Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

[withdrawn by CSA Staff Notice 11-346, September 14, 2023] CSA Staff Notice 54-303 - Progress Report on Review of the Proxy Voting Infrastructure

[withdrawn by CSA Staff Notice 11-346, September 14, 2023] CSA Staff Notice 54-303 - Progress Report on Review of the Proxy Voting Infrastructure

CSA Staff Notice 54-303

Progress Report on Review of the Proxy Voting Infrastructure

The RFP will be available as of the afternoon of January 29, 2015 from Merx at https://www.merx.com and can be found by searching for Merx Reference Number 319007 under "Open Opportunities".

January 29, 2015

1. Purpose of Notice

On August 15, 2013, the Canadian Securities Administrators (the CSA or we) published for comment CSA Consultation Paper 54-401 Review of the Proxy Voting Infrastructure (the Consultation Paper). The purpose of the Consultation Paper was to outline and seek feedback from market participants on a proposed approach to address concerns regarding the integrity and reliability of the proxy voting infrastructure.

This Notice:

• reports on the progress we have made in our review of the proxy voting infrastructure since publication of the Consultation Paper, and

• outlines our next steps in this initiative.

2. Background -- Why We are Reviewing the Proxy Voting Infrastructure

Shareholder voting is one of the most important methods by which shareholders can affect governance and communicate preferences about an issuer's management and stewardship. Issuers rely on shareholder voting to approve corporate governance matters or certain corporate transactions. Shareholder voting is therefore fundamental to, and enhances the quality and integrity of, our public capital markets.

Shareholders typically do not vote in person at meetings, but instead vote by proxy. The proxy voting infrastructure is the network of organizations, systems, legal rules and market practices that support the solicitation, collection, submission and tabulation of proxy votes for a shareholder meeting. It is important that the proxy voting infrastructure is reliable, accurate and transparent and that it operates as a coherent system. It is also important for market confidence that issuers and investors perceive the infrastructure to operate in this way.

Some issuers and investors have expressed concern about the proxy voting infrastructure's integrity and reliability. This lack of confidence stems in large part from the opacity and complexity of the infrastructure, which makes it difficult for issuers and investors to assess it as a whole.

Given the centrality of the proxy voting infrastructure to our public capital markets, we believe that it is appropriate for us as securities regulators to be actively involved in reviewing the proxy voting infrastructure.

3. Our Approach -- Focus on Vote Reconciliation

The Consultation Paper did three things.

First, it provided an overview of how proxy voting works in Canada's intermediated holding system from both legal and operational perspectives.

Second, it identified various aspects of the proxy voting infrastructure that commenters had suggested undermined its integrity and reliability.

Third, it indicated that we intended to evaluate the proxy voting infrastructure's integrity and reliability by focusing on two questions:{1}

Question 1: Is accurate vote reconciliation occurring within the proxy voting infrastructure?

Vote reconciliation is the process by which proxy votes from registered shareholders and voting instructions from beneficial owners of shares are reconciled against the securities entitlements in the intermediated holding system. This is one of the central functions of the proxy voting infrastructure.

There are two distinct aspects of vote reconciliation.

The first aspect is where intermediaries reconcile and allocate vote entitlements to individual client accounts. We refer to this as client account vote reconciliation. Client account vote reconciliation involves the internal back-office systems of intermediaries and how they track and allocate vote entitlements for individual client accounts.

The second is where meeting tabulators reconcile proxy votes to intermediary vote entitlements, which we refer to as meeting vote reconciliation. Meeting vote reconciliation involves the systems and processes that link depositories, intermediaries and meeting tabulators with one another in order for the following three things to occur:

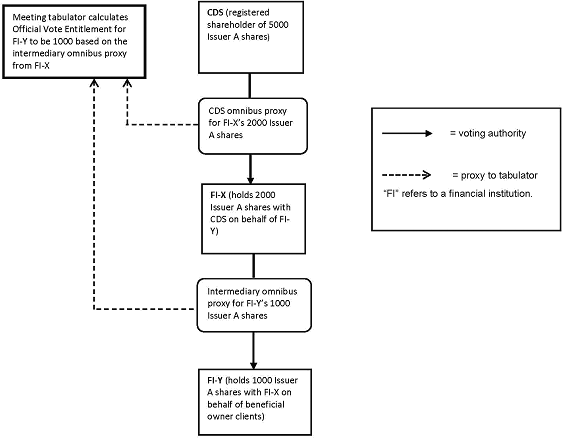

1. Depositories and intermediaries provide vote entitlement information to meeting tabulators through omnibus proxies,

2. Meeting tabulators calculate the vote entitlement that an intermediary has for a meeting based on the information provided by depositories and intermediaries (the Official Vote Entitlement), and

3. Meeting tabulators reconcile intermediary proxy votes to the Official Vote Entitlements.

Appendix A -- Meeting Vote Reconciliation provides more information about the vote reconciliation process.

The Consultation Paper:

• outlined at a high-level the various component processes of vote reconciliation and the parties involved, and

• asked market participants for their views on whether accurate vote reconciliation was occurring, and asked for relevant empirical data to determine whether these various component processes supported accurate vote reconciliation.

Question 2: What type of end-to-end vote confirmation system should be added to the proxy voting infrastructure?

End-to-end vote confirmation is a communication to shareholders that allows them to confirm that their proxy votes and voting instructions have been properly transmitted by the intermediaries, received by the tabulator and tabulated as instructed. The Consultation Paper:

• noted that the proxy voting infrastructure and existing vote reconciliation process did not have such a system in place,

• stated our view that the lack of such a confirmation system could undermine confidence in the accuracy and reliability of proxy voting results, and

• asked market participants for their views on what an end-to-end vote confirmation system should look like and for information on industry initiatives to develop end-to-end vote confirmation.

4. Initial Feedback and Information -- Comment Letters and Roundtables

The comment period ended on November 13, 2013. We received 32 comment letters from various market participants. We have reviewed the comments received and wish to thank all commenters for contributing to the consultation. Appendix B -- Summary of Comments contains a summary of the comments received.

We also sought feedback on our framework and more information on vote reconciliation in the Consultation Paper through roundtables held by the British Columbia Securities Commission, the Alberta Securities Commission, the Ontario Securities Commission and the Autorité des marchés financiers between January and March 2014.{2}

The following were the key themes from the comment letters and roundtables.

1. Securities regulators need to take a leadership role in reviewing the accuracy of vote reconciliation because no single market participant or set of market participants is able to access all the information used for vote reconciliation.

The initial feedback and information confirmed that it was highly unlikely that market participants would be able to adequately assess for themselves whether the proxy voting infrastructure was supporting accurate vote reconciliation. Vote reconciliation requires information about proxy votes and vote entitlements to be generated by and shared among depositories, intermediaries, the intermediaries' service provider (e.g., Broadridge) and meeting tabulators. Not only do issuers and investors lack access to all of this information; the key participants themselves lack access because they operate in silos. For example, an intermediary would typically not know that a meeting tabulator had determined that the intermediary was in an over-vote position because there is no protocol for when and how intermediaries and tabulators communicate with each other about potential over-votes.

The silo-ed nature of vote reconciliation means that securities regulators need to take a leadership role in bringing all the parties together in order to properly assess the accuracy of vote reconciliation.

2. Over-voting is occurring, indicating that vote reconciliation is not always occurring accurately. However, there was no consensus either about the causes or about how to solve the problem.

The initial feedback and information indicated that over-voting is occurring. We define an over-vote as a situation where a meeting tabulator receives proxy votes from an intermediary that exceed the intermediary's Official Vote Entitlement.{3} If unresolved, an over-vote can result in a meeting tabulator rejecting or pro-rating an intermediary's proxy votes (and consequently, the votes of the clients who provided the intermediary with voting instructions).

