Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

CSA Staff Notice: 51-339 - Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2013

CSA Staff Notice: 51-339 - Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2013

CSA Staff Notice 51-339

Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2013

July 18, 2013

INTRODUCTION

This notice contains the results of the reviews conducted by the Canadian Securities Administrators (CSA) within the scope of their Continuous Disclosure (CD) Review Program. This program was established to review the compliance of the CD documents of reporting issuers{1} (issuers) to ensure they are reliable and accurate. The CSA seek to ensure that Canadian investors receive high quality disclosure from issuers.

In this notice, we summarize the results of the CD Review Program for the fiscal year ended March 31, 2013 (fiscal 2013). To raise awareness about the importance of filing compliant CD documents, we also discuss certain areas where common deficiencies were noted and provide examples to help issuers address these deficiencies in the following appendices:

• Appendix A -- Financial Statements Deficiencies

• Appendix B -- Management's Discussion and Analysis (MD&A) Deficiencies

• Appendix C -- Other Regulatory Disclosure Deficiencies

For further details on the CD Review Program, see CSA Staff Notice 51-312 (revised) Harmonized Continuous Disclosure Review Program.

RESULTS FOR FISCAL 2013

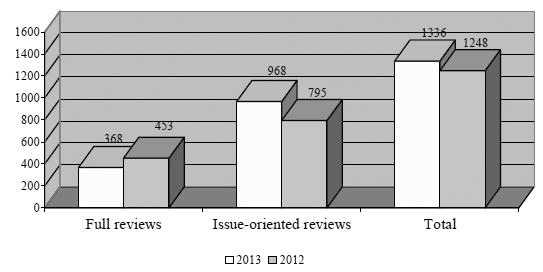

During fiscal 2013, a total of 1,336 CD reviews (368 full reviews and 968 issue-oriented reviews) were conducted. This is a 7% increase compared to the 1,248 CD reviews (453 full reviews and 795 issue-oriented reviews) completed during fiscal 2012.

Review Completed

The increased number of total reviews during fiscal 2013 reflects a slightly greater emphasis on issue-oriented reviews which increased due to certain CSA jurisdictions examining technical disclosure and IFRS specific topics on a larger sample of issuers. Technical issue-oriented reviews focused on compliance with National Instrument 43-101Standards of Disclosure for Mineral Projects (NI 43-101), and National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (NI 51-101). Specific topic issue-oriented reviews were conducted to determine issuers' compliance with a specific IFRS and to determine if the MD&A disclosure on a specific subject was compliant with Form 51-102F1 Management's Discussion & Analysis of National Instrument 51-102 Continuous Disclosure Obligations (Form 51-102F1).

OUTCOMES FOR FISCAL 2013

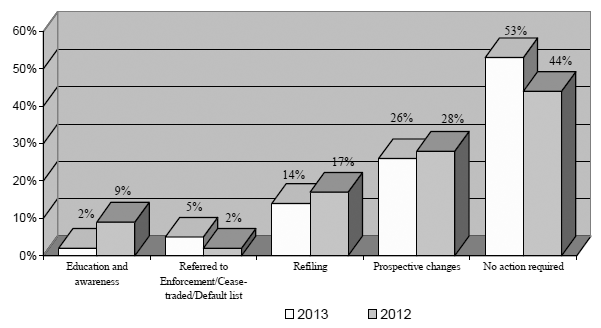

In fiscal 2013, 47% of our review outcomes required issuers to take action to improve their disclosure, compared to 56% in fiscal 2012.

Review outcomes

We classified the outcomes of the full and issue-oriented reviews in the five categories described in Appendix D. Some CD reviews generated more than one category of outcome. For example, an issuer may have been required to refile certain documents and also make certain changes on a prospective basis.

The largest review outcome was in the "no action required" category (53%). This category is made up primarily from the results of issue-oriented reviews on specific IFRS topics and Form 51-102F1 disclosures. These reviews generally did not result in issuing comment letters. Our main objective was to monitor overall quality of disclosure, observe trends and conduct research. Our learning from these findings will be incorporated into our CD review program going forward. These reviews included reviews of cash flow and operating segments.

