

|

|

|

||

|

|

Comments were divided on the whether the disclosure would be helpful to shareholders. |

We continue to take the view that this disclosure is helpful to shareholders. We have made changes to the proposed requirement so that the disclosure regarding stratification is in respect of registered holders and beneficial owners. We also propose to require that the information be disclosed earlier, when the issuer files the notification of meeting. |

|

|

||

|

26. |

Requirement to disclose non-payment for delivery to OBOs |

|

|

|

||

|

|

One comment supported disclosure, while two comments questioned the utility of the disclosure. One of the latter two comments noted that the more fundamental issue was the potential that an OBO would not receive proxy-related materials as a result of the reporting issuer not paying for OBO delivery. The second comment suggested that the disclosure of non-payment should be included in the press release. |

As noted in our responses to Issue/Comment 17 and 32, we do not intend to address the issue of requiring reporting issuers to pay for delivery to OBOs as part of the Proposals. We are maintaining the proposed disclosure requirement, but also propose to require reporting issuers to disclose whether they will pay for OBOs in the notification of meeting. |

|

|

||

|

Use of NOBO information |

||

|

|

||

|

27. |

Increased restrictions on use of NOBO information |

|

|

|

||

|

|

The comments were generally supportive, although one comment questioned why such restrictions were necessary. One comment suggested that issuers, intermediaries and subcontractors be required to adopt specific privacy standards, such as those in PIPEDA and the Canadian Standards Association's Model Code. |

We continue to think that the restrictions are appropriate. We are not adopting the suggestion regarding adoption of specific privacy standards. We expect issuers, intermediaries and service providers to comply with their obligations under privacy legislation, and encourage adoption of appropriate best practices. |

|

|

||

|

Requests for beneficial ownership information |

||

|

|

||

|

28. |

Permitting non-transfer agents to request beneficial ownership information on behalf of reporting issuers |

|

|

|

||

|

|

Comments generally supported this proposed amendment. One comment suggested that s. 2.5(4) be eliminated completely, as information can be delivered using a variety of media and by direct electronic exchange with a much wider array of parties than was anticipated when the original provision was drafted. In the alternative, the assessment regarding technological capacity should be made by the intermediary, as it is the party providing the information. |

We continue to think that issuers and third parties should be able to obtain NOBO lists directly (subject to the permitted purposes for obtaining NOBO lists, and permitted uses of NOBO lists in NI 54-101). We therefore propose changes to the provision that clarify that a reporting issuer can request a NOBO list without using a transfer agent provided the intermediary reasonably believes that the reporting issuer (or the person or company making the request on its behalf) has the technological capacity to receive the information. We note that the client response reform does not indicate that beneficial ownership information will only be released to a transfer agent. |

|

|

||

|

|

However, one comment strongly disagreed with the proposed amendment, noting that: |

|

|

|

||

|

|

(a) beneficial owners completing their client response form do not have the expectation that their information would be accessible to non-transfer agents; and |

|

|

|

||

|

|

(b) transfer agents are trusted entities that are recognized by the regulator and exchanges and are active participants in the daily affairs of publicly traded companies. |

|

|

|

||

|

Miscellaneous comments |

||

|

|

||

|

29. |

Requirement for issuers/intermediaries to retain a record of the Form 54-101F6/7 and the date and time of any voting instructions and proxy appointment |

|

|

|

||

|

|

One comment was supportive of this requirement. However, other comments took the view that the proposed requirements were unclear. For example, one comment noted that the purpose of the proposed requirement was unclear. If the aim was to generate an audit trail for voting, then the recordkeeping requirements should go further to mandate keeping the date(s) the materials were sent to investors, full details of the instructions received and the date(s), time(s) and details of tabulated votes that were sent by an intermediary to the issuer. If the longer term aim was to have a system that can confirm voting instructions and that proxies were executed as securityholders intended, then it would be less expensive and more efficient to require full records to be kept now, rather than introduce additional requirements over time, necessitating multiple systems changes. |

We propose to remove the proposed requirements at this stage. We will consider the broader issue of appropriate recordkeeping in the proxy voting system separately from the Proposals. |

|

|

||

|

30. |

Differences in definitions of special resolution and proxy-related material in NI 51-102 and NI 54-101 |

|

|

|

||

|

|

A comment noted that there were differences in the drafting of the definitions of special resolution and proxy-related material in NI 51-102 and NI 54-101. |

We propose to harmonize the definitions. |

|

|

||

|

31. |

Reasonable assurance of payment to intermediaries before mailing materials |

|

|

|

||

|

|

A comment noted that the language in Part 4 of NI 54-101 relating to the intermediary's obligation to deliver NOBO lists to issuers and proxy-related materials to beneficial owners on behalf of issuers should be amended to make the conditions contingent on the intermediary receiving reasonable assurance of payment. |

We are not proposing to adopt this change at this time. We will consider this issue separately from the Proposals. |

B. Comments on other aspects of NI 54-101

|

# |

Comments |

Response |

|

|

||

|

32. |

Issuers should pay for delivery to OBOs under all circumstances. |

We are not adopting this suggestion at this time. We will consider the issue of whether NI 54-101 should require reporting issuers to deliver to OBOs separately from the Proposals. |

|

|

||

|

33. |

NI 54-101 needs to be strengthened to make intermediaries more accountable. |

We are not adopting this suggestion at this time. We will consider this issue separately from the Proposals. |

|

|

||

|

34. |

For special meetings as defined in NI 54-101, materials should be sent 45 days in advance. |

