Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

CSA Notice of Amendments to National Instrument 45-106 Prospectus Exemptions Relating to Reports of Exempt Distribution

CSA Notice of Amendments to National Instrument 45-106 Prospectus Exemptions Relating to Reports of Exempt Distribution

CSA Notice of Amendments to National Instrument 45-106 Prospectus Exemptions

relating to Reports of Exempt Distribution

April 7, 2016

Introduction

The Canadian Securities Administrators (CSA or we) are making amendments (the rule amendments) to National Instrument 45-106 Prospectus Exemptions (NI 45-106) to introduce a new harmonized report of exempt distribution (the New Report).{1} We are also making related changes to Companion Policy 45-106 Prospectus Exemptions (45-106CP).

We refer to the rule amendments, the New Report and the changes to 45-106CP collectively as the Amendments.

Provided all necessary ministerial approvals are obtained, the Amendments will come into force on June 30, 2016 in all CSA jurisdictions.

Substance and Purpose

The New Report

Issuers and underwriters who rely on certain prospectus exemptions to distribute securities are required to file a report of exempt distribution within the prescribed timeframe. Currently, in all CSA jurisdictions except British Columbia, the form of report is Form 45-106F1 Report of Exempt Distribution (Form 45-106F1). In British Columbia, the form of report is Form 45-106F6 British Columbia Report of Exempt Distribution (Form 45-106F6, and together with Form 45-106F1, the Current Reports).

The Amendments replace the Current Reports with the New Report. The New Report will:

1) reduce the compliance burden for issuers and underwriters by having a harmonized report of exempt distribution, and

2) provide securities regulators with the necessary information to facilitate more effective regulatory oversight of the exempt market and improve analysis for policy development purposes.

The New Report is set out in Annex B and the changes to 45-106CP are set out in Annex C.

Key features of the New Report

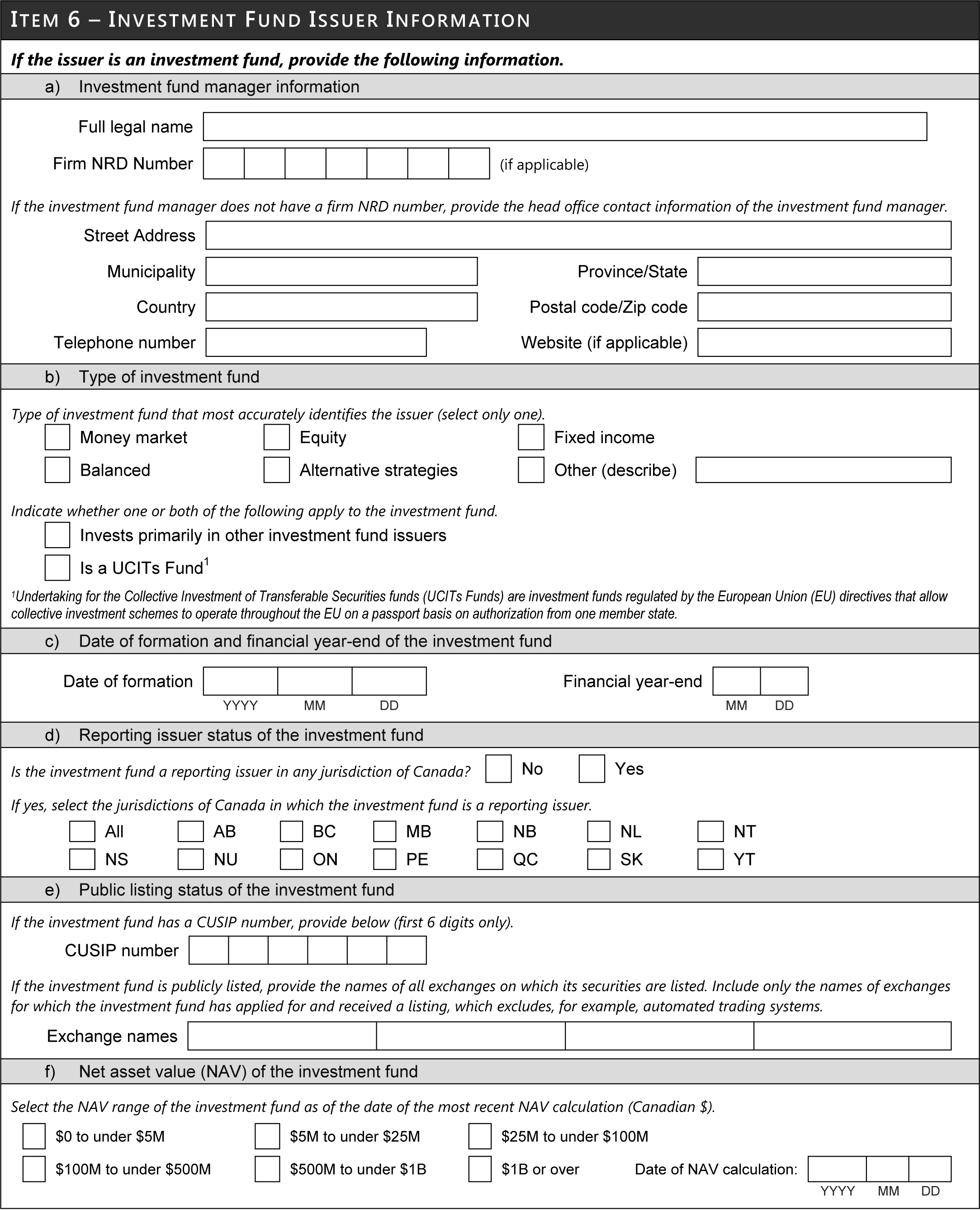

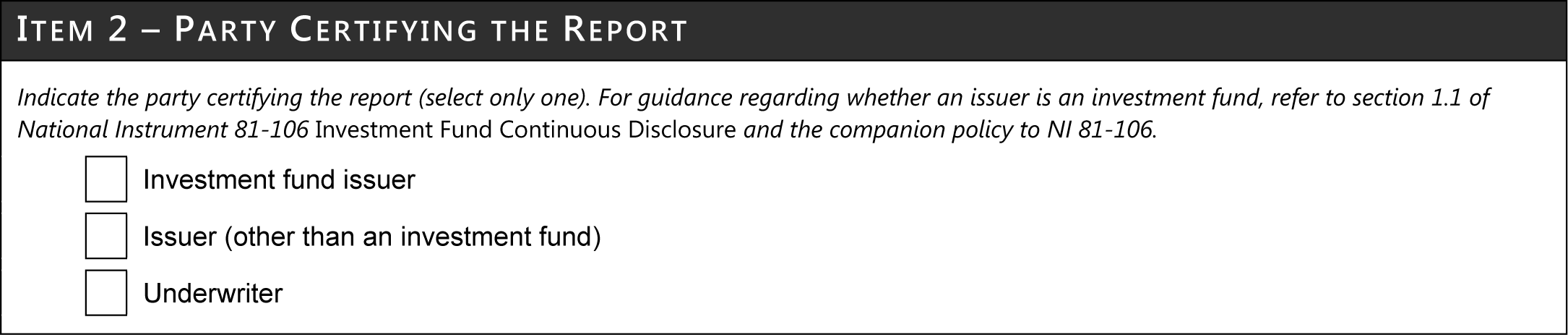

The New Report will apply in all CSA jurisdictions to both investment fund issuers and non-investment fund issuers that distribute securities under certain prospectus exemptions.

The New Report introduces new information requirements, including disclosure of the following:

• additional details about the issuer including its size and primary business activity,

• identities of the directors, executive officers and promoters of certain issuers,{2}

• identities of control persons of certain issuers in a non-public schedule,

• additional details about the securities distributed and, for certain jurisdictions, details about the documents provided in connection with the distribution,

• specific details about the prospectus exemptions relied on, both on an aggregate and per investor basis, and

• details about compensation paid to registrants, connected persons, insiders and employees of the issuer or the investment fund manager involved in the distribution.

For investment fund issuers, the New Report also requires disclosure regarding the size of the fund, the general type of the fund and net proceeds to the fund for the period for which the report is filed.

The New Report provides carve-outs from certain information requirements for:

• investment fund issuers,

• reporting issuers and their wholly owned subsidiaries,

• foreign public issuers and their wholly owned subsidiaries, and

• issuers distributing eligible foreign securities only to permitted clients.

In addition, an issuer is not required to provide certain information in the New Report if the information can be gathered through the issuer's continuous disclosure filings, the issuer's profile on the System for Electronic Document Analysis and Retrieval (SEDAR) or a registrant firm's profile on the National Registration Database (NRD).

Annex D provides a summary of the new information requirements in the New Report.

Background

The CSA published proposed amendments to NI 45-106 and the New Report for a 60-day comment period on August 13, 2015. The New Report is similar to the version published for comment.

Summary of written comments received on the New Report

The comment period expired on October 13, 2015. We received 19 written submissions. We have considered the comments received and thank all of the commenters for their input. The names of the commenters are contained in Annex E and a summary of their comments, together with our responses, is contained in Annex F. The comment letters can be viewed on the Autorité des marchés financiers website at www.lautorite.qc.ca and the Ontario Securities Commission (OSC) website at www.osc.gov.on.ca.

In developing the New Report, we also held informal consultations with advisory committees in certain CSA jurisdictions.

Prior proposals

In 2014, the CSA published two proposals related to the reports of exempt distribution:

• On February 27, 2014, the CSA published for comment proposed amendments to the Current Reports in conjunction with proposed amendments to NI 45-106 relating to the accredited investor and minimum amount investment prospectus exemptions. These proposals proposed to gather additional information related to the category of accredited investor for each purchaser, updated industry categories, and any person being compensated in connection with the distribution, including identifying the purchasers in respect of which the person received compensation.

• On March 20, 2014, Alberta, Saskatchewan, Ontario and New Brunswick published for comment two proposed forms for reporting exempt distributions: (i) proposed Form 45-106F10 Report of Exempt Distribution For Investment Fund Issuers, and (ii) proposed Form 45-106F11 Report of Exempt Distribution For Issuers Other Than Investment Funds. These proposals were intended to streamline exempt market reporting in applicable jurisdictions and obtain additional information about issuers, registrants and investors to enhance our ability to monitor exempt market activity.

Comments from these prior proposals have also informed the New Report.{3}

Summary of Changes Since Publication for Comment

After considering the written comments received on the New Report and the feedback received during our informal consultations, we have made a number of changes to the New Report from the version that was published for comment.

Annex G contains a summary of changes between the New Report and the version that was published for comment. Some of the notable changes include:

• We removed the requirement for issuers making a distribution in more than one jurisdiction of Canada to file a single report in each Canadian jurisdiction where the distribution has occurred, identifying all purchasers. Notwithstanding this change, issuers may continue to satisfy their obligation to file the report by completing a single report identifying all purchasers, and filing it in each Canadian jurisdiction where the distribution occurs.

• We removed the requirement to provide information about beneficial owners of fully managed accounts where a trust company, trust corporation or registered adviser described in paragraphs (p) or (q) of the definition of "accredited investor" in section 1.1 of NI 45-106 is deemed to be purchasing the securities as principal on behalf of a fully managed account. We only require information about the trust company, trust corporation or registered adviser.

• We removed the proposed requirement to disclose information relating to the holdings of the issuer's securities by directors, executive officers, promoters and control persons of certain issuers.