The "prospective changes" category (26%) continues to represent a large portion of our outcomes. If material deficiencies or errors are identified, we expect issuers to correct them by restating and refiling the CD documents. However, when enhancements are required as a result of deficiencies identified, we request that amendments be made when the issuer next files CD documents. We aim to educate issuers by providing future filing comments. Some of the common examples of the "prospective changes" include enhancement of:

• financial statement disclosure for critical judgements, sources of estimation uncertainty disclosure and going concern disclosure, consistent with IFRS requirements;

• MD&A to comply with Form 51-102F1, including discussion of operations, liquidity and transactions between related parties;

• executive compensation disclosure to comply with Form 51-102F6 Statement of Executive Compensation, with emphasis on compensation discussion and analysis.

ISSUE-ORIENTED REVIEWS

An issue-oriented review focuses on a specific accounting, legal or regulatory issue that we believe warrants scrutiny. In fiscal 2013, a total of 72% of the reviews were issue-oriented reviews (as compared to 64% of the reviews in fiscal 2012).

Issue-Oriented reviews 2013

You will find below the results of certain issue-oriented reviews conducted during fiscal 2013 and the common deficiencies noted. Please refer to Appendix C for "Mining, Oil & Gas technical disclosure" common deficiencies.

- - - - - - - - - - - - - - - - - - - -

Cash flow disclosure

Issuers must comply with the disclosure obligations set out in IAS 7 Statement of cash flows, and sections 1.6 and 1.7 of Form 51-102F1 when addressing cash flow reporting in their financial statements and MD&As respectively. When conducting our reviews, we focused on cash flow presentation, liquidity and capital disclosure. Common deficiencies noted include:

• inadequate classification of cash flows between operating, investing or financing activities in the financial statements;

• incomplete or unclear discussion about the issuer's exposure to liquidity risks arising from financial instruments, such as short and long-term borrowing in the financial statements;

• incomplete or unclear discussion in MD&As of why certain non-GAAP cash flow financial measures provide useful information to investors;

• incomplete or unclear discussion in MD&As of the issuer's liquidity, its working capital requirements, its ability to generate sufficient amount of cash to maintain its capacity, meet its planned growth or to fund development activities; and

• incomplete or unclear discussion in MD&As on the status of debt facilities, the amount of facility drawn and remaining, details of covenants, and when there is material risk of default, how the issuer intends to remedy the default or address the risk.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

IFRS transition

During fiscal 2013 we reviewed the first IFRS interim financial reports of issuers with non-calendar year ends. When conducting our reviews, we focused on IFRS transition disclosures. Common deficiencies noted include:

• insufficient or unclear description of the effect of the transition; and

• omission of certain reconciliations with previous Canadian GAAP -- Part V.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Operating segments

Issuers must comply with the disclosure obligations set out in IFRS 8Operating segments, and section 1.2 of Form 51-102F1 when addressing operating segments in their financial statements and MD&As. Common deficiencies noted include:

• incomplete or omitted information about geographic areas and major customers in financial statements;

• failure to combine and disclose in an "all other segments" category information about other business activities and operating segments that are not reportable, i.e. disclosed separately from other reconciling items in the reconciliations required in financial statements;

• failure to provide restated comparative period segment data reflecting a change in reportable segments in financial statements; and

• incomplete analysis of operating segments that are reportable segments in MD&As.

- - - - - - - - - - - - - - - - - - - -

FULL REVIEWS

A full review is broad in scope and covers many types of disclosure. A full review covers the selected issuer's most recent annual and interim financial reports and MD&A filed before the start of the review. For all other CD disclosure documents, the review covers a period of approximately 12 to 15 month. In certain cases, the scope of the review may be extended in order to cover prior periods. The issuer's CD documents are monitored until the review is completed. A full review includes an issuer's technical disclosure (i.e. technical reports for oil and gas and mining issuers), annual information form, annual report, information circulars, press releases, material change reports, business acquisition reports, websites, certifying officers' certifications and material contracts.