Several transfer agent members of the Securities Transfer Association of Canada (STAC) tracked instances of over-voting at meetings for which they were tabulators. STAC compiled these statistics and found that in 2013, over-voting occurred in 51% of the meetings for which these members were tabulators.{4} These statistics were troubling as they suggested that there was significant inaccurate vote reconciliation occurring. We emphasize, however, that these statistics did not provide any insight into the number of vote entitlements or proxy votes involved; nor did they provide any insight into whether over-voting:

• changed the outcome of a shareholder meeting, or

• had a material impact on the relative percentages of For/Against/Withheld proxy votes on the matters being voted on.

While there was consensus that over-voting was occurring, there was no consensus as to its cause. As a consequence, there was no consensus on how to solve the problem. For example:

• STAC suggested that over-voting was caused by problems with client account vote reconciliation. They viewed over-voting as evidence that some intermediaries were allocating vote entitlements to client accounts that significantly exceeded the number of shares that those intermediaries held in accounts with depositories and/or other intermediaries. Some investors and issuers raised a similar concern, and also wanted us to review whether some intermediary back-office systems allowed more than one entity to vote the same share. This situation is known as double or multiple voting.

• The Investment Industry Association of Canada (IIAC) suggested that over-voting was caused by problems with meeting vote reconciliation; specifically, lack of communication between meeting tabulators and intermediaries. They thought that most instances of over-voting could be resolved if meeting tabulators contacted intermediaries when they had problems reconciling an intermediary's proxy votes to its Official Vote Entitlement. However, STAC raised concerns about whether it was feasible or appropriate to place the onus on meeting tabulators to identify and resolve over-voting in this manner.

5. Subsequent Steps in Our Review

Following the comment letter and roundtable process, we undertook the following initiatives related to evaluating vote reconciliation.

1. Shareholder Meeting Review

We felt strongly that a proper assessment of meeting vote reconciliation required key participants in the proxy voting infrastructure to:

• develop a better understanding of how meeting vote reconciliation actually works, i.e. how the various processes that were identified and outlined in the Consultation Paper are actually implemented for shareholder meetings,

• identify and analyze instances where it appeared that an intermediary's calculations of its vote entitlements did not match the meeting tabulator's calculations (i.e. over-reporting), and

• identify and analyze actual instances of over-voting.

To that end, we conducted a qualitative{5} review of six uncontested, uncontentious shareholder meetings that were held in 2014 (the Shareholder Meeting Review). The shareholder meetings were held by reporting issuers in Ontario, Alberta, British Columbia and Quebec. Our sample included issuers:

• that were listed on the Toronto Stock Exchange (TSX) and TSX Venture Exchange,

• that used different meeting tabulators,

• that were listed only in Canada and inter-listed in the U.S.,

• that were closely-- and widely-held,

• that conducted direct NOBO solicitations and that solicited only through intermediaries,

• whose shares were the subject of securities lending activity around the record date, and

• that operated in different industries.

Appendix C -- Shareholder Meeting Review: Objective, Scope and Methodology provides more information about the Shareholder Meeting Review.

By identifying instances of over-reporting and over-voting, we hoped to identify potential gaps in the proxy voting infrastructure. We were particularly interested in finding out whether over-reporting and over-voting were caused by tabulators not receiving some or all of the documents necessary to correctly establish an intermediary's Official Vote Entitlement, i.e. problems with meeting vote reconciliation. We were also interested in finding out whether there was any evidence that over-voting was caused by intermediaries allocating too many vote entitlements to their client accounts relative to the number of shares these intermediaries held in accounts with depositories or other intermediaries, i.e. problems with client account vote reconciliation. Some commenters have suggested that over-voting is extremely common and is evidence of large-scale over-allocation of vote entitlements.

2. Technical Working Group

We also thought it important for securities regulators to continue bringing the key parties in the proxy voting infrastructure together and breaking down the operational and information silos within which these parties performed meeting vote reconciliation. To that end, we formed a Technical Working Group with representatives from:

• issuers,

• investors,

• intermediaries,

• an intermediary service provider, Broadridge,{6}

• transfer agents, and

• CDS.

The Technical Working Group met three times, once in August, once in September and once in November 2014. At each of these meetings, the participants:

• shared information about their respective operational processes in meeting vote reconciliation,

• identified potential gaps in the meeting vote reconciliation process, and

• discussed possible solutions to the gaps. In particular, we asked Broadridge U.S. to present some initial findings on a U.S. pilot project (the U.S. End-to-End Vote Confirmation Pilot) that established an electronic communication tool for meeting tabulators and intermediaries to confirm intermediary vote entitlements for meetings and confirm that an intermediary's proxy votes had been accepted.

3. Targeted consultations with custodians and investment-dealers on client account vote reconciliation and double or multiple voting

As noted above, several investors and issuers raised concerns about double or multiple voting, and wanted us to examine this issue. Double or multiple voting occurs when more than one entity is allowed or not prevented from voting the same share. Double or multiple voting can also be further broken down into:

• possible double or multiple voting, whereby more than one entity may vote or is not prevented from voting the same share, and

• actual double or multiple voting, whereby two or more entities actually vote the same share.

The main area where concerns about double or multiple voting have arisen is share lending. Some intermediaries such as custodians have back-office systems in place that track lent shares per client account, i.e. they have back-office systems that eliminate possible double or multiple voting. Concerns have been raised that other intermediaries do not have the same type of back-office systems in place. In particular, concerns were raised about the client account vote reconciliation methods investment dealers used for retail margin accounts.

We engaged in targeted consultations with custodians and investment dealers through the Canadian Securities Lending Association (CASLA) and IIAC to find out more about the custodian and investment dealer back-office systems used in client account vote reconciliation and the implications for possible and actual double or multiple voting.

6. Key Findings to Date -- Meeting Vote Reconciliation

The following are our five key findings to date on the meeting vote reconciliation process based our Shareholder Meeting Review and our work with the Technical Working Group.

Finding 1: We identified over-reporting and over-voting in all meetings of the Shareholder Meeting Review; however the number of vote entitlements and proxy votes involved did not appear to be material.

In the Shareholder Meeting Review, we identified apparent over-reporting and over-voting in all six shareholder meetings.{7} However, the number of vote entitlements and proxy votes involved in each case was immaterial with respect to:

• the total number of proxy votes submitted for the meeting,

• the relative percentages of proxy votes cast For/Against/Withheld as applicable on the matters being voted on, or

• the outcome of the votes (i.e. in no case would the outcome of any vote have been changed).

We note that meeting tabulators did not always agree with our assessment that over-reporting or an over-vote had occurred. This issue is discussed below in Finding 4.

Finding 2: The over-reporting and over-voting we reviewed was due to meeting tabulators missing or having incorrect vote entitlement information when calculating the Official Vote Entitlement. The causes of missing or incorrect information included the use of paper omnibus proxies and human and technology errors. In the reviews we conducted, we did not find evidence that over-voting was caused by intermediaries submitting "too many" proxy votes because they allocated too many vote entitlements to client accounts.

In the Shareholder Meeting Review, each instance of over-reporting or over-voting that we reviewed was ultimately related to missing or incorrect vote entitlement information that resulted in intermediaries not receiving their full Official Vote Entitlement from the meeting tabulator. In other words, over-voting appeared to be caused by too few vote entitlements being allocated to the Official Vote Entitlement for the intermediary (which signified problems with meeting vote reconciliation). In our review, we did not find evidence that over-voting was due to intermediaries allocating vote entitlements to client accounts that exceeded the number of shares that those intermediaries held in accounts with depositories and/or other intermediaries.