• We moved the proposed requirement to disclose information about control persons to a non-public schedule.

• We changed the transition period available to investment fund issuers that file annually.

• We introduced a requirement for issuers to file Schedules 1 and 2 in .xlsx format using the Excel templates developed by the CSA. The Excel templates, published concurrently with this Notice, are available on the website of each CSA member and at the links below.

In addition to the changes described in Annex G, we have revised the guidance in 45-106CP, which is set out in Annex C.

We do not consider the changes made since the publication for comment to be material and therefore are not publishing the New Report for a further comment period.

Filing Systems

Issuers are required to file the New Report electronically in all CSA jurisdictions, except certain foreign issuers when filing on SEDAR.

The British Columbia Securities Commission (BCSC) is developing a web-based filing system on eServices to accommodate the structured data format of the New Report. Beginning on June 30, 2016, when the New Report is effective, issuers filing in both British Columbia and Ontario will file the New Report with the BCSC and OSC by completing an electronic form on the BCSC's eServices and the OSC's Electronic Filing Portal, respectively.

In all CSA jurisdictions other than British Columbia and Ontario, the New Report will be required to be filed on SEDAR, except by certain foreign issuers.{6} Both the BCSC's eServices and the OSC's Electronic Filing Portal will generate an electronic copy of the completed report, which issuers can then use to file on SEDAR, if required. As noted above, issuers are required to file Schedules 1 and 2 in .xlsx format using the Excel templates developed by the CSA.

We have revised CSA Staff Notice 45-308 (Revised) Guidance for Preparing and Filing Reports of Exempt Distribution under National Instrument 45-106 Prospectus Exemptions (Staff Notice 45-308), published concurrently with this Notice, to provide guidance on how to complete and file the New Report in the various CSA jurisdictions.

A longer-term CSA project is underway to create a single integrated filing system for reports of exempt distribution that would further reduce the regulatory burden on market participants. The integrated filing system is part of the larger CSA National Systems Renewal Program.

Transition to New Report

All issuers, other than investment fund issuers filing reports annually, must use the New Report for distributions that occur on or after June 30, 2016, when the Amendments come into force. If an issuer completes a distribution before June 30, 2016, and the deadline to file the report occurs after June 30, 2016, the issuer must file the Current Report. If an issuer completes multiple distributions on dates that occur within a 10-day period beginning before and ending after June 30, 2016, the issuer may file either the Current Report or the New Report to report such distributions.

Investment funds relying on certain prospectus exemptions may file reports of exempt distribution annually, within 30 days after the end of the calendar year. We have provided a transition period to allow investment fund issuers that file annually to file either the Current Report or the New Report for distributions that occur before January 1, 2017. For distributions that occur on or after January 1, 2017, all investment fund issuers filing annually must file the New Report.

Annex H contains further information on the transition to the New Report.

Withdrawal and Revision of CSA Staff Notices

As a result of the Amendments and the replacement of Form 45-106F6 with the New Report, CSA Staff Notice 11-316 Notice of Local Amendments -- British Columbia (Staff Notice 11-316) is no longer required. Staff Notice 11-316 will be withdrawn effective June 30, 2016.

We are publishing concurrently with this Notice a revised version of Staff Notice 45-308 to reflect the New Report.

Local Matters

Annex I is being published in any local jurisdiction that is making related changes to local securities laws, including local notices or other policy instruments in that jurisdiction.

Annexes to Notice

Annex A -- Amending Instrument for National Instrument 45-106 Prospectus Exemptions

Annex B -- Form 45-106F1 Report of Exempt Distribution (New Report)

Annex C -- Changes to Companion Policy 45-106 Prospectus Exemptions

Annex D -- Summary of New Information Requirements

Annex E -- List of Commenters

Annex F -- Summary of Comments and Responses

Annex G -- Summary of Changes to New Report Since Publication for Comment

Annex H -- Transition to the New Report

Annex I -- Local Matters

Questions

Please refer your questions to any of the following:

[Editor's Note: Annexes A and B follow on separately numbered pages; Bulletin pagination resumes with Annex C.]

{1} The Amending Instrument for NI 45-106 in Annex A includes amendments to certain sections of NI 45-106 that were not adopted in one or more CSA jurisdictions. The amendments to those sections will apply only in those CSA jurisdictions where the sections are in force.

{2} Unlike the version published for comment, the New Report does not require disclosure of information relating to the holdings of the issuer's securities by directors, executive officers, promoters and control persons.

{3}Summaries of the comments received on these prior proposals were included as part of the Notice and Request for Comment on Proposed Amendments to NI 45-106 relating to Reports of Exempt Distribution published on August 13, 2015.

{4} https://www.securities-administrators.ca/wp-content/uploads/2021/09/NI45-106F1Schedule1TemplateEngREVISED20210804.xlsx

{5} https://www.securities-administrators.ca/wp-content/uploads/2021/09/Schedule_2_Form_45-106F1_En.xlsx

{6} See Multilateral CSA Notice of Amendments to National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR) and Multilateral Instrument 13-102 System Fees for SEDAR and NRD, published on December 3, 2015.

ANNEX A

AMENDING INSTRUMENT FOR NATIONAL INSTRUMENT 45-106 PROSPECTUS EXEMPTIONS

Amendments to National Instrument 45-106 Prospectus Exemptions

1. National Instrument 45-106 Prospectus Exemptions is amended by this Instrument.

2. The Instrument is amended by adding the following section:

1.8 Designation of insider -- For the purpose of this Instrument, in Ontario, the following classes of persons are designated as insiders:

(a) a director or an officer of an issuer;

(b) a director or an officer of a person that is an insider or a subsidiary of an issuer;

(c) a person that has

(i) beneficial ownership of, or control or direction over, directly or indirectly, securities of an issuer carrying more than 10% of the voting rights attached to all the issuer's outstanding voting securities, excluding, for the purpose of the calculation of the percentage held, any securities held by the person as underwriter in the course of a distribution, or

(ii) a combination of beneficial ownership of, and control or direction over, directly or indirectly, securities of an issuer carrying more than 10% of the voting rights attached to all the issuer's outstanding voting securities, excluding, for the purpose of the calculation of the percentage held, any securities held by the person as underwriter in the course of a distribution;

(d) an issuer that has purchased, redeemed or otherwise acquired a security of its own issue, for so long as it continues to hold that security.

3. Subsection 6.1(1) is amended by adding "completed" before "report if they make the distribution".

4. Subsection 6.2(2) is amended by replacing "financial year-end of the investment fund" with "end of the calendar year".

5. Section 6.3 is amended by

(a) replacing subsection (1) with the following:

(1) The required form of report under section 6.1 [Report of exempt distribution] is Form 45-106F1., and

(b) deleting "or, in British Columbia, Form 45-106F6" from subsection (2).

6. Section 6.6 is repealed.

7. The Instrument is amended by adding the following section:

8.4.3 Transition -- investment funds -- required form of report -- Despite section 6.3, an investment fund that files a report on or before the date required by subsection 6.2(2) for a distribution that occurred before January 1, 2017 may file a report prepared in accordance with the version of Form 45-106F1 in force on June 29, 2016.

8. Form 45-106F1 is repealed and the following substituted:

Form 45-106F1 Report of Exempt Distribution

A. General Instructions

1. Filing instructions

An issuer or underwriter that is required to file a report of exempt distribution and pay the applicable fee must file the report and pay the fee as follows:

• In British Columbia -- through BCSC eServices at http://www.bcsc.bc.ca.

• In Ontario -- through the online e-form available at http://www.osc.gov.on.ca.

• In all other jurisdictions -- through the System for Electronic Document Analysis and Retrieval (SEDAR) in accordance with National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR) if required, or otherwise with the securities regulatory authority or regulator, as applicable, in the applicable jurisdictions at the addresses listed at the end of this form.

The issuer or underwriter must file the report in a jurisdiction of Canada if the distribution occurs in the jurisdiction. If a distribution is made in more than one jurisdiction of Canada, the issuer or underwriter may satisfy its obligation to file the report by completing a single report identifying all purchasers, and file the report in each jurisdiction of Canada in which the distribution occurs. Filing fees payable in a particular jurisdiction are not affected by identifying all purchasers in a single report.

In order to determine the applicable fee in a particular jurisdiction of Canada, consult the securities legislation of that jurisdiction.

2. Issuers located outside of Canada

If an issuer located outside of Canada determines that a distribution has taken place in a jurisdiction of Canada, include information about purchasers resident in that jurisdiction only.

3. Multiple distributions

An issuer may use one report for multiple distributions occurring within 10 days of each other, provided the report is filed on or before the 10th day following the first distribution date. However, an investment fund issuer that is relying on the exemptions set out in subsection 6.2(2) of NI 45-106 may file the report annually in accordance with that subsection.

4. References to purchaser

References to a purchaser in this form are to the beneficial owner of the securities.

However, if a trust company, trust corporation, or registered adviser described in paragraph (p) or (q) of the definition of "accredited investor" in section 1.1 of NI 45-106 has purchased the securities on behalf of a fully managed account, provide information about the trust company, trust corporation or registered adviser only; do not include information about the beneficial owner of the fully managed account.

5. References to issuer

References to "issuer" in this form include an investment fund issuer and a non-investment fund issuer, unless otherwise specified.

6. Investment fund issuers

If the issuer is an investment fund, complete Items 1-3, 6-8, 10, 11 and Schedule 1 of this form.

7. Mortgage investment entities

If the issuer is a mortgage investment entity, complete all applicable items of this form other than Item 6.

8. Language

The report must be filed in English or in French. In Québec, the issuer or underwriter must comply with linguistic rights and obligations prescribed by Québec law.

9. Currency

All dollar amounts in the report must be in Canadian dollars. If the distribution was made or any compensation was paid in connection with the distribution in a foreign currency, convert the currency to Canadian dollars using the daily noon exchange rate of the Bank of Canada on the distribution date. If the distribution date occurs on a date when the daily noon exchange rate of the Bank of Canada is not available, convert the currency to Canadian dollars using the most recent closing exchange rate of the Bank of Canada available before the distribution date. For investment funds in continuous distribution, convert the currency to Canadian dollars using the average daily noon exchange rate of the Bank of Canada for the distribution period covered by the report.

If the Bank of Canada no longer publishes a daily noon exchange rate and closing exchange rate, convert foreign currency using the daily single indicative exchange rate of the Bank of Canada in the same manner described in each of the three scenarios above.

If the distribution was not made in Canadian dollars, provide the foreign currency in Item 7(a) of the report.

10. Date of information in report

Unless otherwise indicated in this form, provide the information as of the distribution end date.

11. Date of formation

For the date of formation, provide the date on which the issuer was incorporated, continued or organized (formed). If the issuer resulted from an amalgamation, arrangement, merger or reorganization, provide the date of the most recent amalgamation, arrangement, merger or reorganization.