We are not adopting this suggestion as we continue to take the view that 21 days (30 days where notice-and-access is used) is an appropriate period. We note that existing companion policy guidance states that for meetings that deal with contentious matters, good corporate practice will often require that meeting materials be sent earlier than the time frames set out in NI 54-101 so that shareholders have the full opportunity to understand and react to matters raised. |

|

|

||

|

35. |

NOBO status should be the default for beneficial owners; shareholders who wish to remain anonymous must sign waiver of right to receive materials directly. |

We are not adopting this suggestion at this time. We will consider issues generally related to OBO and NOBO status separately from the Proposals. |

|

|

||

|

36. |

Issuers should not be able to override a security holder's choice not to receive materials. In the alternative, securityholders who have declined to receive materials altogether should only be sent a notice package under notice-and-access. |

We are not adopting this suggestion, as we think that reporting issuers are entitled to contact securityholders in connection with voting matters. Nor do we propose to effectively prohibit a reporting issuer from sending a beneficial owner a paper copy of the information circular. However, we encourage issuers to consider whether notice-and-access and stratification can be used to enhance effective communication in the beneficial owner communication process by sending notice-only packages to securityholders who do not wish to receive materials, and including paper copies of the information circulars in notice packages for shareholders who do wish to receive materials. |

|

|

||

|

37. |

Include FINS number in the NOBO list where it is requested by a person other than the reporting issuer. |

We are not adopting this suggestion at this time. We will consider this issue separately from the Proposals. |

|

|

||

|

38. |

OBOs and NOBOs should not be treated in the same manner where it is possible for NOBOs to be treated more like registered shareholders. The Original Materials should be amended to reflect this principle. Issuers should be allowed to provide NOBOs with a form of proxy rather than a request for voting instructions using the STAC protocol for NOBO omnibus proxies. |

We are not adopting this suggestion at this time. We will consider the issue of whether NOBOs should be treated more like registered holders separately from the Proposals. |

|

|

||

|

39. |

NI 54-101 should mandate that any party that has carriage of mailing (such as the transfer agents or Broadridge) file with the CSA and on SEDAR a confirmation that the mailing was completed in accordance with the requirements of NI 54-101. |

We are not adopting this suggestion at this time. We will consider this issue separately from the Proposals. |

|

|

||

|

40. |

Any party involved in the beneficial owner voting process should be entitled to rely upon the consent to electronic delivery of material obtained by another party. |

We are not adopting this suggestion at this time. We will consider this issue separately from the Proposals. |

C. Comments on the proxy voting system generally

|

# |

Comment |

Response |

|

|

||

|

41. |

There needs to be a clear voting audit trail. Consideration should be given to requiring a regulatory or independent audit of meetings where the vote was determined by a narrow margin. |

We thank the commentators for their suggestions on areas where the proxy voting system requires regulatory attention. Although we are not proposing any specific regulatory initiatives as a result of these comments at this time, we continue to consider these comments separately from the Proposals, and what, if any, appropriate regulatory responses to take. |

|

|

||

|

42. |

Shareholders should have the right to confidentiality when voting. |

|

|

|

||

|

43. |

There needs to be a charter of shareholder rights. |

|

|

|

||

|

44. |

The regulators should send each beneficial owner a reminder form about casting votes. |

We support enhancing investor education on the proxy voting system and are considering how we as securities regulators can facilitate achieving this outcome. |

|

|

||

|

45. |

Majority voting/individual director voting should be mandatory for reporting issuers. |

|

|

|

||

|

46. |

Shareholders should have greater access to the proxy. |

|

|

|

||

|

47. |

There should be policy guidance requiring the fair allocation of votes received in respect of all beneficial owner positions at a particular intermediary. |

|

|

|

||

|

48. |

There should be a CSA proxy voting section on CSA websites similar to SEC proxy voting section/There should be an investor education campaign about the beneficial owner voting process. |

|

SCHEDULE B

REVISED PROPOSED AMENDMENT INSTRUMENT TO

NI 54-101 AND BLACKLINE TO THE ORIGINAL MATERIALS

PROPOSED AMENDMENT INSTRUMENT TO

NATIONAL INSTRUMENT 54-101

COMMUNICATION WITH BENEFICIAL OWNERS

OF SECURITIES OF A REPORTING ISSUER

1. National Instrument 54-101 Communication with Beneficial Owners of Securities of a Reporting Issuer is amended by this Instrument.

2. Section 1.1 of National Instrument 54-101 is amended by

(a) repealing the definition of "legal proxy";

(b) amending the definition of "proxy-related materials" to insert "or beneficial owners" between "registered holders" and "of the securities";

(c) adding the following definition after the definition of "non-objecting beneficial owner list":

"notice-and-access" means

(a) in respect of registered holders of voting securities of a reporting issuer, the delivery procedures referred to in section 9.1.1 of National Instrument 51-102 Continuous Disclosure Obligations;

(b) in respect of beneficial owners of securities of a reporting issuer, the delivery procedures referred to in section 2.7.1 of this Instrument;

(d) adding the following definition after the definition of "request for beneficial ownership information":

"SEC issuer" means an issuer that

(a) has a class of securities registered under section 12 of the 1934 Act or is required to file reports under section 15(d) of the 1934 Act; and