In fiscal 2013, a total of 28% of the reviews were full reviews (as compared to 36% of the reviews in fiscal 2012).

COMMON DEFICIENCIES IDENTIFIED

Our full and issue-oriented reviews focus on identifying material deficiencies and potential areas for disclosure enhancements. To help issuers better understand their CD obligations, we have provided guidance and examples of common deficiencies in the following appendices:

Appendix A: Financial Statements Deficiencies

1. Judgements

2. Impairment of goodwill

3. Going concern

Appendix B: Management's Discussion and Analysis (MD&A) Deficiencies

1. Liquidity

2. Discussion of operations

3. Related party transactions

Appendix C: Other Regulatory Disclosure Deficiencies

1. Mineral projects

2. Oil and gas activities

3. Disclosure controls and procedures and internal control over financial reporting in venture issuers' MD&A

4. Executive compensation

This is not an exhaustive list of disclosure deficiencies noted in our reviews. We remind issuers that their CD record must comply with all relevant securities legislation and lengthy disclosure does not necessarily equal full compliance. Examples do not include all requirements that could apply to a particular issuer's situation.

Results by jurisdiction

The Alberta Securities Commission and the Autorité des marchés financiers publish reports summarizing the results of the CD review program in their jurisdictions. See the individual regulator's website for a copy of its report:

• www.albertasecurities.com

• www.lautorite.qc.ca

APPENDIX A

FINANCIAL STATEMENTS DEFICIENCIES

This Appendix provides some examples of deficient disclosure contrasted against more robust entity-specific disclosure for three areas of IFRS requirements. Many issuers could improve compliance in these areas.

1. Judgements

In accordance with paragraph 122 of IAS 1 Presentation of Financial Statements (IAS 1), an issuer shall disclose in the summary of significant accounting policies or other notes, the judgements, apart from those involving estimations, that management has made in the process of applying the entity's accounting policies and that have the most significant effect on the amounts recognised in the financial statements.

We found that the disclosure about judgements that have the most significant effect on the amounts recognised in the financial statements is generally deficient and boilerplate. We noted that some issuers did not disclose any information about judgements. In some instances, issuers included a note with a title referring to judgements and estimates in the financial statements, but the note only included information about estimates. In other instances, issuers listed the financial statements items involving judgements, but they did not disclose the judgements made.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Use of estimates and judgements

The preparation of financial statements in compliance with IFRS requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates are based on management's best knowledge of current events and actions that the Company may undertake in the future. Estimates and underlying assumptions are reviewed on an on-going basis.

Critical judgements in applying accounting policies that have the most significant effect on the amounts recognized in the financial statements include assessing when depletion of capitalized costs for mining properties begins.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

Judgements

In applying the Company's accounting policies, management used its judgement in areas which have the most significant effect on the amounts recognized in the consolidated financial statements, including:

Determining Production Stage of a Mine

The Company capitalizes costs incurred in exploration, evaluation and development as part of mining properties prior to a mine being capable of operating at levels intended by management. Depletion of capitalized costs for mining properties begins upon the mine entering into production stage, which requires significant judgement in its determination. Management considers various factors to determine when a mine is substantially complete and ready for its intended use. These factors include: 1) level of capital expenditures compared to construction cost estimates; 2) completion of a reasonable period of testing of major mine and plant components; 3) achievement of consistent operational results over a reasonable period of time; 4) achievement of planned production capacity for plant and mill; and 5) ability to sustain ongoing production. The Company determined that the ABC mine was capable of operating at levels intended by management and moved into production stage on March 1, 2013.