12. Security codes

Wherever this form requires disclosure of the type of security, use the following security codes:

Security code

Security type

BND

Bonds

CER

Certificates (including pass-through certificates, trust certificates)

CMS

Common shares

CVD

Convertible debentures

CVN

Convertible notes

CVP

Convertible preferred shares

DEB

Debentures

FTS

Flow-through shares

FTU

Flow-through units

LPU

Limited partnership units

NOT

Notes (include all types of notes except convertible notes)

OPT

Options

PRS

Preferred shares

RTS

Rights

UBS

Units of bundled securities (such as a unit consisting of a common share and a warrant)

UNT

Units (exclude units of bundled securities, include trust units and mutual fund units)

WNT

Warrants

OTH

Other securities not included above (if selected, provide details of security type in Item 7d)

B. Terms used in the form

1. For the purposes of this form:

"designated foreign jurisdiction" means Australia, France, Germany, Hong Kong, Italy, Japan, Mexico, the Netherlands, New Zealand, Singapore, South Africa, Spain, Sweden, Switzerland or the United Kingdom of Great Britain and Northern Ireland;

"eligible foreign security" means a security offered primarily in a foreign jurisdiction as part of a distribution of securities in either of the following circumstances:

(a) the security is issued by an issuer

(i) that is incorporated, formed or created under the laws of a foreign jurisdiction,

(ii) that is not a reporting issuer in a jurisdiction of Canada,

(iii) that has its head office outside of Canada, and

(iv) that has a majority of the executive officers and a majority of the directors ordinarily resident outside of Canada;

(b) the security is issued or guaranteed by the government of a foreign jurisdiction;

"foreign public issuer" means an issuer where any of the following apply:

(a) the issuer has a class of securities registered under section 12 of the 1934 Act;

(b) the issuer is required to file reports under section 15(d) of the 1934 Act;

(c) the issuer is required to provide disclosure relating to the issuer and the trading in its securities to the public, to security holders of the issuer or to a regulatory authority and that disclosure is publicly available in a designated foreign jurisdiction;

"legal entity identifier" means a unique identification code assigned to the person

(a) in accordance with the standards set by the Global Legal Entity Identifier System, or

(b) that complies with the standards established by the Legal Entity Identifier Regulatory Oversight Committee for pre-legal entity identifiers;

"permitted client" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

"SEDAR profile" means a filer profile required under section 5.1 of National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR).

2. For the purposes of this form, a person is connected with an issuer or an investment fund manager if either of the following applies:

(a) one of them is controlled by the other;

(b) each of them is controlled by the same person.