The causes of missing or incorrect information included the use of paper omnibus proxies and human and technology errors. Below are some examples:

• Paper intermediary omnibus proxies were sent to tabulator but not actually received

Broadridge generated and mailed a number of intermediary omnibus proxies on behalf of its U.S. intermediary clients for a meeting. The meeting tabulator received some, but not all, of the intermediary omnibus proxies mailed.{8}

• Coding error prevented the generation of intermediary omnibus proxy by Broadridge

Broadridge could not generate an intermediary omnibus proxy for an intermediary client for an annual meeting because there was an error in the coding that meant that an intermediary omnibus proxy would only be generated if the meeting was a special meeting.

• Incorrect intermediary name in an intermediary omnibus proxy

An intermediary omnibus proxy used an outdated name for the client intermediary.

The Technical Working Group also discussed other potential issues that could lead to the meeting tabulator not receiving complete vote entitlement information for an intermediary, such as:

• whether some intermediaries are not providing information to their intermediary service provider (e.g. Broadridge) to allow it to generate intermediary omnibus proxies, and

• Canadian issuers being unfamiliar or uncomfortable with the steps required to obtain a DTC omnibus proxy.

Finding 3: A significant factor that would appear to increase the risk of over-reporting and over-voting is that intermediaries do not have access to their Official Vote Entitlement. As a result, they do not know if the meeting tabulator has missing or incomplete vote entitlement information.

A significant factor that would appear to increase the risk of over-reporting and over-voting is that intermediaries do not have access to their Official Vote Entitlement. As a result, intermediaries do not know if their Official Vote Entitlement as calculated by the meeting tabulator is less than the vote entitlement that they have calculated for themselves or if they do not have an Official Vote Entitlement at all.

Broadridge partially addresses this gap by offering an Over-Reporting Prevention Service to subscribing intermediaries. The Over-Reporting Prevention Service generates a Broadridge-Calculated Vote Entitlement that is intended to be an indicator of the Official Vote Entitlement. The Broadridge-Calculated Vote Entitlement is calculated using:

• information Broadridge obtains from depository data feeds, and

• data provided by intermediaries that is used by Broadridge to generate intermediary omnibus proxies.{9}

Subscribing intermediaries can compare the total number of vote entitlements they have calculated to the Broadridge-Calculated Vote Entitlement to identify if there are any discrepancies.

However, Broadridge's Over-Reporting Prevention Service and the Broadridge-Calculated Vote Entitlement as currently implemented do not perfectly substitute for an intermediary finding out its Official Vote Entitlement for a meeting. Most importantly, the Broadridge-Calculated Vote Entitlement is not based on the information that the meeting tabulator actually uses to calculate the Official Vote Entitlement, i.e. the omnibus proxies that the meeting tabulator actually receives. If the meeting tabulator is missing or has incorrect information, as outlined in Finding 2 above, the Broadridge-Calculated Vote Entitlement for an intermediary will not match the Official Vote Entitlement.

We also found through the Shareholder Meeting Review that for some meetings that occurred during the 2014 proxy season, the Broadridge-Calculated Vote Entitlements for some intermediaries contain duplicates of certain DTC positions. Specifically, a number of intermediaries held shares both directly in CDS and through a DTC account with CDS. The DTC positions held through CDS were included in both the DTC data feed as well as the CDS data feed into Broadridge, resulting in both positions being counted in the Broadridge-Calculated Vote Entitlements for some intermediaries.{10}

Finding 4: Meeting tabulators employed different methods to reconcile proxy votes from intermediaries to Official Vote Entitlements. As a result, a meeting tabulator's determination of whether an intermediary was in an over-vote position appeared to depend to a certain extent on the particular reconciliation method used by that meeting tabulator. A significant cause of these different reconciliation methods is the lack of protocols as to when and how to use numeric intermediary identifiers to match intermediary proxy votes to Official Vote Entitlements.

In the Shareholder Meeting Review, we asked the meeting tabulators to explain why they accepted proxy votes in cases where we identified an over-vote.

Based on the responses provided, we found that meeting tabulators used different methods to reconcile proxy votes from intermediaries to Official Vote Entitlements. In some cases this meant that proxy votes from intermediaries were reconciled to Official Vote Entitlements for intermediaries with different names, usually on the basis of a common numeric intermediary identifier. However, different meeting tabulators used different methods to do so.

For example:

• One meeting tabulator reconciled or matched proxy votes to an Official Vote Entitlement if the meeting tabulator could link the two intermediaries through a CUID, FINS number or DTC number.

In one case, Broadridge sent the meeting tabulator a paper intermediary omnibus proxy from Intermediary B allocating a vote entitlement to Intermediary A. However, the meeting tabulator did not receive the document and therefore theoretically could not establish an Official Vote Entitlement for Intermediary A. The meeting tabulator nevertheless accepted Intermediary A's proxy votes by reconciling them to the Official Vote Entitlement of Intermediary B. The meeting tabulator did so because Intermediary A and Intermediary B had a common DTC number and the meeting tabulator was aware that Intermediary B was the clearing broker for Intermediary A.

• Another meeting tabulator reconciled or matched proxy votes to an Official Vote Entitlement if the other intermediary had a similar name and the same CUID.{11} The tabulator would follow up and try to resolve potential over-vote situations with intermediaries.

These different practices result from the fact that there is no single, industry-wide protocol as to when and how to use numeric intermediary identifiers to match intermediary proxy votes to Official Vote Entitlements in lieu of matching by name. Nor is there a cross-reference or association document as to the numeric identifiers that are associated with particular intermediary names. The intermediary omnibus proxies generated by Broadridge only contain intermediary names and Broadridge client numbers, while Broadridge's formal vote reports can contain, among other identifiers, intermediary names, CUIDs, FINS numbers and DTC numbers.

Finding 5: Some meeting tabulators made errors resulting in valid proxy votes being rejected or not counted. These errors were not detected because there is no communication between meeting tabulators and intermediaries about whether proxy votes are accepted, rejected or pro-rated.

In the Shareholder Meeting Review, we asked for clarification in several situations where the meeting tabulator rejected or pro-rated an intermediary's proxy votes although the meeting documentation indicated there was a sufficient Official Vote Entitlement for the intermediary.

In two of those situations, the meeting tabulators acknowledged that a tabulation error had been made which resulted in valid proxy votes from intermediaries not being counted. In neither case was the number of proxy votes involved material to:

• the relative percentages of proxy votes cast For/Against/Withheld as applicable on the matters being voted on, or

• the outcome of the votes (i.e. in no case would the outcome of any vote have been changed).

However, in one case, the number of votes involved represented approximately 13% of the votes cast on a particular matter for that meeting.{12}

But for the Shareholder Meeting Review, these errors would not have been detected because there is no communication between meeting tabulators and intermediaries about whether proxy votes are accepted, rejected or pro-rated.

7. Information Obtained -- Client Account Vote Reconciliation

CASLA informed us that the bulk of share lending activity in Canada occurs through institutional securities lending programs administered by custodians who act as agents for lenders. The major custodians are:

• CIBC Mellon,

• RBC Investor Services,

• State Street, and

• Northern Trust.

The lenders are custodial-services clients and are typically large institutional investors such as pension funds, mutual funds, endowment funds and insurance companies. These lenders are paid fees for participation in these securities lending programs and treat securities lending as a source of revenue.

We heard from CASLA that each of the four custodians have established back-office systems that track the number of shares that have been lent from each individual client account. The following is an illustrative example:

A custodian has a client that holds 100,000 shares in a custody account. If the client participates in the custodian's securities lending program and 10,000 shares are lent, the custodian's back-office systems would "move" the 10,000 shares from the custody account. There would be a record or coding that these 10,000 shares could not be voted by the client, and no vote entitlements would be allocated for those shares if they were still lent on the record date for a shareholder meeting.