- - - - - - - - - - - - - - - - - - - -

2. Impairment of goodwill

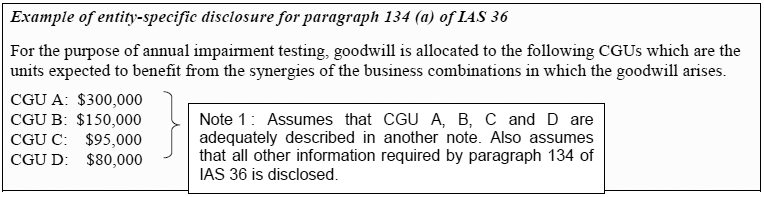

In accordance with paragraph 134 of IAS 36 Impairment of Assets (IAS 36), an issuer must disclose information on each cash-generating unit (CGU) or group of CGUs for which the carrying amount of goodwill or intangible assets with indefinite useful lives allocated to that CGU or group of CGUs is significant in comparison with the entity's total carrying amount of goodwill or intangible assets with indefinite useful lives. If the CGU or group of CGUs' recoverable amount is based on value in use, this information includes a description of each key assumption on which management has based its cash flow projections for the period covered by the most recent budgets/forecasts. Key assumptions are those to which the CGU or group of CGUs' recoverable amount is most sensitive.

Some issuers did not disclose all the information required by paragraph 134 of IAS 36.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Goodwill is tested at least annually for impairment. The Corporation performed its impairment test as at December 31, 2012. For the purpose of impairment testing, goodwill is tested for impairment at the CGU level. The recoverable amount of the CGUs is based on value in use. If the carrying value exceeds the recoverable amount, an impairment charge is recognized to the extent that the carrying value exceeds the recoverable amount.

The recoverable amount of all CGUs has been determined based on cash flow projections on financial budgets approved by management covering a five-year period. Cash flows beyond the five-year period are extrapolated using estimated growth rates of 2%.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure (continued)

The discount rates used are pre-tax and reflect specific risks relating to the relevant CGUs. The pre-tax discount rate used for the value in use calculation was 16%.

No impairment charge has arisen as a result of the review performed as at December 31, 2012. Reasonably possible changes in key assumptions would not cause the recoverable amount of CGUs to fall below the carrying value.

- - - - - - - - - - - - - - - - - - - -

In the above example, the issuer did not provide:

• the carrying amount of goodwill allocated to the CGU or group of CGUs for which the carrying amount of goodwill is significant in comparison with the issuer's total carrying amount of goodwill (Paragraph 134 (a) of IAS 36);

• a complete description, by CGU or group of CGUs, of each key assumption on which management has based its cash flow projections for the period covered by the most recent budgets/forecasts. Key assumptions are those to which the CGU or group of CGUs' recoverable amount is most sensitive (Paragraph 134 (d) (i) of IAS 36). Examples may include revenue growth or gross margin percentage assumptions; and

• a description of management's approach in determining the value (or values) assigned to each key assumption, whether these values reflect past experience or, if appropriate, are consistent with external sources of information, and, if not, how and why they differ from past experience or external sources of information (Paragraph 134 (d) (ii) of IAS 36). For example, if the gross margin percentage for a specific CGU or group of CGUs is higher in the cash flow projection than what has been experienced, it would be important for users to be alerted to this and to understand why.

3. Going concern

Under IAS 1, when management is aware of material uncertainties related to events or conditions that may cast significant doubt upon the issuer's ability to continue as a going concern, the issuer must disclose these uncertainties.

Under paragraph 19 of the Canadian Auditing Standards 570 Going Concern, if adequate disclosure is made in the financial statements, the auditor shall express an unmodified opinion and include an "Emphasis of Matter" paragraph in the auditor's report to highlight the existence of a material uncertainty relating to the event or condition that may cast significant doubt on the entity's ability to continue as a going concern and draw attention to the note in the financial statements that discloses the matters set out in this paragraph.

We sometimes see inconsistent information between the going concern disclosure provided in an issuer's financial statements and the going concern disclosure included in the auditor's report.

Some issuers provide indications of financial difficulty, sometimes under a going concern heading, without explicitly stating that the disclosed uncertainties may cast significant doubt upon the issuer's ability to continue as a going concern despite the fact that the auditor's report highlights the existence of a material uncertainty relating to the event or condition that may cast significant doubt on the issuer's ability to continue as a going concern.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Extract from the auditor's report

Emphasis of Matter paragraph

We draw attention to Note 2 to the financial statements that highlights the existence of a material uncertainty relating to the event or condition that may cast significant doubt on the entity's ability to continue as a going concern. Our opinion is not qualified in respect of this matter.