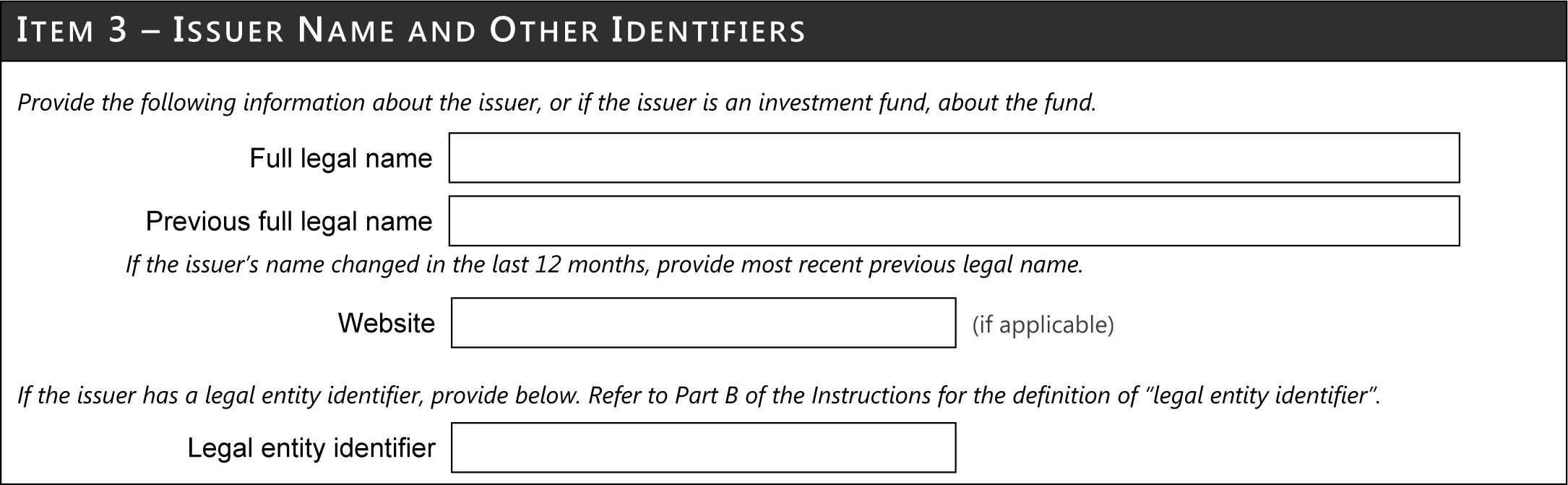

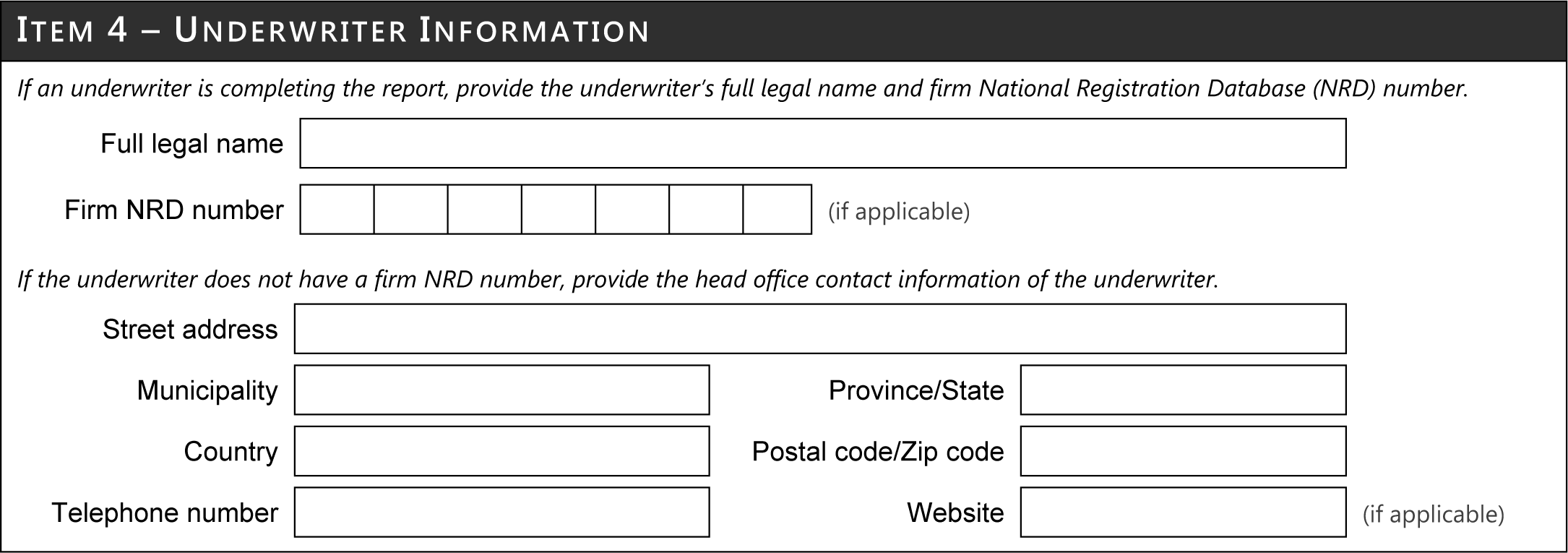

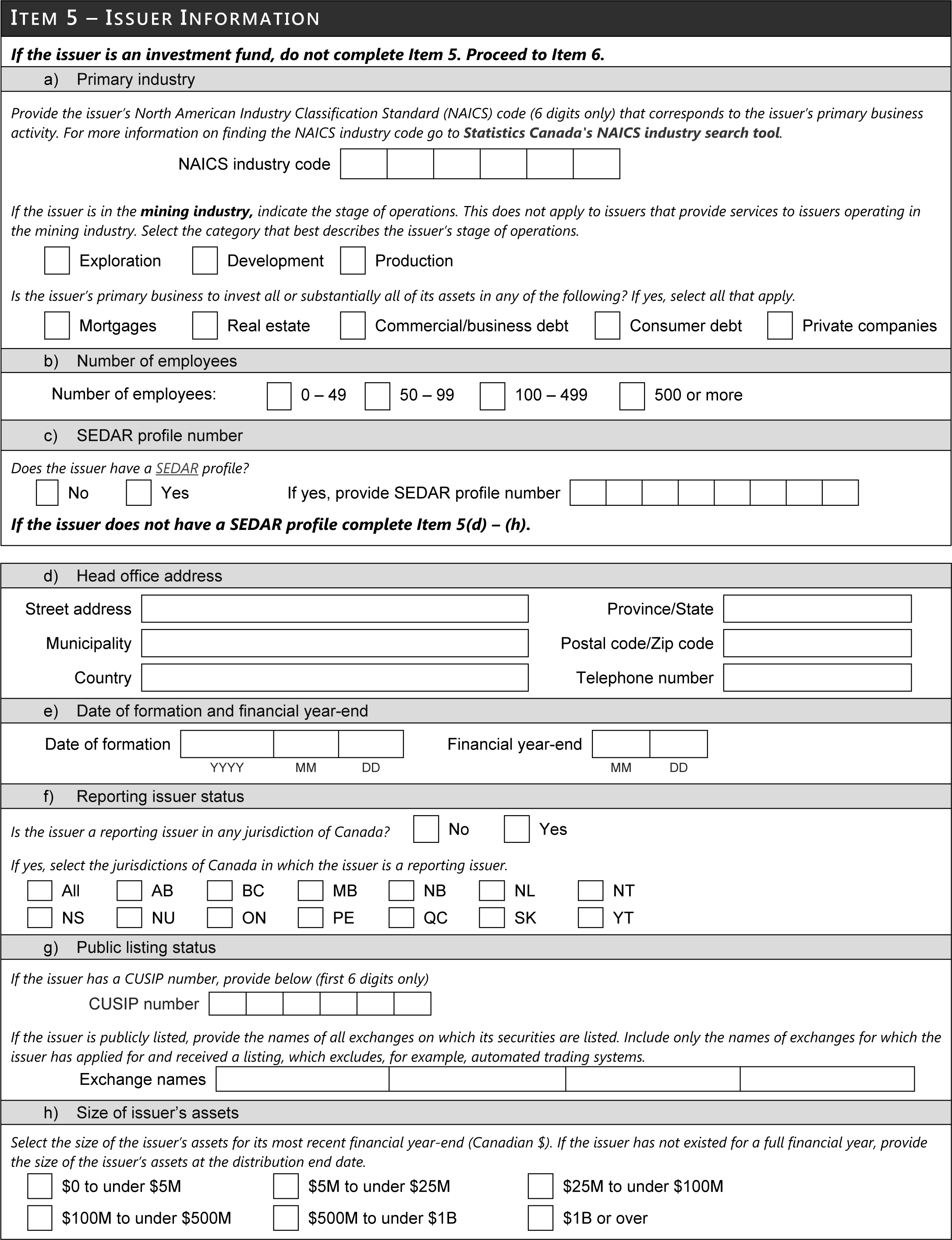

Form 45-106F1 Report of Exempt Distribution

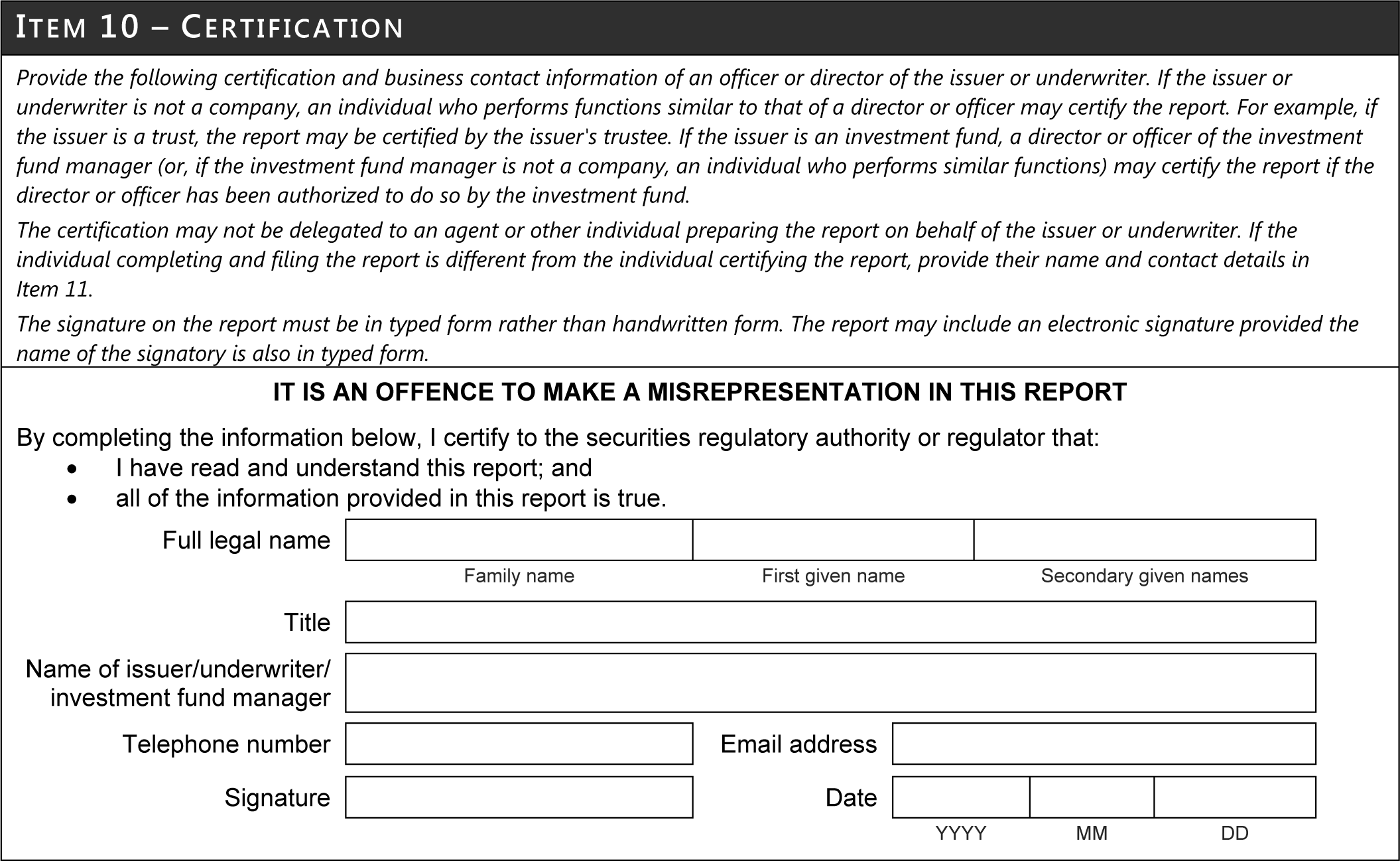

IT IS AN OFFENCE TO MAKE A MISREPRESENTATION IN THIS REPORT

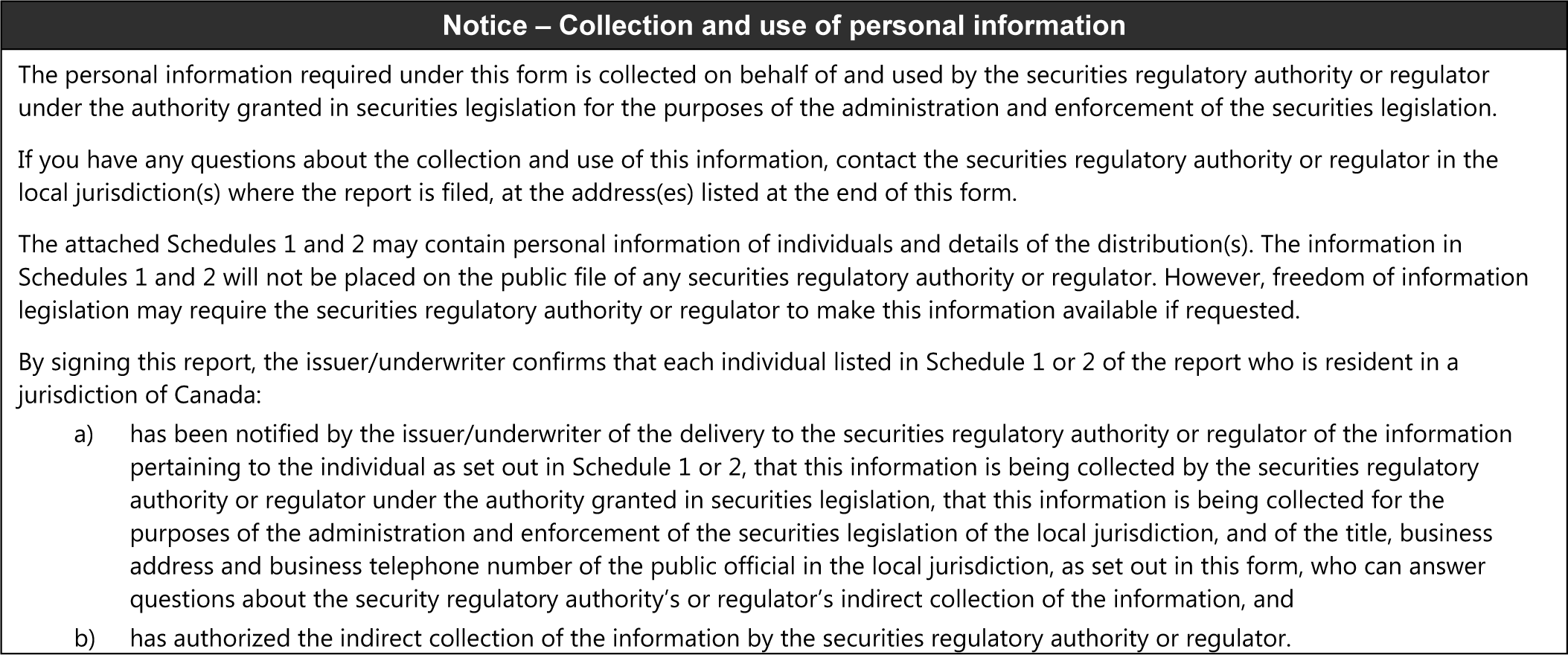

SCHEDULE 1 TO FORM 45-106F1 (CONFIDENTIAL PURCHASER INFORMATION)

Schedule 1 must be filed in the format of an Excel spreadsheet in a form acceptable to the securities regulatory authority or regulator.

The information in this schedule will not be placed on the public file of any securities regulatory authority or regulator. However, freedom of information legislation may require the securities regulatory authority or regulator to make this information available if requested.

a) General information (provide only once)

1. Name of issuer

2. Certification date (YYYY-MM-DD)

Provide the following information for each purchaser that participated in the distribution. For each purchaser, create separate entries for each distribution date, security type and exemption relied on for the distribution.

b) Legal name of purchaser

1. Family name

2. First given name

3. Secondary given names

4. Full legal name of non-individual (if applicable)

c) Contact information of purchaser

1. Residential street address

2. Municipality

3. Province/State

4. Postal code/Zip code

5. Country

6. Telephone number

7. Email address (if available)

d) Details of securities purchased

1. Date of distribution (YYYY-MM-DD)

2. Number of securities

3. Security code

4. Amount paid (Canadian $)

e) Details of exemption relied on

1. Rule, section and subsection number

2. If relying on section 2.3 [Accredited investor] of NI 45-106, provide the paragraph number in the definition of "accredited investor" in section 1.1 of NI 45-106 that applies to the purchaser. (select only one)

3. If relying on section 2.5 [Family, friends and business associates] of NI 45-106, provide:

a. the paragraph number in subsection 2.5(1) that applies to the purchaser (select only one); and

b. if relying on paragraphs 2.5(1)(b) to (i), provide:

i. the name of the director, executive officer, control person, or founder of the issuer or affiliate of the issuer claiming a relationship to the purchaser. (Note: if Item 9(a) has been completed, the name of the director, executive officer or control person must be consistent with the name provided in Item 9 and Schedule 2.)

ii. the position of the director, executive officer, control person, or founder of the issuer or affiliate of the issuer claiming a relationship to the purchaser.

4. If relying on subsection 2.9(2) or, in Alberta, New Brunswick, Nova Scotia, Ontario, Québec, or Saskatchewan, subsection 2.9(2.1) [Offering memorandum] of NI 45-106 and the purchaser is an eligible investor, provide the paragraph number in the definition of "eligible investor" in section 1.1 of NI 45-106 that applies to the purchaser. (select only one)

f) Other information

1. Is the purchaser a registrant? (Y/N)

2. Is the purchaser an insider of the issuer? (Y/N) (not applicable if the issuer is an investment fund)

3. Full legal name of person compensated for distribution to purchaser. If the person compensated is a registered firm, provide the firm NRD number only. (Note: the name must be consistent with name of the person compensated as provided in Item 8.)

INSTRUCTIONS FOR SCHEDULE 1

Any securities issued as payment for commissions or finder's fees must be disclosed in Item 8 of the report, not in Schedule 1.

Details of exemption relied on -- When identifying the exemption the issuer relied on for the distribution to each purchaser, refer to the rule, statute or instrument in which the exemption is provided and identify the specific section and, if applicable, subsection or paragraph. For example, if the issuer is relying on an exemption in a National Instrument, refer to the number of the National Instrument, and the subsection or paragraph number of the specific provision. If the issuer is relying on an exemption in a local blanket order, refer to the blanket order by number.

For exemptions that require the purchaser to meet certain characteristics, such as the exemption in section 2.3 [Accredited investor], section 2.5 [Family, friends and business associates] or subsection 2.9(2) or, in Alberta, New Brunswick, Nova Scotia, Ontario, Québec, or Saskatchewan, subsection 2.9(2.1) [Offering memorandum] of NI 45-106, provide the specific paragraph in the definition of those terms that applies to each purchaser.

Reports filed under paragraph 6.1(1)(j) [TSX Venture Exchange offering] of NI 45-106 -- For reports filed under paragraph 6.1(1)(j) [TSX Venture Exchange offering] of NI 45-106, Schedule 1 needs to list the total number of purchasers by jurisdiction only, and is not required to include the name, residential address, telephone number or email address of the purchasers.

SCHEDULE 2 TO FORM 45-106F1 (CONFIDENTIAL DIRECTOR, EXECUTIVE OFFICER, PROMOTER AND CONTROL PERSON INFORMATION)

Schedule 2 must be filed in the format of an Excel spreadsheet in a form acceptable to the securities regulatory authority or regulator.

Complete the following only if Item 9(a) is required to be completed. This schedule also requires information to be provided about control persons of the issuer at the time of the distribution.