According to CASLA, however, custodians also have recall procedures in place to support clients who wish to vote. CASLA explained that clients either provide standing instructions to their custodian to recall shares for all shareholder meetings, or provide notice on a case-by-case basis to the custodian to recall the shares. A custodian would take steps pursuant to these instructions and pursuant to the recall procedures agreed upon with the client to replace any lent shares so that they would be in the client's custody account on the record date for the shareholder meeting.

We also discussed with IIAC how investment dealer back-office systems track lent or pledged shares from retail margin accounts and whether there is a double or multiple voting risk. A margin account is an account that an investor has with its investment dealer that allows the investor to trade securities on margin, i.e. with money borrowed from the investment dealer. Under the typical terms of a margin agreement, if the investor draws on the margin and is in debt to the investment dealer, a subset of the securities in the margin account is allocated to serve as collateral to cover the drawn-upon amount. The assets that are allocated to serve as margin collateral are available for pledging or lending by the investment dealer and will be included in the investment dealer's own holdings. These holdings are in fungible bulk and include all securities available for pledging or lending. A loan or pledge of shares will be reflected as a reduction in the investment dealer's account with CDS.

Investment dealers do not have back-office systems that eliminate possible double or multiple voting for retail margin accounts, because there are no linkages between the systems that track lent or pledged shares and the systems that track individual client account holdings. However, we heard from IIAC that they think that the risk of actual double or multiple voting occurring in respect of retail margin accounts is low for the following reasons:

1. Shares are less likely to be used as margin collateral than other margin account assets. Generally, investment dealers use back office systems that employ a logic known as a "segregation hierarchy" to determine which margin account assets to use as margin collateral. This process occurs on a daily basis. The logic will look to margin account assets in the following order:

• cash or cash equivalents,

• fixed income securities, and

• equity securities.

2. The likelihood of a share actually being lent or pledged and voted is relatively low. Where shares are used as margin collateral and are available to be lent out or pledged by the dealer, the shares are often not lent out to other intermediaries because there is insufficient quantity to meet a borrower's demand (and thus remain in the investment dealer's inventory). In other instances, shares may be pledged by an investment dealer to its parent bank as collateral on call loans, and are also not voted.

We are continuing to review client account reconciliation practices and to analyze the extent to which they appear to cause double or multiple voting concerns.

8. Next Steps

It is crucial that the proxy voting infrastructure support accurate, reliable and accountable vote reconciliation. Ultimately, the proxy voting infrastructure is meant to operate for the benefit of investors and issuers. The current proxy voting infrastructure is antiquated and fragmented and needs to be improved. Our review to date has clearly demonstrated the need for the following five improvements:

1. modernizing how meeting tabulators receive omnibus proxies (Finding 2),

2. ensuring the accuracy and completeness of vote entitlement information in omnibus proxies (Finding 2),

3. enabling intermediaries to find out their Official Vote Entitlement for a meeting (Finding 3),

4. increasing consistency in how tabulators reconcile proxy votes to Official Vote Entitlements (Finding 4), and

5. establishing communication between meeting tabulators and intermediaries about whether proxy votes are accepted, rejected or pro-rated (Finding 5).

For the 2015 proxy season, all the entities that play key roles in vote reconciliation should assess their meeting vote reconciliation processes to identify and implement any immediate steps they can take to improve the accuracy and reliability of vote reconciliation. In particular:

• Intermediaries should take appropriate steps to ensure that they provide vote entitlement information to meeting tabulators in a timely and accurate manner. In particular, intermediaries that use Broadridge as a service provider should verify that they have provided the requisite information for Broadridge to generate intermediary omnibus proxies and that the information provided to Broadridge is accurate.

• At our request, Broadridge has developed an up-to-date cross-reference or association document that links the various numeric identifiers for intermediaries with the relevant intermediary names. STAC should work with its members to develop consistent and transparent standards for how meeting tabulators use this document to reconcile intermediary proxy votes to Official Vote Entitlements.

In addition, we intend to review in 2015 one or more proxy contests that have occurred to determine if there are any vote reconciliation issues that are specific to proxy contests. We would like to explore whether factors such as higher volumes of proxy votes, revocations of previous proxy votes, and the use of a dissident form of proxy pose specific challenges to accurate meeting vote reconciliation.

For the 2016 proxy season, we will direct the key entities that engage in vote reconciliation to work collectively to develop appropriate industry protocols for meeting vote reconciliation. Having industry protocols would support:

• accuracy in the information used to calculate the Official Vote Entitlement and disclosure of proxy voting results,

• reliability, by reducing inconsistency in vote reconciliation practices, and

• accountability, by providing issuers, investors and regulators with transparent protocols that can be used to evaluate the performance of the key entities in the proxy voting infrastructure.

The protocols would:

• specify the roles and responsibilities that depositories, intermediaries, Broadridge and the meeting tabulator have in meeting vote reconciliation, and

• outline the specific operational processes that each of these key participants is expected to implement in vote reconciliation, including the enhanced use where appropriate of electronic methods of data transmission and communication.

The protocols would, at a minimum, address the five areas requiring improvement that we have identified through our Shareholder Meeting Review and work with the Technical Working Group. We will also use the information obtained from the planned proxy contest review to identify other areas that should be addressed by the protocols.

We intend to continue taking a leadership role by overseeing the development of these protocols. We will also consider if any new rules need to be made in order to allow the various parties to effectively implement these protocols. We may recommend mandating aspects of the protocols and/or regulating entities in the proxy voting infrastructure if it appears to us that this would be necessary or appropriate.

Finally, we also intend to continue gathering more information on the intermediary practices used in client account vote reconciliation. For example, we intend to gain a better understanding of investment dealer practices for shares in institutional margin accounts and that are lent through investment dealer securities lending programs. We will provide a further update should we determine to take any steps in respect of client account reconciliation practices. We invite issuers, investors and other market participants to contact us if they have information they wish to share on this issue.

9. Questions

Please refer your questions to any of:

{1} The Consultation Paper also sought comment on three other issues that had been identified by commenters as potentially affecting the reliability and integrity of the proxy voting infrastructure but that we did not intend to focus on:

• the NOBO-OBO concept,

• gaps in managed account information, and

• the level of accountability or regulatory oversight of service providers.

{2} The OSC roundtable was public and a transcript is available at: http://www.osc.gov.on.ca/documents/en/Securities-Category5/csa_20140129_54-401_roundtable-transcript.pdf

{3} The Consultation Paper used the term over-reporting to refer to this phenomenon. After further analysis, we think over-voting is a more descriptive term as it captures the concept that the discrepancy involves actual proxy votes submitted by an intermediary. We use the term over-reporting elsewhere in this Notice to refer to a discrepancy between the vote entitlements as calculated by an intermediary and the Official Vote Entitlement as calculated by the meeting tabulator. We also note that some commenters define over-voting as a situation where the same share may be voted more than once. We think that a more precise term for this situation is double or multiple voting. We discuss double or multiple voting later in the Notice.

{4} See STAC's comment letter at: http://www.stac.ca/Public/PublicShowFile.aspx?fileID=218

{5} Due to resource and timing constraints, we determined that it was not feasible to conduct a review that would provide us with statistically significant findings regarding the causes of over-reporting and over-voting. We therefore determined that the review would be qualitative in nature.

{6} Broadridge represents intermediaries that hold approximately 97% of all beneficial positions in Canada. See Broadridge's comment letter at: https://www.osc.gov.on.ca/documents/en/Securities-Category5-Comments/com_20131113_54-401_bfsinc.pdf

{7} Please refer to Appendix C -- Shareholder Meeting Review: Objective, Scope and Methodology for an explanation of how we identified over-reporting and over-voting for purposes of the Shareholder Meeting Review.