Extract from the financial statements

Note 2 -- Going concern assumption

At year-end the Company had minimal cash and a working capital deficiency. While the Company has prepared its financial statements on the going concern basis, it is dependent on its ability to obtain additional financing from related parties and external financing to sustain operations and fund its expenditures.

Management is actively pursuing such additional sources of financing, and while it has been successful in doing so in the past, there can be no assurance it will be able to do so in the future.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

Extract from the auditor's report

Emphasis of Matter paragraph

We draw attention to Note 2 to the financial statements that highlights the existence of a material uncertainty relating to the event or condition that may cast significant doubt on the entity's ability to continue as a going concern. Our opinion is not qualified in respect of this matter.

Extract from the financial statements

Note 2 -- Going concern assumption

The financial statements were prepared on a going concern basis. The going concern basis assumes that the Company will continue to operate in the foreseeable future and will be able to realize its assets and discharge its liabilities and commitments in the normal course of business.

For the year ended December 31, 2012, the Company had a net loss from operations of $3 million, a negative cash flow from operations of $2 million. As at year-end, the Company had a working capital deficiency of $1.5 million and cash on hand of $2 million.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Extract from the financial statements (continued)

The Company has a history of operating losses. In recent years, it had negative cash flows from operations and working capital deficiencies. The Company's credit facility contains certain financial covenants that are subject to periodic reviews. As part of its debt agreement, the Company must maintain a working capital ratio of at least 1:1. As at December 31, 2012, this ratio was 0.5:1. Given the breach, the lender has the right to demand full repayment at any time. As a result, the bank debt has been reclassified to short term liabilities resulting in a higher working capital deficiency. The Company is currently in negotiations with the lender to waive the covenant violations.

Whether and when the Company can attain profitability and positive cash flows is uncertain. These uncertainties cast significant doubt upon the Company's ability to continue as a going concern.

The Company will need to complete a short term financing to make the payment for the credit facility, raise sufficient working capital to maintain operations, reduce operating expenses and increase revenues. Subsequent to year end, the Company completed a private placement of $3 million to fund ongoing operations and to pay off the credit facility in the event the waiver cannot be obtained.

- - - - - - - - - - - - - - - - - - - -

We remind issuers, that when there are uncertainties that cast doubt on the issuer's ability to continue as going concern, the MD&A should also provide a discussion and analysis on how the issuer expects to resolve the uncertainty event or condition.

APPENDIX B

MANAGEMENT'S DISCUSSION AND ANALYSIS (MD&A) DEFICIENCIES

As in prior years, deficiencies were noted in the MD&A disclosure. As stated in Part 1(a) of Form 51-102F1 Management's Discussion and Analysis of National Instrument 51-102 Continuous disclosure obligations (Form 51-102F1), the MD&A should include balanced discussions of the issuer's financial performance and financial condition, including, without limitation, such considerations as liquidity and capital resources. The MD&A should help current and prospective investors to understand what the financial statements show and do not show. It should also discuss material information that may not be fully reflected in the financial statements.

There are three important areas of the MD&A where deficient disclosures were noted: 1) liquidity; 2) discussion of operations; and 3) related party transactions. For each area, we have provided examples of deficient disclosure contrasted against more robust entity-specific disclosure.

1. Liquidity

Many smaller issuers focus their resources on completing a project or on expanding their operations. In accordance with section 1.6 of Form 51-102F1, the MD&A should focus on the issuer's ability to generate sufficient liquidity in the short term and in the long term to fund development activities or to meet planned growth. Moreover, the MD&A should explain how an issuer will meet its obligations as they become due and how they will address working capital deficiencies. We often find issuers reproduce in their MD&A information that is readily available from the financial statements without ensuring compliance with section 1.6 of Form 51-102F1.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Liquidity

|

Year ended |

December 31, 2012 |

December 31, 2012 |

Difference |

|

|

$ |

$ |

$ |

|

Cash flows from operating activities |

(270,000) |

102,000 |

(372,000) |

|

|

|||

|

Cash flows from investing activities |

(350,000) |

(340,000) |

(10,000) |

|

|

|||

|

Cash flows from financing activities |

520,000 |

425,000 |

95,000 |

|

|

|||

|

Increase (decrease) of cash flows |

(100,000) |

187,000 |

(287,000) |

Operating activities

The cash flows used in operating activities totalled $270,000. For the same period last year, the cash flow from operating totalled $102,000.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Investing activities

The cash flows used in investing activities increased by $10,000.