The information in this schedule will not be placed on the public file of any securities regulatory authority or regulator. However, freedom of information legislation may require the securities regulatory authority or regulator to make this information available if requested.

a) General information (provide only once)

1. Name of issuer

2. Certification date (YYYY-MM-DD)

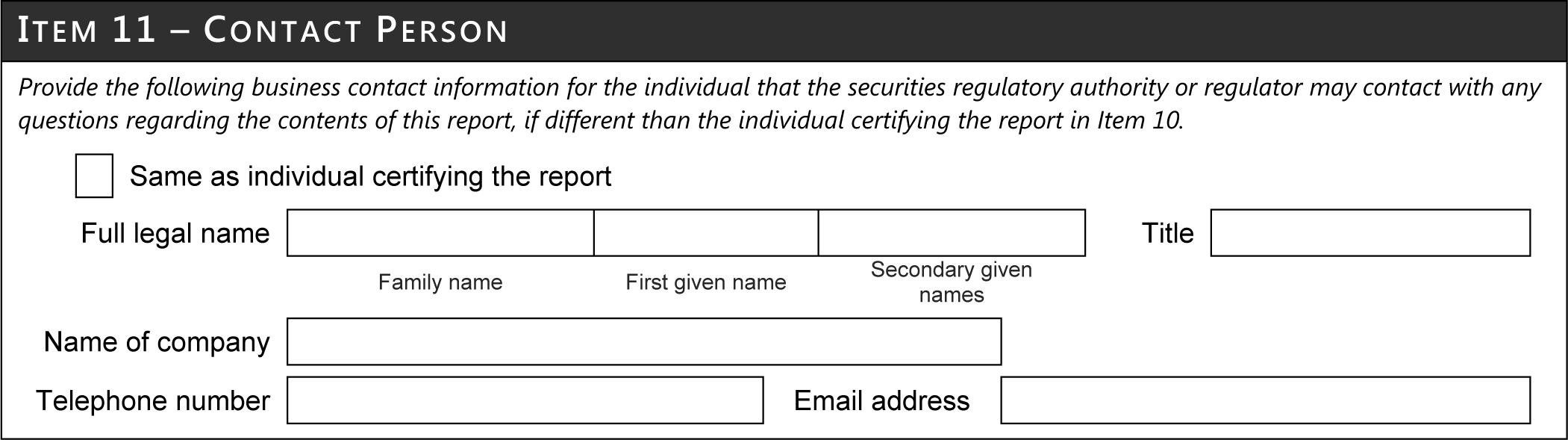

b) Business contact information of Chief Executive Officer (if not provided in Item 10 or 11 of report)

1. Email address

2. Telephone number

c) Residential address of directors, executive officers, promoters and control persons of the issuer

Provide the following information for each individual who is a director, executive officer, promoter or control person of the issuer at the time of the distribution. If the promoter or control person is not an individual, provide the following information for each director and executive officer of the promoter and control person. (Note: names of directors, executive officers and promoters must be consistent with the information in Item 9 of the report, if required to be provided.)

1. Family name

2. First given name

3. Secondary given names

4. Residential street address

5. Municipality

6. Province/State

7. Postal code/Zip code

8. Country

9. Indicate whether the individual is a control person, or a director and/or executive officer of a control person (if applicable)

d) Non-individual control persons (if applicable)

If the control person is not an individual, provide the following information. For locations within Canada, state the province or territory, otherwise state the country.

1. Organization or company name

2. Province or country of business location

Questions:

Refer any questions to:

9. Form 45-106F6 is repealed.

10. This Instrument comes into force on June 30, 2016.

ANNEX B

FORM 45-106F1 REPORT OF EXEMPT DISTRIBUTION (NEW REPORT)

Form 45-106F1 Report of Exempt Distribution

A. General Instructions

1. Filing instructions

An issuer or underwriter that is required to file a report of exempt distribution and pay the applicable fee must file the report and pay the fee as follows:

• In British Columbia -- through BCSC eServices at http://www.bcsc.bc.ca.

• In Ontario -- through the online e-form available at http://www.osc.gov.on.ca.

• In all other jurisdictions -- through the System for Electronic Document Analysis and Retrieval (SEDAR) in accordance with National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR) if required, or otherwise with the securities regulatory authority or regulator, as applicable, in the applicable jurisdictions at the addresses listed at the end of this form.

The issuer or underwriter must file the report in a jurisdiction of Canada if the distribution occurs in the jurisdiction. If a distribution is made in more than one jurisdiction of Canada, the issuer or underwriter may satisfy its obligation to file the report by completing a single report identifying all purchasers, and file the report in each jurisdiction of Canada in which the distribution occurs. Filing fees payable in a particular jurisdiction are not affected by identifying all purchasers in a single report.

In order to determine the applicable fee in a particular jurisdiction of Canada, consult the securities legislation of that jurisdiction.

2. Issuers located outside of Canada

If an issuer located outside of Canada determines that a distribution has taken place in a jurisdiction of Canada, include information about purchasers resident in that jurisdiction only.

3. Multiple distributions

An issuer may use one report for multiple distributions occurring within 10 days of each other, provided the report is filed on or before the 10th day following the first distribution date. However, an investment fund issuer that is relying on the exemptions set out in subsection 6.2(2) of NI 45-106 may file the report annually in accordance with that subsection.

4. References to purchaser

References to a purchaser in this form are to the beneficial owner of the securities.

However, if a trust company, trust corporation, or registered adviser described in paragraph (p) or (q) of the definition of "accredited investor" in section 1.1 of NI 45-106 has purchased the securities on behalf of a fully managed account, provide information about the trust company, trust corporation or registered adviser only; do not include information about the beneficial owner of the fully managed account.

5. References to issuer

References to "issuer" in this form include an investment fund issuer and a non-investment fund issuer, unless otherwise specified.

6. Investment fund issuers

If the issuer is an investment fund, complete Items 1-3, 6-8, 10, 11 and Schedule 1 of this form.

7. Mortgage investment entities

If the issuer is a mortgage investment entity, complete all applicable items of this form other than Item 6.

8. Language

The report must be filed in English or in French. In Québec, the issuer or underwriter must comply with linguistic rights and obligations prescribed by Québec law.

9. Currency

All dollar amounts in the report must be in Canadian dollars. If the distribution was made or any compensation was paid in connection with the distribution in a foreign currency, convert the currency to Canadian dollars using the daily noon exchange rate of the Bank of Canada on the distribution date. If the distribution date occurs on a date when the daily noon exchange rate of the Bank of Canada is not available, convert the currency to Canadian dollars using the most recent closing exchange rate of the Bank of Canada available before the distribution date. For investment funds in continuous distribution, convert the currency to Canadian dollars using the average daily noon exchange rate of the Bank of Canada for the distribution period covered by the report.

If the Bank of Canada no longer publishes a daily noon exchange rate and closing exchange rate, convert foreign currency using the daily single indicative exchange rate of the Bank of Canada in the same manner described in each of the three scenarios above.

If the distribution was not made in Canadian dollars, provide the foreign currency in Item 7(a) of the report.

10. Date of information in report

Unless otherwise indicated in this form, provide the information as of the distribution end date.

11. Date of formation

For the date of formation, provide the date on which the issuer was incorporated, continued or organized (formed). If the issuer resulted from an amalgamation, arrangement, merger or reorganization, provide the date of the most recent amalgamation, arrangement, merger or reorganization.

12. Security codes

Wherever this form requires disclosure of the type of security, use the following security codes:

Security code

Security type

BND

Bonds

CER

Certificates (including pass-through certificates, trust certificates)

CMS

Common shares

CVD

Convertible debentures

CVN

Convertible notes

CVP

Convertible preferred shares

DEB

Debentures

FTS

Flow-through shares

FTU

Flow-through units

LPU

Limited partnership units

NOT

Notes (include all types of notes except convertible notes)

OPT

Options

PRS

Preferred shares

RTS

Rights

UBS

Units of bundled securities (such as a unit consisting of a common share and a warrant)

UNT

Units (exclude units of bundled securities, include trust units and mutual fund units)

WNT

Warrants

OTH

Other securities not included above (if selected, provide details of security type in Item 7d)

B. Terms used in the form

1. For the purposes of this form:

"designated foreign jurisdiction" means Australia, France, Germany, Hong Kong, Italy, Japan, Mexico, the Netherlands, New Zealand, Singapore, South Africa, Spain, Sweden, Switzerland or the United Kingdom of Great Britain and Northern Ireland;

"eligible foreign security" means a security offered primarily in a foreign jurisdiction as part of a distribution of securities in either of the following circumstances:

(a) the security is issued by an issuer

(i) that is incorporated, formed or created under the laws of a foreign jurisdiction,

(ii) that is not a reporting issuer in a jurisdiction of Canada,

(iii) that has its head office outside of Canada, and

(iv) that has a majority of the executive officers and a majority of the directors ordinarily resident outside of Canada;

(b) the security is issued or guaranteed by the government of a foreign jurisdiction;

"foreign public issuer" means an issuer where any of the following apply:

(a) the issuer has a class of securities registered under section 12 of the 1934 Act;

(b) the issuer is required to file reports under section 15(d) of the 1934 Act;

(c) the issuer is required to provide disclosure relating to the issuer and the trading in its securities to the public, to security holders of the issuer or to a regulatory authority and that disclosure is publicly available in a designated foreign jurisdiction;

"legal entity identifier" means a unique identification code assigned to the person

(a) in accordance with the standards set by the Global Legal Entity Identifier System, or

(b) that complies with the standards established by the Legal Entity Identifier Regulatory Oversight Committee for pre-legal entity identifiers;

"permitted client" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

"SEDAR profile" means a filer profile required under section 5.1 of National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR).

2. For the purposes of this form, a person is connected with an issuer or an investment fund manager if either of the following applies:

(a) one of them is controlled by the other;

(b) each of them is controlled by the same person.

Form 45-106F1 Report of Exempt Distribution

IT IS AN OFFENCE TO MAKE A MISREPRESENTATION IN THIS REPORT

SCHEDULE 1 TO FORM 45-106F1 (CONFIDENTIAL PURCHASER INFORMATION)

Schedule 1 must be filed in the format of an Excel spreadsheet in a form acceptable to the securities regulatory authority or regulator.

The information in this schedule will not be placed on the public file of any securities regulatory authority or regulator. However, freedom of information legislation may require the securities regulatory authority or regulator to make this information available if requested.

a) General information (provide only once)

1. Name of issuer

2. Certification date (YYYY-MM-DD)

Provide the following information for each purchaser that participated in the distribution. For each purchaser, create separate entries for each distribution date, security type and exemption relied on for the distribution.

b) Legal name of purchaser

1. Family name

2. First given name

3. Secondary given names

4. Full legal name of non-individual (if applicable)

c) Contact information of purchaser

1. Residential street address

2. Municipality

3. Province/State

4. Postal code/Zip code

5. Country

6. Telephone number

7. Email address (if available)

d) Details of securities purchased

1. Date of distribution (YYYY-MM-DD)

2. Number of securities

3. Security code

4. Amount paid (Canadian $)

e) Details of exemption relied on

1. Rule, section and subsection number

2. If relying on section 2.3 [Accredited investor] of NI 45-106, provide the paragraph number in the definition of "accredited investor" in section 1.1 of NI 45-106 that applies to the purchaser. (select only one)

3. If relying on section 2.5 [Family, friends and business associates] of NI 45-106, provide:

a. the paragraph number in subsection 2.5(1) that applies to the purchaser (select only one); and

b. if relying on paragraphs 2.5(1)(b) to (i), provide:

i. the name of the director, executive officer, control person, or founder of the issuer or affiliate of the issuer claiming a relationship to the purchaser. (Note: if Item 9(a) has been completed, the name of the director, executive officer or control person must be consistent with the name provided in Item 9 and Schedule 2.)

ii. the position of the director, executive officer, control person, or founder of the issuer or affiliate of the issuer claiming a relationship to the purchaser.