{8} Some meeting tabulators also received intermediary omnibus proxies by electronic feeds but will require a stamped or otherwise validly executed paper form of proxy (including a form of proxy transmitted in .pdf format) to establish Official Vote Entitlements.

{9} And where applicable, the NOBO omnibus proxy.

{10} Broadridge informed us that it is working to address this situation and expects to implement a solution prior to the 2015 proxy season.

{11} More precisely, the same first three characters of a CUID which identify a company.

{12} The intermediaries in question did not submit proxy votes on all matters being voted on at the meeting.

CSA Staff Notice 54-303

Appendix A Meeting Vote Reconciliation

1. What is Vote Reconciliation?

Vote reconciliation is the process by which proxy votes from registered holders and voting instructions from beneficial owners of shares are reconciled against the securities entitlements in the intermediated holding system. Vote reconciliation is implemented through the proxy voting infrastructure -- the network of organizations, systems, legal rules and market practices that support the solicitation, collection, submission and tabulation of proxy votes for a shareholder meeting.

There are two distinct aspects of vote reconciliation.

The first aspect is where intermediaries reconcile and allocate voting entitlements to individual client accounts. We refer to this as client account vote reconciliation. Client account vote reconciliation involves the internal back-office systems of intermediaries and how they track and allocate vote entitlements for individual client accounts.

The second is where meeting tabulators reconcile proxy votes to intermediary vote entitlements, which we refer to as meeting vote reconciliation. Meeting vote reconciliation involves the systems and process that link depositories, intermediaries and meeting tabulators with one another in order for the following three things to occur:

1. Depositories and intermediaries provide vote entitlement information to meeting tabulators through omnibus proxies,

2. Meeting tabulators calculate Official Vote Entitlements for intermediaries, and

3. Meeting tabulators reconcile intermediary proxy votes to the Official Vote Entitlements.

2. The Three Phases of Meeting Vote Reconciliation

1. Depositories and intermediaries provide vote entitlement information to meeting tabulators through omnibus proxies

The first phase of meeting vote reconciliation is typically triggered several days after the record date for a meeting.

In functional or operational terms, each depository and intermediary at each tier of the intermediated holding system notifies the meeting tabulator of the vote entitlements that their intermediary clients are entitled to. This notification occurs through depositories and intermediaries sending omnibus proxies to meeting tabulators.

In legal terms, the depository or intermediary who is the registered holder or who itself holds a proxy executes the omnibus proxy to give its clients authority to vote the number of shares in the client's account as at the record date and sends the executed omnibus proxy to the meeting tabulator.

The two main types of omnibus proxies used in Canada are:

• depository omnibus proxies that depositories use to allocate vote entitlements/give voting authority to client intermediaries that are depository participants, and

• intermediary omnibus proxies that custodians and investment dealers use to allocate vote entitlements/give voting authority to client intermediaries.

This chain of cascading omnibus proxies is intended to allow the intermediary that is closest to the beneficial owner to submit proxy votes directly to the meeting tabulator on behalf of beneficial owner clients. This intermediary will submit proxy votes to the meeting tabulator for all its beneficial owner clients that have submitted voting instructions on an aggregate basis, i.e. the meeting tabulator generally has no insight into:

• the identities of an intermediary's beneficial owner clients,

• how many vote entitlements a specific beneficial owner client has in its account with the intermediary, or

• how a particular beneficial owner client voted.

The exception is where a reporting issuer conducts a NOBO solicitation directly. If a reporting issuer conducts a direct NOBO solicitation, the intermediary will also allocate vote entitlements to management of a reporting issuer through a NOBO omnibus proxy. In legal terms, the intermediary executes an omnibus proxy that gives management authority to vote the number of shares that are in the intermediary's NOBO client accounts upon receipt of voting instructions. In that case, the meeting tabulator will know:

• the identities of an intermediary's NOBO clients,

• how many vote entitlements the NOBO client has in its account with the intermediary, and

• how the NOBO client voted.

In practice, most intermediaries provide data to Broadridge about their intermediary clients that Broadridge will use to generate and send intermediary omnibus proxies{1} to the meeting tabulator. Broadridge will also receive voting instructions from beneficial owners{2} on behalf of its intermediary clients and submit proxy votes to the meeting tabulator.

2. Meeting tabulators calculate Official Vote Entitlements for intermediaries

The second phase of meeting vote reconciliation involves the meeting tabulator establishing the vote entitlement for an intermediary. As noted above, depositories and intermediaries will send to meeting tabulators depository omnibus proxies and intermediary omnibus proxies that allocate vote entitlements to their intermediary clients. The meeting tabulator will use the vote entitlement information in these documents{3} to establish the Official Vote Entitlement for each intermediary.

Where the issuer chooses to do a NOBO solicitation, intermediaries (through Broadridge) will also send the meeting tabulator a NOBO omnibus proxy that the tabulator will use to establish the Official Vote Entitlement for NOBOs.

The Official Vote Entitlement for an Intermediary is therefore:

[Vote entitlements allocated to the intermediary in the depository omnibus proxies received by the tabulator]

plus

[Vote entitlements allocated to the intermediary in any intermediary omnibus proxy received by the tabulator]

minus

[Vote entitlements the intermediary allocates to another intermediary through an intermediary omnibus proxy received by the tabulator]

minus

[If the issuer is conducting a direct NOBO solicitation, vote entitlements the intermediary allocates to issuer management in respect of the intermediary's NOBO accounts through a NOBO omnibus proxy received by the tabulator].

There is no process in place for intermediaries to see and verify their Official Vote Entitlement for a meeting. Instead, Broadridge offers an Over-Reporting Prevention Service that generates a Broadridge-Calculated Vote Entitlement. This number is intended to be an indicator of the Official Vote Entitlement. It is calculated using information Broadridge obtains from depository data feeds and data in its system provided by intermediaries and that is used to generate intermediary omnibus proxies.{4}

The Broadridge-Calculated Vote Entitlement for an intermediary is therefore:

[Vote entitlements allocated to the intermediary in the depository data feeds received by Broadridge]

plus

[Vote entitlements allocated to the intermediary based on information that intermediaries have provided to Broadridge's system that is used to generate intermediary omnibus proxies]

minus

[Vote entitlements the intermediary allocates to another intermediary by providing information to Broadridge's system that is used to generate intermediary omnibus proxies]

minus

[If the issuer is conducting a direct NOBO solicitation, vote entitlements the intermediary allocates to issuer management by providing NOBO account information to Broadridge's system]

Over-reporting occurs if the vote entitlement an intermediary calculates for itself is greater than the Official Vote Entitlement, i.e. Intermediary-calculated vote entitlement > Official Vote Entitlement.

3. Meeting tabulators reconcile intermediary proxy votes to the Official Vote Entitlements

The third phase of meeting vote reconciliation occurs when meeting tabulators review proxy votes submitted by each intermediary and reconciles the intermediary's proxy votes to the intermediary's Official Vote Entitlement.

Over-voting occurs if the number of proxy votes an intermediary submits is greater than the Official Vote Entitlement, i.e. Intermediary proxy votes > Official Vote Entitlement.

There is no process in place for intermediaries to find out:

• whether a meeting tabulator has identified an over-vote for an intermediary, or

• whether a meeting tabulator has accepted, rejected or pro-rated an intermediary's proxy votes.

Instead, if an intermediary subscribes to Broadridge's Over-Reporting Prevention Service, the Over-Reporting Prevention Service will pend voting instructions if the number of proxy votes submitted by the subscribing intermediary through the Broadridge system exceeds the Broadridge-Calculated Vote Entitlement and require that the intermediary make adjustments to avoid exceeding the Broadridge-Calculated Vote Entitlement.