Example of deficient disclosure (continued)

Financing activities

The cash flows from financing activities totalled $520,000. For the same period last year, the cash flows from financing totalled $425,000.

|

|

December 31, 2012 |

December 31, 2011 |

Increase (decrease in working capital) |

|

|

$ |

$ |

$ |

|

Cash |

51,000 |

151,000 |

(100,000) |

|

|

|||

|

Accounts receivable |

789,000 |

852,000 |

(63,000) |

|

|

|||

|

Inventory |

800,000 |

942,000 |

(142,000) |

|

|

|||

|

Prepaid expenses |

30,000 |

28,000 |

2,000 |

|

|

|||

|

Bank indebtedness |

350,000 |

0 |

(350,000) |

|

|

|||

|

Loan -- Investment tax credits |

120,000 |

0 |

(120,000) |

|

|

|||

|

Accounts payable |

1,035,000 |

877,000 |

(158,000) |

|

|

|||

|

Current portion of long term debt |

150,000 |

100,000 |

(50,000) |

|

|

|||

|

Total working capital |

15,000 |

996,000 |

(981,000) |

The company's working capital decreased by $981,000.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

At the end of fiscal 2012, the Company had $51,000 of cash on hand and working capital of $15,000.

Given the various projects the Company is handling in the short and medium terms, management still considers the current cash balance and forecast net cash flows from operating activities for the next 12 months to be below the $300,000 desirable for its planned business development activities.

The success of development projects depends greatly on the Company's ability to generate sufficient cash to meet its needs. In fiscal 2012, the Company renegotiated the terms of its financing agreement with its financial institution and obtained an operating line of credit of $500,000 to continue development of its X products distribution activities and to finance growth. As at the end of fiscal 2012, $150,000 was available on the line of credit. Also in 2012, the Company contracted new financing of $120,000, secured by investment tax credits, to continue research and development work on its Y project. This financing was used at the end of fiscal 2012.

Hence, as of the end of fiscal 2012, management was still considering various sources of financing available on the market to increase the Company's liquidity. At year end, management was negotiating a private placement of $500,000 that was completed after year end.

- - - - - - - - - - - - - - - - - - - -

2. Discussion of operations

An MD&A should explain what factors contributed to changes in an issuer's operations. Issuers often reproduce information from the statement of profit or loss and other comprehensive income in their MD&A, without explaining what caused the changes.

In accordance with section 1.4 of Form 51-102F1, the revenue analysis included in an issuer's MD&A should discuss any change caused by selling prices, volume or quantity of goods or services being sold, or the introduction of new products or services. It is useful to investors if the issuer quantifies each of these elements. If other elements affected revenue, such as the introduction of a new competitor, the issuer's MD&A should also address these factors. If an issuer's financial statements present information from more than one reportable segment, the issuer must discuss the results of each segment in its MD&A.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

The Company reported revenue of $7,666,000 for the year ended December 31, 2012, compared with $7,098,000 a year earlier, an increase of 8%. The growth is mainly due to the sales of L products.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

During fiscal 2012, the Company's sales increased by 8%. The Company undertook a new activity, namely the distribution of L product in the Canadian manufacturing sector. As at year end, because of a delay in the manufacturing of L products, this activity had not yet reached the level that management had anticipated. The sales of L products increased sales by 7%.

Since 30% of sales are made in US dollars, the depreciation of the Canadian dollar had a positive impact on sales. This impact was a 3% increase in sales.

Despite the positive effect of the introduction of L product and of the exchange rate, the arrival of a new competitor forced the Company to decrease its sale price on product V. With this decrease, the Company was able to maintain the sale volume of product V. Due to the quality reputation of product V, management believes that no other decrease of the sale price will be necessary to maintain the sale volume of product V in the future. The decrease in the sale price caused a 2% decrease in sales.