4. If relying on subsection 2.9(2) or, in Alberta, New Brunswick, Nova Scotia, Ontario, Québec, or Saskatchewan, subsection 2.9(2.1) [Offering memorandum] of NI 45-106 and the purchaser is an eligible investor, provide the paragraph number in the definition of "eligible investor" in section 1.1 of NI 45-106 that applies to the purchaser. (select only one)

f) Other information

1. Is the purchaser a registrant? (Y/N)

2. Is the purchaser an insider of the issuer? (Y/N) (not applicable if the issuer is an investment fund)

3. Full legal name of person compensated for distribution to purchaser. If the person compensated is a registered firm, provide the firm NRD number only. (Note: the name must be consistent with name of the person compensated as provided in Item 8.)

INSTRUCTIONS FOR SCHEDULE 1

Any securities issued as payment for commissions or finder's fees must be disclosed in Item 8 of the report, not in Schedule 1.

Details of exemption relied on -- When identifying the exemption the issuer relied on for the distribution to each purchaser, refer to the rule, statute or instrument in which the exemption is provided and identify the specific section and, if applicable, subsection or paragraph. For example, if the issuer is relying on an exemption in a National Instrument, refer to the number of the National Instrument, and the subsection or paragraph number of the specific provision. If the issuer is relying on an exemption in a local blanket order, refer to the blanket order by number.

For exemptions that require the purchaser to meet certain characteristics, such as the exemption in section 2.3 [Accredited investor], section 2.5 [Family, friends and business associates] or subsection 2.9(2) or, in Alberta, New Brunswick, Nova Scotia, Ontario, Québec, or Saskatchewan, subsection 2.9(2.1) [Offering memorandum] of NI 45-106, provide the specific paragraph in the definition of those terms that applies to each purchaser.

Reports filed under paragraph 6.1(1)(j) [TSX Venture Exchange offering] of NI 45-106 -- For reports filed under paragraph 6.1(1)(j) [TSX Venture Exchange offering] of NI 45-106, Schedule 1 needs to list the total number of purchasers by jurisdiction only, and is not required to include the name, residential address, telephone number or email address of the purchasers.

SCHEDULE 2 TO FORM 45-106F1 (CONFIDENTIAL DIRECTOR, EXECUTIVE OFFICER, PROMOTER AND CONTROL PERSON INFORMATION)

Schedule 2 must be filed in the format of an Excel spreadsheet in a form acceptable to the securities regulatory authority or regulator.

Complete the following only if Item 9(a) is required to be completed. This schedule also requires information to be provided about control persons of the issuer at the time of the distribution.

The information in this schedule will not be placed on the public file of any securities regulatory authority or regulator. However, freedom of information legislation may require the securities regulatory authority or regulator to make this information available if requested.

a) General information (provide only once)

1. Name of issuer

2. Certification date (YYYY-MM-DD)

b) Business contact information of Chief Executive Officer (if not provided in Item 10 or 11 of report)

1. Email address

2. Telephone number

c) Residential address of directors, executive officers, promoters and control persons of the issuer

Provide the following information for each individual who is a director, executive officer, promoter or control person of the issuer at the time of the distribution. If the promoter or control person is not an individual, provide the following information for each director and executive officer of the promoter and control person. (Note: names of directors, executive officers and promoters must be consistent with the information in Item 9 of the report, if required to be provided.)

1. Family name

2. First given name

3. Secondary given names

4. Residential street address

5. Municipality

6. Province/State

7. Postal code/Zip code

8. Country

9. Indicate whether the individual is a control person, or a director and/or executive officer of a control person (if applicable)

d) Non-individual control persons (if applicable)

If the control person is not an individual, provide the following information. For locations within Canada, state the province or territory, otherwise state the country.

1. Organization or company name

2. Province or country of business location

Questions:

Refer any questions to:

ANNEX C

CHANGES TO COMPANION POLICY 45-106 PROSPECTUS EXEMPTIONS

This Annex shows, by way of blackline, changes to Companion Policy 45-106 Prospectus Exemptions that will take effect upon the coming into force of the rule amendments set out in Annex A. Additions are represented with underlined text and deletions are represented with strikethrough text.

PART 5 -- FORMS

5.1 Report of exempt distribution

(1) Requirement to file

An issuer that has distributed a security of its own issue under any of the prospectus exemptions listed in section 6.1 of NI 45-106 is required to file a report of exempt distribution, on or before the 10th day after the distribution. Alternatively, if an underwriter distributes securities acquired under section 2.33 of NI 45-106, either the issuer or the underwriter may complete and file the form. If there is a syndicate of underwriters, the lead underwriter may file the form on behalf of the syndicate or each underwriter may file a form relating to the portion of the distribution it was responsible for. The required form of report is Form 45-106F1 Report of Exempt Distribution in all jurisdictions except British Columbia. In British Columbia, the required form of report is Form 45-106F6 British Columbia Report of Exempt Distribution.

In determining if it is required to file a report in a particular jurisdiction, the issuer or underwriter should consider the following questions:

(a) Is there a distribution in the jurisdiction? (Please refer to the securities legislation and securities directions of the jurisdiction for guidance, if any, on when a distribution occurs in the jurisdiction.)

(b) If there is a distribution in the jurisdiction, what exemption from the prospectus requirement is the issuer relying on for the distribution of the security?

(c) Does the exemption referred to in paragraph (b) trigger a reporting requirement? (Reports of exempt distribution are required for distributions made in reliance on the prospectus exemptions provided in section 6.1 of NI 45-106, Multilateral Instrument 45-108 Crowdfunding and certain local rules and orders.)

A distribution may occur in more than one jurisdiction. In this case, the issuer is required to file may complete a single report identifying all purchasers, and file the report in each Canadian jurisdiction where the distribution has occurred, except British Columbia. The report will set out all distributions in each Canadian jurisdiction.

If the distribution occurs in British Columbia and one or more other jurisdictions, the issuer is required to file Form 45-106F6 with the British Columbia Securities Commission and file Form 45-106F1 in the other applicable jurisdictions.

(2) Access to information in jurisdictions other than British Columbia

The securities legislation of several provinces requires that information filed with the securities regulatory authority or, where applicable, the regulator under such securities legislation, be made available for public inspection during normal business hours except for information that the securities regulatory authority or, where applicable, the regulator,

(a) believes to be personal or other information of such a nature that the desirability of avoiding disclosure thereof in the interest of any affected individual outweighs the desirability of adhering to the principle that information filed with the securities regulatory authority or the regulator, as applicable, be available to the public for inspection,

(b) in Alberta, considers that it would not be prejudicial to the public interest to hold the information in confidence, and

(c) in Québec, considers that access to the information could result in serious prejudice.

Based on the above-mentioned provisions of securities legislation, the securities regulatory authorities or regulators, as applicable, have determined that the information listed in Schedule 1 and Schedule 2 of Form 45-106F1 Report of Exempt Distribution, Schedule I ("Schedule I") discloses personal or other information of such a nature that the desirability of avoiding disclosure of this personal information outweighs the desirability of making the information available to the public for inspection. In addition, in Alberta, the regulator considers that it would not be prejudicial to the public interest to hold the information listed in Schedule Ithese schedules in confidence. In Québec, the securities regulatory authority considers that access to Schedule Ithese schedules by the public in general could result in serious prejudice and consequently, the information listed in Schedule Ithese schedules will not be made publicly available.

(3) Filings in British Columbia Electronic filing of Form 45-106F1 Report of Exempt Distribution

Form 45-106F1 is required to be filed electronically in all CSA jurisdictions as described below.

For filings made in British Columbia, issuers are required to file Form 45-106F645-106F1 and pay the fees associated with that filing electronically using BCSC e-serviceseServices. This requirement only applies to filings that are required to be made within 10 days of the distribution. It does not apply to filings made annually by investment funds under subsection 6.2(2) of NI 45-106. Please refer to BC Instrument 13-502 Electronic Filing of Reports of Exempt Distribution for further information.

For filings made in Ontario, issuers are required to file Form 45-106F1 electronically through the OSC's Electronic Filing Portal and pay the applicable fees. The electronic filing requirement applies to all issuers that file Form 45-106F1, including investment fund issuers that file annually in accordance with subsection 6.2(2) of NI 45-106. Please see OSC Rule 11-501 Electronic Delivery of Documents to the Ontario Securities Commission and OSC Rule 13-502 Fees for further information.

For filings made in any Canadian jurisdiction except for British Columbia and Ontario, issuers, other than certain foreign issuers, are required to file Form 45-106F1 and pay the fees associated with that filing electronically through the System for Electronic Document Analysis and Retrieval (SEDAR). The electronic filing requirement also applies to investment fund issuers that file annually in accordance with subsection 6.2(2) of NI 45-106. Please refer to National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR) and Multilateral Instrument 13-102 System fees for SEDAR and NRD for further information. Foreign issuers that are not required to file Form 45-106F1 electronically through SEDAR should file the report and pay the applicable fees in each of the jurisdictions in which a distribution is made at the addresses listed at the end of the report.

ANNEX D

SUMMARY OF NEW INFORMATION REQUIREMENTS

The table below summarizes the new information requirements in the New Report, together with an explanation of the rationale for each requirement.

|

Information Required |

Rationale |

|

|

|

||

|

Identifiers{1} |

||

|

|

||

|

Firm NRD number for the underwriter, investment fund manager and registrant being compensated |