3. The Key Players and Their Roles in Meeting Vote Reconciliation

The following chart summarizes the key players and their role in vote reconciliation.

Key Players in Vote Reconciliation

|

<<Key Players>> |

<<Role in Meeting Vote Reconciliation>> |

||

|

|

|||

|

Depositories (CDS and DTC) |

• |

allocate vote entitlements to intermediary participants through depository omnibus proxies |

|

|

|

• |

send the depository omnibus proxies to the meeting tabulator or issuer |

|

|

|

• |

provide data feeds to Broadridge that are used to calculate the Broadridge-Calculated Vote Entitlement |

|

|

|

|||

|

Intermediaries |

• |

provide client intermediary information to Broadridge to generate intermediary omnibus proxies that allocate vote entitlements to their client intermediaries (e.g. clearing broker allocates vote entitlements to correspondent broker) |

|

|

|

• |

if applicable, provide NOBO data to Broadridge to generate the NOBO list and the NOBO omnibus proxy |

|

|

|

|

Note: A widely-held reporting issuer would typically have several hundred intermediaries submitting proxy votes. |

|

|

|

|||

|

Broadridge (for clients who have retained its services) |

• |

assists intermediaries in various aspects of proxy voting including solicitation of voting instructions from beneficial owners and submitting proxy votes for intermediaries to tabulators |

|

|

|

• |

offers Over-Reporting Prevention Service that: |

|

|

|

|

• |

generates the Broadridge-Calculated Vote Entitlement for each subscribing intermediary to assist them with managing the risk of over-reporting |

|

|

|

• |

pends subscribing intermediary voting instructions that exceed the Broadridge-Calculated Vote Entitlement to assist them with managing the risk of over-voting |

|

|

• |

generates and sends to the meeting tabulator intermediary omnibus proxies based on information provided by intermediaries |

|

|

|

• |

if applicable, generates and sends to the meeting tabulator the NOBO omnibus proxy and NOBO list based on information provided by intermediaries |

|

|

|

|||

|

Meeting tabulator |

• |

establishes the Official Vote Entitlement for an intermediary using the depository omnibus proxies and intermediary omnibus proxies (and if applicable, the NOBO omnibus proxy) it has received |

|

|

|

• |

tabulates proxy votes received from each intermediary and accepts, rejects or pro-rates votes depending on whether the number of votes is supported by or exceeds the Official Vote Entitlement for that intermediary |

|

{1} And if applicable, NOBO omnibus proxies.

{2} If an issuer conducts a direct NOBO solicitation, Broadridge will only receive voting instructions from OBOs on behalf of its intermediary clients to submit proxy votes to the meeting tabulator. NOBOs will be submitting voting instructions directly to management of the issuer.

{3} The meeting tabulator will also refer to the list of registered holders to determine the Official Vote Entitlements. However, the vast majority of the shares are held in the intermediated holding system.

{4} And if applicable, NOBO omnibus proxies.

CSA Staff Notice 54-303

Appendix B Summary of Comments

1. General

The commenters generally acknowledged the importance of the proxy voting infrastructure in the capital markets. Through the comment process, a number of commenters, including institutional investors and issuers, expressed a lack of confidence in the accuracy and integrity of the proxy voting system. They viewed over-reporting and over-voting as evidence that accurate vote reconciliation is not occurring within the proxy voting infrastructure. While there was no consensus on the prevalence of over-reporting and over-voting in Canada, some commenters were under the impression that over-reporting and over-voting were not uncommon. STAC provided statistics that, for its members who tracked over-reporting and over-voting, approximately 51% of meetings in 2013 had occurrences of over-reporting and over-voting.

These commenters said that the opacity and complexity of the proxy voting system make it very difficult to understand and assess the infrastructure as a whole. They were concerned that they have no assurance as to whether the votes are received and counted as instructed by the investors.

Intermediaries and their service provider on the other hand emphasized that the proxy voting system is generally well functioning and is not "broken".

Despite these differing views, commenters generally agreed that improvements could be made, and supported securities regulators becoming involved in reviewing the proxy voting infrastructure.

There was no consensus as to the causes or specific solutions to the problem. Some commenters supported improvements to the system that are incremental and take into account the existing structure and improvements that have already been made to it, after a cost-benefit analysis. The solutions proposed by these commenters included ways to improve communication and collaboration between various participants in the system and the development of industry protocols. Others asked the securities regulators to impose prescriptive rules and to audit the entire system. Some commenters encouraged us to take a big picture approach and consider a re-design of the proxy voting system, such as establishing an entity that performs a clearing and settlement function for votes much like the depositories.

2. Meeting Vote Reconciliation

Several commenters, including the institutional investors, transfer agents, intermediaries and proxy solicitation firms, indicated that reconciliation challenges are caused in part by missing documentation. In particular, STAC indicated that for its members who tracked over-reporting and over-voting, approximately 22% of the meetings in 2013 had reconciliation issues caused by missing or incomplete omnibus proxies.

According to the commenters, missing documentation can be a result of:

• incorrect information provided by intermediaries to their service provider (e.g. Broadridge) for the purpose of generating intermediary omnibus proxies,

• reliance on paper omnibus proxies, and

• DTC omnibus proxy sent by DTC to the issuer not received by the transfer agent/meeting tabulator.

Intermediaries also noted reconciliation challenges where shares were held in both CDS and DTC. They indicated that they had difficulty reconciling their positions with the vote entitlement information on Broadridge's system because certain DTC positions did not appear to have been reflected in the electronic feeds that Broadridge received.

Some commenters observed that direct NOBO solicitations by issuers, while in and of themselves are not a cause of reconciliation issues, often highlight the phenomena of over-reporting and over-voting.

We were further informed by some institutional investors, intermediaries and transfer agents that, while rarely used, restricted proxies could be a source of reconciliation discrepancies.

We have also received comments regarding the practices transfer agents use to tabulate proxy votes. Intermediaries, institutional investors and proxy solicitation firms would like more transparency surrounding the methods that meeting tabulators use to tabulate proxy votes. They believe that meeting tabulators should communicate to intermediaries whether votes are accepted, pro-rated or rejected. They suggested that most instances of over-voting can be resolved if there is better communication between intermediaries and meeting tabulators.

The commenters generally supported an end-to-end confirmation system that will allow investors to receive confirmation that their votes have been received by the meeting tabulator and voted correctly.

3. Client Account Vote Reconciliation

Transfer agents suggested to us that over-voting was caused by intermediaries not properly allocating vote entitlement to their client accounts. They viewed over-voting as evidence that these intermediaries were reallocating vote entitlements to client accounts that significantly exceeded the intermediary's vote entitlement for that meeting. Some investors and issuers raised a similar concern. They questioned why vote entitlements are not tracked or reconciled to the same extent as dividend entitlements and wanted us to review whether some intermediary back-office systems allowed double or multiple voting.

The main area where concerns about double or multiple voting have arisen appears to be securities lending. We were informed that institutional lending programs do not appear to give rise to double or multiple voting because custodians use the pre-record date reconciliation method, i.e. they reconcile vote entitlements of lent shares prior to the record date. However, retail margin account lending appears to pose a risk of double or multiple voting because investment dealers use the post-record date reconciliation method, i.e. they allocate vote entitlement to all lent shares and only make adjustments post record date if there is an over-vote situation.

These commenters suggested that intermediaries should be required to adopt pre-record date reconciliation. Institutional investors, in particular, called for one-for-one vote reconciliation, i.e. for each outstanding issuer share, there would be a single entity identified as having authority to provide voting instructions.