- - - - - - - - - - - - - - - - - - - -

3. Related party transactions

Under section 1.9 of Form 51-102F1, issuers are required to identify the related person or entities, to discuss the business purpose of the transaction, to describe the measurement basis used and to discuss ongoing commitments resulting from the transaction. It is common for issuers to reproduce the related party transactions note provided in their financial statements or to simply refer to that note. However, IAS 24 Related Party Disclosures does not require the same level of information as section 1.9 of Form 51-102F1.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

The Company paid $150,000 to a company controlled by a director for consulting services.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

During the year, the Company paid $150,000 to Orange Inc., which is controlled by Mr. Smith, Chief Executive Officer and director of the Company. The $150,000 fee was paid for programming services relating to the implementation of new inventory software. The fee is based on what Orange Inc. usually charges its regular clients less a 10% discount. The Company expects to continue to use Orange Inc.'s programming services until the implementation of the new inventory software is completed.

- - - - - - - - - - - - - - - - - - - -

APPENDIX C

OTHER REGULATORY DISCLOSURE DEFICIENCIES

CSA Staff assess issuer compliance with securities laws. Our objective is to promote clear and informative disclosure that will allow investors to make informed investment decisions. The areas where compliance issues persist include disclosure about: 1) mineral projects; 2) oil and gas activities; 3) disclosure controls and procedures and internal control over financial reporting in venture issuers' MD&A; and 4) executive compensation.

1. Mineral projects

Issuers engaged in mining activities have to comply with the requirements set out in National Instrument 43-101Standards of Disclosure for Mineral Projects. Common deficiencies noted include:

• incomplete or inadequate disclosure of preliminary economic assessments, mineral resources and mineral reserves;

• non-compliant certificates and consents of qualified persons for technical reports;

• incomplete or inadequate disclosure of historical estimates and exploration targets; and

• name of the qualified person omitted in documents containing scientific and technical information.

2. Oil and gas activities

Issuers engaged in oil and gas activities must comply with the requirements set out in National Instrument 51-101Standards of Disclosure for Oil and Gas Activities (NI 51-101). Common deficiencies noted include:

• failure to adapt to current requirements of Form 51-101F1 Statement of Reserves Data and Other Oil and Gas Information (Form 51-101F1), Form 51-101F2 Report on Reserves Data by Independent Qualified Reserves Evaluator or Auditor, and Form 51-101F3 Report of Management and Directors on Oil and Gas Disclosure;

• non-compliance with sections 5.9, 5.16 and 5.17 of NI 51-101 concerning disclosure of resources other than reserves, classification to the most specific category of resources, summation across resource categories and disclosure of high case estimates of resources;

• inadequate disclosure of the meaning of, and method of calculating, the metrics used by issuers to measure and compare oil and gas activities;

• deficiencies in reserves reconciliation disclosure, including, for example, opening balances for the reserves reconciliation required under item 4.1 of Form 51-101F1 that do not agree with the prior year's closing balances; and

• insufficient and boilerplate disclosure of significant factors and uncertainties as per items 5.2 and 6.2.1 of Form 51-101F1, regarding the issuer's proved and probable undeveloped reserves and plans for developing those reserves under item 5.1 of Form 51-101F1.

3. Disclosure controls and procedures (DC&P) and internal control over financial reporting (ICFR) in venture issuers' MD&A

Some venture issuers discussed DC&P or ICFR in their MD&As, but did not include cautionary language. In accordance with section 15.3 of the Companion Policy to National Instrument 52-109Certification of Disclosure in Issuers' Annual and Interim Filings (52-109 CP), if a venture issuer and its certifying officers file Forms 52-109FV1 or 52-109FV2 (Venture Issuers Basic Certificates) and choose to discuss the design or operation of one or more components of their ICFR and DC&P in the MD&A or other regulatory filings, they should also consider disclosing in the same document that:

(a) the venture issuer is not required to certify the design and evaluation of its DC&P and ICFR and has not completed such an evaluation; and

(b) inherent limitations on the ability of the certifying officers to design and implement on a cost-effective basis DC&P and ICFR for the issuer may result in additional risks to the quality, reliability, transparency and timeliness of interim and annual filings and other reports provided under securities legislation.