This unique identifier allows securities regulators to accurately link information available through NRD to assist in our compliance programs. Using the NRD number also reduces duplication of certain information required to be disclosed in the New Report, which is available in NRD. |

|

|

|

||

|

SEDAR profile number |

The SEDAR profile number assists securities regulators in accessing information about the issuer that is filed on SEDAR and the issuer's SEDAR profile. Issuers that provide a SEDAR profile number are not required to complete certain sections of the New Report. |

|

|

|

||

|

Legal entity identifier of issuer |

The Global Legal Entity Identifier System is a system that provides a globally accepted standard for unique identification of parties to financial transactions. This system is overseen by the Legal Entity Identifier Regulatory Oversight Committee. Disclosure of issuers' legal entity identifiers: |

|

|

|

||

|

|

• |

addresses long-standing issues with entity identification, |

|

|

• |

provides a mechanism for linking exempt market reporting with other financial reporting, and |

|

|

• |

builds a more comprehensive risk profile for entities that operate in the exempt market. |

|

|

||

|

CUSIP number |

A CUSIP number is a nine character alphanumeric identifier that uniquely identifies a financial security. The first six digits of a CUSIP number are unique to the issuer, and the last three digits identify securities unique to the issuer. |

|

|

|

||

|

|

Disclosure of CUSIP numbers facilitates additional information gathering about the issuer and the securities being distributed to better inform policy making and monitor exempt market activity. |

|

|

|

||

|

Website of issuer, underwriter and investment fund manager |

Website information facilitates additional information gathering about the issuer, underwriter and investment fund manager to assist in our compliance programs. If a firm NRD number is provided for the underwriter or investment fund manager in the New Report, website information is not required. |

|

|

|

||

|

Previous legal name of issuer |

If the issuer's name has changed in the last 12 months, the issuer's most recent previous legal name must be provided. This information allows us to link information about issuers to assist in our compliance programs. |

|

|

|

||

|

Item 5 -- Issuer Information (Non-Investment Fund Issuers) |

||

|

|

||

|

Primary industry of issuer |

The Current Reports require the issuer to select its industry group from a limited number of categories that do not match any standard industry classification. These categories also do not include all issuer industries, resulting in a large proportion of uncategorized issuers. To resolve these issues, we have changed the industry categories to align with the North American Industry Classification System (NAICS) that is maintained in Canada by Statistics Canada. NAICS is widely used to track industry statistics by a number of North American government agencies, such as the Canada Revenue Agency, Industry Canada and British Columbia Statistics. |

|

|

|

||

|

|

The New Report requires issuers to disclose the six-digit NAICS code that most closely corresponds to their main business activity. Based on our research, we believe NAICS will be familiar to many issuers. Statistics Canada also provides a web-based search tool for issuers to locate their industry category. |

|

|

|

||

|

|

This comprehensive and standardized industry classification system enables us to better understand exempt market activity and link it with other macro-level statistics to assist in more informed policy-making. |

|

|

|

||

|

|

The New Report also requires issuers in the mining industry to disclose their stage of operations and issuers involved in certain investment activities to disclose the areas of their primary asset holdings. We believe these classifications are consistent with how these industries are often analyzed. |

|

|

|

||

|

Number of employees of the issuer |

Issuers are required to indicate their total number of employees, which serves as a proxy for the size of the issuer. Information about the size of the issuer assists us in policy development, helping to assess whether capital raising prospectus exemptions are benefiting small and medium sized businesses. |

|

|

|

||

|

|

The New Report lists four broad ranges of employee numbers for issuers to select. The selected ranges provide a sufficient metric for the size of an issuer because they are broadly consistent with those used by Statistics Canada to differentiate between small, medium and large businesses and so will already be familiar to some issuers. We believe that reporting such a range is likely to be less commercially sensitive than reporting the actual number of employees or revenue of the issuer. |

|

|

|

||

|

Additional information from issuers without a SEDAR profile |

Certain information about an issuer can be obtained from its SEDAR profile. Recent changes to National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR) will require filing of reports of exempt distribution on SEDAR beginning May 24, 2016, for distributions in Canadian jurisdictions other than British Columbia and Ontario. As a result, non-reporting issuers will also have SEDAR profiles. Changes have been made to SEDAR to allow voluntary filing until May 24, 2016. |

|

|

|

||

|

|

The New Report requires disclosure of the following if the issuer does not have a SEDAR profile: |

|

|

|

||

|

|

• |

date of formation, |

|

|

• |

financial year-end, |

|

|

• |

jurisdictions where reporting, |

|

|

• |

stock exchange listings, and |

|

|

• |

size of assets. |

|

|

||

|

|

This information is relevant for our analysis of exempt market activity and allows us to have comparable information across all issuers. |

|

|

|

||

|

Item 6 -- Investment Fund Issuer Information |

||

|

|

||

|

Type of investment fund |

The New Report requires investment fund issuers to identify what type of investment fund they are in order to better understand fund types that are most active in the exempt market. This reporting increases our ability to profile exempt market activity by the investment fund industry and supports the CSA's policy initiatives. |

|

|

|

||

|

Net asset value (NAV) |

Information about the NAV of an investment fund assists securities regulators to understand the size of funds operating in the exempt market, such as foreign investment funds accessing the Canadian market, and further informs policy development for investment funds. |

|

|

|

||

|

Other |

The New Report requires the following information from investment fund issuers that would provide additional insight into the profile of issuers that operate in the exempt market: |

|

|

|

||

|

|

• |

date of formation, |

|

|

• |

financial year-end, |

|

|

• |

jurisdictions where reporting, and |

|

|

• |

stock exchange listings. |

|

|

||

|

Item 7 -- Information About the Distribution |

||

|

|

||

|

Currency |

Information about the currencies in which the distribution was made provides us with greater insight into the distribution and exempt market activity. |

|

|

|

||

|

Type of securities distributed |

The New Report requires an issuer to indicate the type of securities distributed using specific 3-letter codes. Although the Current Reports require a description of the type of securities distributed, the 3-letter codes provide a more structured format for collecting this information. |

|

|

|

||

|

|

Receiving this information in a structured format improves the consistency of the information we receive in reports, making our oversight processes more efficient. Having greater insight into the types of securities that are being distributed in the exempt market assists us in trend analysis, our compliance programs and policy development. |

|

|

|

||

|

Summary of distribution by exemption |

The Current Reports require information about the distribution (number of purchasers and dollar amount raised) for each jurisdiction where a purchaser resides. The New Report requires this information about the distribution to be provided for each jurisdiction where a purchaser resides, and also for: |

|

|

|

• |

each exemption relied on in the jurisdiction where a purchaser resides, if a purchaser resides in a jurisdiction of Canada, and |

|

|

• |

each exemption relied on in Canada, if a purchaser resides in a foreign jurisdiction. |

|

|

||

|

|

If an issuer located outside of Canada completes a distribution in a jurisdiction of Canada, the issuer is required to include distributions to purchasers resident in that jurisdiction of Canada only. |

|

|

|

||

|

|

This provides us with better information about the exemptions relied on to distribute securities and assists us in our analysis of exempt market activity, our compliance programs and policy development. |

|

|

|

||

|

Net proceeds to the investment fund |

The New Report requires an investment fund issuer to provide the net proceeds to the investment fund for each jurisdiction where a purchaser resides. If an issuer located outside of Canada completes a distribution in a jurisdiction of Canada, the issuer is required to include net proceeds for that jurisdiction of Canada only. |

|

|

|

||

|

|

As most investment funds offer some redemption rights, reporting only the purchase amount likely overstates the size of the market. Gathering information about redemptions as well as purchases provides us with a more complete picture of fund flows by investment fund issuers in the exempt market. |

|

|

|

||

|

Offering materials (applicable only in Saskatchewan, Ontario, Québec, New Brunswick and Nova Scotia) |

The New Report requires issuers to list and provide certain details about offering materials that are required to be filed or delivered in connection with a distribution under the securities legislation of Saskatchewan, Ontario, Québec, New Brunswick and Nova Scotia. |

|

|

|

||

|

|

For example, issuers are required to list: |

|

|

|

||

|

|

• |

offering memoranda and any other documents (marketing materials) that are required to be filed under section 2.9 of NI 45-106. |

|

|

• |

offering memoranda that are voluntarily provided, and required to be delivered to the OSC under section 5.4 of OSC Rule 45-501 Ontario Prospectus and Registration Exemptions. |

|

|

• |

crowdfunding offering documents and any other distribution documents (term sheets and other materials summarizing information in a crowdfunding offering document) required to be filed under Multilateral Instrument 45-108 Crowdfunding (MI 45-108). |

|

|

||

|

|

This is a reporting requirement only; the New Report does not impose any new requirements to file or deliver offering documents. The New Report requires reporting that such materials have been filed or delivered only where required by the securities legislation of the applicable jurisdictions. |

|

|

|

||

|

|

In Ontario only, if the offering materials listed are required to be filed or delivered to the OSC, electronic versions of those offering materials are to be attached to and submitted electronically with the New Report on the OSC's Electronic Filing Portal (if not previously filed or delivered to the OSC). |

|

|

|

||

|

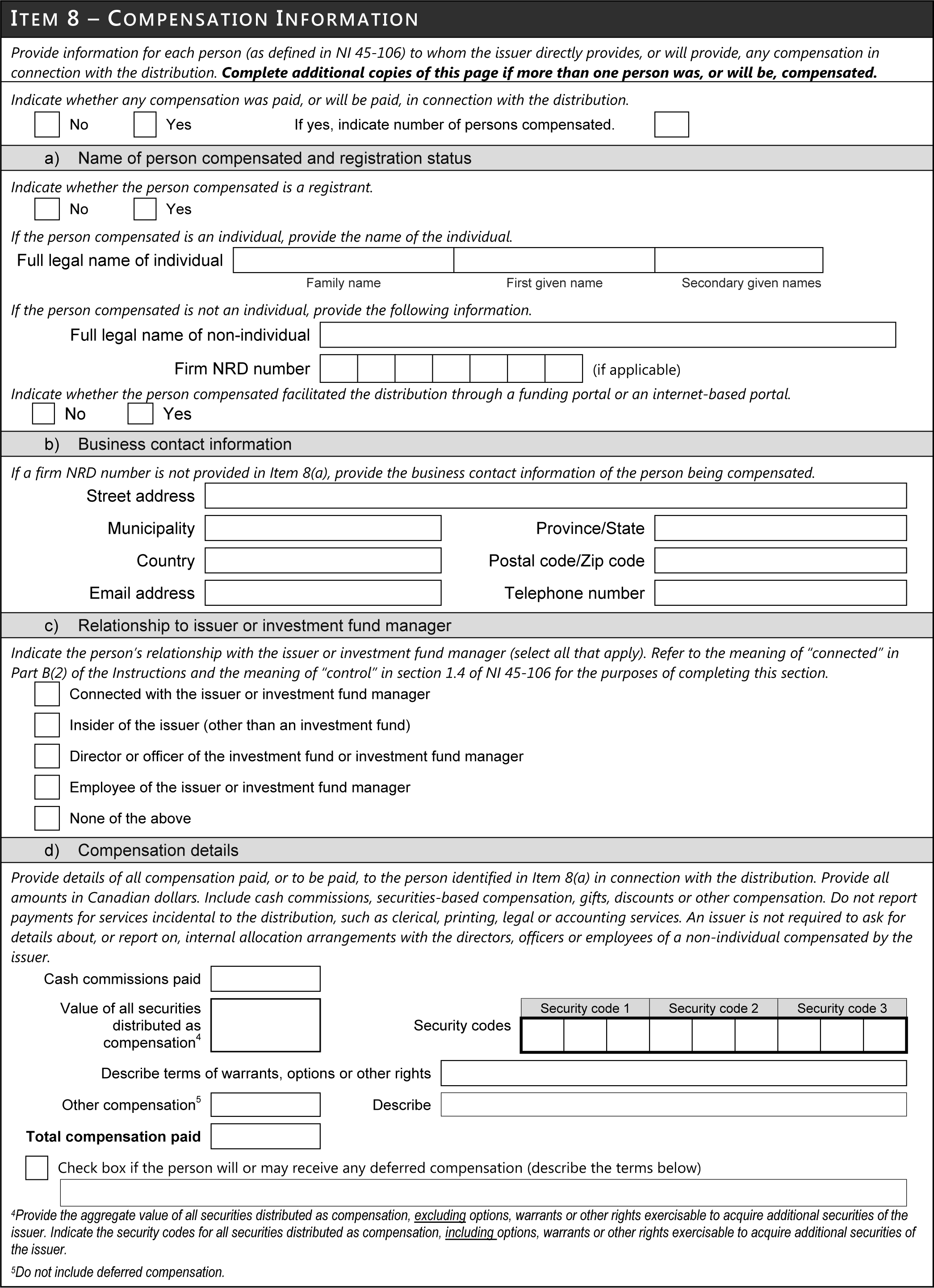

Item 8 -- Compensation Information |

||

|

|

||

|

Funding portals |

The New Report requires issuers to indicate whether the person compensated in connection with the distribution facilitated the distribution through a "funding portal" or an "internet-based portal". These terms generally refer to an intermediary that provides an online platform for issuers to offer and sell securities to investors. These include funding portals as defined under MI 45-108. |