Intermediaries, however, queried whether it is practical or feasible to implement one-for-one reconciliation due to the fungible nature of securities, the complexities of the intermediated holding system and the massive operational infrastructure that is required to support one-for-one reconciliation.

We have also received comments regarding who (the lender or the borrower) should have the right to vote in a securities lending transaction. There was no consensus on this issue.

4. Other Issues

NOBO-OBO Concept

There was no consensus on the impact of the NOBO-OBO concept on the integrity of the proxy voting system. A number of issuers posited that the NOBO-OBO concept is an impediment to communication between issuers and shareholders and reduces transparency in the proxy voting system. They suggested that the NOBO-OBO concept be eliminated, or alternatively, that there at least be a mechanism to temporarily lift the OBO status to enable issuers and meeting tabulators to identify the OBOs.

Institutional investors and intermediaries, on the other hand, believed that the OBO-NOBO concept in and of itself does not compromise the integrity of the proxy voting system. They said that the elimination of the NOBO-OBO concept will not significantly reduce the complexity of the proxy voting system because the complexity is in large part due to the holding of securities through intermediaries. They further submitted that any reform to the NOBO-OBO concept should recognize investors' legitimate preference to maintain anonymity. Some proxy advisory firms raised the same concern about the impact of any reform on the ability of investors to vote confidentially.

Managed Account Information

We have received comments from certain commenters regarding whether there are gaps in managed account information that would result in the inability of investment managers to vote. Intermediaries and their service provider indicated that they were not aware of issues relating to managed account processing. However, certain commenters suggested that there are issues that could arise and warrant further research, including incorrect [account] set-up between intermediaries.

Accountability of Service Providers

Commenters noted that the activities of a number of service providers to support proxy voting are not currently regulated. They further noted the lack of documented process and accountability with respect to some of these activities. Some institutional investors suggested that all major service providers within the proxy voting system should be designated as "market participants" under securities law in order to promote accountability. Intermediaries on the other hand believed that market mechanisms and the existing framework have worked well to support accountability, and indicated that participants in the system have changed their practices in response to the market. They therefore supported an industry developed solution and would only seek guidance from securities regulators if industry is not complying with its own standards.

CSA Staff Notice 54-303

Appendix C Shareholder Meeting Review Objectives, Scope and Methodology

1. Objectives

The objectives of the Shareholder Meeting Review were to:

• allow the key participants in the proxy voting infrastructure to develop a better understanding of how meeting vote reconciliation actually works, i.e how the various processes that were identified and outlined in the Consultation paper are actually implemented for shareholder meetings, and

• identify and analyze instances of over-reporting and over-voting.

By identifying instances of over-reporting and over-voting, we hoped to identify potential gaps in the proxy voting infrastructure. We were particularly interested in finding out whether over-reporting and over-voting were caused by tabulators not receiving some or all of the documents necessary to correctly establish an intermediary's Official Vote Entitlement, i.e. problems with meeting vote reconciliation. We were also interested in finding out whether there was any evidence that over-voting was caused by intermediaries allocating too many vote entitlements to their client accounts in comparison to the number of shares they held in their accounts with depositories or other intermediaries, i.e. problems with client account vote reconciliation. Some commenters have suggested that over-voting is extremely common and is evidence of large-scale over-allocation of vote entitlements.

We conducted the Shareholder Meeting Review with the assistance of a proxy solicitor. The proxy solicitor helped us to design and conduct the review.{1}

2. Scope

Due to resource and timing constraints, we determined that it was not feasible to conduct a review that would provide us with statistically significant findings regarding the causes of over-reporting and over-voting.

We therefore determined that the review would be qualitative in nature.

We selected six reporting issuers from Ontario, Alberta, British Columbia and Quebec. These issuers held an uncontested, uncontentious shareholder meeting in 2014.{2} Five of the issuers had filed a report of voting results pursuant to section 11.3 of National Instrument 51-102 Continuous Disclosure Obligations. The sixth issuer was a venture issuer that was not subject to this requirement.

Our sample included issuers:

• that were listed on the Toronto Stock Exchange (TSX) and TSX Venture Exchange,

• that used different meeting tabulators,

• that were listed only in Canada and inter-listed in the U.S.,

• that were closely-- and widely-held,{3}

• that conducted direct NOBO solicitations and that solicited only through intermediaries,

• whose shares were the subject of securities lending activity around the record date,{4} and

• that operated in different industries.

3. Methodology

Our review had three main components:

1. Review of shareholder meeting documents to identify occurrences of over-reporting and over-voting,

2. Inquiries of meeting tabulators as to specific methods they used to reconcile proxy votes to Official Vote Entitlements (including the process they used to calculate those Official Vote Entitlements), and

3. Further investigation into specific instances of over-reporting and over-voting (including inquiries of specific intermediaries, Broadridge and CDS) to understand their causes, and whether they were isolated or systemic.

1. Document Review to Identify Potential Occurrences of Over-Reporting and Over-Voting

For each shareholder meeting, we obtained the documents that were used by the meeting tabulator to tabulate proxy votes. These included:

• registered holder proxies,

• depository omnibus proxies issued by CDS and DTC,

• intermediary omnibus proxies,

• NOBO omnibus proxies (if applicable),

• the list of registered holders maintained by the transfer agent,

• formal vote reports generated by Broadridge on behalf of intermediaries,

• restricted proxies, and

• the meeting tabulator's list of rejected or uncounted votes.

We reviewed the documents to identify instances of over-reporting and over-voting.{5}

(a) Identification of Over-Reporting -- Comparison of Broadridge-Calculated Vote Entitlements and Official Vote Entitlements

Over-reporting occurs at phase two of vote reconciliation and consists of a discrepancy between the vote entitlements that an intermediary (or its service provider Broadridge) has calculated and the Official Vote Entitlement as calculated by the meeting tabulator.

The meeting tabulator calculates the Official Vote Entitlement for an intermediary using the information in the depository omnibus proxies and intermediary omnibus proxies it has received. The depositories and Broadridge provide vote entitlement information in electronic form through data feeds as well; however, not all tabulators access all of these feeds. Furthermore, tabulators generally will not rely solely on electronic data to support an Official Vote Entitlement but will require a stamped or validly-executed paper form{6} of omnibus proxy.

We:

• identified the Broadridge-Calculated Vote Entitlement for each intermediary using the "Position" field for each intermediary in the formal vote report generated by Broadridge,{7}

• calculated the Official Vote Entitlement for each intermediary using the relevant depository omnibus proxies and intermediary omnibus proxies, and

• compared the Broadridge-Calculated Vote Entitlement{8} to the Official Vote Entitlement to identify any discrepancies.

Where the issuer conducted a NOBO solicitation, we also:

• compared the total number of vote entitlements in the NOBO list to the number of vote entitlements in the NOBO omnibus proxy, and

• identified the vote entitlements allocated by each intermediary in the NOBO omnibus proxy and confirmed that the vote entitlements allocated by the intermediary in the NOBO omnibus proxy did not exceed the positions contained in the depository omnibus proxies and intermediary omnibus proxies for that intermediary (i.e., each intermediary had sufficient entitlements to allocate the number of vote entitlements in the NOBO omnibus proxy).

(b) Identification of Over-Voting -- Comparison of Proxy Votes and Official Vote Entitlements

We reviewed the documents as outlined below to identify instances of over-voting.

Meeting tabulators receive proxy votes through paper formal vote reports generated by Broadridge on behalf of its client intermediaries. In addition, Broadridge also provides an electronic data feed whereby proxy votes are submitted electronically. Only some meeting tabulators access the electronic data feed.

Intermediaries can also submit a vote directly to the tabulator by using a document known as a restricted proxy, although this is rarely done.