Venture Issuers Basic Certificates provided in National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109) include a "Note to Reader" that the certifying officers are not making any representations relating to the establishment and maintenance of:

i) controls and other procedures designed to provide reasonable assurance that information required to be disclosed by the issuer in its annual filings, interim filings or other reports filed or submitted under securities legislation is recorded, processed, summarized and reported within the time periods specified in securities legislation; and

ii) a process to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with the issuer's GAAP.

In the following example, the venture issuer used Venture Issuers Basic Certificates.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Disclosure controls and procedures

The Company's Chief Executive Officer (CEO) and the Chief Financial Officer (CFO) are responsible for establishing and maintaining the Company's disclosure controls and procedures. These controls and procedures have been evaluated as at December 31, 2012 and have been determined to be effective.

Internal controls over financial reporting

The Company's CEO and the CFO are responsible for establishing and maintaining the Company's internal controls over financial reporting.

The internal control system pertaining to financial reporting gives a reasonable assurance as to the reliability of the financial information reported and the preparation of the financial statements in accordance with IFRS.

- - - - - - - - - - - - - - - - - - - -

In the above example, to avoid confusion, it would have been more appropriate for the venture issuer to use Forms 52-109F1 or 52-109F2 (Full Certificates) as allowed by subsections 4.2(2) and 5.2(2) of NI 52-109. However, if the venture issuer does use Full Certificates, it must use a control framework for the design of ICFR, as required by subsection 3.4(2) of NI 52-109. The guidance in Parts 6 and 7 of 52-109 CP regarding establishing and evaluating DC&P and ICFR would also apply.

If in the above example, the venture issuer intends to use only a Venture Issuers Basic Certificate then it could have discussed only one or a few discrete components of DC&P or ICFR. In addition, the MD&A disclosure should be clear and should not include assertions about the design or evaluation of all aspects of DC&P or ICFR, and should not include any conclusions on the effectiveness of DC&P or ICFR. In addition, the cautionary language set out in section 15.3 of 52-109 CP would ensure transparent disclosure.

For additional guidance on NI 52-109, please see CSA Staff Notice 52-325 Certification Compliance Review and CSA Staff Notice 52-327Certification Compliance Update.

4. Executive compensation

Issuers must provide the executive compensation disclosure for the periods set out in, and in accordance with Form 51-102F6 Statement of Executive Compensation of National Instrument 51-102 Continuous disclosure obligations. This disclosure can be included in an information circular, an annual information form (AIF) or as a stand-alone document.

The executive compensation disclosure must be filed not later than 140 days after the end of the issuer's most recently completed financial year pursuant to subsection 11.6(3) of National Instrument 51-102 Continuous Disclosure Obligations. We noted that some issuers failed to file the executive compensation disclosure within 140 days. We remind issuers, that if they are not planning to send an information circular to their securityholders within 140 days after the end of their most recently completed financial year, they must include the executive compensation disclosure in either the AIF or as a stand-alone document, and file it within the 140 days.

APPENDIX D

CATEGORIES OF OUTCOMES

Enforcement referral/ Default list/ Cease trade order

If the issuer has critical CD deficiencies, we may add the issuer to our default list, issue a cease trade order and/or refer the issuer to Enforcement.

Refiling

The issuer must amend and refile certain CD documents.

Prospective Changes

The issuer is informed that certain changes or enhancements are required in its next filing as a result of deficiencies identified.

Education and Awareness

The issuer receives a proactive letter alerting it to certain disclosure enhancements that should be considered in its next filing.

No action required

The issuer does not need to make any changes or additional filings. The issuer could have been selected in order to monitor overall quality disclosure of a specific topic, observe trends and conduct research.

Questions

Please refer your questions to any of the following:

{1}In this notice "issuers" means those reporting issuers contemplated in National Instrument 51-102 Continuous Disclosure Obligations.