|

|

|

||

|

|

This information provides us with insight into the role of funding portals in the distribution of securities in the exempt market and supports our compliance programs and policy development. |

|

|

|

||

|

Relationship to issuer of person being compensated |

The New Report requires disclosure about whether the person compensated in connection with the distribution is a registrant or an insider of the issuer. |

|

|

|

||

|

|

While the BCSC currently requires disclosure of this information in Form 45-106F6, this is a new requirement for jurisdictions that currently require filing of Form 45-106F1. |

|

|

|

||

|

|

The New Report also requires disclosure of whether a person compensated is an employee of the issuer, or connected to the issuer. This additional information enables us to assess the prevalence of financial relationships among issuers and those persons they compensate. |

|

|

|

||

|

|

Having detailed information about these arrangements allows us to enhance our existing compliance programs, and supports policy development. |

|

|

|

||

|

Terms of deferred compensation |

The New Report requires issuers to indicate whether any deferred compensation will or may be paid to a person in connection with a distribution, and to describe the terms of the deferred compensation. While the Current Reports require disclosure of any compensation paid or to be paid in connection with a distribution, there is no requirement for deferred compensation to be specifically identified as such or for the terms of the deferred compensation to be described. |

|

|

|

||

|

|

Disclosure of this information supports our compliance programs, provides us with better information about the financial relationships that exist between issuers and the persons being compensated, and brings greater transparency to these arrangements. |

|

|

|

||

|

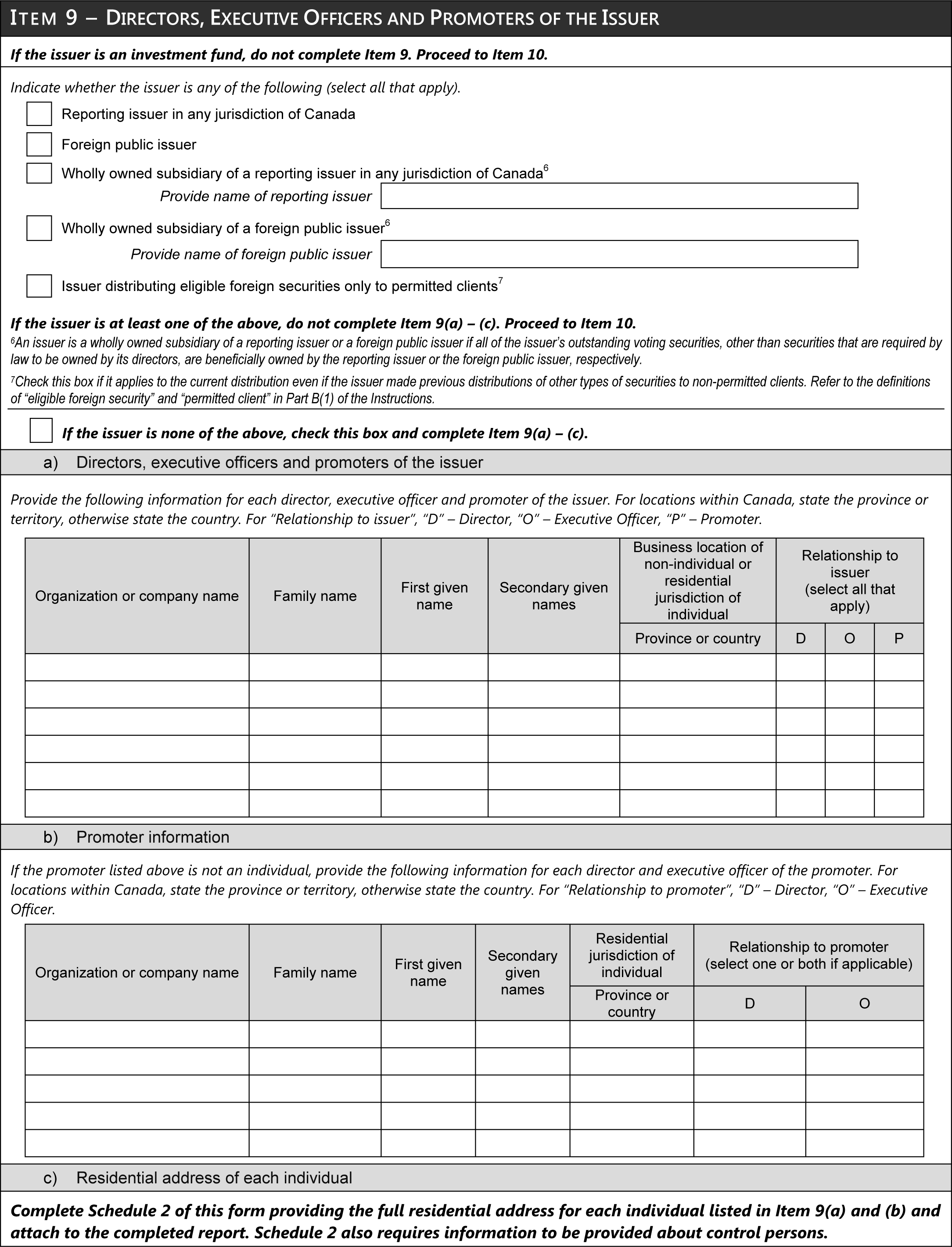

Item 9 -- Directors, Executive Officers and Promoters of the Issuer |

||

|

|

||

|

Name, title and province, state or country of residence of directors, executive officers and promoters of certain issuers |

Disclosure of this information is required for directors, executive officers and promoters of certain issuers. If the promoter is not an individual, information about the directors and executive officers of the promoter is also required. |

|

|

|

||

|

|

We believe this information is necessary to facilitate our oversight of the exempt market, enhance our compliance programs and bring transparency to the exempt market. This information allows us to identify connections between issuers through related executives, directors and promoters. |

|

|

|

||

|

|

While the BCSC currently requires disclosure of information about directors, executive officers and promoters in Form 45-106F6, this is a new requirement for all other CSA jurisdictions. |

|

|

|

||

|

|

In response to comments we received on the New Report, we have moved the information about control persons to Schedule 2, which is not publicly available. |

|

|

|

||

|

|

The New Report does not require this information to be provided by: |

|

|

|

||

|

|

• |

investment fund issuers, |

|

|

• |

reporting issuers and their wholly owned subsidiaries, |

|

|

• |

foreign public issuers and their wholly owned subsidiaries, and |

|

|

• |

issuers distributing eligible foreign securities only to permitted clients. |

|

|

||

|

Schedule 1 -- Confidential Purchaser Information{2} |

||

|

|

||

|

Email address of purchaser |

The New Report requires the email address of the purchaser to be provided if the purchaser has provided this information to the issuer. This information enhances our ability to contact purchasers if needed as part of our compliance programs. |

|

|

|

||

|

Information about exemption relied on |

To assist in our compliance programs and future policy development, the New Report requires the issuer or underwriter to identify the exemption relied on in more detail, by requiring the section, subsection and paragraph of the exemption, where applicable. |

|

|

|

||

|

|

For example, the New Report requires the issuer to specify which category of accredited investor or eligible investor the purchaser met. The New Report requires the issuer to identify only one category for each purchaser. |

|

|

|

||

|

Identification of whether the purchaser is an insider of the issuer or a registrant |

In the New Report, the issuer is required to identify whether the purchaser is an insider of the issuer or a registrant. |

|

|

|

||

|

|

While the BCSC currently requires disclosure of this information in Form 45-106F6, this is a new requirement for all other CSA jurisdictions. |

|

|

|

||

|

|

This information is useful for identifying connections between purchasers and issuers, which facilitates our oversight of the exempt market and supports our compliance programs. |

|

|

|

||

|

Identification of person being compensated for each purchaser |

The New Report requires the issuer to specifically identify the person compensated for a distribution made to each purchaser. If the person is a registered firm, only the firm NRD number must be provided. The names of the persons compensated must be consistent with those provided in Item 8. |

|

|

|

||

|

|

This information supports our compliance programs, provides us with better information about the financial relationships that exist between issuers and the persons being compensated, and allows us to monitor unregistered finders, compensation rates of finders and whether registrants are trading in jurisdictions where they are not registered. |

|

|

|

||

|

Schedule 2 -- Confidential Director, Executive Officer, Promoter and Control Person Information{3} |

||

|

|

||

|

Business contact information for CEO of issuer |

The New Report requires the telephone number and email address of the chief executive officer to be provided for an issuer that is required to complete Item 9(a) of the New Report. We are requesting this information to assist us in addressing past challenges with contacting persons at issuers who are capable of answering questions about the distribution. |

|

|

|

||

|

Full residential address of directors, executive officers, promoters and control persons |

The New Report requires full residential address information to be provided for directors, executive officers, promoters and control persons of issuers that are required to complete Item 9(a) of the New Report. If a promoter or control person is not an individual, this information is required for each director and executive officer of the promoter and control person. |

|

|

|

||

|

|

While the BCSC currently requires disclosure of municipality and country of these individuals in Form 45-106F6, this is a new requirement for all other CSA jurisdictions. |

|

|

|

||

|

|

This information supports our compliance programs by allowing the CSA to more effectively allocate its resources. |

|

|

|

||

|

Name and location of non-individual control person |

If a control person is not an individual, the New Report requires the name and location of the control person to be provided. |

|

|

|

||

|

|

This information supports our compliance programs by allowing us to identify connections between issuers and control persons. |

|

{1} The New Report only requires these identifiers to be provided if the issuer, underwriter, investment fund manager or registrant has such identifiers.

{2} Purchaser information provided in Schedule 1 is not publicly available.

{3} Information provided in Schedule 2 is not publicly available. The information in Schedule 2 is only required to be provided by issuers that are required to complete Item 9(a).

ANNEX E

LIST OF COMMENTERS

1. Alternative Investment Management Association

2. Arrow Capital Management Inc.

3. Borden Ladner Gervais LLP

4. Boyle & Co. LLP

5. British Columbia Investment Management Corporation, Canada Pension Plan Investment Board, Ontario Teachers' Pension Plan Board, RBC Global Asset Management Inc., Barclays Capital Inc., Citigroup Global Markets Inc., Goldman, Sachs & Co., J.P. Morgan Securities LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated

6. Canadian Foundation for Advancement of Investor Rights

7. Davies, Ward, Phillips & Vineberg LLP

8. Fonds de solidarité FTQ

9. Invesco Canada Ltd.

10. Investment Industry Association of Canada

11. National Exempt Market Association

12. Nicola Wealth Management (2 comment letters submitted)

13. Osler, Hoskin & Harcourt LLP

14. Portfolio Management Association of Canada

15. Private Capital Markets Association of Canada

16. Prospectors & Developers Association of Canada

17. R.N. Croft Financial Group Inc.

18. Stikeman Elliott LLP

ANNEX F

SUMMARY OF COMMENTS AND RESPONSES

|

No. |

Topic |

Comments |

Responses |

||

|

|

|||||

|

General |

|||||

|

1. |

Support for harmonized and streamlined report |