Where an issuer conducts a NOBO solicitation, the issuer's management will submit proxy votes on behalf of NOBOs in accordance with instructions provided by the NOBOs to management. In the meetings reviewed, the meeting tabulator used the NOBO voting instruction forms (VIFs) to tabulate NOBO votes.

We:

• calculated the total number of proxy votes submitted by each intermediary using Broadridge's paper formal vote reports{9} and restricted proxies,

• identified the number of proxy votes rejected by the tabulator as over-votes using the list of rejected or uncounted votes, and

• compared the number of proxy votes submitted by each intermediary to the Official Vote Entitlement that the consultant calculated.

We also reviewed the list of rejected or uncounted votes provided by the tabulator to determine on what basis a tabulator rejected a vote.

2. Further inquiries of issuers and meeting tabulators

After the completion of the document review, we sent follow-up questions to issuers and meeting tabulators. In particular, we asked for clarification about how tabulators reconciled proxy votes to Official Vote Entitlements in the following instances:

• the meeting tabulator appeared to have accepted an intermediary's proxy votes although the documentation seemed to indicate that there was an over-vote;

• the meeting tabulator rejected or pro-rated an intermediary's proxy votes although the documentation seemed to indicate that the intermediary's Official Vote Entitlement was sufficient.

3. Detailed review of specific instances of over-reporting and over-voting

We identified specific cases of over-reporting and over-voting to investigate further. We organized meetings with two transfer agents, several Canadian intermediaries, Broadridge and CDS to further review two of the shareholder meetings. We reviewed the cases of over-reporting and over-voting and the various attendees shared information to explain why and how these cases occurred.

{1} References to actions we took in connection with the Shareholder Meeting Review encompass actions taken by the consultant as well.

{2} The matters considered at each of the shareholder meetings were approved by more than 60% of the shareholders who voted at the meeting.

{3} Based on Capital IQ data on retail ownership and whether the issuer had a single shareholder that held more than 10% of its shares.

{4} Based on Markit data on the number of shares outstanding on loan.

{5} We also compared the total number of vote entitlements in depository omnibus proxies with the total number of shares held by the depository in the transfer agent's list of registered holders. We found one instance of a discrepancy involving a very small number of shares the cause of which we have not as yet been able to determine. We found another instance of a discrepancy where the DTC omnibus proxy did not allocate vote entitlements with respect to a very small number of shares in a predecessor class that are reflected on the issuer's share register.

{6} This includes an omnibus proxy that is transmitted electronically in .pdf format, so long as it is stamped or validly executed.

{7} If an intermediary did not subscribe to the Over-Reporting Prevention Service, the share position field for that intermediary in the formal vote report contains the intermediary's "long" position in its record date file that it uploaded onto Broadridge's system.

{8} See footnote 7.

{9} We did not have access to any votes received electronically by the meeting tabulator.

CSA Staff Notice 54-303

Appendix D Glossary{1}

|

<<Term>> |

<<Meaning>> |

|

|

|

||

|

Beneficial owner |

An investor who is not a registered holder of shares, and whose ownership is through a securities entitlement in an intermediary account. |

|

|

|

||

|

Broadridge |

Refers to Broadridge Investor Communication Solutions, Canada, a subsidiary of Broadridge Financial Solutions, Inc. It is a service provider that assists intermediaries in various aspects of proxy voting, including solicitation of voting instructions from beneficial owners and submitting proxy votes on behalf of intermediaries to tabulators. |

|

|

|

||

|

Broadridge-Calculated Vote Entitlement |

For an intermediary that subscribes to the Over-Reporting Prevention Service, the vote entitlement of the intermediary as calculated by Broadridge that is intended to be an indicator of the Official Vote Entitlement. It is calculated using the depository data feeds and data in its system provided by intermediaries that is used to generate intermediary omnibus proxies and, if applicable, NOBO omnibus proxies. See vote entitlement. |

|

|

|

||

|

Broadridge client number |

A numeric identifier assigned by Broadridge to its intermediary clients. See intermediary identifier. |

|

|

|

||

|

Canadian Securities Lending Association (CASLA) |

A securities lending association in Canada. |

|

|

|

||

|

CDS |

Refers to the Canadian Depository for Securities Limited and its subsidiaries, including CDS Clearing and Depository Services Inc. CDS Clearing and Depository Services Inc. is the national securities depository in Canada. See also depository. |

|

|

|

||

|

CDS omnibus proxy |

The omnibus proxy CDS uses to allocate vote entitlements/give voting authority to client intermediaries that are CDS participants. See also depository omnibus proxy. |

|

|

|

||

|

Clearing broker |

A broker that is principal for clearing and settling a trade on behalf of another intermediary. See intermediary. |

|

|

|

||

|

Client account vote reconciliation |

The process by which intermediaries reconcile and allocate vote entitlements to individual client accounts. Client account vote reconciliation involves the internal back-office systems of intermediaries and how they track and allocate vote entitlements for individual client accounts. See vote reconciliation. |

|

|

|

||

|

CUID |

Stands for customer unit identifier. A four letter identifying code system assigned by CDS to institutions that clear and settle securities trades through CDS. The first three characters identify the company and the last character the unit within the company. See intermediary identifier. |

|

|

|

||

|

CUSIP |

Stands for Committee on Uniform Securities Identification Procedures. A nine digit identifier assigned to securities of issuers in the U.S. and Canada. The CUSIP system is owned by the American Bankers Association and operated by Standard & Poor's to facilitate the clearing and settlement process of securities. See intermediary identifier. |

|

|

|

||

|

Custodian |

A financial institutional that holds securities for another person or entity. Custodians in Canada also administer securities lending programs and act as agents for lenders which are typically large institutional investors. See intermediary. |

|

|

|

||

|

Depository |

In connection with clearing and settlement, an entity that takes custody of security certificates or maintains electronic records of securities holdings for participant financial institutions. |

|

|

|

||

|

Depository omnibus proxy |

The omnibus proxy depositories use to allocate vote entitlements/give voting authority to client intermediaries that are depository participants. See also omnibus proxy. |

|

|

|

||

|

Depository participant |

A person or company for whom a depository maintains an account in which entries may be made to effect a transfer or pledge of a security. |

|

|

|

||

|

Double or multiple voting |

A situation in the client account vote reconciliation process where more than one entity is allowed or not prevented from voting the same share. Possible double or multiple voting occurs when more than one entity may vote or is not prevented from voting the same share. Actual double or multiple voting occurs when two or more entities actually vote the same share. |

|

|

|

||

|

DTC |

Stands for Depository Trust Company, a subsidiary of Depository Trust and Clearing Corporation. It is the national securities depository in the United States. See depository. |

|

|

|

||

|

DTC number |

A numeric identifier assigned by DTC to its listed issuers. See intermediary identifier. |

|

|

|

||

|

DTC omnibus proxy |

The omnibus proxy DTC uses to allocate vote entitlements/give voting authority to client intermediaries that are DTC participants. See also depository omnibus proxy. |

|

|

|

||

|

End-to-end vote confirmation |

A communication to shareholders that allows them to confirm that their proxy votes and voting instructions have been properly transmitted by the intermediaries, received by the tabulator and tabulated as instructed. |

|

|

|

||

|

FINS number |

Stands for Financial Institutional Numbering System. A numeric identifier assigned by DTC to each bank, broker-dealer, insurance company, mutual fund, money manager, transfer agent and other institution engaged in securities processing. See intermediary identifier. |

|

|

|

||

|

Form of proxy |

A document by which a security holder or other person with authority to vote appoints a person or company as the security holder's nominee to attend and act for and on the security holder's behalf at a meeting of security holders. |

|

|

|

||

|

Formal vote report |